"Oil off the coast of Alabama"

Ilargi: President Obama said during the G-20 meeting in Toronto, where he was told to take a hike by European leaders, that both he and British prime minister David Cameron

"... are aiming at the same direction, which is long-term sustainable growth that puts people to work..."Somewhat curious, since his Vice President, Joe Biden, said a few days ago that

"...there's no possibility to restore 8 million jobs lost in the Great Recession."Looks a lot as if the nonsense now starts to contradict itself. Perhaps we shouldn't expect anything else.

Biden then added that there is

"...no way to regenerate $3 trillion that was lost. Not misplaced, lost."Don’t know what the Pennsylvania Avenue spin team thinks of Biden's remarks, but they do sound just about right to me, and a lot less hollow than Obama's empty fluff. Biden made me think of Springsteen's My Hometown (see video below), which has this verse:

Now main street's whitewashed windows and vacant stores

Seems like there ain't nobody wants to come down here no more

They're closing down the textile mill across the railroad tracks

Foreman says these jobs are going boys and they ain’t coming back

To your hometown, your hometown, your hometown

That sounds to me like a remarkably accurate portrait of much of America in a few years time. And Britain. And the rest of Europe.

The talk in the press has shifted towards debt, debt and more debt. And austerity. Whether Obama and the rest of the Keynes religion like it or not.

Ambrose Evans-Pritchard writes about an RBS note to its clients that warns of money printing by Bernanke. He says:

"America is one twist shy of a debt-deflation trap."Ambrose is right there. But he's dead wrong in his subsequent remarks:

"There is no doubt that the Fed has the tools to stop this".Oh, believe me, Ambrose, there's plenty doubt.

"Sufficient injections of money will ultimately always reverse a deflation," said Bernanke.Bernanke may say what he wants, but that doesn't make him right. We are in the beginning phase of a debt deflation. And if you want to talk about ultimately, then I’ll give you this one: ultimately debt cannot be repaid with more debt. Haven't the past two years of failing policies taught these people anything? The Fed balance sheet stands at record highs, and bloating it even more will solve the problems? What is it with these folks? It's not as if Ambrose doesn't have the data:

"The ECRI leading indicator produced by the Economic Cycle Research Institute plummeted yet again last week to -6.9, pointing to contraction in the US by the end of the year. It is dropping faster that at any time in the post-War era."No, the debt deflation must and will run its course, and Bernanke is devastatingly powerless to do anything about it. Not that he will ever admit it, even if he knew. But it's like having your local weatherman believe he controls the climate.

The latest data from the CPB Netherlands Bureau shows that world trade slid 1.7% in May, with the biggest fall in Asia. The Baltic Dry Index measuring freight rates on bulk goods has dropped 40% in a month."

$2,5 trillion hasn't done the trick, and neither will $5 trillion. Money velocity is way down and so is M3 broad money supply. How would Bernanke turn that around? The money simply isn't going anywhere. Except into a deep dark void. It's disappearing faster than Bernanke can print.

Once the deflation has run its ugly course, and it will be horrendous, printing presses may cause inflation, and given the level of ass-clowniness among economists it's highly likely that they’ll pick such a course. They've never seen a crisis they couldn't make worse. But I’ll bet you ten to one that by then Bernanke won't be in office anymore.

I’m going to post an article I happenstanced upon today sort of like an extra intro. I don't often do that, but this piece by Texan journalist Richard Parker struck a special chord. And since it brought Joe Bageant to mind, and Joe just posted a new piece, I’ll close today’s TAE with that.

But first, for those of you who haven't seen it yet, once more the wonderful video from CaptainSheeple, "A Tribute to the Automatic Earth".

Richard Parker: Recession as big as Texas pummels rural parts of America

Wimberley, Texas: The grass in the pasture stands tall. Throughout the spring, bluebonnets, Indian paint brushes and black-eyed Susans waved from the roadside. The Blanco River runs clear and full now, and the tourists return to the town square. A wet winter and cold spring have broken the grip of a two-year drought in Texas. But this plenty camouflages a drought of another sort: the economic one. Texas was slow to be swept up by the Great Recession. But now its pain has come home to big cities and small towns, as the lagging effects of the recession batter the ranchers, storekeepers and families who all withstood — until now.

While Washington's fury is directed toward the Gulf oil pill, it has largely lost sight of the recession. Yet Congress continues to weigh financial reform, and it would do well to remember the human cost of the Great Recession, triggered by the titans of Wall Street but borne heavily by everyday people. Since the crisis began and through the first quarter of this year, more than $2 trillion in mutual funds have been wiped out, 4.5 million homes have gone into foreclosure and 6.8 million jobs have been lost. With its art, eclectic character and natural beauty ours is one of the best little towns in the nation to visit; it says so right in the pages of The New York Times and Travel Holiday Magazine.

But for those of us who live here, a quiet crisis whispers of impending poverty. A merchant confides he can't take another year like the last two. A Mexican stonemason tells me that a single project tided his family through winter. A Realtor relays that all over town, people who never took a mortgage they couldn't afford are looking to give up, sell out and move on. The alternative is tallied and cataloged at the stately 102-year old, brick-and-limestone county courthouse over in San Marcos. Jack Hays, for whom this county was named, was a living legend for his exploits as a Texas Ranger, namely for fighting the Comanche.

Today, people are losing their homes not to raiding parties but to banks. There were 157 up for auction in April alone. For 15 withering months there have been 100 or more, according to the San Marcos Daily Record. It cites George Roddy, whose company dutifully counts all of them: "This foreclosure storm is far from over." The list carries the names of familiar ranches, springs and creeks. Yet the tale of Hays County is, sadly, more emblematic than unique in the vast landscape that stretches westward beyond the Hudson and the Potomac. Up in Austin, $6.5 billion in real estate value has been wiped out as if by a tornado. The resultant cuts in money for teachers, cops and services in the city are likely just around the corner.

In Austin and elsewhere, the conservative cultural boosterism of Texas initially downplayed the recession. Heir to George W. Bush's original political office and many of his finest traditions, Republican Gov. Rick Perry quipped of the recession in 2009, "We're in one?" It was his so-far-overlooked Katrina moment as time proved that bravado as prematurely false as that of his predecessor. "Texas has been hit much harder by the 2008-09 recession than previous ones," according to the Federal Reserve Bank of Dallas. Starting with a 6.1 percent unemployment rate at the beginning of the crisis, the job market fell throughout last year to end 2009 at an 8.2 percent unemployment rate. This year, manufacturing orders picked up, but the job creation rate stood stubbornly at zero in the first quarter.

Today in Texas, one in five people struggle to feed themselves and one in five children live in poverty, according to the Center for Public Policy Priorities in Austin, founded by Benedictine nuns. Perhaps Perry's economic prowess will trail him out of the state like a coyote when he seeks the presidency. However, this is not a Texas story but an American one, told in fiscal crises that stretch from California to Illinois, from Alabama to New York. It is in Washington where the Great Recession will be justly dealt with — or not. Realistically, after all, Congress and the regulators have assiduously polished their reputations as hand-maidens of the banks at least since the repeal of Glass-Steagall in 1999.

It doesn't take an expert to understand that much of the legislation in Congress is mere cover for the politicians and the big banks. It isn't designed to redress the latest crisis or stop the next one. It puts matters in the hands of regulators who consistently failed, to, well, regulate. Regardless of party, the politicians will let the big banks go on gambling with other people's money. The only real solution is to reinstate Glass-Steagall and break up the big banks. Only one senator, Democrat Ted Kaufman of Delaware, railed for that and against something dressed up in the Orwellian costume of "reform."

