J. Reynolds, performing acrobatic and balancing acts above 9th Street N.W., Washington DC

Ilargi: There are days when it's hard to figure out what the biggest story in the economy is, the main trend. Like today: is it Wall Street’s sick sense of entitlement, which led to Merrill Lynch CEO John Thain being kicked out the door, or is it the growing unrest around the planet, which today culminated in the demise of the Iceland government? Or is it maybe Obama saying his $825 billion stimulus is on track, while HuffingtonPost reports it's been rejected? Or the ongoing downfall of Britain, which today -surprise!- admits to being in a recession, while even the word depression doesn't cover its situation anymore?

And then, while logging some wood in the rare breaks I allow myself during these long days, I realized it’s all part of the same story.

John Thain redecorated his office to the tune of $1.2 million, 2/3 of which went to the guy who now reinvents the White House, while Merrill’s employees were being handed pink slips. Thain is an obvious idiot. But he is of course by no means alone. And the sick sense of entitlement is not restricted to Wall Street either. It’s the norm in circles of bankers and politicians across the planet. Which is the reason the Icelandic prime minister was forced out today after days, even weeks, of increasingly violent protests. It will also be the reason for many more governments to tumble this year and next, and more after that.

Still, that's the easy part in this. The harder one will come to unfold because of the sense of entitlement that exists all across our societies, that is to say our own ideas about what we are entitled to. It’s not just the bankers who, in Meredith Whitney's words, try to keep their Malibu Barbie Houses. Most of those homes belong to people who are not bankers. And there's many Barbie homes outside of Malibu. The majority among us live in Barbie houses. We just don't call them that. If we look back, say 100 years, and see the size of homes, and the average living space per capita, we find that while the population of our societies has exploded in the last century, so too has the sense of entitlement we feel concerning the amount of space we want, and think we deserve. "Vastly" more people, who all want vastly more space. We can all figure out the trendline there.

We are also confident in telling ourselves we have a right to a nice and warm and fast car, and instantly available world-class health-care, and the best possible education for our children-so they can in time buy their own Barbie homes-, and supermarkets full of products flown, shipped and trucked in from exotic places all around the globe. So we're not really that different from John Thain, are we? He merely has an even higher entitlement pattern than most of us do, not a structurally different one.

I've been critical of Obama's choices for his economic team, and I won't take back one word of that. However, the fiercest criticism should go to his message of getting America back on the track of economic growth. That notion, which is nothing but a fallacy, deserves more scrutiny than any other one. Our economies are shrinking, not growing, and they will continue on down that path for a very long time. Perpetual growth is over, and if you look closely, it has been for at least 30 years. Education, health care and many other fields have become more expensive and less affordable during that time. Who needed day-care in the 1960’s? Who could not afford to go to a doctor? Today, both parents need to work full-time -or more- just to pay the monthly bills. It wasn't like that in the 1960's. Not at all. So were our parents so much less happy than we are? Not at all.

The fallacy of perpetual growth has led us into a sense of entitlement that is based on complete blindness and utterly wrong assumptions. If we are not awake enough to leave that behind, we will be the reason for fighting in the streets, in our own Barbie neighborhoods. If we want to prevent that from happening, we need to take not one, but 826 steps back. But the president of Hope and Belief talks about resuming the economy of growth. That is not possible. People need a reality check. They need to adjust to living on less personal, corporeal, space. If you think or hope that the PM of Iceland is the last one to be thrown out by the wayside, you need to start thinking instead of believing.

NOTE: TIME magazine published its list of the Best 25 Financial Blogs. Of course, The Automatic Earth is nowhere to be found. And that is just fine by me. We have added about 30% more regular readers since Jan 1, and would be comfortably, make that very comfortably, in the Top Ten of Gongol's list of Finance Blogs if we'd open our stats to the public.

Look, Stoneleigh and I have been right about so many things so much of the time, our record speaks for itself. Thank you all who have recognized that. We don't write to try and maximize profits for the investor community, we're here to try and prevent damage for those who don't belong to that community. They are the people who belong here. A financial blog used to be about enhancing profits. Today, it's about minimizing losses. That is a crucial difference, something for which there still is far too little attention. We're here for the bottom part of the population, not for the richest part. We want you to be alright, we're not pre-occupied with making you wealthy. There's plenty places for that if that's your thing.

The credit crisis is not an opportunity, it's a threat. And that is why what we provide is badly needed. I don't care what TIME Magazine thinks, or Gongol, or anybody. It's very clear to me why I do what I do. Not to make you money, but to save it for you. We've been doing great so far. 5 days ahead of our first anniversary, it's grown so much bigger than we ever would have thought, even though we knew all along what was coming. We have saved our combined readership many millions of dollars. That's why we're here. Please remember to donate part of that to The Automatic Earth, so we can continue doing what we do. We're in this together.

Obama Says New $825 Billion Stimulus Plan Is 'on Target'

President Obama said today that efforts to pass a massive new economic stimulus package by mid-February are "on target," despite Republican lawmakers' objections to some elements of the plan. Speaking before a meeting at the White House with a bipartisan group of nine congressional leaders, Obama said he recognizes that "there are still some differences around the table and between the administration and the members of Congress about particular details" of the plan. The proposed $825 billion package is designed to create 3 million to 4 million new jobs, he said. "But what I think unifies this group is recognition that we are experiencing an unprecedented, perhaps, economic crisis that has to be dealt with, and dealt with rapidly," Obama said. He thanked the House and Senate for "moving forward very diligently" on passing what he called a "recovery and renewal plan," adding, "I know that it is a heavy lift."

Obama noted that he has instituted a new daily economic intelligence briefing at the White House. "Frankly, the news has not been good," he said, with each day bringing a greater focus on job losses and "instabilities in the financial system." However, he said, "it appears we are on target" to get the package through Congress by the Presidents' Day weekend. Presidents' Day falls on Feb. 16. Obama told the group: "The recovery package that we're passing is only going to be one leg in at least a three-legged stool." He said it has to be "part and parcel of a reform package" aimed at ensuring transparency and accountability in the way taxpayer dollars are managed as part of the stimulus effort.

Flanking Obama as he spoke were House Speaker Nancy Pelosi (D-Calif.) and Senate Majority Leader Harry M. Reid (D-Nev.). It was Obama's first such meeting with the congressional leadership since he took office Tuesday. Pelosi has said she intends to bring the package to a vote in the House by Jan. 28. But Republicans are seeking deeper tax cuts than the proposal contains and questioning whether $550 billion in new federal spending for roads, bridges and other projects can stimulate the economy quickly enough. Some conservative Democrats are joining Republicans in complaining that the package is too big and some of the spending plans too wasteful.

Addressing reporters outside the White House after the meeting, Republican lawmakers said they made their reservations clear to Obama. "There's unanimity that our economy needs help, and there's also a desire to move a package that would help rescue our economy," said House Minority Leader John A. Boehner (R-Ohio). "We expressed our concerns about some of the spending that's being proposed in the House bill and the fact that it doesn't spend out very quickly." He said there were also "concerns . . . about the size of the package." The GOP proposes "fast-acting tax relief" in the form of bigger tax cuts, Boehner said. "At the end of the day, the government can't solve this problem," he said. "The American people have to solve it. And the way they can solve it is if we allow them to keep more of the money that they earn."

Asked about the views of some economists that the package may be too small, Boehner rejected the idea but indicated that the administration could request more spending in the future if that turned out to be the case. "I think at this point we believe that spending nearly a trillion dollars is really more than we ought to be putting on the backs of our kids and their kids," Boehner said. "We're borrowing this money from our kids." Other Republican lawmakers attending the meeting included Sen. Mitch McConnell (R-Ky.), the Senate minority leader. Pelosi said after the meeting that she was confident a bill could be ready for Obama's signature before the Presidents' Day recess. "If not, there will be no recess," she warned. She said Obama listened carefully to the Republican lawmakers' suggestions.

