Fishing boat at Fulton Market Pier, New York City

Ilargi:

One day, when Ali Baba was in the forest, and had just cut wood enough to load his asses, he saw at a distance a great cloud of dust approaching him. He observed it with attention, and distinguished soon after a body of horsemen, whom he suspected to be robbers. He determined to leave his asses in order to save himself; so climbed up a large tree, planted on a high rock, the branches of which were thick enough to conceal him, and yet enabled him to see all that passed without being discovered.

The troop, to the number of forty, well mounted and armed, came to the foot of the rock on which the tree stood, and there dismounted. Every man unbridled his horse, tied him to some shrub, and hung about his neck a bag of corn which they carried behind them. Then each took off his saddle-bag, which from its weight seemed to Ali Baba to be full of gold and silver. One, whom he took to be their captain, came under the tree in which he was concealed, and making his way through some shrubs, pronounced the words: “Open, Simsim!” A door opened in the rock; and after he had made all his troop enter before him, he followed them, when the door shut again of itself.

The reason I was thinking of Ali Baba is, I was wondering: how do we open our present treasury chambers and political backrooms, what are the magic words that will open up and shine a light on today's secrets? Many of those secrets are so ugly and festering and rotting, at the very least they badly need a ray of daylight. The fact that Ali comes with Forty Thieves in tow of course makes his tale all the more appealing as a metaphor for our times.

President Obama thinks he can help: he considers bailing out newspapers, ostensibly to promote journalistic notions such as truth-finding.

"I am concerned that if the direction of the news is all blogosphere, all opinions, with no serious fact-checking, no serious attempts to put stories in context, that what you will end up getting is people shouting at each other across the void but not a lot of mutual understanding,"

But that of course is the horse a mile and a half behind the cart. And in left field to boot. The reason the blogosphere has gained so much attention is that "serious fact-checking" is a long forgotten part of American journalism. And -financial- government involvement in the news industry, whatever else it may indeed accomplish, is not exactly the most obvious way to get a reporter to go digging in that same government's dirt. What Obama complains about in the blogosphere, that it's all about opinions, doesn't describe that sphere, it describes the news industry that is no longer able to deliver any shrapnel of news without having first run it through the opinion wringer of its editors and ownership.

Whoever wishes to get a fair picture of today's reality has no choice but to turn to the internet. This is so obvious by now, it's become useless to deny. Which means it would be a far better idea to fund those sources, not the established papers, so people can go out digging for the truth who are not affiliated in some way or another with existing interests.

Let me give two examples of subjects that badly need the kind of serious journalism that is simply not provided by the media we expect it from.

Ron Paul has long clamored for an audit of the Federal Reserve. Tim Geithner apparently has proposed a setting in which the Fed, along with "outside experts", can go through its own books. That should work....

The Fed, of course, has said no. I don't find this all that interesting. Simply because I don't think a real audit of the Fed has any chance of happening. What I would like to see answered first of all is on what authority Congress, or the White House for that matter, could force the Fed to open up.

Go through the 1913 statutes, or whatever they may be called, with which Congress founded the Federal Reserve. In those statutes, Congress gave away its constitutional right to issue the nation's money, an act that in itself may very well be unconstitutional: the Founding Fathers never meant for a privately owned central bank to issue the nation's currency, so is it legal for Congress to hand over its constitutional authority to such an institution?

And when it did anyway, did Congress still retain the right to audit the Fed? I'm no lawyer, but I would seriously doubt it. Which is why I think that all the noise Ron Paul is making is just that, noise. Whether he knows that, I can't tell. You would hope, though, that he's prepared before making his noise. But that makes him a suspect person in my view.

I'd venture that all Congress can do is to abolish the Fed (not going to happen), not audit it. But yes, by all means, let's have some Woodwards and Bernsteins out there figure it out in the interest of the American people. If the president wants to fund the research, fine by me, as long as he keeps his nose out of it. Oh, and while they're at it, perhaps their bosses can explain to us why this wasn't already done a long time ago.

A second story that badly needs good reporting is the Bank of America takeover of Merrill Lynch, along with the questions concerning who knew what when and what on earth made the SEC try and sweep it under the carpet for $33 million.

In a nutshell: Fed chairman Ben Bernanke and then Treasury Secretary Paulson are alleged to have pressured BofA into taking over Merrill, after it found out Merrill's situation was much worse than it initially presumed (which is weird in itself: why didn't they read the books a bit better?). The extent of Merrill's problems was then -allegedly- kept from BofA's shareholders leading up to their December 5 2008 vote on the takeover. What was also not revealed, nay, even denied, was that BofA's execs had agreed to pay Merrill execs $5.8 billion in bonuses for running their bank into the ground.

It's that last little ditty that the SEC, on August 3 2009, agreed to settle with BofA for $33 million. However, 2 days later, Federal Judge Jed Rakoff refused to accept the settlement. A nice detail: at least one former Merrill employee received a bonus bigger than the intended $33 million settlement sum. What seems to have irked Judge Rakoff more than anything is that the shareholders, whose interests were harmed by the failure to disclose the bonus payment agreement, would be on the hook for the $33 million supposed to settle the case that harmed them. Rakoff has set a court date no later than February 10, 2010.

So far, it looks like just another tale out of 1001 nights of Wall Street toxicity, albeit with a refreshing point of view from the judicial branch in the playbook. But this may still not be the whole story.

New York Attorney General Andrew Cuomo is also looking into the case, and he subpoenaed 5 BofA directors last week. Cuomo wants to know whether BofA directors withheld information from shareholders. Cuomo’s investigators will ask directors how much they knew about Merrill’s losses, and the role they played in decisions about disclosing information to shareholders. They will also ask if government officials threatened to remove BofA’s management and the board if the bank didn’t proceed with the deal.

Cuomo. Ran for governor in 2002, and failed. Would like another run. He's a career man, married a Kennedy and all that. Has a good team at his disposal, like Elliot Spitzer did when he held the AG post. Spitzer successfully did make the jump to governor.

Cuomo. What would happen if he keeps digging? How would his investigation cross-pollinate with the case before Judge Rakoff? Looks like a great case for a group of go-getting reporters to me. The problem I think with this case is that it looks so much like Watergate, in that it reaches right up to the highest offices in the land. Maybe not the Oval Office, we’ll have to see about that, but certainly uncomfortably close to it.

There are persistent rumors that the Obama team is pressuring New York State Governor David Paterson not to run for another term. Not because it would hurt the Democratic Party, which is the "official"reason, say these rumors, but to open the way for Andrew Cuomo, to move from being Attorney General to making a run for Governor. What the rumors argue (if rumors can be said to do such a thing) is that this would conveniently move Cuomo out of the way of an investigation that he's in the middle of, and that has the potential to damage the reputations of eminent Wall Street bankers as well as very eminent Washington politicians, from both the Bush and Obama administrations.

Now we're getting closer. From where I am seated, I'd suspect that Tim Geithner is sitting neither pretty nor easy. Geithner has so far largely been kept out of the limelight, but he was leading the New York Fed when the BofA/Merrill takeover was being pushed through. It was Geithner's legal team that handled all the details surrounding the deal, which obviously took place inside the New York Fed's jurisdiction.

So what did Geithner know? On April 23, the Wall Street Journal published this revealing article: Lewis Testifies U.S. Urged Silence on Deal, which claims that Paulson and Bernanke pushed BofA CEO Ken Lewis to hide the truth about Merrill Lynch from BofA shareholders ahead of their vote on the takeover. Yes, that would be highly illegal if it turns out to be true. Threatening to kick Lewis out of his job if he didn't comply with the plans is then merely the icing on the criminal cake.

The article doesn't mention Geithner at all. Ain't that just the most curious thing? However, Rep. Edolphus Towns (D-N.Y.) asked Geithner about his role in the takeover. On April 24, the Washington Independent reported:

Geithner, of course, was neck deep in crafting the bailout strategies under the Bush administration, and now Towns, who heads the House Oversight and Government Reform Committee, has joined forces with Rep. Dennis Kucinich (D-Ohio), who chairs the Domestic Policy subpanel, to ask what role Geithner played in the controversial BofA-Merrill deal. From the lawmakers’ April 23 letter to Geithner:If Mr. Lewis’s statement, as reported by the Journal, of discussions that occurred between Mr. Paulson, Mr. Bernanke and himself is accurate, then federal officials were potentially involved in knowingly denying BOA investors material information.The lawmakers are asking Geithner for “all documents prepared for internal use related to discussions with Bank of America and/or Treasury about compensation packages, bonuses, annual losses at Merrill Lynch, and federal guarantees against losses on Merrill Lynch assets, for the period August I, 2008 through January 19,2009,” as well as “discussions relating to public disclosure of information about compensation packages, bonuses, and annual losses at Merrill Lynch.”