Back here in Texas, when European settlers first came to the Hill Country they pushed ever deeper, establishing ranches, farms and homesteads because those early wet years made the land lush, green and inviting. When the Comanche came they scared some settlers. But when the droughts came, revealing a harsh, arid landscape clinging to hard-scrabble rock, it forced the hands of far more. I have taken what I have left and squirreled it away in a small Hill Country bank. But I, too, have to face the inevitable: I ask my 16-year old, Olivia, what she thinks about selling our little place high in the oaks and cedars over the Blanco. She looks at her sister, Isabel, and reflects, then replies: "We've made a lot of good memories here." I nod. So we have. So I will wait until, or unless, this drought forces my hand, too.

US Jobs Aren't Coming Back

by Staff - Daily Bell

Biden: We Can't Recover All the Jobs Lost ... Vice President Joe Biden (left) gave a stark assessment of the economy today, telling an audience of supporters, "there's no possibility to restore 8 million jobs lost in the Great Recession." Appearing at a fundraiser with Sen. Russ Feingold (D-Wisc.) in Milwaukee, the vice president remarked that by the time he and President Obama took office in 2008, the gross domestic product had shrunk and hundreds of thousands of jobs had been lost. "We inherited a godawful mess," he said, adding there was "no way to regenerate $3 trillion that was lost. Not misplaced, lost." – APDominant Social Theme: They may not be able to replace every single job but they're trying.

Free-Market Analysis: One of the hoariest dominant social themes or sub themes promoted by the power elite is that government can create jobs. It is possibly a sub theme because the dominant theme is simply that "government can do it all." In fact, the only things government can do with any modicum of efficiency are collect taxes, inflate currency and pass laws that usually have the opposite effect from what is intended. Of course this doesn't stop government pols from claiming they can create jobs when the economy becomes troubled and needs help. Here's some more from the article:

Claims for jobless benefits fell by the largest number in two months last week, but were still high enough to signal weak job growth. Meanwhile, the Senate on Thursday failed to pass an extension of unemployment benefits. Biden said today the economy is improving and noted that in the past four quarters, there has been 4 percent growth in the economy. Over the last five months, more than 500,000 private sector jobs were created. "We know that's not enough," the vice president said.

Last week the White House put out a Recovery and Reinvestment Act update claiming that between 2.2 million and 2.8 million jobs were either saved or created because of the stimulus as of March 2010. In signing the Recovery Act into law on Feb 17, 2009, Mr. Obama said the measure "will create or save 3- and-a-half million jobs over the next two years."

Peer behind the numbers claimed by the Obama administration and the questions multiply, as was pointed out in a recent Wall Street Journal article, "The Media Fall for Phony Jobs Claims." The article explained that one way the Obama administration had been able to make extravagant claims about jobs was by using the "saved or created." The US president used this phrase recently in announcing that the administration, via certain stimulus spending, had saved or created 150,000 American jobs. Obama then claimed that further job-savings programs were in the works to save another 600,000 jobs, but these numbers still pale against promises to save up to four million jobs that were made previously.

Of course, using such vague language makes it impossible to do any substantive fact-checking of claims. And there are no government or even private bureaus that track such statistics apparently. How is it possible to know whether a job has been "saved" or not? The claims are gobbledygook but the administration gets away with it because it has the bully pulpit and the media repeat the claims. Here's some more from the Journal:

If the "saved or created" formula looks brilliant, it's only because Mr. Obama and his team are not being called on their claims. And don't expect much to change. So long as the news continues to repeat the administration's line that the stimulus has already "saved or created" 150,000 jobs over a time period when the U.S. economy suffered an overall job loss 10 times that number, the White House would be insane to give up a formula that allows them to spin job losses into jobs saved.

The real reason for the downturn and loss of jobs have little to do with the Bush administration or even with the current cyclical downturn. It has everything to do with the constant inflationary measures of the mercantilist Federal Reserve and the company-killing graduated income tax that has sent companies large and small away from American shores. The combination of endless asset inflation and punitive taxation has been hollowing out America for at least a century if not longer. Regulatory "free-trade" agreements that are nothing but "managed trade" don't help either.

The American political regime of the past century has truly begun to bankrupt America. The country has lost vast amounts of manufacturing capability and even the chattering classes today speak of America's "service" economy as if this in some sense can compensate for the loss of the vital entrepreneurialism that builds the wealth of nations and individuals. Meanwhile, America's infrastructure degrades, its cities crumble, its vital middle class shrinks and companies that were founded there move offshore to grow.

Conclusion: The reasons for this ruin are clearly evident in the fiscal and monetary policies that the US has adopted over the past 100 years. To claim in any way that the Federal government is able to "save or create" jobs is truly a misleading statement given the policies that the US Federal government implemented in the 20th century. These policies in fact were supported by the larger Anglo-American power elite that has been trying to tear down the American republic since its inception in order to create a seamless US/European governmental authority. The idea that those who create fundamental policy for the US Federal government actually care about American workers, either blue collar or white collar, or want to see them succeed is a promotion, not a credible reality.

Double-dip drama

by The Economist

More than the European debt crisis is keeping American economic policymakers awake at night just now. Despite a year of government effort, a tentative recovery in the housing market appears to be on the verge of stalling. Home prices have now fallen for the past six months, according to the Case-Shiller home-price index, after rising from their nadir for the five months before that. (Another index, from the Federal Housing Finance Agency, has, however, shown a slight uptick in March and April.)

As for sales volumes, last September home sales soared in anticipation of the planned expiry of a government housing-tax credit, only to tumble thereafter, despite the extension of the deadline to April this year. As the new deadline approached sales duly climbed again. But the latest data show that even before the credit window closed, fewer sales were going through (see chart). Sales of new homes fell 33% from April to May, nearly the worst performance since the bust began.It is not as if the government has not tried. After the housing crash, millions of homeowners—a full quarter of those with mortgages—had loans larger than the value of their homes. Barack Obama hoped to prevent defaults with a plan designed to encourage banks to refinance the mortgages of those unable to pay. On the demand side, the Federal Reserve held down mortgage rates by buying up mortgage-backed securities, while Congress offered a generous tax credit to qualifying buyers.

These programmes have not worked as well as had been hoped. Affordability is no longer the driving factor behind foreclosures; borrowers who took on more debt than they could handle defaulted on their loans long ago. Instead, the problem is negative equity. A borrower deeply underwater on his mortgage may have no choice but to default if he loses his job, since a sale would entail a huge loss. And a growing number of underwater borrowers are opting simply to walk away from mortgages that they can in fact afford.

Banks are balking at rewriting mortgages, despite incentives to do so. Too often borrowers default later on. The latest data on the government’s programme show that 400,000 loans have been renegotiated—far less than the goal of 3m-4m. Neither have government incentives to buy houses helped much. Credits may have done little more than move sales around. The steady drumbeat of foreclosures has continued; they have been running at a rate of over 300,000 filings a month for the past 15 months. By some estimates, it will take more than eight years of normal sales to clear the stock of houses now held by banks. This overhang holds down prices, meaning that the road out of negative equity is a long one.

Yet policy failures can be blamed only so much. A new report from Harvard University’s Joint Centre for Housing Studies notes that, historically, sustained housing recoveries are far more dependent on job growth than on factors like the level of interest rates. So May’s disappointing jobs figures, showing that the private sector added just 41,000 workers, was doubly bad news. With nearly 15m Americans still out of work, a real turnaround could be a long time coming.

RBS tells clients to prepare for 'monster' money-printing by the Federal Reserve

by Ambrose Evans-Pritchard - Telegraph

As recovery starts to stall in the US and Europe with echoes of mid-1931, bond experts are once again dusting off a speech by Ben Bernanke given eight years ago as a freshman governor at the Federal Reserve. Entitled "Deflation: Making Sure It Doesn’t Happen Here", it is a warfare manual for defeating economic slumps by use of extreme monetary stimulus once interest rates have dropped to zero, and implicitly once governments have spent themselves to near bankruptcy. The speech is best known for its irreverent one-liner: "The US government has a technology, called a printing press, that allows it to produce as many US dollars as it wishes at essentially no cost."

