Family walking on highway, five children. Started from Idabel, bound for Krebs. In 1936 the father farmed on thirds and fourths at Eagleton, McCurtain County. Was taken sick with pneumonia and lost farm. Was refused relief in county of 15 years' residence because of temporary residence elsewhere. Pittsburg County, Oklahoma

Ilargi: The following is a conversation between Stoneleigh and Euan Mearns of TOD Europe.

Euan Mearns: At the ASPO conference in Denver, October 2009, I had the good fortune to meet Stoneleigh, former editor of The Oil Drum Canada, who left the TOD crew with colleague Ilargi to set up The Automatic Earth where they publish stories, news and analysis of the unfolding financial crisis.

I spent a couple of days chatting with Stoneleigh where she recounted her rather gloomy prospects for the immediate future of the global economy. The following interview is a summary of her analysis of the unfolding situation. Note that in a departure from convention my questions are set in "blockquotes" to distinguish these from Stoneleigh's responses.

Euan Mearns: Stoneleigh, the world economy seems to be suffering from two great structural woes at present, namely stubbornly high energy prices that are linked to demand that is persistently ahead of the supply curve, and a level of debt that has destabilized the global finance and banking systems.

Can you explain for us the scale and structure of this debt and to what extent write-downs and quantitative easing (QE) have solved this problem?

Stoneleigh: Firstly, I would say that the energy prices that currently seem stubbornly high should fall substantially as the speculative premium evaporates and demand falls on a resumption of the credit crunch. The sucker rally that has spawned all the talk of green shoots is essentially over in my opinion.

The result should be a reversal of a number of trends that depend on the ebb and flow of liquidity - we should see stock markets and commodity prices fall, a significant resurgence in the US dollar and a large contraction of credit. The scale of the reversal should be substantial, as should its effects on energy demand. Demand is not what one wants, but what one is ready, willing and able to pay for, and in a severe credit crunch the capacity to pay for supplies of most things will be severely reduced.

As demand falls, and with it prices, investment in the energy sector is likely to dry up. Many projects will be uneconomic at much lower prices, meaning that the projects which might have cushioned the downslope of Hubbert’s curve (and the much steeper net energy curve), are unlikely to be developed. In this way a demand collapse sets the stage for a supply collapse that could place a hard ceiling on any prospect of economic recovery. That is a recipe for extremely high energy prices in the future.

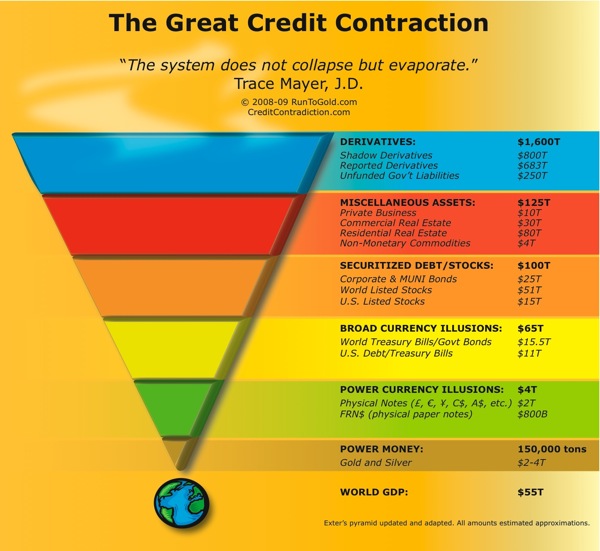

Secondly, our vulnerability to the consequences of debt is extremely high at the moment. The scale of that debt is staggeringly large. The global credit hyper-expansion has been decades in the making and is now significantly larger than notable events of the past such as the South Sea Bubble of the 1720s and the Tulip Bubble of the 1630s. It dwarfs the excesses that led to the Great Depression.

Credit bubbles are inherently self-limiting, proceeding until the debt they generate can no longer be supported. We have already passed that point and we are now two years into a contraction phase that is about to accelerate. As the aftermath of a credit bubble is typically proportional to the scale of the excesses that preceded it, we should be in for the largest economic contraction for at least several hundred years, and it will be global.