A similar version of the letter went to Bernanke. And unlike the first inquiry over executive compensation limits — which Geithner still hasn’t responded to, even eight days after the requested deadline – Towns and Kucinich are threatening to subpoena the officials for the information if they don’t get it otherwise.The implications of Mr. Lewis’ testimony, if accurate, are extremely serious. Under these circumstances failure to comply with the Subcommittee’s request raises the prospect that we will be forced to consider compulsory means to achieve compliance with our request. However, we would prefer your voluntary compliance.

I know what you're thinking: what the hell ever happened to that letter? How did Geithner respond? Where are Towns and Kucinich now? Surely they must be tragically drugged and gagged in an alley someplace, or they would be raising hell? And why does that silence hurt my ears?

Well, that's where the inquiring reporters should come in. And don't. On June 24, Huffington Post had this to say:

Breaking News: Tim Geithner, Treasury Secretary, supposedly emailed telling BofA that they couldn't back out of acquiring Merrill Lynch, according to CNBC.

An email by Geithner telling BofA to close the deal would be a proverbial smoking gun, since BofA honcho Ken Lewis has said he was forced into buying the bank and not publicly revealing the poor financial shape that Merrill Lynch was in, in the wake of pressure from the government.

So what's going on? Why does the White House turn on NY Governor Paterson 15 months before his term is up? Washington meddling in state politics is awkward in the best of times, and this ain't one of them. The world may well be a whole different place by December 2010, and Paterson may be a hero by then. And why does the Obama team choose to leak this so overtly to the press?

We’ll find out more, going forward, by following what the next steps are that Andrew Cuomo is going to take. If he continues his aggressive pursuit of the BofA case, and includes the role played by Geithner in his quest, my suspicions will be unfounded. But that may well cost Geithner his job, if not more. If Cuomo announces he'll run for governor soon, that's a whole different story. Getting Paulson, Bernanke and Geithner behind bars is too much to ask right now, even if these are serious criminal allegations. Pushing those of them out of their public jobs that still hold them looks more realistic. Still, to reiterate, I don't think Congress has the authority to fire Bernanke. Nor does the president, for that matter, though that facade will be kept standing upright at just about any price.

For now, though, forget about Cuomo. I think the best bet to get to Open Sesame is Judge Rakoff. He's set in motion a course of events that may be hard to stop. Even if strange things have been known to happen to judges between September and February.

I hope that what people will take away from this case, from reading and hearing about it as time progresses, is a more complete notion of the depths to which this once democratic system has sunk. If and when the law states that the acts of many of the most powerful people in the country are illegal to such an extent that they should be in jail, while those same people are allowed to continue to make decisions involving trillions of dollars of other people's money, it's safe to say there is a bit of a problem.

And hoping for a few magic words to solve it just won't do. Too much innocence has been lost on the way here.

U.S. mortgage delinquencies set record

High U.S. unemployment keeps pushing up the rate of mortgage delinquencies, which could in turn drive personal bankruptcies and home foreclosures, monthly data from the Equifax Inc credit bureau showed on Monday. Among U.S. homeowners with mortgages, a record 7.58 percent were at least 30 days late on payments in August, up from 7.32 percent in July, according to the data obtained exclusively by Reuters.

August marked the fourth consecutive monthly increase in delinquencies, and the report showed an accelerating pace. By comparison, 4.89 percent of mortgages were 30 days past due in August 2008, while in August 2007, the rate was 3.44 percent, Equifax data showed. The rate of subprime mortgage delinquencies now tops 41 percent, up from about 39 percent in each of the prior five months.

The results, which correlate with consumer bankruptcy filings, suggest U.S. homeowners remain under financial stress despite signs of improving sentiment and fundamentals in the U.S. housing market. August bankruptcy filings were up 32 percent from a year earlier, compared with a 35 percent year-over-year increase in July.

Still, while more Americans were late with mortgage payments, they are keeping up with other bills. The proportion of credit card accounts at least 60 days past due was down in August for the third straight month, while subprime card delinquencies also fell. That improvement in delinquency rates partly reflects risk-aversion among issuers, which have cut the number of cards by 82 million, or 19 percent, over the past year, while slashing credit limits by $721 billion, to about $3.6 trillion.

The number of new cards being issued is down even more dramatically. In June, 2.6 million new cards were issued, compared with 4.7 million a year earlier. Lenders are increasingly targeting consumers with high credit scores, Equifax found. While in 2007, about one in five new cards went to people with a credit score above 760, such consumers account for two in five new cards in 2009. Equifax found similar trends in auto loans.

"The data from August further confirms that we're witnessing a dramatic change in consumer habits," said Dann Adams, president of Equifax's Consumer Information Solutions group. Total consumer debt is down more than $300 billion, or almost 3 percent, from its peak in September 2008, Adams said, while the savings rate is nearing 5 percent, "a level we haven't seen in years."

Housing Suffering Relapse Confronts Bernanke Credit Conundrum

The recovering housing market may be heading for a relapse as President Barack Obama and Federal Reserve Chairman Ben S. Bernanke consider ending support for the source of the global financial crisis.

The Obama administration is studying whether to let a first-time home buyers’ tax credit expire as scheduled at the end of November. Bernanke and his Fed colleagues may continue talking this week about how to wind down purchases of mortgage- backed securities, according to Peter Hooper, chief economist at Deutsche Bank Securities Inc. in New York. The two programs have helped stabilize real-estate demand, with new-house sales rising 9.6 percent in July from the prior month, the most since 2005.

Ending these efforts may stifle the housing rebound by depressing sales and pushing up both mortgage-backed bond yields and interest rates on home loans, even in the face of the record-low zero to 0.25 percent short-term rates the Fed has engineered, said economist Thomas Lawler. A weaker housing market would likely dampen the economic recovery and undercut shares of builders including Fort Worth, Texas-based D.R. Horton Inc. and Miami-based Lennar Corp., that have risen 40 percent this year, based on the Standard and Poor’s Supercomposite Homebuilding Index of 12 companies.

"Things could get ugly," said Lawler, an independent consultant in Leesburg, Virginia, who spent 22 years at Fannie Mae, a Washington, D.C.-based government-controlled mortgage- finance company. "We could be facing a triple whammy at the end of the year: the expiration of the tax credit, the end of the Fed mortgage-buying program and rising foreclosures."

This is the first major test of policy makers’ ability to coordinate exit strategies as they seek to wean the economy off government support, said Brian Bethune, chief financial economist of IHS Global Insight, a forecasting company in Lexington, Massachusetts. They have already acted separately, with the administration ending its $3 billion "cash-for-clunkers" automobile trade-in program on Aug. 24 and the Fed starting to wind down its purchases of Treasury debt, which totaled $285.2 billion between March 25, when the initiative began, and Sept. 16.

The 55-year-old Bernanke and his colleagues, who meet tomorrow and Wednesday to map monetary strategy, discussed "tapering" off the Fed’s purchases of mortgage-backed securities and housing-agency debt at their last gathering in August, according to the minutes of that meeting. No decision was made by the central bank’s policy-making Federal Open Market Committee.

Under the current program, the Fed is scheduled to buy up to $1.25 trillion of mortgage-backed securities and $200 billion of agency debt by the end of the year. So far, it has purchased $862 billion of the former and $125 billion of the latter. A trio of Fed presidents -- Jeffrey Lacker of Richmond, James Bullard of St. Louis and Dennis Lockhart of Atlanta -- has publicly raised the possibility the central bank might not spend all the money authorized for the mortgage-backed securities. Lacker questioned whether the economy needs the additional stimulus in an Aug. 27 speech.