Bernanke began putting the script into action after the credit system seized up in 2008, purchasing $1.75 trillion of Treasuries, mortgage securities, and agency bonds to shore up the US credit system. He stopped far short of the $5 trillion balance sheet quietly pencilled in by the Fed Board as the upper limit for quantitative easing (QE). Investors basking in Wall Street's V-shaped rally had assumed that this bizarre episode was over. So did the Fed, which has been shutting liquidity spigots one by one. But the latest batch of data is disturbing. The ECRI leading indicator produced by the Economic Cycle Research Institute plummeted yet again last week to -6.9, pointing to contraction in the US by the end of the year. It is dropping faster that at any time in the post-War era.

The latest data from the CPB Netherlands Bureau shows that world trade slid 1.7pc in May, with the biggest fall in Asia. The Baltic Dry Index measuring freight rates on bulk goods has dropped 40pc in a month. This is a volatile index that can be distorted by the supply of new ships, but those who watch it as an early warning signal for China and commodities are nervous. Andrew Roberts, credit chief at RBS, is advising clients to read the Bernanke text very closely because the Fed is soon going to have to the pull the lever on "monster" quantitative easing (QE)". "We cannot stress enough how strongly we believe that a cliff-edge may be around the corner, for the global banking system (particularly in Europe) and for the global economy. Think the unthinkable," he said in a note to investors.

Roberts said the Fed will shift tack, resorting to the 1940s strategy of capping bond yields around 2pc by force majeure said this is the option "which I personally prefer". A recent paper by the San Francisco Fed argues that interest rates should now be minus 5pc under the bank's "rule of thumb" measure of capacity use and unemployment. The rate is currently minus 2pc when QE is factored in. You could conclude, very crudely, that the Fed must therefore buy another $2 trillion of bonds, and even more if Europe's EMU debacle goes from bad to worse. I suspect that this hints at the Bernanke view, but it is anathema to hardliners at the Kansas, Richmond, Philadephia, and Dallas Feds.

Societe Generale's uber-bear Albert Edwards said the Fed and other central banks will be forced to print more money whatever they now say, given the "stinking fiscal mess" across the developed world. "The response to the coming deflationary maelstrom will be additional money printing that will make the recent QE seem insignificant," he said. Despite the apparent rift with Europe, the US is arguably tightening fiscal policy just as hard. Congress has cut off benefits for those unemployed beyond six months, leaving 1.3m without support. California has to slash $19bn in spending this year, as much as Greece, Portugal, Ireland, Hungary, and Romania combined. The states together must cut $112bn to comply with state laws.

The Congressional Budget Office said federal stimulus from the Obama package peaked in the first quarter. The effect will turn sharply negative by next year as tax rises automatically kick in, a net swing of 4pc of GDP. This is happening as the US housing market tips into a double-dip. New homes sales crashed 33pc to a record low of 300,000 in May after subsidies expired. It is sobering that zero rates, QE a l'outrance, and an $800bn fiscal blitz should should have delivered so little. Just as it is sobering that Club Med bond purchases by the European Central Bank and the creation of the EU's €750bn rescue "shield" have failed to stabilize Europe's debt markets.

Greek default contracts reached an all-time high of 1,125 on Friday even though the €110bn EU-IMF rescue is up and running. Are investors questioning EU solvency itself, or making a judgment on German willingness to back pledges with real money? Clearly we are nearing the end of the "Phoney War", that phase of the global crisis when it seemed as if governments could conjure away the Great Debt. The trauma has merely been displaced from banks, auto makers, and homeowners onto the taxpayer, lifting public debt in the OECD bloc from 70pc of GDP to 100pc by next year. As the Bank for International Settlements warns, sovereign debt crises are nearing "boiling point" in half the world economy.

Fiscal largesse had its place last year. It arrested the downward spiral at a crucial moment, but that moment has passed. There is a time to love and a time to hate, a time for war and a time for peace. The Krugman doctrine of perma-deficits is ruinous - and has in fact ruined Japan. The only plausible escape route for the West is a decade of fiscal austerity offset by helicopter drops of printed money, for as long as it takes. Some say that the Fed's QE policies have failed. I profoundly disagree. The US property market - and therefore the banks - would have imploded if the Fed had not pulled down mortgage rates so aggressively, but you can never prove a counter-factual.

The case for fresh QE is not to inflate away the debt or default on Chinese creditors by stealth devaluation. It is to prevent deflation. Bernanke warned in that speech eight years ago that "sustained deflation can be highly destructive to a modern economy" because it leads to slow death from a rising real burden of debt. At the time, the broad money supply was growing at 6pc and the Dallas Fed's `trimmed mean' index of core inflation was 2.2pc.

We are much nearer the tipping today. The M3 money supply has contracted by 5.5pc over the last year, and the pace is accelerating: the 'trimmed mean' index is now 0.6pc on a six-month basis, the lowest ever. America is one twist shy of a debt-deflation trap. There is no doubt that the Fed has the tools to stop this. "Sufficient injections of money will ultimately always reverse a deflation," said Bernanke. The question is whether he can muster support for such action in the face of massive popular disgust, a Republican Fronde in Congress, and resistance from the liquidationists at the Kansas, Philadelphia, and Richmond Feds. If he cannot, we are in grave trouble.

Look out for another financial avalanche

by Timothy Garton Ash - Globe and Mail

Our mighty bond markets, feared but also fearful, contribute to the very crises they wish to avert

I felt it was time I got to know the almighty. I mean, of course, the bond markets. For at their call, the governments of this world tremble. Before them, every knee shall bow. To fend off their wrath, Britain’s Chancellor of the Exchequer, George Osborne, has just presented the most draconian budget in living memory – a burnt offering on the altar of this god we call simply "the markets." So, over the past few weeks, I have been talking to traders, strategists and analysts in London’s bond markets. Let me say at once that I am a complete novice and amateur in this field. If you want expertise, read no further; turn instead to the Financial Times. If, however, you will accept me as your ordinary citizen’s emissary to Mount Olympus, read on.

The first thing that struck me was a Wizard of Oz effect. Pull back the curtain and you find, behind that giant figure with his booming, mysterious voice, a little man pushing buttons and pulling levers. Or rather, thousands of men (and a few women). Most of them, far from manifesting Olympian, god-like arrogance, seem even more terrified than the rest of us. Partly, no doubt, this is because they are paid to be nervous, but it is also because they better understand the very dangerous place we are in. And one reason they understand it better is that they know the danger comes also from themselves. For the financial markets are a classic example of what social scientists call a collective-action problem. Thousands of individual traders make decisions that are individually rational, at least in the short term, but collectively irrational.

An essential feature of financial markets is that those involved are simultaneously spectators and actors. George Soros, who has spent half a lifetime trying to explain this phenomenon to a wider world, said last week in London that "markets don’t reflect the facts very well, partly because they create the facts themselves." In what Mr. Soros calls "reflexivity," trends in the real world reinforce a bias in market participants’ minds, which in turn reinforces those trends in "a double feedback, reflexive connection." Realities create expectations, but expectations also create realities, and so on.

One analyst I spoke to developed a compelling metaphor of the bond markets now standing like skiers before the threat of a "sovereign avalanche." A single government defaulting could initiate a chain reaction of further defaults, accelerated by the collapse of banks holding too much of that government’s debt. In short, a "sovereign avalanche." The difference is this: On the slopes of Chamonix, even if a thousand skiers peer nervously up the slopes, their fear will have zero impact on the probability of an avalanche. In the financial markets, it is the skiers’ fear that triggers the avalanche.

Obviously, for such an avalanche danger to exist, there had first to be teetering piles of snow up the mountain. While overheated, overleveraged financial markets did contribute to piling up the snow, they were not primarily responsible for it. Governments, companies and, not least, you and me – in our double role as consumers and voters – were the main pilers of the snow. What the bond-market analysts show you with staggering clarity is, in most (though not all) of the developed world, and especially in many European countries, a ghastly tale of two Ds: debt and demography.

