"Tramps in boxcar playing cards, location unknown"

Ilargi: Let's start off with what Tom McGurk wrote in Ireland's Sunday Business Post:

Time to reclaim the land that is rightfully oursLast Thursday, a group of ten leading economists wrote to the Irish Times, arguing that some form of mortgage debt forgiveness was not only essential for our society, but also for the economy.

The group argued that, were mortgage debt forgiveness not introduced - and radical reform not introduced to our debt and bankruptcy laws - then our financial crisis would only deepen. At the core of their argument was the following assertion: ‘‘As there are three parties to the problem - the banks, the regulator (ie the state) and the individual - these three must also be part of the solution."

With the government having insisted on a year’s grace for home repossessions by the banks, we are currently in some sort of unreal financial hiatus. It means that the full dimensions of the crisis to come are still hidden.

But late next year, when property and water taxes have been introduced - and when interest rates begin to rise, as they surely must - then the personal debt crisis has the potential to become the most serious crisis in the history of the state.

If the banks attempt a process of mass repossession next year, then they must be met by organized citizens’ action. Boycotting was invented in 19th century Ireland, and the time to use it again may be now.

The problem here is that, if we restrict ourselves to looking at recent events, operations like QE2 and the impending bail-out of Ireland all play out against a backdrop that hasn’t changed one iota from that of earlier bailouts in the past three years, even if the media and public attention have shifted away from it. That is to say, while these measures are being presented as being beneficial for 'the people', they’re in actual fact the exact opposite.

If there’s one common theme in all of this, it's that the one and only haircuts involved involve taxpayers; they conveniently get to pay the entire bill.

Financial restructurings of bankrupt and failed institutions have routinely always, and should, involve and hurt everyone with "skin in the game". Hence, bondholders, stockholders, taxpayers et al should divide losses among them. And that’s what usually happens, or at least should happen. In the present situation, however, it does not.

Now we can argue that this has a lot to do with the fact that financial institutions have dramatically increased their level of political power in recent years, and that argument would most certainly be valid.

But there’s another, a "B", factor that comes into play, and though it's not entirely separate from the A factor, the political power grabbing, it's a new player introduced into the game.

If debt restructuring would follow its normal path, which would see all stakeholders take their losses, we'd see a problem emerge that past examples didn't have to deal with.

The kind of haircut that used to be seen as normal for parties such as banks and other financial institutions, and pension funds and more, - re: the US Savings and Loans crisis-, would today put many of these parties in a position where quite a few of them would be challenged to survive at all.

That is why the EU is negotiating with Ireland on the terms that it is, and that is why QE2 has taken the shape it has. The bottom line, which hasn't changed for three years, is that the debts inside the vaults of these parties, the major global financial instituitions, are so great that any disturbance to the established non-mark-to-market Wile E. Coyote status quo instantly threatens to topple them.

And no living politician will volunteer to initiate a potential domino reaction that may see either their national or even global banks struggling to live another day. When faced with the choice right now, every Tom Dick and Harry dreaming of political power will side with the banks, and choose to spend your future tax revenues to save the banks as well as their own political future. None among them will say: "I can’t vote this or that way, because my conscience won’t let me, but this means you won’t have access to your bank accounts anymore as per tomorrow morning."

For Ireland, and the Irish people, this is something like: "sorry that you have to be first in line, but we need to set an example". The EU will take over Irish fiscal and economic sovereignty, and the first thing that will go is the tax advantages for foreign corporations. And frankly, I have to say I never really got those: if and when you’re part and parcel of a union such as the EU, you can’t really hope to base your prosperity on handing Intel and Microsoft conditions they could otherwise only find in Vietnam, and still hope no-one in that union doth protest.

A large part of the blame lies within Ireland itself. It had and has blatant corruption, and it has scores of politicians that are either for sale or too dumb to put their socks on the right foot in the morning, or -which seems quite likely- both.

But the thing is that it’s not the Irish people, even if they might have known better when Dublin real estate prices increased five- or tenfold. The Irish have through their history gone through literally hundreds of years of hardship the kind of which is presently seen only in places like Bangla Desh or Rwanda, and it very much looks like that's where the country is heading once again.

And before, wherever you are on the globe, you elect to count your blessings, beware: most of you will see your politicians, too, choose to save their banks rather than their people, and you too will follow the Irish down that same steep slope. It’s the old "be careful what you wish for" theme.

If Ireland should mean anything to the rest of us today, and in the days going forward, it's as a big bold read flashing warning sign: you're next in line.

Debt crisis team heads for Dublin

by Peter Spiegel, George Parker and David Oakley - Financial Times

European Union authorities and Dublin have agreed that a team of EU and International Monetary Fund officials will visit Ireland for what senior European officials called a “short and focused discussion” on the country’s debt crisis, the clearest sign yet that a bail-out for the country’s ailing banks is imminent. There were also signs that the UK, Ireland’s neighbour but not a member of the eurozone, was considering providing its own direct loans as part of the aid effort.

George Osborne, UK chancellor, was considering billions of pounds in loans to help the bail-out, a move likely to be more palatable to his Conservative party’s Eurosceptic members than joining in an EU package. Before heading to a meeting of European finance ministers later on Wednesday Mr Osborne said: “Britain stands ready to support Ireland in the steps that it needs to take to bring about stability.”

Although officials in Brussels on Tuesday night refused to term the visiting group an official assessment team to prepare for a rescue, it will include personnel from the same three agencies – the IMF, European Central Bank, and European Commission, the EU’s executive branch – that were sent to Athens earlier in the year as part of Greece’s bail-out. “This can be regarded as an intensification of preparations of a potential programme in case it is requested and deemed necessary,” said Olli Rehn, the EU’s top economic official, speaking after a Brussels summit of finance ministers from the 16 countries that use the euro.

Brian Lenihan, the Irish finance minister, told reporters following the meeting that it was “not inevitable” that the country would require a bail-out, but said the talks would begin later this week. “I’m not going to impose timelines, but this is urgent,” Mr Lenihan said of the new talks. “We do have to examine how security and stability can be brought into the system.” The minister told Irish broadcaster RTE on Wednesday morning that the government would “fully engage with the process”. “[We will] work with the mission to ensure that everything possible is done to secure the Irish banking system,” he said.

However he stressed that there was “no question of loading on to the Irish sovereign and the Irish state some kind of unspecified burden”. “That’s why the government took great care not to make a formal application at this stage but to engage in intensive discussions to see exactly what the options are ... and should be taken at this stage.” The talks are scheduled to start on Thursday, Mr Lenihan said.

Separately, clearing house LCH.Clearnet raised its margin requirements to trade Irish debt to 30 per cent of net position. The last time LCH increased the same margin, a week ago, it led to a flurry of selling as traders were forced to close positions, but Wednesday’s moved appeared to have little impact on Dublin’s paper. The agreement comes after days of speculation over whether Ireland would accept an EU-led aid package, with Dublin resisting entreaties from European officials, particularly from the ECB, to take aid and stabilise financial markets. Irish and other “peripheral” EU bonds have been beaten down in recent weeks, making it nearly impossible for at-risk economies to borrow money at reasonable rates and pushing the eurozone to the verge of another debt crisis.

In an address to the Irish parliament, Brian Cowen, prime minister, acknowledged that Ireland had to help calm the debt markets, but added: “This is not an insurmountable challenge.” Christine Lagarde, the French finance minister, said she believed the Irish talks would go more smoothly than those leading up to EU-led Greek bail-out. “The big difference with the previous crisis is that we are fully equipped,” Ms Lagarde said. Although Ireland has not made a request for aid, Mr Osborne arrived in Brussels on Tuesday night for a full Ecofin meeting amid growing expectation that Britain will play its part in a rescue alongside other EU countries and the IMF.