New York Fed President William Dudley, who is vice chairman of the FOMC, has sounded more cautious. "The market expects us to complete these programs," he said Aug 31. "To contradict that market expectation is a pretty high hurdle."

An abrupt stop might push up mortgage rates by a half to one percentage point, said Hooper, a former Fed official. Tapering off -- by reducing weekly purchases and stretching them beyond the end of the year -- would have a more muted effect, pushing rates up by at least a quarter percentage point, he said, adding that the Fed may announce just such a strategy after its meeting this week. Mortgage rates for 30-year fixed home loans averaged 5.04 percent in the week ended Sept. 17, down from 5.07 percent the previous week, according to McLean, Virginia-based Freddie Mac, a government-controlled mortgage-finance company.

Borrowing costs for home buyers are relatively high based on the historical relationship with the Fed’s target rate for overnight loans between banks, currently at zero to 0.25 percent. The yield on the benchmark 10-year Treasury note is 3.22 percentage points more than the federal-funds rate, compared with an average of 1.45 percentage points during the past 20 years, according to data compiled by Bloomberg. Thirty-year mortgage rates average 1.69 percentage points more. While that is down from 3.19 percentage points in December, it is still above the average of 1.4 percentage points for this decade before the credit markets seized up in the second half of 2007.

The Fed’s purchases of mortgage-backed debt so far this year have dwarfed net issues of such securities by Fannie Mae, Freddie Mac and government-run mortgage-bond insurer Ginnie Mae, which totaled about $440 billion through the end of August, said Walt Schmidt, a mortgage-bond strategist in Chicago at FTN Financial. Once the Fed exits the market, the spread between yields on mortgage-backed debt and Treasury securities will have to rise, perhaps by a half percentage point, in order to attract other buyers, he said. The spread now is about 140 to 145 basis points, down from around 215 at the start of the year.

"One of the key linchpins to the restabilization of our economy is getting housing back," said Laurence Fink, chairman and chief executive officer of New York-based BlackRock Inc., the largest publicly traded U.S. money manager. "There is a great need" for the Fed to "continue to invest in the mortgage market right now," added Fink, 56. A number of Washington-based organizations -- the National Association of Home Builders, the National Association of Realtors and the Mortgage Bankers Association -- say an extension of the buyer’s tax credit is also crucial.

Lawrence Yun, chief economist of the realtors’ group, estimates that about 350,000 home sales through August were directly attributable to the tax credit of up to $8,000 for first-time buyers. Treasury Secretary Timothy Geithner, 48, called signs of stabilization in the U.S. housing market "very encouraging" and told reporters on Sept. 17 that the Obama administration will take a "careful look" at extending the credit.

Congress may not pass an extension; the chances "seem slim," said Mark Calabria, director of financial-regulation studies at the Cato Institute in Washington and a former staffer on the Senate Banking Committee. Public opposition to increasing the federal budget deficit is high, and there’s little appetite on Capitol Hill for finding spending cuts to offset the cost of the tax credit, he said.

The deficit will total $1.6 trillion this year as revenue falls and the government spends at the fastest pace in 57 years, according to the nonpartisan Congressional Budget Office. In a sign of the public’s concern about the deficit, 62 percent of people surveyed in a Sept. 10-14 Bloomberg News poll said they would be willing to risk a longer-lasting recession to avoid more government spending. The impact of terminating the tax credit will show up first in the new-home market, said David Crowe, chief economist of the home-builders’ association. "It takes at least four months to build a house, and you need to buy it before Dec. 1 to qualify," he said. "If you haven’t started building it by now, it’s too late."

Single-family housing starts fell 3 percent in August to a 479,000 annual rate -- the first decline since January -- according to seasonally adjusted figures in a Sept. 17 report from the Commerce Department. Residential construction and home sales led the way out of the previous seven recessions going back to 1960, according to David Berson, chief economist of PMI Group, a mortgage insurer in Walnut Creek, California. Real-estate sales fuel consumer spending, which historically accounts for about 70 percent of gross domestic product, he said.

"Housing has been the sector of the economy with the largest multiplier effect," said Berson, former chief economist at Fannie Mae. "Whether buying new homes or existing homes, people tend to fill them up with things: new furniture, new appliances, new window coverings." To be sure, some economists are betting the housing recovery is here to stay. The market has "clearly bottomed," said Dean Maki, chief U.S. economist for Barclays Capital in New York.

Even some of the optimists are hedging their bets given how dependent the market has been on government and central bank support. "I’m right in there with the rest of the cheerleaders, but there are no historical anecdotes, no historical data points to use for this," said Lewis Ranieri, the 62-year-old mortgage- bond pioneer who is chairman of New York-based Hyperion Partners LP. The U.S. housing market is "still very fragile."

Moody’s Property Index Resumes 'Steep' Fall in July

Commercial real estate prices in the U.S. resumed a "steep decline" in July after showing signs of leveling off in June, Moody’s Investors Service said, as credit restrictions curtail lending and push landlords toward default. The Moody’s/REAL Commercial Property Price Indices fell 5.1 percent in July from the month before, Moody’s said today in a statement. The index is down almost 39 percent from its October 2007 peak. The decline in June was 1 percent.

Commercial property sales this year may fall to an 18-year low. This latest set of numbers suggests no letup in that trend, said Neal Elkin, president of Real Estate Analytics LLC, a New York firm that partners with Moody’s in producing the report. "We are still vulnerable to moves on the downside," Elkin said in a telephone interview. "As time passes, the distress and the stress among those who need to sell is growing."

Elkin cited figures from Real Capital Analytics Inc., whose data are used in compiling the report, showing the portion of sales classified as "troubled" -- those properties in or close to default -- almost doubled to 23 percent in July from March. That’s "something we’ve never seen," Elkin said. Sales this year through July totaled about one-third of the year-earlier number, Moody’s Managing Director Nick Levidy said in the statement. The market averaged about 375 sales a month this year compared with almost 1,100 a month last year, he said.

Office sale prices fell 23 percent from a year ago in New York, 27 percent in San Francisco and 22 percent in Washington, according to the report. Prices of apartment buildings in the U.S. South have seen some of the steepest value declines, according to the report. Apartment prices in the [South] dropped 44 percent in the 12 months through June, almost twice the nationwide decline of 24 percent, and are now about half what they were two years ago. Florida apartment values tumbled 40 percent in a year, the report said. "That’s eye-popping," Elkin said. The decline is being caused in part by "a ripple effect" from the overbuilding of condominiums in those markets, many of which are now competing as rentals, he said.

Clunkers and Housing: A Government Subsidized Facade

by Michael Panzner

Although it was obvious from the start that the cash-for-clunkers program would not live up to the promises of proponents, hard evidence is beginning to trickle in that the pessimists were right. Instead of priming the pump for a self-sustaining recovery in the beleaguered auto sector (or the economy at large), the initiative simply borrowed sales from the future. Now that the government is no longer throwing free money at buyers, Automotive News reports in "September Sales Rate Will Tie Lowest on Record, Edmunds Says," the bottom has fallen out:Edmunds’ SAAR of 8.8 million would be lowest in nearly 28 years

September’s light-vehicle sales rate will fall to 8.8 million units, consumer auto site Edmunds.com said. That would be the lowest rate in nearly 28 years, tying the worst demand on record.

After the cash-for-clunkers program boosted August sales to their first year-over-year increase since October 2007, demand has plunged. In at least the last 33 years, the U.S. seasonally adjusted annual rate has only dropped as low as 8.8 million units once -- in December 1981 -- with records stretching back to January 1976.

Amid a global recession, U.S. sales fell to 13.2 million units in 2008, from 16.2 million in 2007. The slide continued, with demand ranging from 9.1 million to 9.9 million in the first half of this year.

Cynic that I am, I wonder if this rapid and painful reversal of fortunes is giving us a taste of what's to come in the housing market, which is at risk of losing at least some of the substantial financial assistance being provided to it by Washington in the months ahead? In "Policy and Housing: Someone’s Gotta Give!" Angry Bear's Rebecca Wilder highlights some developments to keep an eye on:

Housing demand is being propped up by government subsidies and low mortgage rates, and the level of supply is held back by low prices. Right now, the housing market is a complicated hodgepodge of policy, foreclosures, and very weary potential home-buyers.