Over the past half-century, we have built up a staggering burden of corporate, household and public debt. Following the financial crisis, the emphasis has shifted from unsustainable private-sector borrowing to unsustainable public-sector borrowing. While the good-time bankers are laughing all the way to their yachts, a private-sector debt crisis has become a sovereign debt crisis. And, by the way, the virtuous, high-saving, exporter nations, such as China and Germany (or "Chermany," as Martin Wolf wittily dubs it), have depended on the credit-fuelled profligacy of others who buy their exports.

Meanwhile, the baby boomers are moving into retirement and the proportion of the population over 65 is soaring. Unless we have massive, successfully integrated youthful immigration, we will all have to work longer – and our welfare states will have to get shockingly leaner and meaner. Mr. Osborne’s axe is but a small taste of things to come. Financial markets are not mainly to blame for this double whammy of debt and demography, but nor are they merely "the messenger." The wizards to whom I spoke all identified some big problems with the way these markets work.

Until recently, it was taken as axiomatic that government bonds were virtually risk-free. Government bond yields were described as "the risk-free rate." Within the euro zone, the markets grossly mispriced the risk on countries like Greece. Yes, the Greek government had to pay a little more than Germany to borrow in the markets, but nothing like as much as it should have. Then there is the problem of chronic and growing short-termism. Asset managers now measure performance on a quarterly or at most a six-monthly time frame, with valuations being done at current market prices. So if there is a bubble, you as a fund manager must jump into it – even if you know the bubble is going to burst. If you don’t jump in, your sober pessimism may be justified in the slightly longer term, but in the meantime you’ll be out of a job, since investors will have taken their money elsewhere.

This in turn magnifies that inherent feature of markets, the Soros reflexivity effect. Whether you look at government debt, risk management or economic growth itself (which partly depends on how rich people feel, reflecting the current valuation of their assets), you see the same pattern of self-reinforcing upward or downward spirals. In layman’s terms, the ship is inherently unstable. If this analysis is not completely wide of the mark (and I welcome all learned explanations of why it is), then several questions follow. Can markets to some extent correct the way they themselves work, to address the problem of chronic short-termism, for example? If so, how? Can governments, international organizations and the co-ordinated actions of individual states regulate them more effectively? This will be a major subject of this weekend’s G20 meeting in Toronto.

Yet if bond markets have a collective-action problem, so do states. A clear impression I gained from my conversations is that one thing that really impresses the markets is determined, large-scale, "shock and awe," coûte que coûte action by a single, serious sovereign – i.e., a kind of power that the bond markets themselves can never be. Examples include the U.S. in the financial crisis, China and perhaps even (we shall see) little Britain today. One reason they are not yet convinced by the euro zone’s response to its crisis is that it does not have that single, serious, utterly determined sovereign. But if even the relatively tightly knit euro zone does not convince, how can a loose, disparate constellation of 20 states? I hope for the best at the G20 summit this weekend; I hope against hope. But if I were you, wherever you are, I’d prepare for more pain – and watch out for another avalanche.

Timothy Garton Ash is a professor of European studies at Oxford University.

You don’t recover from a debt crisis with more debt

by Gwyn Morgan - Globe and Mail

Hard to imagine a major economy with a greater need to tackle the deficit quickly than the U.S.

The normal format for global gatherings is for the leaders to avoid personal engagement until they arrive, followed by rubber stamping of a communiqué previously worked out by their advance entourages. The Canadian G8/G20 meetings broke sharply from that pattern. And the driving issue behind that change were sharply differing views on public spending.

In the run-up to the gatherings, summit host Prime Minister Stephen Harper sent a letter to G20 leaders calling for a wind down in stimulus spending and a focus on deficit reduction. A letter from U.S. President Barack Obama cautioned that premature "consolidation" (a new euphemism for spending reductions) could cause "renewed economic hardships and recession." European Union leaders, fresh from grappling with a credit and currency crisis that threatens the very survival of the euro zone, declared that the bigger risk is failure to control runaway deficits.

Responding to Mr. Obama’s call for "unity of purpose to provide the policy [spending] support necessary to keep economic growth strong," German Chancellor Angela Merkel stated, "It’s not about growth at any price, it’s about sustainable growth," and unleashed two of her ministers to expand on her government’s position. German Finance Minister Wolfgang Schaeuble told reporters "Nobody can seriously dispute that excessive public debts, not only in Europe, are one of the main causes of the crisis," while Economy Minister Rainer Bruederle said the U.S. must join Europe in "urgently" cutting spending. EU President Herman Van Rompuy said, "Failure to correct unsustainable deficits would ultimately lead to fatal loss of credibility and confidence with lasting economic damage."

British Prime Minister David Cameron noted that "for some countries, such as our own, there is a need to get on and tackle the deficit more quickly." With a national debt topping $13-trillion (U.S.), a deficit expected to be another $1.5-trillion in the 2010-2011 fiscal year, it’s hard to imagine a major economy with a greater need to "tackle the deficit more quickly" than the United States. Mr. Obama’s letter referenced plans to cut the U.S. deficit by half by 2013 and "work to reduce our fiscal deficit to 3 per cent of GDP by 2015," which would mean cutting the current deficit by 70 per cent, or more than $1-trillion.

To say that this seems like dreaming in Technicolor is an understatement. Mr. Obama’s expensive health-care reforms, along with rising Social Security costs, are certain to increase program spending, while interest payments on the national debt will grow substantially. (At the weekend G20 meeting in Toronto, leaders agreed on a plan for advanced countries to cut deficits in half by 2013 and stabilize debt loads by 2016.)

But even the incredible U.S. deficit doesn’t tell the whole story. American states face a combined budget shortfall of some $300-billion and some are in even more financial trouble than the euro zone’s so-called PIGS (Portugal, Italy, Greece and Spain). But in the U.S. case, the member of the union in the most trouble is also the biggest, and its deficit position is worse than that of Greece. The state of California faces a 30-per-cent shortfall on next year’s budget of some $125-billion, or a whopping $37-billion. Obama adviser Warren Buffett has said that a federal bailout of troubled states is "inevitable" if they are to avoid default on state bonds.

A look at countries that have experienced profound economic failure shows a convergence of forces creating an unrecoverable "debt spiral." Huge fiscal deficits, ever-rising interest costs on a mushrooming national debt, and growth capital sucked from the private sector to finance public sector deficits – they all lead financial markets to conclude that a country’s central bank will either default on its debt or resort to printing money, causing catastrophic currency devaluation.

Who could have predicted that this Group of 20 meeting would see the chronically profligate Europeans counselling fiscal prudence, while the world’s traditional economic bedrock and issuer of the global reserve currency spends it way toward disaster? The euro zone crisis demonstrated that financial markets can lose confidence in the bonds and currency of sovereign states in a heartbeat. Remember that the combined deficits of borrowing states must be financed by private investors and countries that are running fiscal surpluses, such as China and Middle Eastern oil producers. A loss of confidence in U.S. federal and state bonds, and in the world’s reserve currency itself, could trigger an economic conflagration that would making the recent global financial crisis seem like a walk in the park.

The U.S. administration is playing an extremely high-risk game that could see Mr. Obama go down as the most damaging president in history. You don’t recover from alcoholism by taking another drink, and you don’t recover from a debt crisis with more debt. It’s past time that John Maynard Keynes’s long-discredited deficit spending theories be tucked back in his grave. Even if they are, it will take decades to repair the damage already done.

The Keynesian Dead End

by WSJ Editorial

Spending our way to prosperity is going out of style.

Today's G-20 meeting has been advertised as a showdown between the U.S. and Europe over more spending "stimulus," and so it is. But the larger story is the end of the neo-Keynesian economic moment, and perhaps the start of a healthier policy turn. For going on three years, the developed world's economic policy has been dominated by the revival of the old idea that vast amounts of public spending could prevent deflation, cure a recession, and ignite a new era of government-led prosperity. It hasn't turned out that way.