UK Treasury officials stressed no request had so far been received from other eurozone countries for the UK to make bilateral loans to Dublin, but they refused to rule them out. A request for British participation in an Irish rescue effort would prove highly controversial with Eurosceptic Conservative MPs. Senior Conservatives believe that loans to Ireland – a country with which Britain has a land border and strong financial and trade ties – would be easier to sell to Tory MPs if they were not part of an EU rescue. “Tory backbenchers would not be opposed to UK assistance to Ireland but they are worried about a European mechanism,” said one leading Tory.

Britain is already committed to about £6bn in contingent liabilities if Ireland approached the €60bn European financial stability mechanism but the UK is not part of a wider €440bn European financial stability facility. Tory eurosceptics are already voicing deep concern over UK taxpayers underwriting a eurozone bail-out, but their anger might be diluted if British assistance was made directly or through the IMF. Douglas Carswell, a Tory MP, said on his blog: “I wonder what excuses they’ll be using for spending our money on bailing out the euro? What blah blah sound bites will the politicians be rehearsing to justify another EU bill?”

Ireland resists humiliating bail-out as UK pledges £7bn

by Bruno Waterfield - Telegraph

Brian Cowen, the Prime Minister, dismissing the term 'bailout' as pejorative, said: "There has been no question of the government ... [being] in a negotiation for a bail-out." Instead Ireland committed itself to working with a European Union-IMF mission on urgent steps to help its stricken banking sector. Financial markets appeared unimpressed by Dublin's decision to reject assistance, with the premium investors charge for holding Irish 10-year bonds rather than German Bunds rising to a near-record 595 basis points.

The cost of insuring against default by Ireland jumped, with five-year credit default swaps widening by 25 basis points on the day to 545 bps, while those for Spain and Portugal also rose - a sign of the contagion that EU policymakers fear most. George Osborne, the British Chancellor, has pledged British support of up to £7bn for an EU bail-out of Ireland and its banking sector. The Chancellor arrived in Brussels for a meeting of EU finance ministers aware that exposure of British financial institutions to Irish banks is £140bn.

“Ireland is our closest neighbour. And it's in Britain's national interest that the Irish economy is successful and we have a stable banking system,” he said. “Britain stands ready to support Ireland.” Britain is not part of the 16 member eurozone but is a member of a £51bn “European Financial Stabilisation Mechanism” that will be used to aid Ireland. The European Commission said a potential British role was “under discussion” as EU and IMF officials headed to Dublin today to carry out “intensified, short and focused” preparations for a bailout of Ireland. Officials said that multi-billion cash injection could be ready within “five to eight days” of a eurozone decision to step into save Irish banks.

The intervention is climb down for Ireland after other eurozone countries pushed it into accepting an intervention against its wishes. Brian Lenihan, Irish finance minister, insisted that a bail-out was not inevitable but admitted that Irish sovereignty was compromised by its membership of the euro. “When you borrow, you lose a little bit of your sovereignty, no matter who you borrow from,” he said. “Sovereignty, in my view in a European context, is shared. We have a duty to the eurozone as our currency and it is Ireland’s currency as much as it is Germany’s or France’s. We have a duty to sustain the stability of the eurozone. Ireland is the zone of attack in the eurozone.”

Mr Lenihan said talks with the IMF-EU team would begin on Thursday. He set out his stall ahead of the talks by dismissing suggestions that Ireland should raise its ultra-low 12.5pc corporation tax rate to help cut its debt. "Of course our corporate tax rate is safe," he said.

However, higher-tax countries, including Britain, have long seen the Irish rate as a form of unfair competition and many commentators believe the raising the rate will be a conditions attached to any rescue package - be it for the country or just the banks. The European Central Bank and other euro currency members have been concerned that that Irish banks have been increasingly dependent on support and putting Ireland under intense pressure to give to controversial aid conditions that will reduce the country economic independence.

No details of a rescue emerged at meeting of eurozone ministers last night but it is likely that a bail-out will be choreographed with an Irish four year spending plan and austerity programme which could be as early as next week. Jean-Claude Juncker, Luxembourg’s Prime Minister and chairman of the eurogroup, said he expected a decision on the bail-out “within the coming days”. “Market conditions have not normalised and pressures remain, giving rise to concerns that further reforms and stabilisation measures may be appropriate,” he said.

EU economics commissioner Olli Rehn said the talks would centre in the main on a package to stabilise Ireland’s banks and said it would be available if the Government choose to seek aid. Olli Rehn, the European economic and monetary affairs commissioner, said the EU-IMF teams sent into Ireland would have an “accent on restructuring its banking sector”. “This can be regarded as an intensification of preparations for a potential programme in case it is requested and deemed necessary,” he said. “This is a time for cool heads and clear determination to take the necessary decisions to that effect both at the EU level and in every member state.”

The Irish government has insisted that it can afford to repay its record debts, despite having an annual deficit equivalent to almost a third of the size of its economy. The growing market turmoil surrounding Ireland has also threatened to push Spain and Portugal into crisis. The cost of Spanish government borrowing rose sharply on Tuesday. A full EU-IMF bail-out would mean Ireland losing key areas of political and economic sovereignty. This would be deeply controversial and could cost the Irish government its majority.

Senior EU figures have suggested that Ireland should increase its low corporate tax rates, regarded by the Irish as key to Ireland’s economic recovery. Herman Van Rompuy warned on Tuesday, that the deepening debt crisis in Ireland which has spread to other parts of the eurozone has left the single currency and EU fighting for their “survival”. “We are in a survival crisis,” he said. “We all have to work together in order to survive with the euro zone because if we don't survive with the euro zone, we will not survive with the EU.”

Irish Obstinacy Unsettles the Euro Zone

by Carsten Volkery - Der Spiegel

Ireland's government insists it needs no assistance -- and the euro has become highly unstable as a result. Euro-zone finance ministers were unable to persuade Dublin otherwise at Tuesday's crisis meeting in Brussels. Their half-hearted assurances of help are unlikely to calm financial markets.

The rhetoric sounded strangely familiar. There is no Europe without the euro, German Chancellor Angela Merkel had said ahead of Tuesday's meeting of the 16 euro-zone finance ministers in Brussels. The EU was in a "survival crisis," seconded European Council President Herman Van Rompuy. Meanwhile Luxembourg's Prime Minister Jean-Claude Juncker, the head of the Eurogroup of finance ministers, asserted that they would defend the euro by any means.

Europe's leaders had used precisely such words back in May, before they decided on a €110 billion ($150 billion) rescue package for Greece. Are they about to do the same thing for Ireland? Apparently not. When the next candidate for a bailout was discussed at the late-night meeting on Tuesday in Brussels, the finance ministers appeared unwilling to put their money where their mouths are. Instead of announcing a concrete aid figure for Ireland, the finance ministers were basically content to repeat -- for the umpteenth time -- that the EU would help Ireland in an emergency.

No Figures Given

Merkel also attempted to strike a calming note. "I do not believe that the euro zone is at risk, but we are experiencing turbulence and situations of a kind that I would never have dreamed of a year and a half ago," she told the German public broadcaster ARD. "The most important thing is that, apart from the rescue measures that have been agreed to, we coordinate our economies better with each other."

The EU and the International Monetary Fund (IMF) will now send a larger group of experts to Dublin to work out a support package for the Irish banks, as a precursor to a possible bailout. "This can be regarded as an intensification of preparations of a potential program in case it is requested and deemed necessary," European Monetary Affairs Commissioner Olli Rehn said after the meeting. He did not, however, give details or name any figures. Neither did other participants in the meeting. Hence the question remains open why a second emergency plan is required, given that the EU's €750 billion stabilization fund has been available since the Greek crisis and could be used to help Ireland.

After the meeting, the ministers went to bed without having reached any concrete decisions and were presumeably awaiting the opening of financial markets on Wednesday morning with a certain amount of trepidation. They must have been asking themselves if the markets would believe their assurances, or if they would send the euro into turmoil again.