Reid told reporters, "There wasn't a single person [in the meeting] who felt we couldn't work our way out of the problems that we have." He added: "The president was leading us to be united, not divided. He listened to all of the suggestions, whether from us or the Republicans." Asked if he worried that Republicans would block the legislation, Reid answered, "No." Underscoring the nation's bleak economic situation was more bad news on the jobs and housing fronts. The Commerce Department reported yesterday that the number of new housing starts has dropped to its lowest level since the department began keeping data in 1959.

Initial claims for jobless benefits, meanwhile, jumped 62,000 to 589,000 for the week ended Jan. 17, matching the highest level since the recession of the early 1980s. Unemployment stands at 7.2 percent, but many economists expect it to continue to rise by at least another point. At the same time, analysts and economists are predicting more staggering bank losses of $1 trillion or more, a prospect that could overwhelm the federal $700 billion financial rescue plan known as Troubled Assets Relief Program. The dismal economic news raised fears that the nation's recession, which began in late 2007, would continue through much of this year.

House Rejects Obama's Request For Rest Of TARP

The House expressed its bipartisan anger over a massive financial bailout package Thursday as the Obama administration undertook to assure lawmakers that it would spend the remaining money prudently and with greater oversight than the Bush administration. In a symbolic vote, the House voted to reject President Barack Obama's request for the unspent $350 billion in a bailout fund for the financial sector. The 270-155 tally was a moot point because the Senate had refused to block the release of the money last week. That effectively made it available to the new administration. The vote let Obama know that in seeking to shore up a shaky financial sector, he, like Bush before him, is operating on shaky political ground, even as the weakened banking industry continues to roil the stock markets.

Eager to signal a change, the Obama administration promised to force bankers to report their lending activity on a quarterly basis and to meet tougher executive pay requirements. From the podium of the White House briefing room and in written responses to senators, Obama officials pledged to ensure that the money is used to extend credit to small businesses and consumers. "Those principles include ensuring that executive compensation is limited so that the American taxpayer can feel confident that any money that's used as a part of a financial stability package doesn't go to line the pockets of a CEO," White House spokesman Robert Gibbs said.

Timothy Geithner, whose nomination to be treasury secretary cleared the Senate Finance Committee on Thursday, told the committee in written response to questions that "oversight and transparency requirements in the original proposal were inadequate." He said banks would have to provide "detailed and timely information on their lending patterns broken down by category."

In addition, a new special inspector general assigned to oversee the funds said Thursday that he will ask all institutions that have already received money from the Troubled Asset Relief Program to account for their use of the money and to detail any steps they have taken to meet existing executive pay caps. "If the American taxpayer is to be expected to fund this extraordinary effort to stabilize the financial system, it is not unreasonable that the public and its representatives in Congress have some understanding as to how those funds have been used by the recipients," the inspector general, Neil Barofsky, wrote to Sen. Charles Grassley. Thursday's vote illustrated how the House, where members face election every two years, is much more sensitive to public opinion than the Senate, with its six-year terms of office.

Ninety-nine Democrats joined 171 Republicans in voting to reject the money in a vote that put conservatives and liberals on the same prevailing side. Republicans had grudgingly voted for the $700 billion Troubled Asset Relief Program last fall and were still smarting over Bush administration decisions to use some of the money to help the auto industry and to give money to banks with few conditions. Democrats, freed by the Senate from the pressure to support Obama, fled from the program as well. "My goodness, I can't stand here as a member of Congress and vote to release the second half of this money without knowing what happened to the first half of it," said House Minority Leader John Boehner, R-Ohio.

Democratic opponents of the fund described the bailout as a misplaced priority. "There's a massive transfer of wealth going on, taking money out of the pockets of the American people and putting it into these banks," said Rep. Dennis Kucinich, D-Ohio. "This has to stop. We have to stop." The vote came a day after the House voted 260-166 to set greater reporting requirements on banks that receive bailout funds. House Financial Services Chairman Barney Frank, D-Mass., who supported releasing the funds, conceded Thursday's vote was moot. "Why are we still voting on it?" he asked. "Because there is a degree of anger in the American public at what they think is a very unfair system that gives benefits unduly and disproportionately to some of those who caused the problem, while denying health care and unemployment compensation and a decent higher education for working-class people."

Meredith Whitney on BofA, Merrill Lynch, John Thain being booted, new Citi chairman ”not good news” and the Malibu Barbie house

Wall Street’s Sick Psychology of Entitlement

The news that Merrill Lynch paid out $15 billion in bonuses is sure to ignite new questions about the wisdom of bailing out Wall Street. Merrill Lynch took $10 billion from the TARP, allegedly to fill holes in its balance sheet. But instead of using that to repair its financial health, it simply put the money into the pockets of its employees. There is no way to defend this disgusting payout. But that won’t stop Bank of America, which now owns Merrill, from defending the bonuses. And across Wall Street there are lots of people who actually believe that Merrill did the right thing. How can so many smart people be so dumb?

Easily. There is a sick psychology of entitlement on Wall Street that was created during the bubble years. Many simply cannot believe that they do not deserve huge pay packages. Their brains have not caught up with the idea that they are working in broken institutions that would be unable to pay to keep the lights on if not for the fact that Washington has given them billions of taxpayer dollars. Of course, smart people are very good at rationalizing their fantasies, especially when the fantasy serves to make them money. There are three rationales they’ll offer when pressed on this. Each one is easily skewered.This is the most sophisticated argument for huge bonuses. In Germany, this actually happened. As it turns out, executives would rather risk their firm collapsing due to lack of capital than give up their big paydays. But there's an easy solution to this: throw the bastards out. The boards of every single financial company that turned down bailout bucks with a bonus limit could demand a full accounting of why a bank's executives think it is healthy enough to forego a bailout. And if they aren't satisfied they should just fire the management.

- "We made money. It was just one part of the firm that lost it all. So we deserve to be paid." Sorry, buddy. That’s not the way capitalism works. Ask the guy who just lost his job installing seat belts in GM cars. He was really good at that but since no one is buying those cars, he’s out of a job. Being really good at what you do doesn’t matter if your firm is broke—and your firm is broke. It’s now on taxpayer supported life-support.

- "We didn’t use taxpayer money to pay the bonuses." This is the most ridiculous idea ever. Money is fungible. If you use billions to pay bonuses and then need to ask the government for money to stay alive, you are using taxpayer money to fill in the hole you dug by paying the bonuses.

- "We’ll lose all the greatest people if we don’t pay them." Oh really? Where will they go? Who, exactly, is going to hire them? Also: so what? That’s how capitalism works. Failing firms that cannot afford to pay for talent lose that talent to successful firms. That’s an important part of market discipline.

- "If we don't pay bonuses when firms take the TARP, they won't take it."

Look. We’re not hysterical opponents of paying big bonuses. Actually, I'm on the record as defending huge bonuses from a couple of years ago. If your firm makes money, it can decide how to reward its employees. If it loses money, it can still decide to pay bonuses if it still has cash on hand. But when you pay yourself a bonus with taxpayer money you are simply taking money from someone who earned it and giving it to someone who didn't. If the government hadn’t supplied the means for redistributing that money, you’d just be a mugger.

It was only a few months ago that we were being told that Merrill Lynch, among others, desperately needed billions of dollars to survive, that without injections of new capital the financial system would come crashing down around us. If any of this was true, it should have been impossible for Merrill to pay out $15 billion in bonuses. Even the sharpest critics of the bailout never imagined that it would be used to make wealthy idiots even wealthier. All of this is a reminder of why it is very, very dangerous to allow the government to rescue firms instead of allowing the market to decide who should survive. Perhaps instead of a bailout, we should have confined the TARP to overseeing the orderly disolution of failed financial institutions.