Now the political and fiscal bills are coming due even as the U.S. and European economies are merely muddling along. The Europeans have had enough and want to swear off the sauce, while the Obama Administration wants to keep running a bar tab. So this would seem to be a good time to examine recent policy history and assess the results.

***

Like many bad ideas, the current Keynesian revival began under George W. Bush. Larry Summers, then a private economist, told Congress that a "timely, targeted and temporary" spending program of $150 billion was urgently needed to boost consumer "demand." Democrats who had retaken Congress adopted the idea—they love an excuse to spend—and the politically tapped-out Mr. Bush went along with $168 billion in spending and one-time tax rebates.

The cash did produce a statistical blip in GDP growth in mid-2008, but it didn't stop the financial panic and second phase of recession. So enter Stimulus II, with Mr. Summers again leading the intellectual charge, this time as President Obama's adviser and this time suggesting upwards of $500 billion. When Congress was done two months later, in February 2009, the amount was $862 billion. A pair of White House economists famously promised that this spending would keep the unemployment rate below 8%.

Seventeen months later, and despite historically easy monetary policy for that entire period, the jobless rate is still 9.7%. Yesterday, the Bureau of Economic Analysis once again reduced the GDP estimate for first quarter growth, this time to 2.7%, while economic indicators in the second quarter have been mediocre. As the nearby table shows, this is a far cry from the snappy recovery that typically follows a steep recession, most recently in 1983-84 after the Reagan tax cuts.

The response at the White House and among Congressional leaders has been . . . Stimulus III. While talking about the need for "fiscal discipline" some time in the future, President Obama wants more spending today to again boost "demand." Thirty months after Mr. Summers won his first victory, we are back at the same policy stand. The difference this time is that the Keynesian political consensus is cracking up. In Europe, the bond vigilantes have pulled the credit cards of Greece, Portugal and Spain, with Britain and Italy in their sights.

Policy makers are now making a 180-degree turn from their own stimulus blowouts to cut spending and raise taxes. The austerity budget offered this month by the new British government is typical of Europe's new consensus. To put it another way, Germany's Angela Merkel has won the bet she made in early 2009 by keeping her country's stimulus far more modest. We suspect Mr. Obama will find a political stonewall this weekend in Toronto when he pleads with his fellow leaders to join him again for a spending spree.

Meanwhile, in Congress, even many Democrats are revolting against Stimulus III. The original White House package of jobless benefits and aid to the states had to be watered down several times, and the latest version failed again in the Senate late this week. (See below.) Mr. Obama is having his credit card pulled too—not by the bond markets, but by a voting public that sees the troubles in Europe and is telling pollsters that it doesn't want a Grecian bath.

***

The larger lesson here is about policy. The original sin—and it was nearly global—was to revive the Keynesian economic model that had last cracked up in the 1970s, while forgetting the lessons of the long prosperity from 1982 through 2007. The Reagan and Clinton-Gingrich booms were fostered by a policy environment for most of that era of lower taxes, spending restraint and sound money. The spending restraint began to end in the late 1990s, sound money vanished earlier this decade, and now Democrats are promising a series of enormous tax increases.

Notice that we aren't saying that spending restraint alone is a miracle economic cure. The spending cuts now in fashion in Europe are essential, but cuts by themselves won't balance annual deficits reaching 10% of GDP. That requires new revenues from faster growth, and there's a danger that the tax increases now sweeping Europe will dampen growth further.

President Obama's tragic mistake was to blow out the U.S. federal balance sheet on spending that has produced little bang for the buck. The fantastical Keynesian notion (the "multiplier") that $1 of spending produces $1.50 in growth was long ago demolished by Harvard's Robert Barro, among others. That $1 in spending has to come from somewhere, which means in taxes or borrowing from productive parts of the private economy. Given that so much of the U.S. stimulus went for transfer payments such as Medicaid and unemployment insurance, the "multiplier" has almost certainly been negative.

With the economy in recession in 2008 and 2009, we argued that some stimulus was justified and an increase in the deficit was understandable and inevitable. However, we also argued that permanent tax cuts aimed at marginal individual and corporate tax rates would have done far more to revive animal spirits, and in our view would have led to a far more robust recovery.

***

What the world has now reached instead is a Keynesian dead end. We are told to let Congress continue to spend and borrow until the precise moment when Mr. Summers and Mark Zandi and the other architects of our current policy say it is time to raise taxes to reduce the huge deficits and debt that their spending has produced. Meanwhile, individuals and businesses are supposed to be unaffected by the prospect of future tax increases, higher interest rates, and more government control over nearly every area of the economy. Even the CEOs of the Business Roundtable now see the damage this is doing.

A better economic policy will have to await a new Congress, which we hope at a minimum can prevent punishing tax increases. But for now the good news is that voters and markets are telling politicians to stop doing what hasn't worked.

The Pendulum Swings Toward Austerity

by Tyler Cowen - New York Times

"The Road To Serfdom," the critique of socialism written 65 years ago by the Nobel laureate economist Friedrich von Hayek, was recently No. 1 in nonfiction sales at Amazon.com. Many people, including the Fox News commentator Glenn Beck, have contended that growth of government power has, indeed, set us on such a road today. But the reality looks different. In many respects, the expansionary phase of big government is coming to an end, and quickly.

In the last few years, we have seen — for better or worse — huge financial bailouts, a $787 billion stimulus plan and legislation for near-universal health insurance coverage. But the policy mood in Washington is now much more modest: no second major stimulus is forthcoming and, in the environmental arena, a cap-and-trade system for greenhouse gas emissions is unlikely to move forward. The financial regulation bill will most likely pass, but it won’t fundamentally restructure the American economy. For instance, there is no longer talk of breaking up the big financial institutions, and Simon Johnson, the M.I.T. economist, has described the legislation as a failure.

To the extent that the bill limits proprietary trading by American banks — through the so-called Volcker amendment, named for the former Federal Reserve chairman — loopholes may enable banks to keep trading through asset management companies. The most extreme outcome would be that more financial market trading is pushed out of banks and into hedge funds and other bank competitors. That would matter a lot for bank profits, but American capital markets would perform essentially the same functions as before. The bill we’re getting may be a mere hodgepodge, and that is after the biggest financial crisis since the Great Depression.

If any financial policy idea is taking a major place on the American and global stages, it is fiscal austerity. It is not that fiscal conservatives have won a grand battle of ideas, but rather that governments realize that the bills are coming due. In the United States, we face rising health care costs and pension problems in state governments, with no clear long-run solution for bringing the books into balance. That makes responsible politicians reluctant to undertake major new commitments. At the very least, they embrace the rhetoric of fiscal conservatism, even when actual progress toward the ideal is slow.

In short, it’s not that ideas of government interventionism and free markets are fighting a titanic intellectual struggle. The reality is more mundane. The ascendancy of one view often creates the conditions for an economic counterreaction. We’ve seen such cyclical trends before. During the 1980s and 1990s, history seemed to be on the side of freer markets. Communism staged a mass retreat, China and India embraced economic growth and a wide range of governments adopted privatization. The United States cut marginal tax rates and the Clinton administration promoted free trade and welfare reform.

Eventually, things started to go wrong, in part because investors developed too much self-confidence and became complacent about systemic risk. Early cracks in the edifice appeared in the 1990s, during the Mexican and Asian financial crises, but the bigger, broader explosion of 2007 revealed a badly overextended world economy, which led to bailouts. The weak economy brought victory for the Democrats in 2008, which in turn enabled passage of a health care overhaul. Now the pendulum is swinging back. The economy will now likely make Congress much more Republican, as voters overreact to whatever is not working at the moment.

The unfolding of the financial crisis has also changed the public’s sense of where change is needed, both in the United States and Europe. The tragedies of 2008 were represented by Bear Stearns and Lehman Brothers — both private-sector institutions. In 2010, the financial crisis has spread to sovereign debt, with Greece as the most obvious example. All of these developments are part of one broader story of overreach and complacency.