Fears of Bailout Stigma

The reason for the vague statements from Brussels is simple. The Irish government does not want help. It took a firm line at the meeting, despite pressure from the other troubled euro-zone countries -- Portugal, Spain and Greece -- and the European Central Bank (ECB). They are all concerned that the euro will falter once again and that yields on bonds issued by all the euro zone's problem countries will rise dramatically.

Ireland is nevertheless insisting it does not need the EU's aid. It does not need to refinance its government bonds on the markets until next summer, and it hopes that the worst will be over by then. Irish Finance Minister Brian Lenihan told his colleagues on Tuesday that he did not have a mandate from the Irish government to negotiate an emergency package. The government in Dublin fears the stigma that would be attached to a bailout. The bond markets would effectively be closed to the country for years, and the EU and the IMF would have even more power to dictate the Irish government's policies than is already the case.

The other euro-zone finance ministers can not force Ireland ministers to accept the money. They are now hoping that Dublin will have a change of heart over the coming days. In a concession to the conservative Prime Minister Brian Cowen, they talked of preparing an emergency plan for the ailing Irish banks as an alternative to a bailout for the state. The Irish government has now a few days to make a decision, Juncker said. The Irish government has set up a deposit guarantee scheme for six of the country's financial institutions, the most prominent being the nationalized Anglo Irish Bank. As a result, Ireland's deficit has temporarily ballooned to 32 percent of its gross domestic product -- over 10 times as much as allowed under the EU's Stability Pact.

A Continent Divided

The disagreement of the finance ministers illustrates just how far apart the euro-zone countries are in their positions on how to deal with the crisis:

- Portugal, Greece and Spain accuse the Irish government of unsettling the financial markets with its obstinacy and driving up interest rates.

- Together with Ireland, they accuse Germany of having caused the latest debt crisis through its insistence that private-sector creditors take their share of losses in future debt crises.

- Germany in turn sees itself as the guardian of the long-term stability of the euro zone and wants to ensure that taxpayers are not left to foot the bill in future crises.

- The ECB is insisting that Ireland should avail itself of the EU's stabilization fund, so that it can roll back its existing emergency support for the country. In October, the ECB made €130 billion in emergency loans available to the Irish banking system -- one-fifth of the total funds that the central bank currently has on loan to all euro-zone banks. Without this help, the Irish banking system would collapse. The ECB argues that the current situation is not sustainable in the long run.

High Hopes

The financial markets will hardly be impressed by the half-hearted assurances made by the euro-zone finance ministers. Besides, expectations for Tuesday's meeting had been ratcheted up too high over the past few days. As a precaution, several representatives of the euro zone made statements emphasizing that an aid package for Ireland would be available within days if a call came from Dublin.

The Irish government's resilience will be tested again in the coming days. Other European countries will try to entice it with promises. According to French Finance Minister Christine Lagarde, bilateral aid would be possible, involving Britain alongside the euro-zone countries. According to the Financial Times, the British government is considering providing assistance to the tune of several billion pounds. So far, the Irish government has continued insisting that it will manage by itself. It is currently working on its four-year budgetary plan, which is expected to be presented next week. The plan is supposed to calm the markets. Many observers fear that hope will be in vain.

The horrible truth starts to dawn on Europe's leaders

by Ambrose Evans-Pritchard - Telegraph

The entire European Project is now at risk of disintegration, with strategic and economic consequences that are very hard to predict. In a speech this morning, EU President Herman Van Rompuy (poet, and writer of Japanese and Latin verse) warned that if Europe’s leaders mishandle the current crisis and allow the eurozone to break up, they will destroy the European Union itself. “We’re in a survival crisis. We all have to work together in order to survive with the euro zone, because if we don’t survive with the euro zone we will not survive with the European Union,” he said.

Well, well. This theme is all too familiar to readers of The Daily Telegraph, but it comes as something of a shock to hear such a confession after all these years from Europe’s president.

He is admitting that the gamble of launching a premature and dysfunctional currency without a central treasury, or debt union, or economic government, to back it up – and before the economies, legal systems, wage bargaining practices, productivity growth, and interest rate sensitivity, of North and South Europe had come anywhere near sustainable convergence – may now backfire horribly.

Jacques Delors and fellow fathers of EMU were told by Commission economists in the early 1990s that this reckless adventure could not work as constructed, and would lead to a traumatic crisis. They shrugged off the warnings. They were told too that currency unions do not eliminate risk: they merely switch it from currency risk to default risk. For that reason it was all the more important to have a workable mechanism for sovereign defaults and bondholder haircuts in place from the beginning, with clear rules to establish the proper pricing of that risk.

But no, the EU masters would hear none of it. There could be no defaults, and no preparations were made or even permitted for such an entirely predictable outcome. Political faith alone was enough. Investors who should have known better walked straight into the trap, buying Greek, Portuguese, and Irish debt at 25-35 basis points over Bunds. At the top of boom funds were buying Spanish bonds at a spread of 4 basis points. Now we are seeing what happens when you build such moral hazard into the system, and shut down the warning thermostat.

Mr Delors told colleagues that any crisis would be a “beneficial crisis”, allowing the EU to break down resistance to fiscal federalism, and to accumulate fresh power. The purpose of EMU was political, not economic, so the objections of economists could happily be disregarded. Once the currency was in existence, EU states would have give up national sovereignty to make it work over time. It would lead ineluctably to the Monnet dream of a fully-fledged EU state. Bring the crisis on.

Behind this gamble, of course, was the assumption that any crisis could be contained at a tolerable cost once the imbalances of EMU’s one-size-fits-none monetary system had already reached catastrophic levels, and once the credit bubbles of Club Med and Ireland had collapsed. It assumed too that Germany, The Netherlands, and Finland would ultimately – under much protest – agree to foot the bill for a ‘Transferunion’.

We may soon find out whether either assumption is correct. Far from binding Europe together, monetary union is leading to acrimony and mutual recriminations. We had the first eruption earlier this year when Greece’s deputy premier accused the Germans of stealing Greek gold from the vaults of the central bank and killing 300,000 people during the Nazi occupation.

Greece is now under an EU protectorate, or the “Memorandum” as they call it. This has prompted pin-prick terrorist attacks against anybody associated with EU rule. Ireland and Portugal are further behind on this road to serfdom, but they are already facing policy dictates from Brussels, but will soon be under formal protectorates as well in any case. Spain has more or less been forced to cut public wages by 5pc to comply with EU demands made in May. All are having to knuckle down to Europe’s agenda of austerity, without the offsetting relief of devaluation and looser monetary policy.

As this continues into next year, with unemployment stuck at depression levels or even creeping higher, it starts to matter who has political “ownership” over these policies. Is there full democratic consent, or is this suffering being imposed by foreign over-lords with an ideological aim? It does not take much imagination to see what this is going to do to concord in Europe.

My own view is that the EU became illegitimate when it refused to accept the rejection of the European Constitution by French and Dutch voters in 2005. There can be no justification for reviving the text as the Lisbon Treaty and ramming it through by parliamentary procedure without referenda, in what amounted to an authoritarian Putsch. (Yes, the national parliaments were themselves elected – so don’t write indignant comments pointing this out – but what was their motive for denying their own peoples a vote in this specific instance? Elected leaders can violate democracy as well. There was a corporal from Austria … but let’s not get into that).

Ireland was the one country forced to hold a vote by its constitutional court. When this lonely electorate also voted no, the EU again disregarded the result and intimidated Ireland into voting a second time to get it “right”. This is the behaviour of a proto-Fascist organization, so if Ireland now – by historic irony, and in condign retribution – sets off the chain-reaction that destroys the eurozone and the European Union, it will be hard to resist the temptation of opening a bottle of Connemara whisky and enjoying the moment. But resist one must. The cataclysm will not be pretty.

My one thought for all those old friends still working for the EU institutions is what will happen to their euro pensions if Mr Van Rompuy is right?