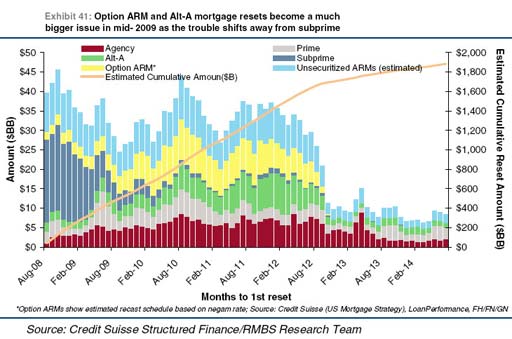

Real estate, which is a major focus of the mania, should do particularly badly in the coming years (in fact the coming decades or longer). There is still so much deleveraging ahead, and so many danger signals, such as the scale of the coming interest resets on US mortgages between now and 2012 (below). While the subprime resets are ending, Alt A and Option ARMs are just beginning.

There will be a very significant undershoot of historically average values, as there always is following a mania (much more than the Case-Shiller projection below suggests). In my opinion, housing prices are likely to fall at least 90% on average. For those who own property on margin, this will be a disaster.

For evidence that this crisis is indeed global, look, for instance, at European housing bubbles, which were worse than in the US.

Unlike inflation, which divides the underlying real wealth pie into smaller and smaller pieces, credit expansion creates multiple and mutually exclusive claims to the same pieces of pie. Once a credit expansion reaches its maximum extent, and contraction begins, these excess claims begin to be extinguished.

Unfortunately, the leverage is such that there are probably over a hundred claims to each piece of pie. While contraction begins slowly, as is the nature of positive feedback loops, it picks up momentum until a cascade point is reached, whereupon one can expect the excess claims to be extinguished in a rapid and chaotic process. This amounts to a rapid collapse in the supply of money and credit relative to available goods and services, which is the definition of deflation.

The scale of the problem has been temporarily concealed by a market rally and the shovelling of tens of trillions of dollars of taxpayer’s money into a giant black hole of credit destruction. This has done nothing to reignite lending, but the temporary (and entirely irrational) resurgence of confidence has restored a measure of liquidity. As that confidence evaporates with the end of the rally, that liquidity will also disappear

Banks hold extremely large amounts of illiquid ‘assets’ which are currently marked-to-make-believe. So long as large-scale price discovery events can be avoided, this fiction can continue. Unfortunately, a large-scale loss of confidence is exactly the kind of circumstance that is likely to result in a fire-sale of distressed assets. The structure of the credit default swap component of the derivatives market makes this very much more likely.

The CDS market allowed large bets to be placed on certain prices falling, and by entities which did not have to own those assets. This creates a perverse incentive for some parties to cause others to fail for profit (akin to me being able to take out fire insurance on your house and thereby give me an incentive to burn it down).

An added complication is the extreme degree of counterparty risk that resulted from a complete lack of capital adequacy regulation. Many parties with winning bets will not be able to collect, so they may cause financial mayhem for nothing. The CDS market is worth some $62 trillion, and a meltdown is very likely in my opinion.

A large-scale mark-to-market event of banks illiquid ‘assets’ would reprice entire asset classes across the board, probably at pennies on the dollar. This would amount to a very rapid destruction of staggering amounts of putative value. This is the essence of deflation.

Euan Mearns: I have for a long time argued and believed that there are so many interests vested in protecting our current system that national governments, the IMF and institutions working together would keep the market flooded with liquidity in order to ward off the threat of deflation.

In fact, it seems that a prolonged period of inflation is the only way to diminish our debts. I sensed at ASPO International in Denver that this was the majority view. Do you agree that inflation is the most likely near term outcome of current monetary policy?

Stoneleigh: Absolutely not. I agree that this is the consensus opinion, but I see it as fundamentally mistaken. The debt monetization that is going on has done nothing to increase the supply of money and credit relative to available goods and services, which is the definition of inflation.

Credit contraction dwarfs debt monetization, leaving us in a state of net contraction, even though we have just experienced a large rally lasting months, which should have been the most favourable condition for reigniting lending if such a thing were in fact possible. I would argue that it is simply not possible and that deflation is inevitable.

Credit bubbles always end this way, with the mass extinguishing of the excess claims debt represents. They are essentially Ponzi schemes, crucially dependent on the continued buy-in of new entrants. Globalized finance brought a flood of new entrants following the liberalization of the early 1980s, but there are now no more new sources of wealth to tap.

Deregulation allowed the reckless to gamble away virtually everything, including bank deposits and pension funds. Globalized finance has created a giant Enron, which while appearing robust is actually almost completely hollowed out. Such structures implode, often without much notice.

In my opinion, deflationary deleveraging will continue until the (small amount of) remaining debt is acceptably collateralized to the (few) remaining creditors. Until that point, there can be no lasting return of the confidence required to rebuild shattered credit markets.

Deflation is ultimately psychological. Without trust we will see hoarding of the cash which will be very scarce in the absence of the credit that currently comprises the vast majority of the effective money supply. The combination of scarce cash and a very low velocity of money will be toxic.