Yet the 2008 crises were attached more directly to market institutions, while the 2010 crises are more closely linked to governments. Because politicians and voters are more influenced by the latest developments than by news from two or three years earlier, a cautious attitude toward public-sector spending has been further cemented. While we can expect a larger public sector in America, the cause is mainly the aging of the population, and it will play itself out over the next 30 years with an increase in government transfer payments, mostly through Medicare. Furthermore, even Professor Hayek favored welfare spending and social insurance, so those programs will not alone bring us to serfdom.

Democracies, like markets, have some self-correcting mechanisms, and we are now seeing those at work in the United States and many European countries. (Spain and Britain, for example, are pursuing fiscal austerity aggressively.) The lessons are straightforward. First, to paraphrase the French moralist La Rochefoucauld, things are never as good, or as bad, as they seem. Second, the Obama reforms, like the Reagan revolution, are turning out to be radically incomplete, which should come as no surprise.

Finally, effective political ideas are those that can still do good in half-baked form. We have neglected this insight in designing financial reform, and it remains to be seen if we can apply it successfully to climate change. And when it comes to the budget? Even if our real fiscal problems lie in the more distant future, it’s important to start worrying about them now, because we cannot count on a grand plan later to save the day.

Repent at leisure

by Philip Coggan - The Economist

Borrowing has been the answer to all economic troubles in the past 25 years. Now debt itself has become the problem

Man is born free but is everywhere in debt. In the rich world, getting hold of your first credit card is a rite of passage far more important for your daily life than casting your first vote. Buying your first home normally requires taking on a debt several times the size of your annual income. And even if you shun the temptation of borrowing to indulge yourself, you are still saddled with your portion of the national debt.

Throughout the 1980s and 1990s a rise in debt levels accompanied what economists called the "great moderation", when growth was steady and unemployment and inflation remained low. No longer did Western banks have to raise rates to halt consumer booms. By the early 2000s a vast international scheme of vendor financing had been created. China and the oil exporters amassed current-account surpluses and then lent the money back to the developed world so it could keep buying their goods.

Those who cautioned against rising debt levels were dismissed as doom-mongers; after all, asset prices were rising even faster, so balance-sheets looked healthy. And with the economy buoyant, debtors could afford to meet their interest payments without defaulting. In short, it paid to borrow and it paid to lend. Like alcohol, a debt boom tends to induce euphoria. Traders and investors saw the asset-price rises it brought with it as proof of their brilliance; central banks and governments thought that rising markets and higher tax revenues attested to the soundness of their policies.The answer to all problems seemed to be more debt. Depressed? Use your credit card for a shopping spree "because you’re worth it". Want to get rich quick? Work for a private-equity or hedge-fund firm, using borrowed money to enhance returns. Looking for faster growth for your company? Borrow money and make an acquisition. And if the economy is in recession, let the government go into deficit to bolster spending. When the European Union countries met in May to deal with the Greek crisis, they proposed a €750 billion ($900 billion) rescue programme largely consisting of even more borrowed money.

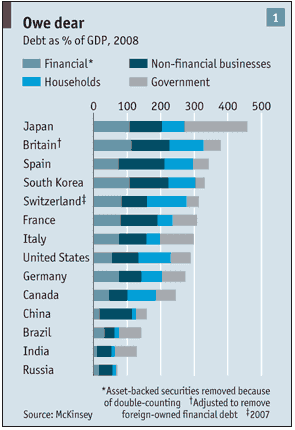

Debt increased at every level, from consumers to companies to banks to whole countries. The effect varied from country to country, but a survey by the McKinsey Global Institute found that average total debt (private and public sector combined) in ten mature economies rose from 200% of GDP in 1995 to 300% in 2008 (see chart 1 for a breakdown by country). There were even more startling rises in Iceland and Ireland, where debt-to-GDP ratios reached 1,200% and 700% respectively. The burdens proved too much for those two countries, plunging them into financial crisis. Such turmoil is a sign that debt is not the instant solution it was made out to be. The market cheer that greeted the EU package for Greece lasted just one day before the doubts resurfaced.

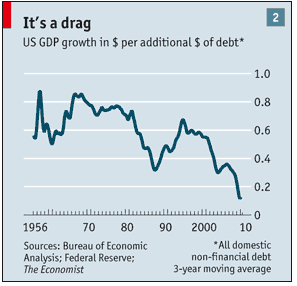

From early 2007 onwards there were signs that economies were reaching the limit of their ability to absorb more borrowing. The growth-boosting potential of debt seemed to peter out. According to Leigh Skene of Lombard Street Research, each additional dollar of debt was associated with less and less growth (see chart 2).

Stopping the debt supercycle

The big question is whether this rapid build-up of debt—a phenomenon which Martin Barnes of the Bank Credit Analyst, a research group, has dubbed the "debt supercycle"—has now come to an end. Debt reduction has become a hot political issue. Rioters on the streets of Athens have been protesting against the "junta of the markets" that is imposing austerity on the Greek economy, and tea-party activists in America, angry about trillion-dollar deficits and growing government involvement in the economy, have been upsetting the calculations of both the Democratic and Republican party leaderships.To understand why debt may have become a burden rather than a boon, it is necessary to go back to first principles. Why do people, companies and countries borrow? One obvious answer is that it is the only way they can maintain their desired level of spending. Another reason is optimism; they believe the return on the borrowed money will be greater than the cost of servicing the debt. Crucially, creditors must believe that debtors’ incomes will rise; otherwise how would they be able to pay the interest and repay the capital?

But in parts of the rich world such optimism may now be misplaced. With ageing populations and shrinking workforces, their economies may grow more slowly than they have done in the past. They may have borrowed from the future, using debt to enjoy a standard of living that is unsustainable. Greece provides a stark example. Standard & Poor’s, a rating agency, estimates that its GDP will not regain its 2008 level until 2017.

Rising government debt is a Ponzi scheme that requires an ever-growing population to assume the burden—unless some deus ex machina, such as a technological breakthrough, can boost growth. As Roland Nash, head of research at Renaissance Capital, an investment bank, puts it: "Can the West, with its regulated industry, uncompetitive labour and large government, afford its borrowing-funded living standards and increasingly expensive public sectors?"

Sovereign default is far from inconceivable. Many people are forecasting that Greece, despite its bail-out package from the EU and the IMF, will be unable to repay its debts in full and on time. Faced with the choice between punishing their populations with austerity programmes and letting down foreign creditors, countries may find it easier to disappoint the foreigners. Defaults have been common in the past, as Carmen Reinhart and Ken Rogoff showed in their book, "This Time is Different". Adam Smith, a founding father of economics, noted in "The Wealth of Nations" that "when national debts have once been accumulated to a certain degree, there is scarce, I believe, a single instance of their having being fairly and completely paid."

Governments now face a tricky period when they have to deal with the debt overhang, decide how quickly to cut their deficits (and risk undermining growth), and try to distribute the pain of doing so as equitably as possible. Debt is often treated as a moral issue as well as an economic one. Margaret Atwood, in her book of essays, "Payback: Debt and the Shadow Side of Wealth", notes that the Aramaic words for debt and sin are the same. And some versions of the Lord’s Prayer say "Forgive us our debts" rather than "Forgive us our trespasses".

The Live 8 campaign in 2005 tried to shame developed nations into forgiving the debts of poor countries, particularly in sub-Saharan Africa. Economists have developed the concept of "odious debt" in which citizens should not be forced to repay money borrowed by tyrannical or kleptocratic rulers. Interest payments on debt are often regarded as an onerous burden placed on the poor; interest is seen as an unjustified reward for capital, a concept that goes back to Aristotle and is implicit in the Christian idea of usury. Islam forbids it altogether. The book of Deuteronomy suggested a debt amnesty every seven years, which survived into later Jewish custom.