Europe seems at loss to stop rot

by Paul Taylor - Reuters

Despite public assurances of unity and determination, it’s not clear that eurozone finance ministers know how to stop the rot gnawing away at the 16-nation European currency area. Ireland, the latest member to come under intense bond market pressure, agreed on Monday to discuss with an EU-ECB-IMF team how to stabilise its state-guaranteed banks but continues to resist applying for the kind of state bailout granted to Greece.

Even if, as seems likely, Dublin accepts an international rescue after more face-saving words, analysts increasingly doubt that will stop contagion spreading to fellow weakling Portugal and, more ominously, perhaps to the much larger Spain. “In practice, hopes that Ireland can be ’ring-fenced’ are unlikely to succeed,” Citi economists Juergen Michels, Giada Giani and Michael Saunders wrote in a note to clients.

In what can become a self-sustaining frenzy, investors bid up the borrowing costs of troubled countries on the bond market until they reach an unsustainable level when a government needs to raise money or roll over expiring debt. The European Union stemmed the first wave of debt crisis in May with “shock and awe” tactics by rescuing Greece along with the International Monetary Fund and creating a US$1-trillion financial safety net for other euro zone states in distress.

Six months later, the deterrent effect of the 440 billion euro European Financial Stability Facility (EFSF), the main component of that contingency fund, which EU officials said they believed would never need to be used, seems to have worn off. German Chancellor Angela Merkel and European Commission President Jose Manuel Barroso played down any sense of a renewed eurozone crisis this week, saying all the necessary instruments were now in place in case a country needed help.

But with typical European cacophony, the man who chairs EU summits and heads a task force on reforming euro zone economic governance, Herman Van Rompuy, undermined such soothing talk by saying the currency bloc was now in a “survival crisis.”

Markets are concerned not just by the scale of deficits, public and private debts and economic contraction or stagnation around the euro zone periphery, but also by Germany’s campaign for the EU to make bond holders share with taxpayers the pain of any future debt restructuring. “The successful ring-fencing of Greece owed much to the fact that the EFSF was created at the same time, plus strong political commitments that no euro area sovereign would be allowed to default,” the Citi economists wrote. “That commitment has been greatly weakened, given Germany’s recent insistence on the need for a sovereign default mechanism in the future.”

Assurances by the EU’s big five last week that this would only apply to debt issued after mid-2013 and all existing bonds were safe failed to calm investors trying to reprice the risk of peripheral eurozone government debt. Berlin may have backed off from its call for private creditors to take a “haircut” on the value of their holdings of a distressed state’s debt, but months of uncertainty lie ahead before the EU agrees on a debt resolution mechanism and all 27 member states ratify the necessary treaty amendment.

Diplomats say Merkel cannot climb down from her core demand both due to domestic political pressure and because the German Constitutional Court may otherwise rule the existing EU rescues incompatible with the treaty’s “no bailout” clause. Meanwhile, Austria’s threat on Monday to delay its share of the next tranche of emergency loans to Greece because Athens has not met the agreed deficit reduction target has highlighted the complexity of the euro zone-IMF bailout mechanism.

Recipients are potentially at the mercy of 15 individual governments — some of them fractious coalitions with restive parliaments — as well as being subject to decisions taken in Brussels, Frankfurt and Washington. Slovakia, the newest and poorest member of the eurozone, refused to take part in the 110 billion euro rescue for Greece, declining to lend money to a country wealthier than itself. The public backlash in wealthy, fiscally conservative Germany and the Netherlands against bailing out Greece is only likely to grow if additional states have to be assisted.

Radical Solutions

Each eurozone struggler’s case is different. Ireland and Spain had healthy budgets and below-average public debt before real estate bubbles burst in 2007-8, leaving huge private debts, mass unemployment and a gaping hole in government revenues. Ireland has been dragged down by its banks’ reckless property lending, while EU stress tests in July showed Spain’s biggest banks remain healthy and Madrid has begun to isolate and resolve problems in its weaker savings banks. Portugal has suffered an inexorable loss of competitiveness since in joined the euro at its creation in 1999.

Back-of-the-envelope calculations on the volume of emergency loans required for Ireland and Portugal suggest each could need up to 100 billion euros over three years, market analysts say. The EFSF, and a more readily accessible 60 billion euro European Financial Stability Mechanism, should be able to cover those needs with the IMF lending up to a quarter of the total. However a financial rescue for Spain, if that were to become necessary, would pose a challenge of a different dimension.

Some economists are urging radical action that seems politically unrealistic — pre-emptive debt restructuring by the most indebted states, large-scale sovereign bond purchases by the European Central Bank or big fiscal transfers from richer to poorer euro zone countries. In May, the EU briefly managed to get “ahead of the curve” in its response to the crisis. But there is little sign that its current course can restore confidence in the markets.

“Unless the EU changes track and agrees to make the EFSF permanent and the ECB steps up its purchases of the hard-hit countries’ government bonds, investors will believe that default is inevitable and demand correspondingly punitive interest rates,” said Simon Tilford, chief economist at the Centre for European Reform in London. “Contagion to other member states will be all but inevitable. If, and when, it reaches Spain, the crisis risks spiralling out of control.”

Austria says Greece will have to wait for next pay out, EU denies delay

by Sarah Harman - AP

Austria says it won't hand over its share of the funds for the next installment of Greece's 110 billion euro bailout until Greece fufillls its side of the bargain. Greece's 2010 deficit is even higher than thought. Austrian Finance Minister Josef Proell announced Wednesday that the decision to grant the delay was made on the sidelines of the EU finance ministers' meeting in Bruessels on Tuesday night. Proell said Austria would not release its share of the money because Greece had not fulfilled the requirements of the bailout agreement.

However, the EU has denied that the next loan payout will be delayed. The office of the EU's monetary affairs chief refuted Austria's claims, saying "it has always been the case that the actual release of the third tranche should be taken in December and that the release will be in January."

The European Union and the International Monetary Fund (IMF) agreed to lend Athens 110 billion euros ($150 billion) earlier this year to save the debt-wracked nation from bankruptcy. The money is to be doled out over three years, in accordance with the country's progress in reducing its budget deficit. In return, the Greek government of Prime Minister Giorgos Papandreou agreed to enact drastic austerity measures in order to get the deficit under 3 percent of gross domestic product (GDP) by 2014.

On Monday the European statistics agency Eurostat announced that Greece's 2010 deficit would exceed earlier forecasts, climbing 2 points to 15.4 of GDP, almost 2 points higher than the previously indicated 13.6 percent.

Time to reclaim the land that is rightfully ours

by Tom McGurk - Sunday Business Post

Ireland invented the boycott during the land wars, and perhaps it is time to take this effective weapon of resistance down from the thatch to deal with repossessions and resales Despite the spiralling economic crisis we are in, there was, last week, an epiphany at a small auction in Co Meath.

A 67-acre farm in Crossakiel, which had been repossessed by ACC bank, was up for sale. Despite a reasonable attendance by local farmers at the auction, there was only one derisory bid of €1.

There was, according to some present, ‘‘an atmosphere’’ in the room, and the auctioneer later told the Irish Times that ‘‘there was no question but that people weren’t bidding because it was being sold by the bank’’.

At one stage, one person present questioned whether the land was being sold with the goodwill of the owner - and was told that the bank had the authority to sell the land.

The owner of the land had reached this financial crisis after using the land to raise funds for a property development which then crashed. The farm remains unsold.

It is not difficult to imagine the historical ghosts which haunted that Meath auction room, and I make no excuse for returning yet again to the personal debt crisis that I have been writing about for some weeks now.

One result of this issue has been the emergence of the New Beginning organisation, a group of some 50 barristers, businesspeople and citizens who are prepared to give free legal support to those facing repossession. And three cheers for them.

The failed land sale in Meath is yet another sign that, if the banks think they can regain the high financial ground over the thousands to whom they over-loaned in a reckless fashion by repossessing land, they may have to think again.

This applies equally to the government, which scooped up so many million euro in stamp duty.