Money is the lubricant in the economic engine and without enough of it that engine will seize up as it did in the 1930s, when farmers dumped milk they couldn’t sell into ditches while others were starving for want of the money to buy food. There was plenty of everything except money, and without money, one cannot connect buyers and sellers.

Potential buyers will have no purchasing power as they will have lost access to credit and their ability to earn an income will be hit by spiking unemployment. Those who still have jobs will find that they have no bargaining power and there is therefore no wage support.

Sellers and producers will have no market and will themselves lose the means to purchase supplies or raw materials for the things they would like to produce.

If conditions remain frozen for any length of time, they will go out of business. The deeper the collapse, the more protracted the trough and the more difficult the eventual recovery.

I would argue that we have no need to fear inflation until we have reached a trough - until the deleveraging impulse is spent. We can expect to spend a long time in the liquidity trap, where real interest rates will be much higher than nominal rates, leaving central bankers “pushing on a string”.

Euan Mearns: Some would argue that faced with the unimaginable specter of deflation that governments will seize control of interest rates from the bond market. Why do you think this may not happen?

Stoneleigh: The bond market is far more powerful than governments at this point. While the international debt financing model remains, the bond market will retain its power to prevent money printing. Even though governments are not succeeding in increasing the effective money supply for reasons already discussed, they are nevertheless increasing systemic risk with their activities.

This is a recipe for very much higher interest rates as a risk premium. Governments do not set interest rates, they decide what rate to defend, but if that rate is substantially different from what the bond market requires, then defending it would be ruinous.

I think we are headed (not imminently but eventually) for a bond market dislocation, with nominal interest rates on government debt spiking into the double digits. This will amount to hitting the emergency stop button on the economy, especially since real interest rates will be substantially higher (the nominal rate minus negative inflation).

I am in fact expecting interest rates on private debt to rise before we see problems in the market for government debt, as the latter should benefit substantially in the shorter term from a flight to safety. The risk premium on private debt is already rising, which is a serious danger signal for such thoroughly indebted societies as we see in the developed world.

Euan Mearns: But stock markets are booming again, several OECD economies are emerging from recession, unemployment has stabilized, there are green shoots everywhere. Surely the current QE strategy is working?

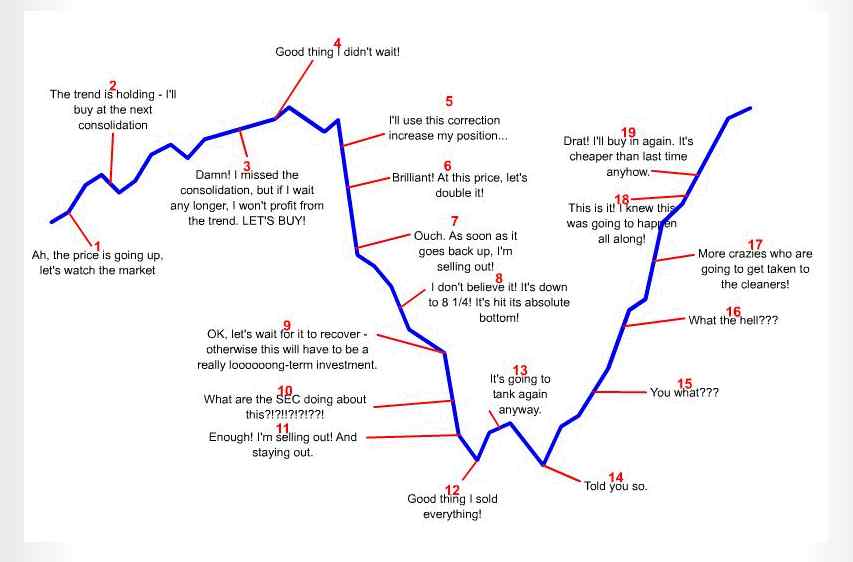

Stoneleigh: The green shoots are gangrenous. Some of the largest market rallies on record happened during the course of the Great Depression, as depressions are associated with very high volatility. Look for instance at the great sucker rally of 1930. There are always rallies of all different sizes in any bear market, just as there are pullbacks of all sizes in bull markets. No market ever moves in only one direction.

People tend to extrapolate recent trends forward, but this amounts to stepping on the gas while looking only in the rearview mirror. This is one reason why major trend changes are so rarely anticipated. Another is that the prevailing view of markets is fundamentally wrong. There is no perfect information, perfect competition, stabilizing negative feedback, rational utility maximization or efficient markets.