Expect the World Economy to Suffer Through 2009

By IAN BREMMER and NOURIEL ROUBINI

Political risk is a bigger factor than ever.

Some optimistic experts are now saying that though this will be a turbulent year for global markets, the worst of the financial crisis is now behind us. Would it were so. We believe that 2009 will be tougher than many anticipate. We enter the new year grappling with the most serious global economic and financial crisis since the Great Depression. The U.S. economy is, at best, halfway through a recession that began in December 2007 and will prove the longest and most severe of the postwar period. Credit losses of close to $3 trillion are leaving the U.S. banking and financial system insolvent. And the credit crunch will persist as households, financial firms and corporations with high debt ratios and solvency problems undergo a sharp deleveraging process.

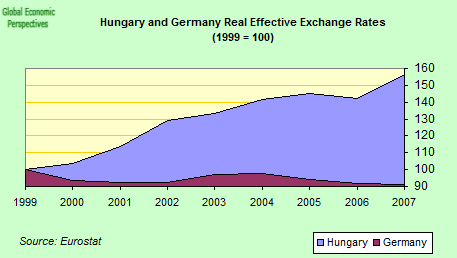

Worse, all of the world's advanced economies are in recession. Many emerging markets, including China, face the threat of a hard landing. Some fear that these conditions will produce a dangerous spike in inflation, but the greater risk is for a kind of global "stag-deflation": a toxic combination of economic stagnation, recession and falling prices. We're likely to see vulnerable European markets (Hungary, Romania and Bulgaria), key Latin American markets (Argentina, Venezuela, Ecuador and Mexico), Asian countries (Pakistan, Indonesia and South Korea), and countries like Russia, Ukraine and the Baltic states facing severe financial pressure.

Policy remedies will have limited effect as insolvency problems constrain the effectiveness of monetary stimulus, and the risk of rising interest rates (following the issuance of a wave of public debt) erodes the growth effects of fiscal stimulus packages. Only when insolvent banks are shut down, others are cleaned up, and the debt level of insolvent households is reduced will conditions ease. Between now and then, we can expect further downside risks to equity markets and other risky assets, given the likelihood that markets will continue to be jolted by worse-than-expected financial news.

The U.S. twin fiscal and current-account deficits will rise over the next two years as the country runs trillion dollar-plus fiscal deficits. We're all aware that foreign actors have financed most of this debt over the past several years. During the 1980s, the U.S. also faced the burdens of twin deficits, but relied on financing from key strategic partners like Japan and Germany. This time, the situation is more worrisome because today's financing comes not from U.S. allies, but from strategic rivals like Russia, China and a number of relatively unstable petrostates. This leaves the U.S. perilously dependent on the kindness of strangers.

There's some good news in this interdependence. The mutually assured economic destruction that this relationship implies ensures that China can't simply pull the plug on all this financing without suffering a considerable amount of self-inflicted pain. Reducing its financing of Washington would, among other things, put significant upward pressure on the value of China's currency, sharply undermining its export sector and, therefore, the country's economic growth. But over time, the ability and willingness of China and others to finance U.S. deficits will diminish as they begin to run fiscal deficits of their own. They'll need to use their financial resources at home just as a tsunami of U.S. Treasury bond issuances peaks.

Politics will make matters worse, primarily because governments in both the rich and the developing worlds are intervening in their economies more broadly and deeply than at any time since the end of World War II. Policy makers around the world are hard at work crafting stimulus packages filled with subsidies and protections they hope will breathe new life into their domestic economies, and preparing to rewrite the rules and regulations that govern global markets.

Why is this dangerous? At the G-20 summit a few weeks ago, world leaders pledged to address the crisis by coordinating their economic policy responses. That's not going to happen, because politicians design stimulus packages with political motives -- to satisfy the needs of their constituents -- not to address imbalances in the global economy. This is as true in Washington as in Beijing. That's why politics will drive the global economy more directly (and less efficiently) in 2009 than at any point in decades. Its politics that is creating the biggest risk for markets this year.

This is part of a worrisome long- term trend. In China and Russia, where histories of command economics predispose governments toward what we've come to call state capitalism, the phenomenon is especially obvious. National oil companies, other state-owned enterprises, and sovereign wealth funds have brought politicians and political bureaucrats into economic decision-making on a scale we haven't seen in a very long time.

Now the U.S. has gotten in on the game. New York, once the financial capital of the world, is no longer even the financial capital of the U.S. That honor falls on Washington, where lawmakers are now injecting populist politics into economics decisions. Companies and sectors that should be left to drown are being floated lifeboats. This drama is also playing out across Europe and Asia. As engines of economic growth, Shanghai is losing ground to Beijing, Mumbai to Delhi, and Dubai to Abu Dhabi.

Global markets will also face the more traditional forms of political risk in 2009. Militancy in an increasingly unstable and financially fragile Pakistan will continue to spill across borders into Afghanistan and India. National elections in Israel and Iran risk bringing the international conflict over Iran's nuclear program to a boil, injecting new volatility into oil markets. The impact of the financial crisis on Russia's economy could produce significant levels of unrest across the country. And Iraq may face renewed civil violence, as recently dormant militia groups compete to fill the vacuum left by departing U.S. troops. The world's first global recession is just getting started.

Roubini, Edwards Predict Slump in S&P 500 on China

Stocks will retreat around the world because of shrinking demand from China as growth in the third- biggest economy slows, said Nouriel Roubini, the New York University professor who predicted last year’s financial crisis. Global equities will fall 20 percent from current levels as China, which contributed 19.5 percent to total growth in 2007, contends with its slowest expansion in seven years, he said. Wall Street strategists predict the Standard & Poor’s 500 Index will rise 29 percent this year from the closing level yesterday.

Roubini, an economics professor at NYU’s Stern School of Business, said China already is in a "recession" despite government data showing a 6.8 percent fourth-quarter growth rate, as power output drops and manufacturing shrinks. "Demand is falling in China, they’re over-invested in capacity and there’s a global supply glut," Roubini, 50, said in a telephone interview. "It has very, very important implications." Roubini’s view is shared by Societe Generale SA global strategist Albert Edwards, who was correct in forecasting in March 2007 that a U.S. contraction would spur a bear market in equities. Edwards says the China slowdown will reduce earnings at industrial, energy and raw-materials companies, worsening a selloff in emerging and developed-market stocks that may send the S&P 500 down 40 percent to 500.

"People should be thinking really hard about this rather than sticking their heads in the sand," said Edwards, a London- based strategist and member of the top-ranked global investment strategy team in Thomson Extel’s surveys the past three years. "We’re just pointing out when the emperor doesn’t have any clothes on." The consensus among eight strategists surveyed by Bloomberg this week is for the index to end the year at 1,066. The S&P 500 fell 1.5 percent yesterday to 827.50, and futures on the index dropped 2.2 percent as of 4:32 a.m. in New York. Data at China’s National Bureau of Statistics is gathered in a "scientific and realistic method," Ma Jiantang, the agency’s director, said at a briefing in Beijing yesterday in response to a question about the accuracy of government figures. Zhang Yingxiang, a spokeswoman for the statistics bureau, declined further comment when contacted by phone today.

China’s economy grew 9 percent for all of 2008 after a 13 percent expansion in the previous year, the fastest in the world. China’s CSI 300 Index fell 0.6 percent at the close in Shanghai, the biggest drop in eight days. Commodity producers led declines after Aluminum Corp. of China Ltd. and Yunnan Copper Industry Co. reported lower profit. Economists at JPMorgan Chase & Co., Citigroup Inc., the World Bank and the International Monetary Fund all predict China will grow at least 7 percent this year, while investors Jim Rogers and Mark Mobius are buying Chinese shares on expectations the government will bolster economic growth with interest-rate cuts and fiscal stimulus. The IMF said China’s contribution to global growth increased to 19.5 percent in 2007 from 17.2 percent in the previous year.