Given Ireland’s history, those silent farmers in the auction room in Co Meath last week would have had a far better sense of where all of this will lead than the men running our banks. If the banks and the political and financial establishment think that our current bank repossession methods and laws on debt and bankruptcy are adequate for the forthcoming crisis, they had better think again. Parallels with the land and eviction crisis of the 19th century are beginning to look pertinent, particularly when one considers that, by late next year, almost 20 per cent of Irish home ownership may be in negative equity.

At the outset of this crisis, most people didn’t really understand what had happened and were prepared to let the government get on with saving the banks since they were essential - so the government argued - to safeguarding our economic future. Well, we did that, but the economy is still in crisis.

As the months have passed, the government’s financial targets have been missed, the debt crisis has grown and the public mood has changed. The realisation that thousands of families in this country are so in debt to the banks, that their children and unborn children will be paying it off, is slowly sinking in.

The auction in Meath last week may prove to have been be a significant turning point.

There have been two recent significant interventions in this debate. Professor Morgan Kelly of UCD warned in an Irish Times article that we were headed to what he depicted as a new type of land war between those who could pay their mortgages and those who could not.

He summed up the public mood as follows: ‘‘The perception growing among borrowers is that, while they played by the rules, the banks certainly did not, cynically persuading them into mortgages that they had no hope of affording.

‘‘Facing a choice between obligations to the banks and to their families’ mortgage or food, growing numbers are choosing the latter," he wrote.

Last Thursday, a group of ten leading economists wrote to the Irish Times, arguing that some form of mortgage debt forgiveness was not only essential for our society, but also for the economy.

The group argued that, were mortgage debt forgiveness not introduced - and radical reform not introduced to our debt and bankruptcy laws - then our financial crisis would only deepen. At the core of their argument was the following assertion: ‘‘As there are three parties to the problem - the banks, the regulator (ie the state) and the individual - these three must also be part of the solution."

With the government having insisted on a year’s grace for home repossessions by the banks, we are currently in some sort of unreal financial hiatus. It means that the full dimensions of the crisis to come are still hidden.

But late next year,when property and water taxes have been introduced - and when interest rates begin to rise, as they surely must - then the personal debt crisis has the potential to become the most serious crisis in the history of the state.

If the banks attempt a process of mass repossession next year, then they must be met by organised citizens’ action. Boycotting was invented in 19th century Ireland, and the time to use it again may be now.

Like the Tea Party movement in the US, which was organised on the internet and through websites and social networking, people in Ireland now have the organisational resources in their living rooms to bring the full power of the boycott against bank repossessions and attempted resales.

Boycott.ie - when it is set up - should be the rallying point to help those facing eviction. It could lead to the organised boycott of anyone involved in the eviction and, most especially, the auction of repossessed property. In the forthcoming general election, independent candidates fighting the repossession crisis should be put up through Boycott.ie.

It seems that, in this crisis, everyone except the taxpayers and homeowners of Ireland were allowed to make up the rules as they went along.

Now is the time for the citizens of the Republic to take back control of their lives and their finances and, like the Meath farmers, bond together in an unbreakable moral crusade for justice.

Our great-grandfathers and great-grandmothers did this before, and we can do it again.

Ghost estates and broken lives: the human cost of the Irish crash

by Michael Savage and Donald Mahoney - The Independent

They stand empty across Ireland: 300,000 unoccupied homes, a silent reproach to those who built them believing that the country's economic boom would never end. As Europe's finance ministers laboured in vain to reach an agreement on how to ease Ireland's economic misery last night, the so-called ghost estates were an awful reminder that the "survival crisis" the politicians were warning was under way had already hit ordinary people.

Dave O'Hara was one of those who bought into the "Celtic Tiger" at the beginning of the decade, eschewing a seven-generation family tradition of carving headstones in favour of a piece of the country's building boom. He founded a firm that constructed bespoke windows and doors for the thousands of upscale homes being built. The firm grew into a multimillion-euro enterprise, until the recession – and the collapse of the building industry – hit in September 2008. Now his company is in liquidation, and Mr O'Hara, 41, who has one child, is on the dole. He owes the Bank of Scotland more than €1m (£850,000).

Like many others, Mr O'Hara's anger is aimed at the banks, which have already been bailed out and seem destined to force the government to seek further help of some kind from Ireland's European partners. "Everyone is responsible for their own actions, but the burden is being brought to bear on the people on the end of the line. In Ireland right now, it's better to owe €50m than €50,000. The people who have sinned the most are suffering the least," he said, sitting in his cottage along the borderlands between Leitrim and Sligo, in the boggy north-west of the country. "I don't know what's coming, but I know what we've got isn't going to stay. I've lost all faith and confidence in our system."

Not far from Mr O'Hara's home, the "ghost estates" are well-known eyesores along the rugged landscape. And the crisis that created them has hit not just the people who built them, but those who might once have expected to move in, as well. Hundreds of thousands of homeowners have already found themselves saddled with negative equity as a result of the crash, economists estimate, with as many as one in seven families affected. The toxic combination of the glut of house-building during Ireland's boom and the current dearth in demand means they have been lumbered with a property worth less than the loan they secured to buy it.

Personal indebtedness is also an issue, as are redundancy and the end of easy loans, meaning around 100,000 households are struggling to make regular repayments on the money they owe. And yet, house prices continue to fall precipitously. Together with slumping disposable incomes due to frozen wages and stubbornly high unemployment, still running at more than one in every eight adults of working age, many fear a social disaster is unfolding. Even for the few who have yet to feel the pinch from the crisis, its effects on families will be felt next week, when the Budget that was brought forward yesterday yanks a further €15bn out of the economy through major spending cuts and tax rises.

Many have taken drastic action already. With youth unemployment topping 30 per cent, some have already fled abroad to seek their fortune, or at least stay above the breadline.

The Economic and Social Research Institute think-tank estimates that the labour market will not pick up within the next two years, pushing as many as 100,000 people to seek work abroad. In a country of just 4.5 million, that would cause a dent in potential consumer spending, as well as a level of emigration-fuelled social upheaval reminiscent of the 1980s and after the Second World War.

In Dublin, ministers were maintaining a tough-talking stance, refusing to go cap-in-hand to the EU even as discussions were continuing in Brussels. There was a not-so-subtle resentment in the capital that a growing number of European players were insisting a bailout was the best option. Yesterday, Jean-Claude Juncker, the Luxembourg politician leading the group of euro-area finance ministers, said help was there if it was wanted.

There must be a bitter irony in it all for Mr O'Hara. While the Irish government is working hard to avoid calling on the ample help on offer, he continues to struggle. However, he is opposed to Ireland opting for an embarrassing bailout. "I use be to be pro-European," he said. "But my feeling now is that the solution can't come from Europe. It's akin to giving a credit card to a family already massively in debt. I think the banks need to collapse."

There are some who now want their leaders to swallow their pride and take the help on offer, however humiliating. "Maybe a bailout isn't such an bad thing," said Jackie McKenna, a sculptor in Manorhamilton, Co Leitrim. "It wouldn't be the end of the world. If we don't we won't get out of this. Something needs to be done. Businesses are closing and we need to do something."

Despite his plight, Mr O'Hara remains remarkably upbeat. "I'm actually excited for the future," he said, adding that his situation was a "time for reinvention". Now it can no longer rely on its building sector, the Irish economy will also have to undergo a similar, and painful, transformation.

Don’t blame the euro for Ireland’s mess

by Philippe Legrain - Financial Times

Sceptics of the euro see the Irish crisis as proof of the single currency’s folly. But while the eurozone needs reform, the notion that the euro is to blame for Ireland’s travails is simplistic. Even many euro supporters now regret that in the boom years the currency permitted huge capital flows from Germany and other surplus countries to Spain, Portugal, Greece, and Ireland. These imbalances, conventional wisdom has it, are unhealthy – and the European Union is now drafting rules to limit them.