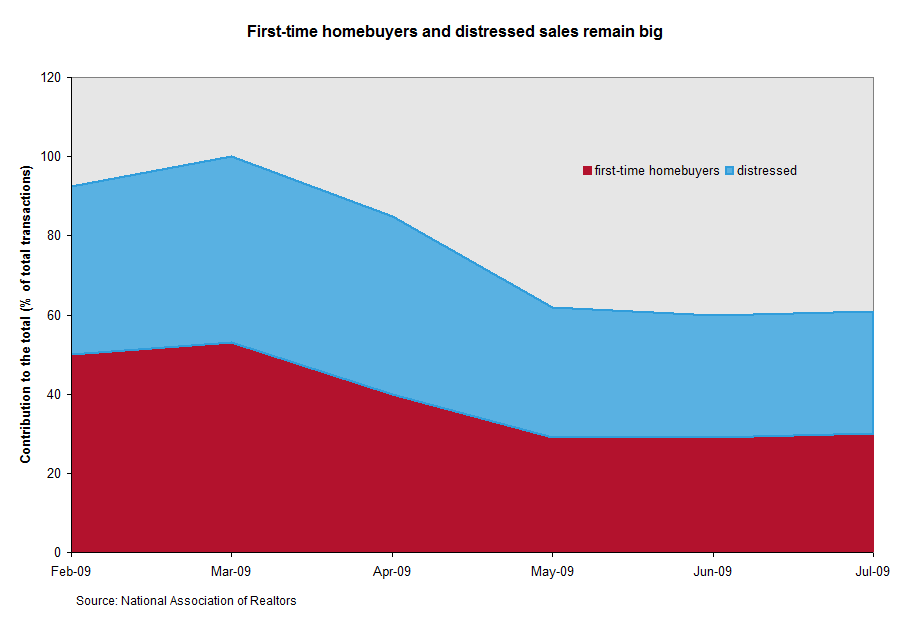

Home sales are stabilizing; home building is stabilizing; and home prices (might be) stabilizing - the chart to the left illustrates a positive trend in sales away from distressed and first-time home-buyers, the targets of policy, according to the NAR. But what would the housing market look like if the massive policy expired this year? Not good, and it will.

Some points on the housing market:Subsidies are set to expire. If the Fed continues to buy its average of $105 billion in GSE-backed MBS per month (see the NY Fed’s website for weekly updates), it will max out the announced $1.25 trillion in four months. The $8,000 tax credit for first-time home-buyers expires at the end of this year. The Fed’s Treasury buyback program will run its course by October.

There are several home price indices out there, each painting a slightly different picture of the level and trend in aggregate home values (see AB post).

The foreclosure modifications program is holding off some foreclosures; but the program is no match for market forces.

There is a large shadow inventory out there - potential sellers that are reluctant or unwilling (TIME calls some of these sellers accidental landlords”) to relinquish home ownership at current prices. However, if home values continue to take baby steps forward, shadow sellers (new supply) will emerge.

There is a bimodal distribution of sales across the high-end and low-end housing markets. Low-end sales are hot, while the upper end is not.

House Moves To Extend Unemployment Benefits

Despite predictions the Great Recession is running out of steam, the House is taking up emergency legislation this week to help the millions of Americans who see no immediate end to their economic miseries. A bill offered by Rep. Jim McDermott, D-Wash., and expected to pass easily would provide 13 weeks of extended unemployment benefits for more than 300,000 jobless people who live in states with unemployment rates of at least 8.5 percent and who are scheduled to run out of benefits by the end of September.

The 13-week extension would supplement the 26 weeks of benefits most states offer and the federally funded extensions of up to 53 weeks that Congress approved in legislation last year and in the stimulus bill enacted last February. People from North Carolina to California "have been calling my office to tell me they still cannot find work a year or more after becoming unemployed, and they need some additional help to keep their heads above water," McDermott said.

Critics of unemployment insurance argue that it can be a disincentive to looking for work, and that extending benefits at a time the economy is showing signs of recovery could be counterproductive. But this recession has been particularly pernicious to the job market, others say. Some 5 million people, about one-third of those on the unemployment list, have been without a job for six months or more, a record since data started being recorded in 1948, according to the research and advocacy group National Employment Law Project. "It smashes any other figure we have ever seen. It is an unthinkable number," said Andrew Stettner, NELP's deputy director. He said there are currently about six jobless people for every job opening, so it's unlikely people are purposefully living off unemployment insurance while waiting for something better to come along.

The current state unemployment check is about $300 a week, supplemented by $25 included in the stimulus act. That doesn't go very far when a loaf of bread can cost $2.79 and a gallon of milk $2.72, Senate Finance Committee Chairman Max Baucus, D-Mont., said at a hearing last week on the unemployment insurance issue. "We need to keep our unemployed neighbors from falling into poverty. We need to figure out how best to make our safety net work," Baucus said.

The jobless rate currently stands at 9.7 percent and is likely to hover above 10 percent for much of 2010. Gary Burtless, a senior fellow at the Brookings Institution, said at the Finance Committee hearing that, according to Labor Department figures, 51 percent of unemployment insurance claimants exhausted their regular benefits in July, the highest rate ever. "It is likely the exhaustion rate will continue to increase in coming months" as the unemployment rate continues to rise, he said. Stettner predicted that Congress will likely have to continue extending jobless benefits through 2011.

McDermott in July introduced a more ambitious bill that would have extended through 2010 the compensation programs included in the stimulus act. Those benefits are now scheduled to expire at the end of this year. But with a price tag of up to $70 billion, that bill would have been far more difficult to pass. McDermott instead decided to offer the scaled-down 13-week extension to meet the urgent needs of those seeing their benefits disappear this year.

McDermott said his bill would not add to the deficit because it would extend for a year a federal unemployment tax of $14 per employee per year that employers have been paying for more than 30 years. It would also require better reporting on newly hired employees to reduce unemployment insurance overpayments. Three-fourths of the 400,000 workers projected to exhaust their benefits this month live in high unemployment states that would qualify for the additional 13 weeks of benefits under his bill, McDermott said.

They include Alabama, Arizona, California, District of Columbia, Florida, Georgia, Illinois, Indiana, Kentucky, Massachusetts, Michigan, Mississippi, Missouri, Nevada, New Jersey, North Carolina, New York, Ohio, Oregon, Pennsylvania, Puerto Rico, South Carolina, Tennessee, Washington, Wisconsin and West Virginia. Other states could qualify for more benefits if their unemployment rates are approaching the 8.5 percent threshold.

Bank of England warns of the consequences of thrift

An attempt by British consumers to rein in spending after the harsh lessons of the recession could limit growth and therefore depress household income further, the Bank of England warns today. It says in its latest Quarterly Bulletin that household decisions to spend or save will have major consequences for the economic outlook, because consumer spending accounts for two-thirds of total spending in the UK. "Any attempt to reduce consumption is likely to push down on output and hence household incomes. That could actually make it harder for households to increase their savings – known as the paradox of thrift."

The Bank says that even if households saved as much as 10pc of income, it would take nine years to bring wealth back up to the average of the last 20 years. Credit conditions are likely to remain tight, the Bank says, which could limit spending – as could job insecurity. The Bank also says that most financial asset prices have continued to increase over the third quarter and conditions in bank funding markets have improved. Improvement in sentiment has prompted analysts to revise upwards their expectations for short-term corporate earnings, coinciding with a rise in equity prices. It reveals in the Bulletin that, from July 24 to August 4, the Bank did not buy any corporate bonds after receiving no offers in five consecutive auctions.

Retirement? Good luck with that

The destructive effects of the financial crisis may be waning, but your retirement account won't soon forget. Savers lost 40% or more in the downturn -- a collective $2.1 trillion disappeared from 401(k) and IRA assets in 2008 alone -- and while the recent stock-market recovery may feel good, it's done little to stem a mounting crisis in the retirement system in the United States. It's not just investments that are the problem: Social Security needs financial resuscitation, and the bursting of the housing bubble that helped spark the financial crisis vaporized the home equity many people were counting on to fund their golden years. Corporations are curtailing traditional pensions and older Americans are being forced to work longer to make up the difference.