China, which has $1.9 trillion set aside in the world’s largest reserves, plans to spend at least 4 trillion yuan on bridges, housing and tax breaks to boost the economy. Chinese President Hu Jintao has pledged further measures to maintain stable growth in the face of "serious challenges and difficulties." Rogers, who predicted the start of the commodities rally in 1999, recommends investors buy China’s agriculture, water treatment, power generation and infrastructure stocks because the companies won’t be hurt by the nation’s slowing economy. "China could be in recession, I have no idea and it’s not relevant to me because I’m using my judgment as to what will happen six months from now," said Rogers, who authored books on investing including "A Bull in China: Investing Profitably in the World’s Greatest Market." "There is a lot happening in China and there will be those that will hold up well."

China’s economy will grow 6.3 percent this quarter from a year earlier, according to the median estimate of nine economists surveyed by Bloomberg after yesterday’s GDP report. China’s electricity output declined 7.8 percent in November from a year earlier and fell 3 percent in October, the first declines since February 2002, according to China Economic Information Net data compiled by Bloomberg. Manufacturing shrank for a third month as the deepening global recession cut demand for the nation’s toys, clothes and electronics. Edwards said rising unemployment among factory workers will fuel social unrest, threatening the Communist Party’s survival and increasing the risk authorities will devalue the yuan to boost exports.

The yuan appreciated about 19 percent against the dollar between 2005 and July 2008 as China redressed what U.S. officials saw as an unfair price advantage for exports. The yuan has since stabilized at about 6.85 per dollar. Timothy Geithner, President Barack Obama’s nominee for Treasury secretary, said yesterday that China is "manipulating" its currency. The yuan fell the most in a month today as the nation’s banks refuted the new U.S. administration’s accusation. "If you amble your way through the analysis, you realize if push comes to shove they will devalue" the yuan, Edwards said. That may spur lawmakers in the U.S. and China to increase trade barriers, he said.

Roubini’s Gloom Gets Traction in Panicky Tokyo

The champagne must be flowing at Toyota Motor Corp. headquarters. It just ended General Motors Corp.’s 77-year reign as the world’s largest automaker. Toyota also is looking ahead and going full circle in terms of management: It just named the grandson of the company’s founder as president. The celebrations and nostalgia will be short-lived, and not just because Toyota is forecasting its first operating loss in 71 years. It’s on the frontline of an economic plunge that might push Japan into another "Lost Decade." That’s a strong statement, and one that’s worth exploring in Japan and beyond.

Economic data coming out of Tokyo have been atrocious. Exports, for example, plummeted 35 percent in December from a year earlier. That was the sharpest decline since 1980 (there are no comparable data before then). Exports were the main driver of the recovery that now has died a very sudden death. With nothing self-reinforcing about Japan’s expansion, Asia’s biggest economy seemed to go from 120 kilometers (75 miles) per hour to zero in all of a week. Now it’s going in reverse, and picking up speed. Global demand for cars and electronics is drying up fast. Toyota, Sony Corp. and Honda Motor Co. are shedding thousands of workers and closing production lines as profits and sales dwindle. It’s just the beginning as the U.S. and Europe sink.

The global crisis blindsided most Japanese executives and politicians. Much of the chatter in 2008 was about how Japan’s cash-rich banks would play a white-knight role for a Wall Street in turmoil. Mitsubishi UFJ Financial Group Inc.’s $9 billion investment in Morgan Stanley was seen as the first of many such deals. As 2009 unfolds, the folly of that view will come into sharper focus. Yes, Japan’s government has the resources and borrowing potential to forestall a meltdown. The roughly $15 trillion of household savings is a comforting counterpoint to press reports of rising Japanese poverty and homelessness.

Yet Japan will have the same problem as China this year. Both economies can hold their ground when others are booming. With the U.S and Europe in deepening recessions, all that’s left is domestic stimulus. That goes for Asia, too. Singapore may contract a record 5 percent this year. In South Korea, industrial production fell by the most on record in November. Officials in Indonesia, Malaysia, the Philippines, Taiwan and Thailand are struggling to boost slowing economic growth. No serious economist thinks Japan is going to crash. Yet the odds of another 1990s-like period of negligible growth and deflation are increasing as economies such as the U.S. risk a similar fate.

Minimal household savings, sliding home prices and dwindling retirement accounts leave Americans with one option: thrift. The specter of Americans consuming less is prompting a rapid reassessment of Japan’s prospects. "We’d better get ready for a three-year recession," says Hiroshi Yoshikawa, head of the government committee that charts economic cycles. The decline "will be very severe, not only in terms of duration but also depth." Richard Jerram, chief economist at Macquarie Securities Ltd. in Tokyo, headlined a Jan. 20 report: "Panic on Jobs." Yesterday’s was called "Unprecedented Contraction," arguing that the speed of declines in exports and production "is more than twice as fast as anything on record."

Such trends are engendering the kind of gloom envisioned by market seers such as Nouriel Roubini. The views of the chairman of Roubini Global Economics LLC in New York are worth considering. That goes both for what he’s saying now -- that Japan is in for a severe recession -- and more than decade ago. In November 1996, Roubini delivered a speech in Tokyo titled "Japan’s Economic Crisis." What is striking when reading Roubini’s remarks then is how, with a few changes here and there, many of them are just as relevant in January 2009. "The different social culture and history of Japan suggest that Japan will not and should not follow the brutal ‘Wild-West’ American model of restructuring and reform," Roubini said. "However, there is need in Japan for major structural reforms and economic deregulation in order to foster entrepreneurship, risk-taking, innovation and long-run growth."

Roubini added that "delaying these reforms will not help because short-run reduction of the pain might lead to more serious problems in the long-run." Prescient words. Because Japan did delay much-needed economic changes, it’s now in a very bad way. The Bank of Japan has already failed to boost growth by cutting interest rates to zero. Japan has already tried, and failed, to create a thriving domestic economy with massive public spending. The BOJ and the government will pull out all the stops to keep a recession from becoming a depression. Wealthy Japan is far better positioned to stay out of the abyss than peers in Asia. Yet Japan won’t be making the changes needed to prepare for a rapidly aging population and or help it to thrive in a region in which its standard of living is too high to compete. Unless officials in Tokyo act fast and furiously, Japan risks another lost decade. Or something even worse.

The World Won't Buy Unlimited U.S. Debt

By PETER SCHIFF

Barack Obama has spoken often of sacrifice. And as recently as a week ago, he said that to stave off the deepening recession Americans should be prepared to face "trillion dollar deficits for years to come." But apart from a stirring call for volunteerism in his inaugural address, the only specific sacrifices the president has outlined thus far include lower taxes, millions of federally funded jobs, expanded corporate bailouts, and direct stimulus checks to consumers. Could this be described as sacrificial?

What he might have said was that the nations funding the majority of America's public debt -- most notably the Chinese, Japanese and the Saudis -- need to be prepared to sacrifice. They have to fund America's annual trillion-dollar deficits for the foreseeable future. These creditor nations, who already own trillions of dollars of U.S. government debt, are the only entities capable of underwriting the spending that Mr. Obama envisions and that U.S. citizens demand. These nations, in other words, must never use the money to buy other assets or fund domestic spending initiatives for their own people. When the old Treasury bills mature, they can do nothing with the money except buy new ones. To do otherwise would implode the market for U.S. Treasurys (sending U.S. interest rates much higher) and start a run on the dollar. (If foreign central banks become net sellers of Treasurys, the demand for dollars needed to buy them would plummet.)

In sum, our creditors must give up all hope of accessing the principal, and may be compensated only by the paltry 2%-3% yield our bonds currently deliver. As absurd as this may appear on the surface, it seems inconceivable to President Obama, or any respected economist for that matter, that our creditors may decline to sign on. Their confidence is derived from the fact that the arrangement has gone on for some time, and that our creditors would be unwilling to face the economic turbulence that would result from an interruption of the status quo. But just because the game has lasted thus far does not mean that they will continue playing it indefinitely. Thanks to projected huge deficits, the U.S. government is severely raising the stakes. At the same time, the global economic contraction will make larger Treasury purchases by foreign central banks both economically and politically more difficult.