Yet enabling capital to flow from one member country to another without exchange-rate risk is a key advantage of the euro. If this were possible globally, emerging economies would not feel compelled to amass huge reserves to protect against crises and could be net recipients of investment instead. When integrated financial markets work well, they offer investors higher returns, businesses cheaper finance and a better allocation of capital all around.

The problem is not that savings flowed from Germany to Europe’s periphery. It is that they funded property bubbles rather than productive investment. But the blame for that lies with herd-like investors, flawed banks and foolish governments, not the euro. After all, America, Britain, Iceland and other non-euro countries all had huge property bubbles too.

Granted, joining the euro did slash Irish interest rates, creating cheap borrowing that fuelled the boom. But at a macro level the Irish government could have tightened fiscal policy – in effect, run large budget surpluses. At a micro level, it could also have limited banks’ property lending – through higher, counter-cyclical capital requirements for instance – rather than encouraging it with tax breaks.

Ireland’s property bubble was particularly big. The value of its housing stock quadrupled in the decade to 2006, with construction swelling to an eighth of the economy. The price of a typical Dublin house shot up more than fivefold – and has since nearly halved. Such a property crash is inevitably painful. But it need not have led to a sovereign debt crisis. Ireland’s public debt was only 25 per cent of gross domestic product on the eve of the crisis, the lowest in the eurozone.

The government’s fatal mistake was stepping in to guarantee not just all the depositors of Irish banks but also all their bondholders. Now the bust banks’ huge losses are dragging down the Irish state with them. Had Britain’s recession worsened, the UK government might have ended up in a similar situation.

Only cheap finance from the European Central Bank has kept those bust Irish banks on life-support, until now. Outside the euro, Ireland would doubtless have suffered Iceland’s fate: its currency would have crashed and its central bank would have run short of foreign funds to keep its banks afloat. Far from precipitating the crisis, the euro has given Ireland vital breathing space. More’s the pity that the government has failed to make good use of it.

It is true that, outside the euro, Ireland would now enjoy a weaker currency. That could boost exports, and hence growth. But in very small open economies, devaluations tend to feed through rapidly into inflation, so the competitive boost might not have been that great. In any case, Ireland has already slashed wages and prices to restore competitiveness – in effect, an internal devaluation. And if it wished to cut unit labour costs further, it could reduce its high payroll taxes and replace the revenues with higher value added tax or a tax on land values.

Leaving the euro and reintroducing the punt is certainly not a solution, since Ireland would be incapable of repaying its euro-denominated debts in devalued punts. Nor, on its own, is an EU or International Monetary Fund “bail-out” – in practice, a loan at punitively high interest rates. That would merely postpone the crisis.

Irish taxpayers should not be bled dry to pay off investors – among them, European banks and American hedge funds – who gambled on lending to Irish banks. Instead those creditors should take a haircut, via a debt restructuring with the EU or IMF providing a bridging loan until Ireland has fixed its budget deficit. Ironically, it is Germany’s proposal that bondholders should lose out in future that brought this crisis to a head. It is such a good idea that it should be implemented now.

Anger at Germany boils over

by Peter Spiegel and Gerrit Wiesmann - Financial Times

When George Papandreou, the Greek prime minister, this week aired frustration with Germany for pushing the eurozone to the brink of another debt crisis, he was saying publicly what other senior European officials and diplomats have been saying privately for weeks. The drive by Angela Merkel, the German chancellor, to rewrite the European Union’s treaties to set up a new bail-out system for future Greek-like collapses – and her insistence that private investors bear more of the cost of such rescues – was quietly resented when she bulldozed it through last month’s summit of EU leaders.

But as bond markets have reacted and plummeted in the weeks since, that resentment has begun to boil over, with increasing accusations that Ms Merkel has put many of her fellow eurozone leaders in untenable positions in order to reinforce her own standing with German taxpayers. “They’re unprintable at times,” said Daniel Gros, director of the Brussels-based Centre for European Policy Studies, of the angry remarks he has heard aimed towards Berlin.

German officials insist their campaign to get private bondholders to shoulder more bail-out costs is not just about domestic considerations. The government is more concerned that the current system – which condemns well-managed states to bailing out badly managed ones – is unsustainable. But even some of those well-managed states have expressed anger at German tactics. Countries such as the Netherlands, Finland and Austria, all normally allies of Germany in economic governance issues, have raised questions about Berlin’s behaviour.

Anger first arose in October after Berlin cut a deal with France over the new bail-out system, even as it was working closely on economic reform issues with several of its allies among the northern, fiscally prudent caucus. Ever since the deal was struck, Germany has slowly lost support for its hardline stance on the new rescue mechanism and has been forced to back away from its original ideas about setting strict rules for private investors’ role in a bail-out “ex-ante”, or before a rescue even occurs. “Everybody should be more [of] an owner of this process; it shouldn’t just be Germany,” said Mikolaj Dowgielewicz, Poland’s EU minister.

Senior EU officials have become increasingly alarmed by the internecine sniping. Olli Rehn, the EU’s top economic official, on Tuesday called for leaders to “restore the sense of unity” and to end the “somewhat divisive tone in the public debate”. Several European officials said, however, that Germany was unprepared for the market’s angry reaction to the bail-out proposal and has since begun to backtrack. Two senior officials briefed on deliberations during the G20 summit in Seoul said a statement put out there by finance ministers of the EU’s five largest economies, in which they reassured bondholders that no current owner of debt would be forced to pay for a sovereign bail-out, was in part a concession by Berlin that it had overplayed its hand.

Mr Gros noted the dust-up is the second time Ms Merkel has pushed the eurozone into turmoil by digging in her heels on what, to her, is a principled stand against bailing out profligate member states. Earlier this year, Ms Merkel refused for months to offer concrete help for Greece until forced into action in May by an angry bond market. “That is the fundamental flaw in Merkel’s approach,” Mr Gros said. “What she somehow doesn’t get is that markets are not like political systems. They anticipate things. And they anticipate vaguely, not rationally.”

As the turmoil has gathered steam, German officials have insisted they are sympathetic with Ireland’s plight, particularly since Dublin was the first “peripheral” EU economy to slash budgets to try to get its fiscal house in order. Berlin has repeatedly insisted that they are not putting pressure on Ireland to accept EU aid. At the same time, Berlin has grown frustrated with Dublin’s handling of the crisis, believing Irish officials have failed to inform other eurozone members how they want to move forward. But Berlin appears prepared to tough it out, despite the criticisms from the likes of Mr Papandreou and Jean-Claude Trichet, the European Central Bank president who loudly opposed the German move to reopen the treaties for fear that the markets would react exactly as they have. German officials acknowledge that uncertainty over the future bail-out system is not ideal, but they insist they need more time to work out its details.

Sovereign Debt Crisis Redux? "Tough Medicine" Isn't Curing Europe's PIIGS

by Aaron Task - Tech Ticker

Financial markets were relatively and notably calm Monday despite the latest evidence of Europe's ongoing sovereign debt crisis. Irish officials repeatedly denied they are seeking a bailout, although major EU nations pledged to provide one at the G20 confab and are expected to follow through Tuesday when European Finance Ministers meet in Brussels.

The need for Ireland to get its financial house in order before its Dec. 7 budget announcement was highlighted by the latest news about Greece: Eurostat, the EU's official statistical organization, revised Greece's 2009 budget shortfall to 15.4% of GDP from 13.6% and vs. the EU's target of 3%.

"The revisions mean that Greece won't achieve the deficit targets it agreed to in return for the 110 billion euros ($150 billion) in EU-IMF emergency loans," Bloomberg reports. After Eurostat's revisions, the Greek Finance Ministry revised its own targets for 2010; Greece now projects debt will hit 144% of GDP in 2010 vs. 126.8% in 2009, which is already the highest in the EU. The Greek experience shows the paradox of austerity, especially in Europe's "Club Med" nations, where economic growth is traditionally heavily dependent on government spending.