Where does this leave our retirement plans? Ask a middle-class American when he plans to retire, and more often than not you'll get a wry chuckle and "I'll be working until I die." The attempt at humor masks what may be close to reality for some people. The retirement-savings system in the U.S. is "a failed experiment," said Teresa Ghilarducci, the Bernard Schwartz professor of economics at The New School for Social Research in New York.

The U.S. system is "headed for a serious train wreck," said John Bogle, founder and former chief executive of the Vanguard Group, in testimony to a House committee hearing on retirement security in February.

Separately, Ghilarducci and Bogle each have called for some substantial changes to the current system, but even those who like what we've got now say it needs improving -- and certainly demands better financial education be offered to savers.

"Many people are very overwhelmed with the notion of retirement," said Gregg S. Fisher, president and chief investment officer of Gerstein Fisher, a financial advisory firm. "How much do we need to put away? Where should it go? How should I invest?" Read tips on how you could help your nest egg recover more quickly.

Of course, people's retirement outlooks vary widely. Some 20 million workers still participate in a traditional pension plan, and employers pay pension benefits to millions more retirees (that doesn't even count government-sponsored public plans), according to Boston College's Center for Retirement Research. Those workers are sitting a lot prettier than the more than half of U.S. families who aren't covered by any kind of pension at their current job, according to the Employee Benefit Research Institute, a nonprofit, nonpartisan group. Still, even a well-prepared person may get thrown off by a job loss or unexpected health-care costs. (Average medical costs in retirement can run into the six figures even for those covered by Medicare, according to EBRI.)

And those lucky people with traditional pensions likely are wondering how long the money will last as the financial crisis shreds employers' ability to fund such plans for the long haul. See related story on PBGC.

Defined-contribution plans such as 401(k)s have largely taken the place of traditional pensions: 67% of workers say they have a DC plan, up from 26% in 1988, while 31% of workers participate in a traditional pension, down from 57% in 1988, according to EBRI.

But, while lower-income workers face a worrisome retirement reality all their own, middle- and upper-middle class workers likely face the biggest living-standard shock. That's because lower-income people can replace a good chunk of their preretirement income with Social Security, and high-income people generally have enough personal savings. But middle-class workers may see their relatively comfortable life change drastically come retirement.

"People in the middle and upper-middle have highly variable rates of savings," said Eric Toder, a fellow at the Urban Institute, a nonprofit, nonpartisan research center in Washington. Social Security will take up some of the slack, but the program was never intended to provide full wages -- it replaces about 57% of lower-income workers' preretirement wages, about 43% of medium-income earnings, and 35% of higher-income earnings. A replacement rate of 70% to 75% usually allows retirees to maintain their standard of living, according to a report by the Center for Retirement Research.

And Social Security's and Medicare's financial outlook means that future retirees likely will find the program pays even less. Without changes, the Social Security trust fund is expected to run out in 2037 and Medicare will be broke by 2017. The financial outlook for both programs has worsened as the recession and 6 million job losses have shrunk tax revenues.

You could argue that whatever system we have now is better than nothing, and before the creation of Social Security in 1935, few people other than government workers had a retirement-savings plan. Of course, back then, shorter life spans made retirement savings less crucial. Combine the growth in private pension plans during World War II with Social Security and you get a veritable golden age of retirement savings, at least for those -- never more than about half the work force -- who participate in workplace plans.

Now, thanks to the slow death of the traditional pension and the rise of 401(k)-type plans, one thing is clear: Workers are increasingly responsible for managing their retirement investments. Some say that's a major problem. "For 30 years we thought that if we gave people financial advice that over time they would learn something," Ghilarducci said. "But just as we can't expect people to excise their own molars or do their own surgery, we can't expect them to professionally manage their money over a long period of time."

Others agree risk is an issue. "People are being exposed to risk that they're not even aware of and they're being told don't worry about it, as long as it's far in the future everything will be all right," said Zvi Bodie, professor of finance at Boston University's School of Management and co-author of the book "Worry-Free Investing." "That's complete nonsense," he said. What matters, he said, is the risk that on the day you need the money your investments have tanked.

The recent market crash is a sharp reminder of what can go wrong. Sure, the S&P 500's almost 35% rebound since March is good news, but it's not enough to make savers whole. From its peak in Oct. 2007 through this March, the S&P 500 lost almost 49%. Shave 49% off a $100,000 investment and you'll need a 96% gain just to get back to even. Younger savers can overcome that hit with time, but it's a lot tougher for people close to retirement, and nigh impossible for retirees forced to pull money out to live on just as the market swoons.

As for tapping into home equity in retirement? While homeowners' equity did rise in the second quarter, U.S. households lost real-estate wealth for nine consecutive quarters before this second-quarter gain, according to the Federal Reserve. Moody's Investors Service said recently it'll take 10 years before housing prices regain their peak. U.S. household net worth is down $12.2 trillion from the high in 2007, thanks to the stock-market crash and the housing-market meltdown.

The retirement-savings crisis is not going unnoticed. The Obama administration, plus the AARP and many academic researchers, see automatic workplace-plan enrollment as the first step to pumping up retirement savings. Forcing workers to opt out of their 401(k) rather than waiting for them to opt in dramatically raises participation rates (inertia leads most people to stick with the plan). The president has proposed at least two retirement-savings laws (Congress has yet to act on either). With "automatic IRAs," employers who don't offer a workplace plan now would enroll workers in an IRA to which workers could contribute via their paycheck. Obama also wants to expand the savers' credit, which rewards people who put money aside for retirement.

Some are calling for more extreme changes. In February, Bogle, the Vanguard founder, spoke in favor of defined-contribution plans, but decried the inadequate savings rates -- the median balance at the end of 2008 was just $15,000 -- and steep costs, among other problems. He called for a Federal Retirement Board to oversee the system and look out for participants' best interests. Ghilarducci, the economist, proposes reducing the tax break for 401(k)s by lowering the maximum annual contribution to $5,000, then using the tax revenues to create mandatory guaranteed accounts for all. The government would contribute $600 annually to every account; people would contribute 5% of income annually.

The government-managed account would belong to the individual, and would be in addition to Social Security. Ghilarducci said capping 401(k) contributions pays for the plan. One of Ghilarducci's gripes with the current system is that retirement-plan tax breaks go largely to higher-income earners -- she'd like to see the government's largesse spread more equitably. Looking at all types of tax-advantaged retirement plans, people with income above $104,000 enjoy 80% of the tax breaks, according to research co-authored by Toder of the Urban Institute.

It's not hard to find people who disagree with Ghilarducci's approach. "The idea of centrally planning peoples' investment strategies is not appropriate and is going to take away from the beauty of the system, which is really one of self-determination," said Mike Francis, president of Francis Investment Counsel LLC in Pewaukee, Wis. Currently, he said, people can choose a low-risk, low-return plan (which may require a higher savings rate) or they can take on more risk to get more return.

Plus, in surveys, employees usually say they like their 401(k) plans. Also, workers can take their 401(k) to a new job, unlike traditional pensions. That's important in economic times like this, Francis said. "You could argue," he said, that the millions of people who've lost a job in the recession "are meaningfully better off having participated in a defined-contribution program than they would have been in a defined-benefit plan." But there's still that nagging problem: A huge amount of risk is being put on individual's shoulders. Bodie says 401(k)s are fine as long as savers invest the right way -- for Bodie that means not putting essential assets at risk in the stock market.

His choice for retirement plans: Treasury Inflation Protected Securities. "What anybody wants," Bodie said, "is a supplement to their Social Security benefits -- something that is protected against inflation, is guaranteed for life, and doesn't have the same political risk as Social Security." In the end, it may be that baby boomers simply pay a steep cost for living at a time when defined-benefit plans started disappearing. As the retirement-savings system goes through a seismic shift, young adults today are seeing the mistakes their parents made -- most notably, failing to save early and often.

Younger people will "learn a lot of lessons about the stock market. They won't expect a job for life. They'll probably be more self-reliant," said Frank Haines, chief investment officer with Christian Brothers Investment Services Inc. in New York. "If you can do it at a young enough age, the power of compounding is very, very powerful," he said. "Unfortunately, it's the generations in their 30s to 60s who probably weren't instructed to do that as much as they should have been."