The root problem is not that America may have difficulty borrowing enough from abroad to maintain our GDP, but that our economy was too large in the first place. America's GDP is composed of more than 70% consumer spending. For many years, much of that spending has been a function of voracious consumer borrowing through home equity extractions (averaging more than $850 billion annually in 2005 and 2006, according to the Federal Reserve) and rapid expansion of credit card and other consumer debt. Now that credit is scarce, it is inevitable that GDP will fall. Neither the left nor the right of the American political spectrum has shown any willingness to tolerate such a contraction. Recently, for example, Nobel Prize-winning economist Paul Krugman estimated that a 6.8% contraction in GDP will result in $2.1 trillion in "lost output," which the government should redeem through fiscal stimulation. In his view, the $775 billion announced in Mr. Obama's plan is two-thirds too small.

Although Mr. Krugman may not get all that he wishes, it is clear that Mr. Obama's opening bid will likely move north considerably before any legislation is passed. It is also clear from the political chatter that the policies most favored will be those that encourage rapid consumer spending, not lasting or sustainable economic change. So when the effects of this stimulus dissipate, the same unbalanced economy will remain -- only now with a far higher debt load. If any other country were to face these conditions, unpalatable measures such as severe government austerity or currency devaluation would be the only options. But with our currency's reserve status, we have much more attractive alternatives. We are planning to spend as much as we like, for as long as we like, and we will let the rest of the world pick up the tab.

Currently, U.S. citizens comprise less than 5% of world population, but account for more than 25% of global GDP. Given our debts and weakening economy, this disproportionate advantage should narrow. Yet the U.S. is asking much poorer foreign nations to maintain the status quo, and incredibly, they are complying. At least for now. You can't blame the Obama administration for choosing to go down this path. If these other nations are giving, it becomes very easy to take. However, given his supposedly post-ideological pragmatic gifts, one would hope that Mr. Obama can see that, just like all other bubbles in world history, the U.S. debt bubble will end badly. Taking on more debt to maintain spending is neither sacrificial nor beneficial.

Pressure Grows for More Rescue Funds

The White House's economic team is under pressure from Congress to finalize its financial rescue plan within a week amid a growing realization among lawmakers that they will have to find extra money to fund the new administration's program. The team is hammering out a three-pronged approach that focuses on stemming foreclosures, revamping the government's bailout program and purchasing toxic assets weighing down bank balance sheets and pressuring stock prices. White House spokesman Robert Gibbs said Thursday the plan will be completed "shortly."

The scale of the effort is almost certain to be larger than the $350 billion secured last week through the Troubled Asset Relief Program. Lawmakers say that means they need a proposal from the White House within days so they can appropriate more money. Congress could do that by either attaching the funds to the economic-stimulus plan already totaling $825 billion, or by approving legislation that expands TARP and includes new restrictions on banks that receive money. Kent Conrad (D., N.D.), chairman of the Senate Budget Committee, has told senior aides to President Barack Obama that $350 billion won't be enough.

Some members of Congress said they were worried the White House isn't moving fast enough. "I didn't feel I got the sense of immediacy, the sense of urgency that these questions warrant," said Senate Finance Committee member Ron Wyden (D., Ore.), who has pressed the administration to force financial institutions to disclose the toxic assets on their balance sheets. "I'm just going to ride this every day." The White House on Thursday sought to project that sense of urgency. Mr. Gibbs said the president began what will be daily economic briefings from National Economic Council director Lawrence Summers and other senior staff, along the lines of the president's traditional daily intelligence briefing. Work on the next phase of the Wall Street rescue is happening "as we speak," Mr. Gibbs said.

"The president will make a decision as soon as the financial team gives him those recommendations," he added. "He believes, obviously, that we have to act expeditiously to get this economy moving again." Timothy Geithner, Mr. Obama's nominee for Treasury secretary, told Congress Wednesday that the administration has no "current plans" to request more money, but might seek additional resources if financial conditions worsen. Mr. Geithner received the approval of the Senate Finance Committee by an 18 to 5 vote, paving the way for a full Senate vote in coming days. "We have to be prepared to act flexibly and with speed if conditions worsen appreciably, to devote more resources if that is necessary to secure our objectives," Mr. Geithner wrote in response to questions from lawmakers considering his nomination.

The administration has said it plans to devote between $50 billion and $100 billion in a "sweeping" effort to help homeowners. It also is considering a potentially expensive plan to remove the toxic assets clogging bank's balance sheets, including possibly by having the government purchase those assets. Some economists estimate that could cost trillions of dollars. One reason former Treasury Secretary Henry Paulson abandoned his plan to buy the assets was because of the high cost. "It's an incredibly difficult thing to do and to get right," Mr. Geithner told lawmakers at his confirmation hearing. "And getting it right will be central to the basic credibility of the program."

If the government pays too low a price, banks may have to take deeper write-downs than they have already, exacerbating their financial woes. But if the prices are too high, then banks are benefiting at taxpayer expense. Mr. Geithner said there are several ways to deal with the asset prices, including looking at how the market is pricing the assets, using a third-party to evaluate their value or getting a financial institution's supervisors to assess what the assets are worth. "All of them have risks. All of them are imperfect. They all have limitations," Mr. Geithner said.

The right and wrong way to bail out the banks

By GEORGE SOROS

According to reports in Washington, the Obama administration may be close to devoting as much as $100bn of the second tranche of the troubled asset relief programme funds to creating an "aggregator bank" that would remove toxic securities from the balance sheets of banks. The plan would be to leverage this amount up 10-fold, using the Federal Reserve’s balance sheet, so that the banking system could be relieved of up to $1,000bn (€770bn, £726bn) worth of bad assets.

Although the details have not yet been decided, this approach harks back to the approach originally taken – but eventually abandoned – by Hank Paulson, the former US Treasury secretary. The proposal suffers from the same shortcomings: the toxic securities are, by definition, hard to value. The introduction of a significant buyer will result, not in price discovery, but in price distortion.

Moreover, the securities are not homogeneous, which means that even an auction process would leave the aggregator bank with inferior assets through adverse selection. Even with artificially inflated prices, most banks could not afford to mark their remaining portfolios to market so they would have to be given some additional relief. The most likely solution is to "ring-fence" their portfolios, with the Federal Reserve absorbing losses that extend beyond certain limits. These measures – if enacted – would provide artificial life support for the banks at considerable expense to the taxpayer, but would not put the banks in a position to resume lending at competitive rates. The banks would need fat margins and steep yield curves for a long time to rebuild their equity.

In my view, an equity injection scheme based on realistic valuations, followed by a cut in minimum capital requirements for banks, would be much more effective in restarting the economy. The downside is that it would require significantly more than $1,000bn of new capital. It would involve a good bank/bad bank solution, where appropriate. That would heavily dilute existing shareholders and risk putting the majority of bank equity into government hands. The hard choice facing the Obama administration is between partially nationalising the banks, or leaving them in private hands but nationalising their toxic assets. Choosing the first course would inflict great pain on a broad segment of the population – not only on bank shareholders but also on the beneficiaries of pension funds. However, it would clear the air and restart the economy.

The latter course would avoid recognising and coming to terms with the painful economic realities, but it would put the banking system into the same quandary that proved the undoing of the government sponsored enterprises (GSEs) – Fannie Mae and Freddie Mac. The public interest would dictate that the banks should resume lending on attractive terms. However, this lending would have to be enforced by government diktat because the self-interest of the banks would lead them to focus on preserving and rebuilding their own equity. Political realities are pushing the Obama administration towards the latter course. It cannot go to Congress and ask for the authorisation to spend an additional $1,000bn on recapitalising the banks because Mr Paulson has poisoned the well in the way he demanded and then spent the money for Tarp. Even the second tranche of Tarp – the remaining $350bn – could only be pried loose by a congressional manoeuvre. That is what is leading the Obama administration to contemplate reserving up to $100bn of that tranche for the "aggregator bank" solution.