The Paradox of Austerity

Cutting back on government spending means lower GDP, which means more spending on unemployment insurance and other social safety nets. "The medicine is pretty tough [so] you never really get the expected cuts in the deficit," notes Gary Shilling, president of A. Gary Shilling & Co. "The whole things feeds on itself." Yields on Greek debt rose Monday and the dollar hit a 6-week high vs. the euro in reaction. Amid hopes for a EU bailout, yields on Irish debt actually fell, albeit modestly and from record levels reached last week.

But overall, the financial markets reacted with a collective shrug, especially compared with the drama that unfolded last spring, Shilling, whose latest book The Age of Deleveraging is out this week, attributes the market's relative lack of concern about Europe to a "been there, done that" mentality among fund managers. "People say ‘I shouldn't have sold back then,'" he quips, and are putting their faith in the $1 trillion "euro TARP" put together by the EU-IMF.

In addition, the dollar has not strengthened dramatically in reaction to the EU crisis, as was the case last spring. But it's probably not a coincidence the stock market hit a bit of an air pocket last week as the dollar recovered from its pre-QE2 shellacking. Noting U.S. banks have about $750 billion of debt exposure to the EU and U.K., Shilling is less sanguine than most on Wall Street about goings on ‘over there.'

"Another sovereign debt crisis [is] possible," he says, wondering: "Is that euro bailout fund going to save the day - or will there be issues with implementing it?"

Of Course The Fed's Latest Plan Won't Work, Says Gary Shilling--We're Still Deleveraging!

by Henry Blodget - Tech Ticker

The theory behind most of what the Federal Reserve does to stimulate the economy is this: If we make money cheaper, people will borrow more of it--and then they'll start spending again.

That theory works in most recessions. When the economy begins to weaken, the Fed cuts interest rates. Banks, companies, and consumers see that it now costs less to borrow money to buy the things they want to buy. So they borrow money and buy them. And the economy strengthens again.

But we aren't in a normal weak economy, says economist Gary Shilling of A. Gary Shilling & Co. We're in a "deleveraging" economy. And that means that we will keep reducing our debts and borrowing, no matter how cheap money gets.

The key to understanding the difference between today's economic weakness and normal economic weakness, Gary says, is to look at the past 30 years. Beginning in 1982, Americans spent their way to apparent prosperity. Savings rates plummeted, as consumers spent almost everything they earned. Home equity withdrawals soared, as consumers realized they could use their rapidly appreciating houses as personal ATM machines. And, across the economy, total debt surged to a previously unheard-of 375% of GDP.

But now all those forces have reversed. Savings rates are climbing again, as consumers realize they have almost nothing left to retire on. Home equity withdrawals have ceased, because house prices have stopped appreciating and started falling (Gary thinks they'll fall another 20%). And consumers are looking at ways to reduce their debts, not borrow more money. These trends will continue for at least another decade, Gary Shilling thinks. He lays out this theory in his new book, "The Age Of Deleveraging."

The economy will grow in the next decade, Gary says, but it will grow much more slowly than it has grown in the past. Unemployment will remain high. Consumers will continue to be forced to embrace a new frugality. And no matter how cheap the Fed makes money, overall borrowing will continue to decrease. In the process of this, stocks will do poorly. House prices will fall another 20%. Only Treasury bonds will do well.

Middle Class in Crisis: America Needs a Reality Check

by Stacy Curtin - Tech Ticker

This country was built atop a strong middle class workforce and with the belief that anyone could aspire to achieving the American dream. But that foundation has been crumbling as middle class jobs -- manufacturing and service alike -- have been sent overseas in recent decades to low-cost labor markets. The 'Great Recession' isn’t helping this reality. Unemployment is stuck at 9.6% and record numbers have been out of the workforce six months or longer.

To top it off, CEO pay is on the rise -- even during this economic downturn -- and the wage gap between the rich and poor is the widest it has ever been. The percent of income garnered by the wealthiest 10% of U.S. households hit 48.2% in 2008, up from 34.6% in 1980, according to a recent report on income equality by the Congressional Joint Economic Committee. "Much of the spike was driven by the share of total income accrued by the richest 1% of households. Between 1980 and 2008, their share rose from 10% to 21%, making the United States one of the most unequal countries in the world."

And the income gap has actually widened since the financial crisis: According to the 2010 Census, the top 20% of workers -- those making more than $100,000 each year -- received 49.4% of all income generated in the U.S., compared with the 3.4% earned by those below the poverty line. As reported by Slate.com, that ratio of 14.5-to-1 was an increase from 13.6 in 2008 and nearly double a low of 7.69 in 1968.

This dire situation is not likely to get better any time soon, says Gary Shilling, president of A. Gary Shilling & Co, who predicts a prolonged period of slow economic growth and high unemployment. Even when thing do start to look up, "people are going to have to be much more realistic about their income levels." Shilling believes there will be jobs, but says, "People are going to have to work very hard to get trained and educated for jobs that do exist."

To that point, in his latest newsletter he makes the argument that a college degree is not for everyone, nor should you expect a degree to yield you a certain level of income. "Wouldn’t many be better off learning a skilled trade rather than facing bleak job prospects and lifetime student loan repayments after graduating from lesser institutions?," he writes.

Shilling, author of a new book "The Age of Deleveraging", is optimistic and believes that America is "still the land of opportunity" where the American dream can be achieved. But first, he says, Americans need to "align themselves with reality" and become comfortable with the fact that things are not going to be the same as during the "salad days" of the 1980s and 1990s.

U.S. Sets 50 Bank Probes

by Jean Eaglesham - Wall Street Journal

The Federal Deposit Insurance Corp. is conducting about 50 criminal investigations of former executives, directors and employees at U.S. banks that have failed since the start of the financial crisis. The agency responsible for dealing with bank failures is stepping up its effort to punish alleged recklessness, fraud and other criminal behavior, as U.S. officials did in the wake of the savings-and-loan crisis a generation ago. More than 300 banks and savings institutions have failed since the start of 2008, but just a few have led to criminal charges being filed against bank officials.

In an interview, Fred W. Gibson, deputy inspector general at the FDIC, which works with the Federal Bureau of Investigation to investigate crime at financial institutions, said the probes involve failed banks of all sizes in cities across the U.S. The FDIC is also ramping up civil claims to recover money from former bankers at busted lenders. He declined to identify any of the people or banks under investigation. "We anticipate results from our investigations, although we cannot predict when a particular case will reach a stage at which disclosure of specifics would be appropriate," Mr. Gibson said.

Pressure is high on regulators to identify and prosecute bankers for any wrongdoing that contributed to the largest number of failures in nearly 20 years. The September 2008 collapse of Washington Mutual Inc. was the biggest ever, with seven times the value of the assets that Continental Illinois Corp. had when it failed in 1984. The current epidemic of bank failures, including 146 so far this year, has deepened the nation's lending drought and left the industry's survivors with more muscle to squeeze customers.The S&L crisis of the 1980s and 1990s killed more than 1,800 institutions. From 1990 to 1995, federal officials prosecuted about 1,850 bank insiders. More than 1,000 officers, directors and other officials went to prison, and federal agencies collected $4.5 billion in professional-liability claims. In the current mess, no high-profile banker has been criminally charged in connection with a financial institution's demise, as Charles Keating was for fraud after American Continental Corp. failed in 1989. He served four years in prison and became synonymous with the S&L crisis.

FDIC officials also are ramping up efforts to use civil litigation to recover money from former bank officials. Hundreds of "demand" letters have been sent to former executives, directors and other employees, as well as their professional-liability insurers, putting them on notice of potential claims, the FDIC says. The agency's board has authorized the filing of lawsuits seeking to recover more than $2 billion from more than 80 officers and directors of failed banks. The total is up from about 50 approved suits as of last month, seeking more than $1 billion. "These numbers will continue to increase as time goes on," Richard Osterman, acting general counsel at the FDIC, said in an interview.