Bank of America to Pay for Merrill Backstop, Faces SEC Trial

Bank of America Corp., the biggest U.S. bank, said it will pay the government $425 million to cancel an unused guarantee of Merrill Lynch & Co.’s assets and cut reliance on federal support after two bailouts. The payment would end a dispute over what the bank owes the U.S. for a promise to help absorb losses on $118 billion of holdings, mostly at Merrill Lynch. The federal guarantee helped seal Bank of America’s takeover of the New York-based brokerage after fourth-quarter losses spiraled past $15 billion. While the accord was announced in January, an agreement was never signed and the bank resisted paying.

Chief Executive Officer Kenneth D. Lewis has said he wants to shrink the U.S. role in company affairs. Paying the fee is part of a plan to reduce "reliance on government support and return to normal market funding," the company said today in a statement. The Treasury Department, Federal Reserve and Federal Deposit Insurance Corp. will get the money. "The bank is a wounded duck and everybody wants a piece of them," said Robert Serino, a partner at Buckley Sandler LLP in Washington and a former director of the Comptroller of the Currency’s enforcement and compliance division.

"In the past, Ken Lewis was a pretty strong character but now he’s been beaten down like everybody else." Even as the payment was announced, the Securities and Exchange Commission pledged to "vigorously pursue" a case against the bank for not disclosing $3.6 billion in bonuses to Merrill before the acquisition was completed. U.S. Judge Jed Rakoff last week rejected a $33 million settlement, accusing both the bank and SEC of trying to avoid a public trial.

Bank of America also faces pressure from Representative Edolphus Towns, a New York Democrat and chairman of the House Oversight Committee, who scolded the bank today for missing a deadline to turn over documents sought by his panel. Chief Marketing Officer Anne Finucane plans to meet with Towns to discuss how to provide information "without violating attorney- client privilege," bank spokesman Scott Silvestri said. Lewis "is holding up very well," spokesman Robert Stickler said. "He doesn’t dwell on things that he can’t control and he remains convinced that the deal will be a good one for shareholders over time."

The Merrill asset guarantees prompted regulators to press for compensation from the Charlotte, North Carolina-based bank. The government said Bank of America benefited from the accord’s implied U.S. backing for three to four months as investors were speculating the company might fail or be nationalized. The agreement reflects "an encouraging sign of increased stability in the financial system," Treasury spokesman Andrew Williams said. The bank said in July it expected a settlement of the dispute within 30 days.

"This is another terrible deal for taxpayers negotiated by the U.S. Treasury," said Linus Wilson, a University of Louisiana professor who has studied government bailout programs. The bank is paying less than 10 percent of a potential $4.3 billion cost, including warrants associated with $4 billion in preferred shares cited in the term sheet and never issued. "The insurance company does not refund most of your premium just because you did not wreck your car in the last six months," Wilson said. Bank of America hasn’t received permission to repay the extra $20 billion of U.S. rescue funds that came with the Merrill deal, Chief Financial Officer Joe Price said last week. The bank received a total of $45 billion from the Troubled Asset Relief Program and expects to repay the money in installments, pending approval by regulators, Price said.

The bank today added its sixth new board member this year, tapping DuPont Co. Chairman Charles "Chad" Holliday Jr. Bank of America will have 15 members on its board, down from 18, with all positions now filled. Holliday "will get the board to gel in the proper way," said Ram Charan, an author, management consultant and former Harvard Business School professor who said he has known the DuPont executive for 25 years. "The board will do what is necessary to get the most out of a franchise that is the envy of the rest of the banking industry." During Holliday’s 11 years as DuPont CEO, the shares of the third-biggest U.S. chemical maker declined 55 percent. Bank of America shares have dropped by more than a third since Lewis took over as CEO in April 2001. Holliday didn’t respond to a request for a comment through DuPont spokeswoman Lori Captain.

It takes character to call time on a cover-up

First there was Bloodgate – a leader ordering a disreputable act, attempting to cover it up and almost getting away with it. The leader was Dean Richards, veteran England rugby international and, latterly, rugby director at the London club Harlequins. In the final minutes of a crucial cup match, Richards wanted Tom Williams, one of his players, off the field so that he could send someone else on. He gave instructions that Williams should fake a bloody injury.

Williams did this by biting a joke-shop blood capsule he had been given and lying on the field. To the staff of the opposing team, it was clearly not blood dribbling from his mouth. He did not improve matters by winking as he came off.

At the disciplinary hearing, Richards, Williams and two other Harlequins officials denied everything. The hearing decided there was insufficient evidence to find anyone guilty, apart from Williams, whom it suspended from playing for 12 months. Shocked at being singled out, Williams took independent advice for the first time. He decided to tell the full story to an appeal committee. Richards then confessed to organising both the incident and the cover-up. He admitted that Williams’ fake injury "looked like something out of the circus". The appeal committee suspended Richards from rugby management for three years. It reduced Williams’ suspension to four months.

Now we have Crashgate. Once again, a leader is accused of organising a cheating incident – this one potentially lethal. Nelson Piquet Jr, a Formula One racing driver, claimed he had been ordered by his bosses at Renault to crash during last year’s Singapore Grand Prix, which he did, to help team-mate Fernando Alonso win. Flavio Briatore, managing director of the Renault team, initially denied it and accused Piquet and his father of blackmail. Last week, however, Renault announced the departure of Briatore and Pat Symonds, the engineering director, and said it would "not dispute" Piquet’s allegations. Briatore was yesterday banned for life and Symonds for five years. Piquet had less compunction about pointing the finger than Williams, but then Renault had fired him during the summer.

Our third attempted cover-up does not seem to have a name yet, but perhaps we can call it "Merrillgate". Last year, when Bank of America announced the acquisition of Merrill Lynch, it told its shareholders that Merrill had agreed not to pay year-end performance bonuses without BofA’s consent. In fact, BofA had already agreed that Merrill could hand out up to $5.8bn in bonuses. The Securities and Exchange Commission investigated but did not discover who was responsible. To resolve the matter, the SEC and BofA agreed that the bank would pay a fine of $33m and undertake not to make any future false statements. The bank would not admit or deny the accusations. The SEC and the BofA submitted this agreement for the approval of Judge Jed Rakoff of the US district court, southern district of New York.

I like US court judgments: their type-written appearance is often matched by a similarly old-fashioned clarity of exposition. Judge Rakoff did not disappoint. Usually, he said in his judgment last week, the courts did not interfere with the amicable resolution of disputes, provided they were "within the bounds of fairness, reasonableness and adequacy". Was this one? No. "It does not comport with the most elementary notions of justice and morality," he said. What the two sides were proposing was that "the management of Bank of America – having allegedly hidden from the bank’s shareholders that as much as $5.8bn of their money would be given as bonuses to the executives of Merrill who had run that company nearly into bankruptcy – would now settle the legal consequences of their lying by paying the SEC $33m more of their shareholders’ money".

The SEC and BofA were asking him to agree that "the victims of the violation pay an additional penalty for their own victimisation". The SEC argued the penalty sent a signal that shareholders needed to assess the quality of BofA management. Judge Rakoff replied: "The notion that Bank of America shareholders, having been lied to...need to lose another $33m of their money in order to ‘better assess the quality and performance of management’ is absurd." Corporate cover-ups go on all the time. If Williams had not felt scapegoated and Piquet not been fired, perhaps their bosses would have escaped detection. BofA’s executives seem to have thought they could get away with it too. Another judge might have let them. Their misfortune was to come up against one as luminous as he was angry.

Bank chiefs owe a personal debt to taxpayers

by William Cohan

Few could argue with Barack Obama last week when the US president said Wall Street owed a debt of gratitude to taxpayers. Some of America’s largest banks would not have survived without the trillions of dollars the government used to shore up the financial sector. Less remarked upon, however, is the personal windfall executives of the bailed-out institutions received as a result of Washington’s largesse. This is no doubt a controversial conclusion, since most of the chief executives whose banks were forced to take funds from the troubled asset relief programme, or Tarp, nearly a year ago will point immediately – and correctly – to the fact that many of them eschewed a bonus for 2008.