The stock market is pressing for an early decision by putting pressure on financial stocks. But the new team should avoid repeating the mistakes of the previous one and announcing a programme before it has been thoroughly thought out. The choice between the two courses is momentous; once made, it will become irreversible. It should be based on a careful evaluation of the alternatives. President Barack Obama can fulfil his promise of a bold new approach only by establishing a discontinuity with the previous team. Congress and the public are right in feeling that too much has been done for the banks and not enough for beleaguered householders. The government ought to take the GSEs out of limbo and use them more actively to stabilise the housing market. Having done so, it could go back to Congress for authorisation to recapitalise the banking system the right way.

The Next Bank Bailout

With financial stocks sliding as fears grow that more major banks may fail, it’s easy to overlook the problems at the Federal Home Loan Banks, a group of 12 regional institutions that play a crucial role in providing banks around the country with money for mortgage lending. But that would be a mistake. The banks served as a lender of last resort as the credit crunch tightened, propping up other banks that now have gone under. The crisis now facing them exemplifies the regulatory and other weaknesses in the financial system that have led to the worsening banking crisis, analysts say - sloppy accounting, a lack of transparency, lax oversight, and the trend toward "scheming" a way out of the credit crunch. Wall Street is nervous because it can’t determine the true extent of problems at the banks. And, once again, taxpayers may end up picking up the tab.

"They’ve got a real problem on their hands," said James Bianco, president of Bianco Research in Chicago, a leading analyst and market commentator, in reference to the Federal Home Loan Bank system. "And it’s helping to drag down larger banks as well." The difficulties of the once-obscure government-backed but privately-run banks came into the spotlight earlier this month, when Moody’s released a report saying that in a worst-case scenario, eight of the 12 banks could run low on cash because they own billions of dollars of toxic mortgage securities that are now worthless. The banks are a major source of low-cost lending to 8,000 institutions ranging from small community banks to commercial banks to credit unions.

Federal Home Loan banks in both Seattle and Pittsburgh in particular warned recently that their capital is running low. Moody’s concluded the government may have to step in with funding to keep the banks going. Michael Youngblood, founder of Five Bridges Capital, an asset management company in Bethesda, Md., described the banks as "a victim of circumstance that has affected financial institutions doing mortgage lending in the United States." And Bert Ely, an industry analyst in Alexandria, Va. said the banks’ problems also are tied to accounting rules that make their losses seem more severe than they are. "Their investments have backfired on them," Ely said. "But I think they’re going to be all right. If they go under, we’ve got even worse problems in the economy than we thought."

But on Wall Street, that’s exactly what already-jittery investors fear. Some think the Atlanta FHLB could be taken over by the Federal Reserve, that the San Francisco bank could be merged with other banks, and that the New York bank has lost a significant amount of money, Bianco said. He doesn’t buy the argument that accounting problems are to blame: "That’s the same thing they used to say about Fannie Mae and Freddie Mac," he said. The government took control of the two mortgage giants in September, after the agencies suffered losses from risky mortgage-basked securities. The Federal Home Loan Banks have been plagued for years by "sloppy" accounting, Bianco said, and investors are wary of assurances that the worst-case scenario described by Moody’s is unlikely. "They could be sitting on big losses," Bianco said. "We don’t know how many bad loans they have, and their accounting is so bad investors don’t have any confidence in their numbers."

The banks’ regulator until recently was the Federal Housing Finance Board, created in the wake of the savings and loan scandal of the late 1980s. Asking why the banks were permitted to operate for years with poor accounting practices, Bianco said, is "like asking why the SEC never cracked down on Bernie Madoff," who ran a Ponzi scheme for years that ultimately cost investors $50 billion. The same regulators of the savings and loans that collapsed were hired on with the Federal Housing Finance Board, which meant real reform never happened. "When you fail in Washington," Bianco said, "you get a promotion." In July, the government merged the Federal Housing Finance Board into the Federal Housing Finance Agency, which now also oversees Fannie and Freddie and has expanded regulatory powers.

The problems of the Depression-era banks stem from the sharp expansion of their role in the credit crisis, beginning in 2007. The government used the banks as a "defacto discount window" to prop up the financial system, as other sources of credit began to dry up, Bianco said. Banks that eventually failed or were sold, from Countrywide to Washington Mutual to Citigroup, quickly borrowed a record $163 billion from the Federal Home Loan Banks to stay afloat. "The government was using the Federal Home Loan Banks as a way to bail out the banking system early on," he said.

The moves raised some questions at the time. Sen. Charles Schumer (D-N.Y.) wrote a letter in November 2007 to the Federal Housing Finance Board, complaining about $51.5 billion in loans from the Atlanta Federal Home Loan Bank to Countrywide. Schumer said he found the figures "alarming." Peter Wallison, an American Enterprise Institute scholar who studies the financial system, also expressed concern that the government was taking unnecessary risks in making the banks the lender of last resort. But not only did the lending continue - it grew even more. In February of last year, Barry Ritholtz of The Big Picture called the banks’ expanded role a covert bailout and an "ongoing and expensive venture into irresponsible lending and speculation - all at the taxpayer’s expense."

Youngblood, of Five Bridges, said the Federal Home Loan Banks had little choice. The Office of Thrift Supervision, Countrywide’s regulator, had declared the bank sound, giving the banks little criteria to turn down loans. Besides, the alternative might have been making the credit crunch even worse, he said. "It was a calculated risk," he explained. But Washington Mutual eventually collapsed, in the biggest bank failure in U.S. history. Countrywide, once the nation’s largest subprime lender, was bought by Bank of America in January, and its shares have fallen by 64 percent since then. Citigroup, awash in bad loans, said it lost $19 billion last year. Investors are worried about Wells Fargo since its acquisition of Wachovia and its toxic mortgage securities. Nouriel Roubini, the New York University business professor who predicted the credit crisis, this week called the U.S. banking system "essentially insolvent."

The Federal Home Loan Banks are chartered by the government but operate as a privately run cooperative. As they did with Fannie and Freddie, investors assume the federal government would bail the system out if it got in trouble. The banks receive top ratings from the ratings agencies and are able to borrow money more cheaply due to the implicit government backing. The banks’ problems illustrate how the government may have promised more than it can deliver in keeping failed or troubled institutions afloat, Bianco said. "Everybody thinks we can scheme our way out of this," Bianco said. "There’s no scheming our way out of it. There’s not enough credit to go around." With the real possibility of government guarantees being called on "all in one day," he said, "the whole system is coming apart."

Not everyone is as pessimistic as Bianco. Alex Pollock, a banking expert at the conservative think tank, American Enterprise Institute, said the doesn’t think the Federal Home Loan Banks are in peril of going under. "It doesn’t really look to me like an insolvency issue," Pollock said. Neither Youngblood nor Ely also thinks the banks will fail, but acknowledged they may need some financial help from the government. Regardless of whether they survive, the crisis has opened a window into longtime, overlooked weaknesses in Federal Home Loan Bank system and its oversight. Ely said the in the 1980s, the Federal Home Loans Banks were known as "flubs," for their poor risk controls. Bianco described them as "having had losses for years." Yet as the credit crisis intensified, the government chose to make them the lender of last resort to major banks overwhelmed with toxic mortgages. And that leaves taxpayers facing the possibility of yet another bailout.