Authorization of a civil suit by the FDIC doesn't necessarily mean a case will be filed in court. Some former bank officers and directors could avoid being sued by negotiating settlements with the agency. So far, the FDIC has filed just two civil lawsuits related to recent failures. The agency is seeking $300 million in damages from four former executives of IndyMac Bancorp, the Pasadena, Calif., lender that sank in 2008. Eleven former directors and officers of Heritage Community Bank are being pursued for $20 million in damages related to the Glenwood, Ill., bank's collapse last year.

In a statement through their lawyers, the Heritage directors and officers said the FDIC's suit is "regrettable and wrong," adding that the agency is blaming them "for not anticipating the same market forces that also caught central bankers, national banks, economists, major Wall Street firms and the regulators themselves by surprise." The former IndyMac executives have denied wrongdoing. Kirby Behre of law firm Paul Hastings, who is acting for two of the former IndyMac directors, said: "Not only weren't they negligent, they were very diligent, and forces beyond their control were responsible for any losses."

Michael W. Fitzgerald, of Corbin, Fitzgerald & Athey LLP, which is representing the other two former IndyMac executives, said the "charges by the FDIC are completely false and we will vigorously defend them." The few criminal prosecutions of failed banks so far include Integrity Bank, which opened in Alpharetta, Ga., in 2000 and was seized by regulators in 2008. In July, two former executives pleaded guilty to fraud-related charges. Prosecutors alleged that the executives helped the bank's biggest customer use a construction loan to buy a private island in the Bahamas.

Mr. Gibson, the FDIC's deputy inspector general, said the roughly 50 criminal investigations under way typically relate to loan officers at the vice president or senior vice president level. Some of the probes involve higher-ranking officials, including former directors of failed institutions, he added. Suspected criminal activity is handled by the FDIC's office of investigations, usually working with the FBI. Recommendations for prosecutions are referred to the Justice Department. It often takes at least 18 months for legal action to be brought after a bank fails, meaning the surge in scrutiny is likely to continue for years. FDIC officials expect the failure wave to peak this year.

Some lawyers predict it will be hard to win convictions in many cases. "To prove criminal fraud and get a conviction, you really need the equivalent of stealing money from the vault,'' said Thomas Vartanian, a partner at law firm Dechert LLP. As a result, many civil and criminal defendants are "eventually likely to settle for money,'' he said. Federal officials also will have to overcome the likely defense that bank failures were caused by an unforeseeable real-estate bust. Samuel Buffone, a partner at law firm BuckleySandler LLP, said the most striking part of the FDIC's civil suit against former Heritage officers and directors is "the call for 20/20 hindsight.'' Mr. Buffone isn't involved in the case.

Mr. Osterman, the FDIC's acting general counsel, noted that the "same argument'' was used by defendants during the S&L crisis. "The courts didn't agree that time, and we don't expect they will this time,'' he said. "People are allowed to exercise business judgments. As long as they comply with their legal duties, they don't have anything to worry about.''

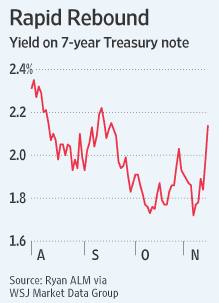

Bond Market Defies Fed

by Mark Gongloff - Wall Street Journal

Interest Rates Rise Despite Launch of Treasury Buying as Investors Take Profits

Bucking the Federal Reserve's efforts to push interest rates lower, investors are selling off U.S. government debt, driving rates in many cases to their highest levels in more than three months. The Fed's $600 billion program to buy Treasury bonds began late last week and is kicking into high gear this week, with the central bank buying up tens of billions of dollars of debt.

That should have driven prices up on those bonds and lowered their interest rates, or yields, which move opposite to the price. Instead, yields on almost every Treasury have been rising. The trend is a potential problem for the economy and the Fed. Rates had fallen sharply for months in anticipation of a Fed buying program, and in a short time much of that effect has been lost, spelling an unwelcome rise in borrowing costs throughout the economy.That could throw a wrench in what the Fed is trying to accomplish: to use low rates to encourage more borrowing and risk-taking by consumers, businesses and investors, thereby reviving growth. Still, it is far too early to declare that the Fed's plan is failing, and many rates remain near historic lows. And recent economic indicators, such as a Monday report on retail sales, suggest the economy continues to recover—which is the Fed's ultimate concern. "The recent run-up in bond yields is worrying to many," said Dan Greenhaus, chief economic strategist at Miller Tabak, a New York trading firm, but "you need to keep it in context of what happened before the Fed moved."

The Fed has only begun to put its plan in motion, and many investors are simply cashing out of lucrative bond-market bets they placed in the long prelude to the Fed's announcement of its purchasing program. Rates in most cases are still far lower than they were in the spring. Many observers still believe that the power of the Fed's printing press will prove overwhelming and economic growth disappointing. Both forces would eventually drive rates lower. Still, the recent move in rates has been jarring, raising some market worries that the Fed's program might be ineffective or backfiring. That could damage the Fed's credibility and raise borrowing costs broadly.

The recent move in interest rates may be due partly to the rosier tone of economic data recently, including data released on Monday that showed retail sales at their highest level since August 2008, the month before the fall of Lehman Brothers Holdings Inc. Sales rose 1.2% to $373.1 billion in October, compared with the month before. If the economy keeps improving, then the Fed's bond-buying program could end sooner than expected. That would be a much happier outcome for the Fed, though most economists still don't expect it. In an interview conducted last week, the Fed's new vice chair, Janet Yellen, defended the program, given an economic outlook that seemed to portend high unemployment, low inflation and lackluster growth for some time.

"I'm having a hard time seeing where really robust growth can come from," Ms. Yellen told The Wall Street Journal. "And I see inflation lingering around current levels for a long time." For now, the market seems to be driven mainly by the momentum of investors selling Treasury bonds to take a hefty profit after a rally that began in the spring, gathered steam as the economy weakened this summer and peaked amid talk of a new Fed buying program.

The 10-year Treasury note's yield, which influences most residential mortgage rates, surged on Monday to 2.911%, the highest since Aug. 5. Bond prices and yields move in the opposite direction. The 10-year note has now more than erased all of the beneficial effects of comments in late-August by Fed Chairman Ben Bernanke in Jackson Hole, Wyo., in which he first hinted at another round of bond-buying. And on Monday, the yield on the 7-year Treasury note rose to 2.14%, a 2-month high, despite the Fed's buying $7.92 billion in 6- and 7-year Treasury debt in the morning. Yields were more or less steady while the Fed was buying, but surged through the end of the day.

Several other factors have been working against Treasurys in recent days, including a backlash against the Fed's program overseas and among conservative politicians and economists in the U.S. Corporate bond issuance has been heavy since the Fed announced its bond-buying plan, which often leads to a temporary selloff in Treasurys. Moody's Investors Service may have contributed to the punishment late on Monday when it warned that an extension of Bush-era tax cuts, set to expire on Dec. 31, could harm the country's fiscal standing. Though the tax-cut issue isn't new, and though Moody's said the U.S. credit rating was secure, the bond market is sometimes sensitive to rating-agency comments.

The Fed plans to buy Treasurys every day this week, including 2- to 3-year notes on Tuesday and 8- to 10-year notes on Wednesday. It has committed to buying through the second quarter of 2011. It also plans to use whatever cash it gets from expiring mortgages on its balance sheet to buy still more Treasurys, taking total purchases closer to $900 billion, according to some estimates. That, Mr. Greenhaus notes, is more Treasury debt than China owned at the end of August. "Those screaming the end of the bond-market rally might be better served by waiting just a bit longer," he said.

California Will Default On Its Debt, Says Chris Whalen

by Henry Blodget - Tech Ticker

Municipal bonds have plummeted in recent days, as investors have suddenly focused on huge state and city budget deficits that there's no easy way to fix. Nowhere has this collapse been more visible than California, which faces a massive $25 billion shortfall and red ink for as far as the eye can see.