For instance, Lloyd Blankfein of Goldman Sachs was paid about $70m in 2007 but only his $600,000 salary for 2008 (plus $111,000 for the cost of a car and driver). John Mack, who has just announced his resignation as chief executive of Morgan Stanley effective from January 2010, received an annual salary of $800,000 (plus $438,000 of imputed income from perks such as use of the corporate jet, which Morgan Stanley requires for "security" purposes) in 2008. He never received a cash bonus during his four and a half years at the helm at Morgan Stanley, although he did receive 500,000 shares of restricted stock, then worth $26m, when he rejoined the bank from Credit Suisse in June 2005. Jamie Dimon, chief executive of JPMorgan Chase, had to make do with his $1m salary in 2008 (plus car and driver and aircraft income) but received no cash bonus. Ken Lewis, the chief executive of the beleaguered Bank of America, somehow came out the winner on a relative cash basis in 2008, with a salary of $1.5m and, like the others, perk allowances and no cash bonus.

But whether these men received a cash bonus or not in 2008 almost certainly obscures the important larger point: the bail-outs of their banks through the Tarp, through the Federal Deposit Insurance Corporation guarantees of their debt financings and through government-backed securitisation programmes such as the term asset-backed loan facility, or Talf, provided an essential boost to long-term investor confidence – and their stock prices – at a crucial juncture. This is how each of these men benefited personally from the government bail-outs.

To be sure, the government’s initiatives were not solely responsible for keeping these institutions alive. Their own efforts were crucial too, whether it was Goldman’s decision to raise $10bn from both the public markets and from investor Warren Buffett on September 29 or Morgan Stanley’s ability to raise – in a cliffhanger – $9bn from UFJ Mitsubishi on October 10. But the $10bn both Goldman and Morgan Stanley received from the Tarp on October 13 did not hurt either, and nor did the swift approval by the Federal Reserve – on September 22 – that allowed the two to become bank holding companies and thus receive virtually free financing on a regular basis from the central bank. As for Bank of America, it would be hard to argue that without the US taxpayers’ $45bn the bank would still be around. (For what it is worth, JPMorgan does not believe it was bailed out but rather that it helped save other banks.)

What is not hard to argue is that the smorgasbord of government programmes and initiatives have helped ensure the survival of these institutions by restoring investor confidence, in turn boosting their stock prices and the value of the chief executives’ stock holdings.

For instance, Mr Blankfein’s 3.4m shares of Goldman, worth about $168m at one point last year, were worth closer to $623m (€425m, £385m) at Friday’s closing prices. Mr Mack’s 4m Morgan Stanley shares, which were worth as little as $27m, have rebounded to $125m. Mr Dimon’s 11.2m shares of JPMorgan are valued at about $503m these days, up considerably from their recent low of $168m. And Mr Lewis’s 4.7m Bank of America shares, at one point valued at around $15m, are now worth about $83m. These calculations do not reflect the additional increased value of the executives’ stock options and unvested stock awards, which have moved up smartly – at least on paper (they are not tradeable) – as a result of the rise in the banks’ stock prices.

This is not a trivial matter, although it is barely mentioned. Those who find the observation petty or unfair would do well to ask Dick Fuld, Lehman Brothers’ one-time chief executive, if he would be willing to trade places with any of his former Wall Street brethren. Unlike Mr Blankfein and Mr Mack, he could not win Fed approval to convert Lehman into a bank holding company. We all know there was no government bailout for Lehman. After Lehman filed for bankruptcy a year ago, Mr Fuld’s 10m shares of Lehman plus options – once worth as much as $1bn – were rendered worthless, which seems like the correct price for the stock of a bank that was way overleveraged and took too many foolish risks. "I don’t expect you to feel sorry for me," Mr Fuld testified in front of Congress last October. And we don’t.

But a year later, we still have no good answer as to why the other chief executives were permitted to benefit from the government’s largesse while Mr Fuld could not.

Congressional Report Says A.I.G. Has Stabilized

The research arm of Congress reported on Monday that the American International Group’s financial condition had stabilized but said it was not clear whether the giant insurance group would ever be able to restructure and repay its federal rescue package. The Government Accountability Office’s new report on the bailout of A.I.G. coincided with word that a senior House Democrat was planning to push for an easing of A.I.G.’s terms on its government debt.

Representative Edolphus Towns of New York, the chairman of the House Committee on Oversight and Government Reform, was said to be considering debt relief after meeting last week with Maurice R. Greenberg, A.I.G.’s former chief executive, who was forced out during an accounting scandal in 2005. The terms of A.I.G.’s rescue have already been eased three times because they were too tough for the troubled giant to manage. The company has been extended $182 billion by the Federal Reserve and the Treasury, although not all of it has been in use at the same time.

The G.A.O. said the huge bailout had succeeded in braking A.I.G.’s fall by the first half of this year, and was producing signs of improvement among A.I.G.’s individual insurance companies. Although the crisis at A.I.G. was touched off by exotic derivatives, other activities, such as a risky securities-lending program, harmed its insurance business, too. The government researchers said A.I.G.’s ability to turn the corner would depend on "the long-term health of the company, market conditions, and continued government support."

Fed not acting like there's a recovery

Federal Reserve Chairman Ben Bernanke has said that the recession is "very likely over," but the Fed isn't acting like we're in a recovery. Economists widely believe the central bank will keep interest rates between 0% and 0.25% at the conclusion of its two-day meeting Wednesday. The Fed is also expected to say very little about its plans to wind down more than a trillion dollars in lending and bailout programs, and it will likely stay away from any overly enthusiastic language about the economic outlook.

"This will be one the quietest Fed meetings in quite some time," said Rich Yamarone, director of economic research at Argus Research. "The last thing they want to do at this stage of the game is to upset the apple cart. They're liking what they're seeing in some of the economic data, so it's just steady as she goes." The Fed uses its rate-setting tool in an attempt to balance unemployment and inflation, typically lowering rates during a recession to boost economic activity and raising rates coming out of a downturn to stave off rampant inflation.

But experts argue that the recovery from this recession is so tenuous that the Fed is right to keep its finger off the rate-hike button for now. "The Fed normally anticipates the recovery by raising rates, taking away the punch bowl just as the party gets interesting," said Peter Morici, professor of economics at the University of Maryland. "But this is not a normal recovery. It's tepid and weak." Unemployment is still rising, retail sales are far from robust, manufacturers' capacity utilization remains at ultra-low levels and wages are still depressed. Home sales and new home construction are making a comeback, but they're coming off of historic lows.

Inflation not an issue for now: As a result of the still shaky economy and low consumer confidence, concerns about inflation have been mostly muted. "If people aren't spending the money, you can't have inflation," said Morici. "If Bernanke puts a pile of money out on the street, it doesn't count if it doesn't chase goods." Still, the Fed continues to oversee dozens of expensive and unprecedented economic rescue programs. They have largely been credited with staving off an even deeper and more prolonged recession, but they could contribute to out-of-control inflation if they are not pared back in time.

"Bernanke is a student of history, and he knows that the real problems during the Depression occurred when the government pulled back its stimulus too quickly," said Doug Roberts, chief investment strategist at ChannelCapitalResearch.com. "Also, the Fed chief is up for reappointment, and he won't help his case if unemployment hits 12, 13 or 14%." "But at the same time, he should start to gently pull back some of the programs to ease inflation concerns," Roberts added.

No rate changes until next year: Roberts said a gradual winding down of those programs will reduce the risk of inflation without slamming the brakes on the recovery. Most economists think the Fed is keeping a close eye on any signs of stabilization in the labor, banking and housing sectors. When those become more obvious, the Fed will need to aggressively raise rates and end those emergency lending initiatives.

But a majority of forecasts don't show stabilization until the end of the year or beginning of 2010. Until then, the Fed is likely to keep rates unchanged so it doesn't disrupt what appear to be the underpinnings of an economic rebound. "The idea is to not tighten up too soon," said Morici. "If the economy turns down again, we could fall off the cliff."

Fed Rejects Geithner Request for Study of Governance, Structure

The Federal Reserve Board has rejected a request by U.S. Treasury Secretary Timothy Geithner for a public review of the central bank’s structure and governance, three people familiar with the matter said. The Obama administration proposed on June 17 a financial- regulatory overhaul including a "comprehensive review" of the Fed’s "ability to accomplish its existing and proposed functions" and the role of its regional banks. The Fed was to lead the study and enlist the Treasury and "a wide range of external experts."