Fed Likely to Keep Focus on Rates, Loans

Federal Reserve officials are likely next week to stick closely to their approach for handling the financial crisis -- near-zero interest rates and a focus on special lending programs -- despite internal rifts about some of their tactics. Some steps being considered -- such as setting an inflation target or buying Treasury securities -- are likely to stay on the back burner as Fed officials examine the efficacy of those ideas. An inflation target could help manage expectations for future inflation, while Treasury purchases could help bring longer-term interest rates down further, but officials want to study them more.

The efforts by some regional Fed bank presidents -- most notably Charles Plosser of the Philadelphia Fed -- to get the central bank to set numerical targets for how much money it pumps into the financial system also have gone nowhere so far. Those targets could act as a constraint on its rescue programs -- a prospect Fed Chairman Ben Bernanke wants to avoid. The Federal Open Market Committee, the Fed's policy-making arm, meets next Tuesday and Wednesday. The committee, which sets monetary policy, consists of members of the Federal Reserve Board in Washington and a rotation of five presidents from the 12 regional Fed banks. In normal times, the focus of FOMC meetings is the level of the Fed's benchmark interest rate, the federal-funds rate. At the FOMC's December meeting, the central bank said it would push the fed-funds rate to near zero. With policy makers unable to move the target lower to boost the weak economy, the focus of FOMC meetings has shifted to the wide range of new lending and asset-purchase programs the Fed has introduced.Much of the coming meeting will be spent reviewing these programs, their effectiveness and challenges the Fed will face in running them and one day unwinding them. The programs -- ranging from efforts to buy commercial paper to offering emergency loans to banks and securities firms -- are the province of the Federal Reserve Board and the New York Fed. Some regional Fed bank presidents worry that these new programs are causing the central bank's balance sheet and some measures of the U.S.'s money supply to grow too quickly, which could eventually cause inflation. They are pushing for stricter guidelines on how fast the programs can grow. "I believe we must proceed with caution," Mr. Plosser, the Philadelphia Fed president, said in a speech earlier this month. "While the lending programs are designed to improve the flow of credit, they are currently injecting enormous amounts of liquidity into the system," said Mr. Plosser, who doesn't have a vote at the FOMC this year.

In another speech this month, Richmond Fed president Jeffrey Lacker, who does vote on the FOMC, warned that the Fed's market interventions could conflict with its independence. Mr. Bernanke, whose view carries the day, opposes efforts to set limits or targets for how much the Fed's balance sheet should grow, or how much cash it pumps into the economy. Such limits, he said in a speech last week, could force the Fed to be more restrained at a time when its intervention is most needed. "The usage of Federal Reserve credit is determined in large part by borrower needs and thus will tend to increase when market conditions worsen and decline when market conditions improve," Mr. Bernanke said. Setting targets for the balance sheet "could thus have the perverse effect of forcing the Fed to tighten the terms and availability of its lending at times when market conditions were worsening." In their statement following next week's meeting, Fed officials are likely to acknowledge the continued deterioration in the economy since officials last met, and the quick slowdown in inflation.

Several Fed officials have highlighted the potential benefits of an inflation target, which could help convince investors of two things: officials won't pump so much money into the economy that they will create inflation later, and they won't let the economy sink so low that deflation, a broad decline in prices, would set in. But officials aren't prepared to take such a step. Setting a target raises many questions, including: What is the appropriate inflation rate to target? And what is the appropriate measure of inflation? They are also examining closely the idea of buying Treasury securities, but this also appears to be on the back burner for now. Such a policy could help push long-term interest rates lower, but some Fed officials worry that investors could see it as an effort by the central bank to finance large government budget deficits, which could be inflationary. They are instead focused on other efforts to bring down other long-term rates, such as mortgages.

RIP: Credit as Money

by EUGENE LINDEN

The drumbeat over the Obama administration’s plans to fix the banking crisis has reached fever pitch. Over the past week, what appears to be a carefully choreographed series of leaks has raised expectations that the administration has something very big planned (my guess is that it would've been announced today, but for the delay in Timothy Geithner’s confirmation as Treasury Secretary). Various newspapers and blogs have speculated on the details, some of which would be truly dramatic. Examples include: An omnibus take-over of a raft of banks; a process that would include wiping out existing shareholders; converting debt to equity to avoid the new N-word (nationalization); the FDIC providing a backstop for deposits; and, to restore trust in bank balance sheets, the establishment of a new entity to buy, hold, and trade trillions of dollars in now-suspect bank assets.

Clearly something needs to be done, and just as clearly, the banks have gotten wind of the proposals and are trying to head off the scariest parts of the plan. (I interpret the trumpeted insider-share purchases by JPMorgan Chase’s Jamie Dimon and execs at Bank of America to be a message: "Hey, no need to nationalize us, we believe in our equity value!") Ignored by much of the commentary, however, has been a small but crucial change in the proposed composition of the much-discussed new entity to buy toxic bank assets. Moreover, if this entity comes to pass, it will serve as the grave for a widely shared -- but very dangerous -- artifact of the bubble years: the confusion of money as credit.

First, the new wrinkle in the "bad bank" concept. Last week on CNBC, Sheila Bair, the outgoing and incoming head of the FDIC, remarked on the possibility of setting up an entity funded by both public and private money to buy toxic assets. The involvement of private money is new, and the timing of this announcement begs many questions. In the CNBC interview, Bair said, "One approach we think might have some merit is what we call an "aggregator bank" where you would set up a facility capitalized through some portion of the TARP fund to acquire troubled assets…" So far so good. The basic idea has been floated many times over the past year. But then she remarked that the new structure would "also require those institutions selling assets into this facility to contribute some capital cushion themselves…"

The suggestion about lenders having a stake in the entity is both crucial and new - at least new to the Bush administration. (A number of observers, including me, suggested such an entity at the beginning of the crisis in Aug. 2007.) Forcing banks to have skin in the game alongside taxpayers makes it less likely that financial institutions will try to screw the taxpayers. Having the government involved also provides adult supervision in the setting of the ground rules. Why then, didn’t,the Bush administration put forth this key provision before the very end? Someone must have suggested it - after all, it’s little more than common sense. If it’s a good idea in the full teeth of the crisis, why wasn’t it a good idea at the outset? That it will be the Obama administration that launches this entity implies that the Bush administration was loathe to push for the self-policing aspects of having the banks provide capital.

And then, there’s the end-of-an-era aspect of plan. Whether it’s called a "bad bank" or "aggregator" or "RTC II," the new entity represents an explicit admission that no one else is willing to accept trillions of dollars in credit instruments that 2 years ago were treated as interchangeable with money. Thanks to the ingenuity of Wall Street’s rocket scientists, so-called structured credit products proliferated wildly during this decade, backed by mortgages and other obligations (or by other credit instruments that in turn, were backed by assets). With credit rating agencies blessing these products as AAA, these instruments were treated almost as money, and provided much of the liquidity that spurred the illusion of wealth creation during the bubble years.

Now, pension funds, hedge funds, endowments and financial institutions that confused money and credit have discovered -- in the most brutal fashion -- that the value of anything deemed to be money-good rests entirely on the willingness of someone else to accept it. With no one but the government willing to accept these assets, this former currency will be retired as scrap. RIP, money as credit. Unfortunately, the story does not end there. While officials cross their fingers that these disgraced credit instruments will remain quarantined, this nuclear waste could still leach into the financial system - particularly if the prices paid are above market (whatever that is!). The scale of this pollution is such that the sum total of government guarantees and obligations may impact the value the rest of the world puts on the US dollar, the linchpin of the global financial system. In the end then, money and credit do turn out to have some something in common: the value of either depends entirely on the trust of strangers.

U.S. Stance on the Yuan Gets Tougher

President Barack Obama's nominee for Treasury secretary accused China on Thursday of "manipulating" its currency, a sharp rhetorical break from the Bush administration's approach to Beijing's controversial exchange-rate policy. Timothy Geithner's use of the term signaled an escalation in the war of words -- if not necessarily of actions -- over Beijing's practice of keeping the yuan artificially weak against the dollar. Many U.S. manufacturers, unions and lawmakers charge that Beijing tinkers with its currency to give Chinese companies an edge over foreign competitors. Responding to questions from the Senate Finance Committee overseeing his confirmation hearings, Mr. Geithner stressed Mr. Obama's promise to "use aggressively all diplomatic avenues open to him to seek change in China's currency practices."