But conventional morality has not always been on the side of the borrowers. Some regard debt as the road to ruin and the failure to repay as a breach of trust. In the 18th and 19th century debtors in Britain were often thrown into jail (as in Charles Dickens’s "Little Dorrit"), though Samuel Johnson spotted the flaws of the practice: "We have now imprisoned one generation of debtors after another, but we do not find that their numbers lessen. We have now learned that rashness and imprudence will not be deterred from taking credit; let us try whether fraud and avarice may be more easily restrained from giving it."

Movable morals

In the past 100 years the moral battle has moved in favour of the debtors. Bankruptcy is no longer stigmatised but simply regarded as bad luck. When consumers borrow beyond their means, the blame is laid on lax lending practices rather than irresponsible borrowing. Governments have encouraged more people to become homeowners and thus to take on debt. And defaulting on one’s debts has become much less cumbersome; in the current housing slump many American homeowners have resorted to "jingle mail", dropping their keys through the lender’s letterbox and walking away from their property.

In business, a few failed directorships are a sign of entrepreneurship rather than incompetence. America’s Chapter 11 process allows the managers of companies to remain in place and the business to be protected from its creditors. The number of companies with safe AAA credit ratings has collapsed as more have acted on the theory that a debt-laden balance-sheet is more efficient (because interest payments are tax-deductible in most countries). The recent crisis has also diminished belief in the judgment of the financial markets. The role of banks in the credit crunch and the cost of the financial sector bail-out has undermined the idea that the markets assess risk fairly and rationally. Instead, higher borrowing costs are seen as the result of unscrupulous speculation.

The role of sovereign credit-default swaps (CDS), a way of betting on the likelihood of a country’s failure to repay the money it has borrowed, has proved particularly controversial. Southern European nations, which have been at the heart of the recent market turmoil, have been quick to blame an Anglo-Saxon conspiracy, brewed up by hedge funds, credit-rating agencies and even newspapers like this one, for unfairly pushing up their borrowing costs. The German government moved to ban short-selling of government bonds and some CDS transactions last month. As Charles Stanley, a stockbroking firm, cynically puts it, EU nations are saying: "Please fund our lifestyles, but don’t hold us to any commitments."

Why it matters

If a husband borrows money from his wife, the family is no worse off. By extension, just as every debt is a liability for the borrower, it is an asset for the creditor. Since Earth is not borrowing money from Mars, does the debt explosion really matter, or is it just an accounting device? During the credit boom of the early 1990s and 2000s the conventional view was that it did not matter. Not only were asset prices rising even faster than debt but the use of derivatives was spreading risk across the system and, in particular, away from the banks, which had capital ratios well above the regulatory minimum.

The problem with debt, though, is the need to repay it. Not for nothing does the word credit have its roots in the Latin word credere, to believe. If creditors lose faith in their borrowers, they will demand the repayment of existing debt or refuse to renew old loans. If the debt is secured against assets, then the borrower may be forced to sell. A lot of forced sales will cause asset prices to fall and make creditors even less willing to extend loans. If the asset price falls below the value of the loan, then both creditors and borrowers will lose money. This is particularly troublesome if the economy slips into deflation, as happened globally in the 1930s and in Japan in the 1990s.

Debt levels are fixed in nominal terms whereas asset prices can go up or down. So falling prices create a spiral in which assets are sold off to repay debts, triggering further price falls and further sales. Irving Fisher, an economist who worked in the first half of the 20th century, called this the debt deflation trap. Another reason why debt matters is to do with the role of banks in the economy. By their nature, banks borrow short (from depositors or the wholesale markets) and lend long. The business depends on confidence; no bank can survive if its depositors (or its wholesale lenders) all want their money back at once. If banks struggle to meet their own debts, they have no choice but to reduce their lending. If this happens on a large scale, as it did in the 1930s, the ripple effect for the economy as a whole can be devastating.

Both of these effects were seen in the debt crisis of 2007-08. Falling property prices caused defaults and a liquidity crisis in the banking system so severe that the authorities feared the cash machines would stop working. Hence the unprecedented largesse of the bank bail-out.

Hyman Minsky, an American economist who has become more fashionable since his death in 1996, argued that these debt crises were both inherent in the capitalist system and cyclical. Prosperous times encourage individuals and companies to take on more risk, meaning more debt. Initially such speculation is successful and encourages others to follow suit; eventually credit is extended to those who will be able to repay the debt only if asset prices keep rising (a succinct description of the subprime-lending boom). In the end the pyramid collapses.

In the aftermath of the latest collapse it is clear that the distinction between debt in the private and public sector has become blurred. If the private sector suffers, the public sector may be forced to step in and assume, or guarantee, the debt, as happened in 2008. Otherwise the economy may suffer a deep recession which will cut the tax revenues governments need to service their own debt.

If the Western world faces an era of austerity as debts are paid down, how will that affect day-to-day life? Clearly a society built on consumption will have to pay more attention to saving. The idea that using borrowed money to buy assets is the smart road to riches might lose currency, changing attitudes to home ownership as well as to parts of the finance sector such as private equity.

This special report will argue that, for the developed world, the debt-financed model has reached its limit. Most of the options for dealing with the debt overhang are unpalatable. As has already been seen in Greece and Ireland, each government will have to find its own way of reducing the burden. The battle between borrowers and creditors may be the defining struggle of the next generation.

At G-20 Summit Talks, Obama Lacks Strong Hand on Stimulus

by Jackie Calmes and Sewell Chan - New York Times

Despite President Obama’s pitch at the summit meeting for developed nations here for continued stimulus measures to prevent another global economic downturn, the United States will go along with other leaders who are more concerned about rising debt and join in a commitment to cut their governments’ deficits in half by 2013, administration officials said on Saturday.

That goal is the proposal of Stephen Harper, the prime minister of Canada and the host of the two-day Group of 20 summit of developed nations. Mr. Harper wanted it to be part of the communiqué on global economic policy that the group adopts before concluding on Sunday, and he had the support of European leaders, including David Cameron, the new prime minister of Britain, who has proposed the most ambitious austerity plan of spending cuts and tax increases in his country in a half-century.

Mr. Cameron and Mr. Obama, in their first private meeting since Mr. Cameron took office, acknowledged their different approaches toward balancing the need to promote greater economic growth and job creation in the short term with the long-term desire to reduce national debts, which reached dangerous heights during the downturn. But they downplayed those differences. Mr. Obama said the two leaders were bound to have different approaches given their country’s separate budget outlooks; Britain’s debt is bigger than that of the United States, measured against the size of their respective economies. "But we are aiming at the same direction, which is long-term sustainable growth that puts people to work," Mr. Obama said.

Mr. Cameron added, "Those countries that have big deficit problems like ours have to take action in order to keep that level of confidence in the economy which is absolutely vital to growth." He joked that he could not afford to pay for the helicopter ride that Mr. Obama had given him Saturday from the isolated site of the Group of 8 talks to the subsequent G-20 session in Toronto. The separate approaches represented by Mr. Obama and Mr. Cameron reflected the splintering that is occurring within the G-20 as the global economy recovers, if haltingly, amid some fears of another recession. In three previous summit meetings since the financial and economic crisis began in 2008, the Group of 20 has coordinated on stimulus measures, banking regulations and anti-protectionist measures.

The Obama administration did have allies at the summit in opposing rapid moves to withdraw governments’ stimulus measures. The Brazilian finance minister, Guido Mantega, told reporters that the debt-reduction targets could compromise economic growth and would be "too draconian" for certain countries to meet. "It is clear that we need to cut, but at what speed?" he asked. Japan has also taken a position more closely aligned with the United States’.

Treasury Secretary Timothy F. Geithner emphasized the American position again Saturday as he arrived here for the beginning of the G-20 talks. Speaking to reporters, he said that for all the progress the G-20 countries had made since late 2008, "the scars of this crisis are still with us." Trying to bridge the differences among leaders here, he said: "Our challenge, as the G-20, is to act together to strengthen the prospects for growth. This will require different strategies in different countries. We are coming out of the crisis at different speeds."