Markets are irrational, driven by swings of optimism and pessimism, or greed and fear, in an endless tug of war, and largely in an information vacuum. Investors chase momentum by jumping on passing bandwagons, hence demand for financial assets increases when prices are rising and falls when prices are falling, in classic positive feedback loops.

We have just lived through a period of several months when greed and complacency were in the ascendancy, but that trend is about to reverse in my opinion. Looking at markets as constructs of human herding behaviour allows them to be probabilistically predictable, permitting the forecasting of trend changes. For anyone who is interested in pursuing this idea further, I suggest looking into Bob Prechter’s socionomics - a fascinating subject which delves into the many effects of changes in collective mood.

For instance, as pessimism deepens, driving economic contraction, one would expect to see many manifestations of collective anger and mistrust. As this progresses it is likely to lead to xenophobia and a blame-game, with skillful manipulators (such as the fascist BNP leader Nick Griffin in the UK) poised to direct the anger of the herd towards their own chosen targets.

The potential for serious social fragmentation is very high when expectations have been dashed and there is not enough to go around. Having lived through a very long period of manic optimism and increasing inclusion, we in the developed world are not used to expressions of the dark side of human nature, except for entertainment purposes in popular television programmes. It will come as a considerable shock.

Euan Mearns: Would you care to give your opinion on where the Dow Jones Industrial Average is headed in the near (1 year) and medium terms (2 to 5 years)?

Stoneleigh: I think the market will fall hard (intervening short rallies notwithstanding) for perhaps 18 months. This was the length of the first leg down (October 2007-March 2009) and so represents a reasonable first guess at how long the next leg at the same degree of trend might last.

I think we will see falls of thousands of points in a series of cascades. I don’t see the markets reaching a lasting bottom until probably the middle of the next decade, and even then I don’t expect it to be a final bottom. This has been the largest credit bubble in history, and the aftermath of a major bubble always undershoots where it began before any kind of recovery begins.

The aftermath of the last major mania - the South Sea Bubble in the 1720s - lasted decades and culminated in a series of revolutions. We are still relatively near the beginning of our own crisis, but already it compares with the Great Depression.

Euan Mearns: How do you see the US$, gold and oil trading in the same time frame?

Stoneleigh: I think almost all assets will fall as price support is knocked out from underneath them, but the dollar should rise initially on a flight to safety. Scarce cash will be king for a long time, and the value of one’s currency relative to available goods and services domestically will matter much more for most people than its value relative to other currencies internationally.

In a deflationary scenario, prices fall, but purchasing power typically falls even faster, meaning that everything becomes less affordable despite the lower nominal prices. Prices in real terms, adjusted for changes in the supply of money and credit, are what matter.

In a world where almost everything is becoming rapidly less affordable, the essentials will be the least affordable of all, as a much larger percentage of a much smaller money supply will be chasing them. This will confer relative price support.

Although we could initially see a large glut in energy supply as demand falls off a cliff, this is likely to lead to supply collapse as investment dries up, hence I expect energy prices to bottom early in this depression.

Both financial and physical risks to energy exploration are likely to increase substantially in a destabilized and capital constrained world, and even maintaining existing assets could become very difficult. This is a recipe for much greater state involvement in ownership and exploitation of (probably deteriorating) energy assets, with increasing conflict over those assets as supply gets dramatically tighter with lack of investment.

As for gold, I expect it to fall initially as people sell not what they would like to, but what they can, in order to raise the cash they need for living expenses and debt servicing. Owning gold is likely to become illegal again (as it did in the Great Depression) in my opinion.

This wouldn’t necessarily stop you owning it, but would stop you trading it (at least without taking major risks) for other things you might need. Owning gold now therefore only makes sense if one is confident of being able to sit on it for a very long time, as it will hold its value over the long term as it has for thousands of years.

Euan Mearns: What will be the consequences for unemployment levels and services provided by government?

Stoneleigh: Unemployment will go through the roof as the prospects for selling most goods and services decline dramatically. In the developed world we are nations of middle men - generally service economies where we make a living figuratively taking in each other’s laundry.