Should Mr. Geithner win Senate confirmation, as the committee recommended, his choice of language will likely draw attention to Treasury's next report on international currency practices, due in April. U.S. trade law requires the report to identify any country that manipulates its exchange rate for purposes of gaining an advantage in international trade. Such a designation would require the Treasury Department to open formal negotiations with Beijing over currency policy. Treasury officials frequently talk currency with their Chinese counterparts. The manipulator label would be a symbolic slap. While the Bush administration pressed Beijing to loosen its grip on the yuan, it consistently declined to brand China a currency manipulator. When he was in the Senate, Mr. Obama co-sponsored legislation to create new penalties "so countries like China cannot continue to get a free pass for undermining fair trade principles," in Mr. Geithner's words.

Mr. Geithner didn't say whether Mr. Obama would take a more punitive approach to China over its currency policy. He said the immediate priority is to persuade China to stimulate its domestic economy. "You don't want to be the bull in the China shop when it comes to currencies right now," said Frank Vargo, a vice president of the National Association of Manufacturers, which has long lobbied against China's yuan policy. "But...we all know the Chinese currency is deliberately undervalued." A spokesman for the Chinese Embassy in Washington couldn't be reached for comment on Thursday afternoon. President George W. Bush's Treasury secretary, Henry Paulson has cited the 21% appreciation of the yuan since July 2005 as evidence that China understands the need to liberalize the exchange-rate regime.

Timothy Geithner currency 'manipulation' accusation angers China

China has responded angrily to an accusation of currency "manipulation" by Timothy Geithner, the new US Treasury Secretary. Mr Geithner wrote three times to a senate finance committee that "President Obama, backed by the conclusions of a broad range of economists, believes that China is manipulating its currency." He added: "President Obama has pledged as President to use aggressively all the diplomatic avenues open to him to seek change in China's currency practises. While in the US Senate, he co-sponsored tough legislation to overhaul the US process for currency manipulation and authorising new measures so that countries like China cannot continue to get a free pass for undermining fair trade principles."

His comments, on only the second day of Mr Obama's presidency, sent a much stronger message to China than his predecessor, Hank Paulson, ever dared to. Mr Paulson often urged China to revalue its currency upwards but stopped short of using the word "manipulation" for fear of offending Beijing. The US has long-standing concerns that China has artificially depressed the value of the renminbi in order to boost exports. It believes the subsequent imbalance was detrimental to US business and may have helped trigger the financial crisis. China abandoned a fixed currency peg with the US dollar in 2005 for a managed float and since then the renminbi has appreciated by about 20pc against the greenback. Mr Geithner's comments had little effect on the exchange rate on Friday. In Shanghai, the dollar traded at 6.8401 yuan, compared to 6.8371 yuan on Thursday.

Mr Geithner stopped short of warning that the US Treasury would formally name China as a currency manipulator in its annual report. "The question is how and when to broach the subject in order to do more good than harm," he said. He also said the "most important" priority was to help China to boost its domestic demand, and said the US would urge China to embark on a further stimulus package, in addition to the £400bn it has already pledged. Nevertheless, Mr Geithner's words are sure to have angered the Chinese leadership, which issued a short message on Friday to say it had "noted" his remarks.

The timing of the comment was particularly provocative, since China has staunchly refrained from devaluing the renminbi since the financial crisis began, despite a wave of closures in its export sector and a fast-deflating economy. Nouriel Roubini has become the latest high-profile economist to remark that the Chinese economy is now on the verge of a full-blown recession. He said on Thursday that the latest GDP figures, which showed 6.8pc growth in the last quarter of 2008, were misleading since they did not show that growth had stalled to "zero" between the third and fourth quarters. "I was very disappointed and surprised at the remarks," said Hua Ercheng, chief economist at China Construction Bank. "We are concerned about rising trade protectionism in the US."

Party Line Central Banking

With Tim Geithner poised to become Treasury Secretary, his current post as president of the New York Federal Reserve Bank now opens. The bank's search committee has reportedly settled on Fed insider William Dudley as his replacement, which wouldn't help the Fed's reputation for independence, or the world's confidence in the dollar. By all accounts Mr. Dudley has done a fine technical job running the New York Fed's markets desk since January 2007. The presidency is a policy position, however, and during the current financial panic a crucial one. The New York Fed president is both vice chairman of the larger Federal Reserve's Open Market Committee and serves as the Fed's main liaison with the financial community. At the current moment especially, the New York Fed needs new blood -- someone markets will see as a bulwark against political meddling and a force for U.S. financial strength.

Mr. Dudley will be perceived, and fairly so, as a Geithner and White House loyalist. This isn't helpful at a time when the Fed is already widely seen as far too willing to bend to Treasury and Capitol Hill wishes. Mr. Dudley won't be a voice for restraint against the Fed's tendency to create new taxpayer guarantees and obligations. And he'd be no match for Larry Summers, the White House economic adviser who would like to replace Ben Bernanke when the Fed chairman's term expires in a year. The last thing Mr. Summers wants is competition. One of the Fed's most important tasks in coming months will be deciding when to remove the oceans of liquidity that it has been pushing into the economy to fight off a deeper recession. Remove it too late once the recovery begins, and the Fed will risk creating new asset bubbles or a run on the dollar. Yet as chief economist for many years at Goldman Sachs, Mr. Dudley consistently supported a weak dollar in the name of reducing the U.S. trade deficit.

This is a dangerous message to send at any time, but in particular as the new Administration embarks on an epic spending spree that will require from $2 trillion to $3 trillion in new U.S. borrowing over the next two years. The world's creditors aren't likely to lend as much, or as cheaply, if they think their dollar assets will be debased as a matter of U.S. policy. The head of the New York Fed search committee is Stephen Friedman, also of Goldman Sachs. We think that in focusing on Mr. Dudley the committee is bending more to the wishes of Mr. Geithner and the Obama Administration, rather than relying on an old Goldman school tie. But the Goldman political optics of the selection won't help either Mr. Dudley or the new Administration as they try to design the rules for a new financial regulatory system.

Financial circles are full of conspiracy theories that major Treasury and Fed decisions have been made to help Goldman -- for example, nationalizing AIG in order to rescue Goldman's counterparty trades with the insurer. We've seen no evidence to support these claims. But the perception alone is a market reality that hurts the credibility of U.S. officials as they try to lead the financial world. We believe Presidents deserve the policy advisers they want in most cases. But the Fed and the regional Fed banks in particular are supposed to be independent. Perhaps Mr. Dudley will surprise us and emerge as his own policy man, but on the evidence so far America's creditors are right to wonder what his selection means for the Fed's independence in the Obama era.

EU states monitor spread of civil unrest

EU member states are "intensively" monitoring the risk of spreading civil unrest in Europe, as riots over the economic crisis erupt in Iceland following street clashes in Latvia, Lithuania, Bulgaria and Greece. The worst street disturbances for 50 years struck Reykjavik on Thursday (22 January), as police streamed a hardcore of a few hundred anti-government protesters in the early morning with pepper spray and then tear gas after an earlier crowd of around 2,000 gathered outside the Althingi, the country's parliament, to demand the government resign.

The crowds surrounded the building while banging pots and pans and shooting off fireworks. The demonstrators also lobbed paving stones, rolls of toilet paper and shoes. It was the second day of protests after on Wednesday protesters jostled Minister Geir Haarde's limousine, pummelling it with cans of soft drinks and eggs. The regular demonstrations have strained the government coalition, with the ruling Independence Party on Thursday saying it "realises that there will be elections this year."