Mr. Obama came to the summit table this weekend with a strong hand to press his case to foreign leaders for tougher banking regulations, after Congress agreed to a far-reaching overhaul of the American regulatory system. But he was hindered in his effort to persuade other governments to keep stimulating their economies. Even as Congress allowed Mr. Obama to pack the big victory on banking regulation as he left for the Group of 20 summit talks, the Senate separately dealt him a significant setback that no doubt resonated with the foreign leaders here pushing fiscal austerity: Democratic leaders shelved an economic stimulus package of aid for the long-term unemployed and financially squeezed states, along with assorted tax cuts.

The setback underscored the difficulty Mr. Obama has had in making the case for stimulus. At home as abroad, Mr. Obama is confronting the limits of the consensus that took hold after the economic crisis began in 2008, which favored bigger deficits to spur job creation. At stake, as the administration sees it, is continued global recovery or a relapse into another recession. Yet even within Mr. Obama’s administration there are fault lines on how much additional stimulus is desirable.

Some news reports in recent days suggested that Peter R. Orszag, the budget director who recently announced that he would be leaving in late July, was resigning partly out of frustration that he had lost the argument for deeper and quicker reductions in projected deficits. Advisers and associates of Mr. Orszag insist that is not so, however, and Mr. Orszag was moved to address the issue late Friday in his blog on the Web site of the Office of Management and Budget.

Saying that "it was simply time for me to move on," Mr. Orszag recounted the deficit-reduction steps that Mr. Obama has proposed: a three-year freeze after this fiscal year for nonsecurity domestic appropriations, $1 trillion in reductions over the coming decade and a bipartisan fiscal commission — a priority of Mr. Orszag’s — that will try to make recommendations, with a Dec. 1 target, for reducing the debt. "The president has made it clear to his economic team that he is seriously committed to tackling our fiscal problems," Mr. Orszag wrote.

Indeed, Mr. Orszag has complained to associates that the debate over job creation versus deficit reduction is a false one; the only disagreement is over timing. In advance of the G-20, Mr. Geithner, who is closer in his thinking to Mr. Orszag, and Lawrence H. Summers, the director of the White House National Economic Council, and a proponent of more short-term stimulus measures, co-wrote an op-ed column in The Wall Street Journal to project a united front on the issue. "We must demonstrate a commitment to reducing long-term deficits, but not at the price of short-term growth," they wrote. "Without growth now, deficits will rise further and undermine future growth."

European countries generally are running annual deficits of about 6 percent of the size of their economies — twice as large as the limit that the European Union tries to enforce. Even before Mr. Cameron took action in London, Germany’s chancellor, Angela Merkel, and Nicolas Sarkozy, the president of France, had begun turning from stimulus to immediate deficit reductions. Mr. Harper of Canada on Friday praised Mr. Cameron for his austerity initiative, saying it was the sort of fiscal constraint the rest of the G-20 nations should adopt. On Saturday, an adviser said Mr. Harper was lobbying the other leaders to commit to fully implement "existing" stimulus plans — suggesting no additional spending or tax cut measures — and to cut their annual deficits in half by 2013 and put them on a downward trajectory after 2016.

That is a more ambitious and constrictive path than the one Mr. Obama has proposed as the goal of his fiscal commission. He has proposed that the United States cut its annual deficit to 3 percent of the gross domestic product by fiscal year 2015.

Germany Warns US Not to Become 'Addicted to Borrowing'

by Der Spiegel

The US has heavily criticized German austerity measures in recent days. Now, Germany's finance minister has fired back, warning against becoming addicted to deficit spending and noting that history has made the country extremely wary of national debt and inflation. Conflict, it would seem, will be everywhere in Toronto this weekend as world leaders gather for the G-20 summit to discuss possible reforms to the global financial system. Already, new British Prime Minister David Cameron has said that he may end up trying to avoid sitting next to German Chancellor Angela Merkel on Sunday. "I'm not sure if that will be safe. We might get a bit carried away," he said.

Cameron's comments were, of course, tongue in cheek. He was referring to Sunday's World Cup battle between Germany and England in South Africa. Still, there is little doubt that sparks will fly this weekend, particularly when it comes to competing views on fiscal policy between Europe and the United States. Indeed, German Finance Minister Wolfgang Schäuble poured more fuel on the fire in a contribution published Friday in the business daily Handelsblatt. Referring to US demands that Germany abandon austerity in favor of additional economic stimulus measures, Schäuble said that "governments should not become addicted to borrowing as a quick fix to stimulate demand. Deficit spending cannot become a permanent state of affairs."

The Longer View

Schäuble said that he cannot relate to accusations that Germany hasn't done its part to stimulate the economy, pointing out that Berlin passed a massive stimulus package in 2008. "Additionally," he said, "we also have so-called automatic stabilizers (such as high social welfare expenditures) that do not play as big a role in the countries that are now criticizing us." Merkel's finance minister also pointed out that "while US policymakers like to focus on short-term corrective measures, we take the longer view and are, therefore, more preoccupied with the implications of excessive deficits and the dangers of high inflation." Schäuble remarked that, while US economic history has taught the country to be wary of deflation, Germany's history has resulted in widespread fear of deficits and inflation.

Schäuble's remarks were just the latest in a trans-Atlantic back-and-forth that has continued all week. US President Barack Obama's letter to G-20 leaders , in which he wrote, "I am concerned about weak private sector demand and continued heavy reliance on exports by some countries with already large external surpluses," kicked off the debate late last week. Most interpreted the line as a warning directed at Berlin. Merkel has since been energetic in her defense of Berlin's focus on debt and deficit reduction, telling German public broadcaster ARD on Thursday that "I don't think we should relent."

'No More Room for Deficit Spending'

Berlin has received support in recent days from European Central Bank President Jean-Claude Trichet. Speaking to the Italian daily La Repubblica on Thursday, he said "with regards to economic growth, it is wrong to believe that the (European) austerity measures will result in stagnation." European Commission President Jose Manuel Barroso also backed up the German chancellor, telling reporters in Toronto that "there is no more room for deficit spending." US Secretary of the Treasury, Timothy Geithner, appeared eager to play down the disagreement on Thursday, telling BBC World News America that "our job is to make sure we're all sitting together, focused on this challenge of growth and confidence because growth and confidence are paramount."

Still, even if Europe and the US agree to disagree when it comes to the austerity versus stimulus debate, there are plenty of other items on the agenda that are likely to result in discord. A European proposal for a global tax on financial transactions appears to be headed for the dustbin in Toronto. Similarly, a worldwide levy on banks to build up a fund for the next crisis is likely to be rejected. China, Australia and host Canada -- all countries that did not have to bail out their banking industry during the financial crisis -- are opposed to the measures.

Orszag exit reveals deficit policy split

by Edward Luce - Financial Times

Peter Orszag, Barack Obama’s budget director, resigned this week partly in frustration over his lack of success in persuading the Obama administration to tackle the fiscal deficit more aggressively, according to sources inside and outside the White House. Mr Orszag, whose publicly stated reasons for leaving were that he was exhausted after years in high pressure jobs and also that he wanted to plan for his wedding in September, is seen as the guardian of fiscal conservatism within the White House.

Other members of Mr Obama’s economic team, notably Lawrence Summers, the head of the National Economic Council, have placed more emphasis on the need for continued short-term spending increases to counteract what increasingly looks like an anaemic economic recovery in the US. Although Mr Orszag agrees with the need to push short-term spending, particularly in the Senate, which again this week failed to pass a measure extending insurance to the unemployed, the budget director has become increasingly frustrated with the administration’s caution on longer-term fiscal restraint.

Mr Orszag, whom Mr Obama has dubbed a "propeller-head" because of his brilliant facility with projections and spreadsheets, has tried but failed to convince his colleagues to "step up the action", according to one insider. In particular, he has collided with the political team, led by Rahm Emanuel, Mr Obama’s chief of staff, over Mr Obama’s 2008 election pledge not to raise taxes on any households earning less than $250,000 a year – a category that covers more than 98 per cent of Americans.