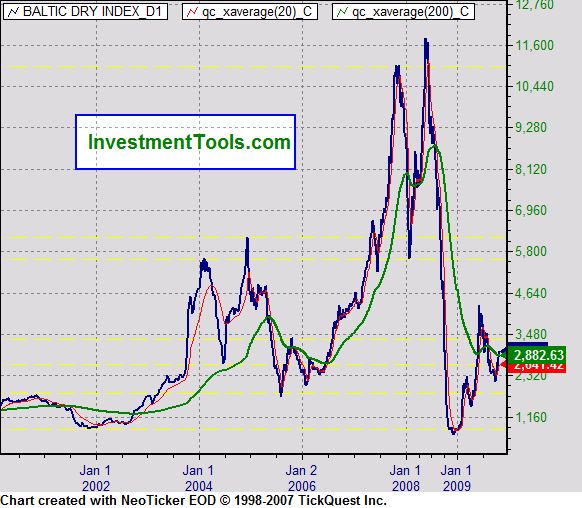

Most of us produce relatively little. Even those who do will find almost no market for their exports, and those who could find buyers may not be able to send shipments as credit contraction prevents shippers from getting the letters of credit they need to ship goods. A glance at what has happened to the Baltic Dry Index (below) indicates the difficulties already facing shipping companies.

Unfortunately middlemen are almost completely expendable, and the services of others are likely to become unaffordable for the majority very quickly. While there will be a huge surplus of labour, and the few who retain purchasing power will be able to hire anyone they want for very little, most people will have to do everything for themselves, as poor people have done throughout history and as most of the population of the world does now.

Not only will we lose access to the paid labour of others, but we will lose our virtual energy slaves as well. This will represent an enormous fall in the standard of living for the vast majority.

Whereas inflation can conceal a fall in purchasing power, so that people may not even realize it is happening, deflation brutally exposes it. Wages would have to fall just to keep purchasing power the same, but keeping it the same will not be an option for cash-strapped employers. In addition, with a large surplus of labour, workers will have no bargaining power.

This is a recipe for exploitation the like of which we have not seen for a very long time, but in the intervening adjustment period it is likely to lead first to war in the labour markets.

I would expect general strikes and a breakdown in the reliability of centralized services such as healthcare, education, power systems, water treatment, garbage (and snow) removal etc. This will be exacerbated by plunging tax revenues for all levels of government, which governments will try to compensate for by raising taxes, on anyone still capable of paying, to punitive levels. We would thus expect rapidly deteriorating services at much higher cost.

Many people are at risk of being eventually priced out of the market for goods and services, and particularly the essential ones, entirely.

In my opinion, we stand on the brink of truly tragic circumstances.

Euan Mearns: End note:

The day before the ASPO conference began in Denver, Stoneleigh, Rembrandt Koppelaar and myself took a drive into the Rocky Mountains National Park providing the opportunity to discuss and reflect upon the current global situation. As the week unfolded I realised that I was in denial about the gravity of the global financial situation. In what has become a situation of complexity that is beyond the ken of most folks, I find it simpler to break this down into smaller components that I can relate to.

In the UK, we have an escalating burden of government debt that we can unlikely ever repay. Unemployment is rising, tax receipts are plunging whilst expenditure on social security, health and the elderly go through the roof. We have been living way beyond our means, which with the peaking of UK oil and gas have suddenly become more meagre.

We have an election in May 2010. The new government will want to raise taxes and cut public spending. The current reversal in global growth is sending energy prices higher. Higher unemployment, higher taxes, higher energy prices and reduced public services are a toxic mixture for an ailing economy. If the bond market decides to price in the risk premium for escalating debt it will be game over. The questions are if and when? Figure 12 (Fed Follows the Market) is one of the more interesting for me.

That's me (Euan) on the left and Rembrandt Koppelaar on the right, contemplating our future after a most enlightening, if not very cold day in the Rocky Mountains. Photographer - Stoneleigh.

Ilargi: The Automatic Earth’s Fall Fund Drive (see the left hand column) is going well, and we owe heartfelt thanks to all of you who have donated. That said, in order to execute what we think would be the appropriate and logical next steps for us, more is needed, and quite a bit of it actually.

There are many thousands of people who read us every single day, and if everyone of them would donate just a dime for every time they read us we'd be doing just fine. But obviously, most never will.

We would love to be able to expand on what we do, to involve more people, more opinions, a more diverse view from more places in the world. And that is unfortunately not possible right now. Along the same lines, we would like for Stoneleigh to be much more involved at TAE. Not happening. On a happy note, our brand-new Twitter and Facebook presences are directed by our good friend VK, all the way from Nairobi, Kenya, the first time we’ve been able -and willing- to expand and relinquish control at least a little.

The Automatic Earth will be busier than ever as the real economy deteriorates in the months to come and things come to a head. Inevitably that will take more from us, and we hope you will do more as well.

Again for those among you who have donated to us -and many have in the past 3 weeks-, and those who will do so in the days and weeks and months to come, please know we are deeply grateful for, and humbled by, the confidence you have in us.