Some top central bank officials, after agreeing to the review, saw a potential threat to Fed independence after the Treasury released the proposal, two of the people said. The Obama plan said the Treasury would consider recommendations from the review and "propose any changes to the Fed’s governance and structure." "It is not obvious at all why that is a Treasury responsibility or even appropriate why the Treasury would undertake that kind of study," said Robert Eisenbeis, chief monetary economist at Cumberland Advisors Inc. in Vineland, New Jersey, and a former Atlanta Fed research director. "The Fed was created by Congress and it is not part of the executive branch."

U.S. lawmakers have also called for a review of the Fed’s power and structure, saying Fed Chairman Ben S. Bernanke overstepped his authority as he bailed out creditors of Bear Stearns Cos. and American International Group Inc. while battling a crisis that led to $1.62 trillion in writedowns and losses at financial firms. While the report requested by the Treasury hasn’t been formally scrapped, no work has been done on the project, which was due Oct. 1, the people said. Treasury spokesman Andrew Williams declined to comment, as did Fed spokeswoman Michelle Smith.

The central bank is performing its own reviews of possible operational changes following the financial crisis. Fed Governor Elizabeth Duke is leading an internal study of the roles of the directors that serve on each of the boards at regional Fed banks. "The institution is trying to keep a low profile," said Vincent Reinhart, a resident scholar at the American Enterprise Institute in Washington and the former director of Division of Monetary Affairs at the Fed Board. "To publish a report now invites comment on that report."

The Senate passed 96-2 a nonbinding budget amendment in April supporting "an evaluation of the appropriate number and the associated costs" of the district banks. The measure was sponsored by Senate Banking Committee Chairman Christopher Dodd, a Connecticut Democrat, and Alabama Senator Richard Shelby, the senior Republican on the panel. House Financial Services Committee Chairman Barney Frank, a Massachusetts Democrat, has also called for more scrutiny of the central bank, saying last year he aims to probe how the 12 regional Fed presidents are appointed and their role in setting interest rates. The Fed banks are semi-private entities, each overseen by a nine-member board of directors.

Legislation in both houses of Congress would allow for audits by the Government Accountability Office of the central bank’s monetary policy and other operations. Bernanke opposes the measure, which was introduced in the House by Representative Ron Paul of Texas, a Republican. Frank has scheduled a committee hearing on the issue for Sept. 25. Along with the study by Duke, the Fed is reviewing how to overhaul supervision based on lessons learned from the financial crisis. The Treasury interest in a Fed structural review partially stems from the administration’s proposal to make the central bank the lead regulator for the largest, most inter-connected financial institutions.

Fed Governor Daniel Tarullo, an Obama appointee, is working on changes to the supervisory process that are preparing the central bank for a larger role in tracking risks across the financial system. Tarullo is focusing on bank-to-bank comparisons and quantitative scenario testing of bank portfolios. The Fed is currently examining the vulnerability of banks with assets under $100 billion to falling commercial real estate values. Congressional leaders have balked at the notion of giving the Fed more power and are leaning toward vesting authority over capital, liquidity and risk-management practices of big banks in a council of regulators. "There will be a council," Frank told Bloomberg Television Sept. 14.

The review led by Duke followed the resignation in May of Stephen Friedman as New York Fed chairman because of ties to Goldman Sachs Group Inc. Friedman is a director on Goldman Sachs’s board.

Goldman Sachs became a bank holding company in September 2008, a change that would have normally barred Friedman from continuing to serve in his New York Fed post. Officials gave him a waiver so he could remain in the job, which has mostly an advisory role. Friedman, chairman of Stone Point Capital LLC, said at the time of his resignation that he had complied with all the Fed’s rules and his service on the board was "mischaracterized as improper." Some analysts said a Fed revision of the role of directors is overdue.

"Allowing local bankers to play a leading role in selecting reserve bank presidents is the most worrying aspect of the current system," Lou Crandall, chief economist at Wrightson ICAP LLC, wrote to clients in July. District bank presidents are nominated by committees made up of people whose institutions the nominees may have supervised. "The conflicts of interest inherent in the current system are glaring," Crandall said.

Ginnie Mae MBS seen vulnerable to FHA loan losses

Investors in U.S. mortgage bonds backed by the Federal Housing Administration own one of the safest bets on Wall Street, yet mounting defaults on the underlying collateral are seen posing risks. Ginnie Mae pools loans backed by the FHA and Veterans Administration and packages them into mortgage-backed securities. Unlike its mortgage market counterparts, Fannie Mae and Freddie Mac, they carry the full faith and credit of the U.S. government.

But homeowners have increasingly been defaulting on their mortgages, leading to uncertainty about the timing of cash flows and raising the risk that Ginnie Mae bonds will be paid back early, a phenomenon known as prepayment risk. MBS investors do not want to be paid early. An issuer may repurchase loans which are in default and this repurchased loan is paid in full to the investor at par, who then must reinvest the proceeds, possibly in lower yielding securities. The only risk of loss is to the extent an above par price was paid.

Ginnie Mae bonds have become very richly valued on the back of their government guarantee, and some investors are exiting the debt because they don't think the prices can hold. "We have been net sellers of Ginnie Mae MBS due to rich valuations of these securities," said Jeffery Elswick, director of fixed income at Frost Investment Advisors in San Antonio, Texas. So far in 2009, Ginnie Mae MBS prepayments have been running ahead of Fannie Mae and Freddie Mac due to greater, relative to the other U.S. mortgage agencies, mortgage defaults as well as a shorter timing in loan modifications.

"This has resulted in higher prepayment volatility and lower future relative valuations in Ginnie Mae MBS relative to the other conventional agency MBS," Elswick added. Some 7.8 percent of FHA-backed loans were 90 days late or more delinquent, or in the foreclosure at the end of June, according to the Mortgage Bankers Association, up from 5.4 percent year ago. These loan losses have taken a toll on the FHA's reserves. The FHA on Friday proposed a number of rules changes designed to improve credit quality of FHA-guaranteed loans. The changes are expected to help rebuild reserves falling below congressionally mandated levels.

In research published on Friday, Citigroup said the changes should lead to slower Ginnie prepayments, especially for higher-premium coupons. "Over the long run, the rules are likely to further improve Ginnie Mae credit quality," Citi said. Matt Hastings, portfolio manager of the Schwab Premier Income fund, who is based in San Francisco, California, said prepayment risk is inherent in Ginnie Mae MBS, but they are trying to limit their exposure, although they cannot reduce it entirely. Hastings, also co-manager of the Schwab GNMA fund, said their strategy is to focus on "older," or "seasoned," bonds, for example, those backed by loans originated earlier this decade. "Seasoned securities have more voluntary and involuntary prepayment history for investors to analyze," he said.

Ginnie Mae and the FHA, units of the U.S. Department of Housing and Urban Development, have been pivotal players in the hard-hit U.S. housing market. The FHA extends credit to borrowers who in many cases could not afford large down payments or who wanted to refinance, but had little home equity. Ginnie Mae's market share, while a relatively small component of the roughly $5 trillion agency MBS market, has ballooned.

The Ginnie Mae MBS market surged to $640 billion at the end of 2009's first quarter from $450 billion at the end of 2007. During the same time, Fannie Mae increased to $2.855 trillion from $2.259 trillion, while Freddie Mac grew to $1.819 trillion from $1.727 trillion, according to Arthur Frank, director and head of MBS research at Deutsche Bank Securities in New York. "The demise of the securitization market at the end of 2007 is behind the growth since the only outlet for new securitization became Fannie Mae, Freddie Mac and Ginnie Mae," he said.

Ginnie Mae MBS prices have gained more than Fannie Mae MBS, mostly since investors have demanded higher credit quality and depository investors prefer an asset with a lower risk weighting toward regulatory capital, according to Kevin Cavin, a mortgage strategist at FTN Financial Capital Markets in Chicago. MBS from Ginnie Mae have a zero percent risk weighting, while Fannie Mae and Freddie Mac have a 20 percent risk weighting. "This has made banks big buyers," Cavin said.

Using the 30-year 5.00 percent MBS coupon -- the most liquid coupon -- as a proxy, Ginnie Mae has seen 24 basis points more spread tightening to Treasuries this year than Fannie Mae, he said.