"Mrs. Charles Benning sweeping steps of shack in Shantytown. Spencer, Iowa"

Ilargi: A double header today for your weekend reading. First the depressing spectacle in Europe, where Slovenia, Austria and Spain have -each in their own way- been added to the list of countries at risk of -further- downgrades, while France has received a temporary break, sort of a fleeting breather. Second, Ashvin introduces Nathan Carey from Ontario who writes about Hardwick, VT, and shines a light on the successful efforts at the economic revitalization of the community.

Ilargi: I'm convinced it’s not so much that it's hard to understand; instead, it's hard to accept. Still, for most people that's enough reason to not understand.

It might therefore be a good moment to reiterate what we've said often before at The Automatic Earth: the financial system as we know it can not be saved. It doesn't matter whether "official institutions" nominate 30 banks as being too big to fail, or 300. It is inevitable that the enormous amounts of debt accumulated in a relatively and amazingly short period of time must be serviced. Pay offs, write downs, defaults, bankruptcies. They're cast in stone. It's too late, too big to fail or not.

Just as it is too late for the Eurozone. Tons of "experts" clamor for Europe to move closer together, and form for instance a full fiscal, if not political union. But it's way too late for that. The interests at this point in time have simply become too divergent.

There now seem to be talks underway to form a strong Euro core group. Ironically, these talks are led by France. Ironic, because France is the only country that really stands to benefit from such a core group. That is, if it's allowed to be a member. Which is highly questionable.

French President Nicolas Sarkozy is witnessing the fall of Italian PM Berlusconi with sweaty palms. He has ample reason, says also Henry Samuel in the Telegraph:

'France will be the next to crumble', warns Gordon BrownFrance risks becoming the next victim of the sovereign-debt crisis "in the coming weeks", Gordon Brown, the former prime minister, has warned.

Mr Brown’s prediction came as the difference between French borrowing costs and those of Germany hit record levels. EU leaders urged France to draw up further austerity measures to meet its deficit reduction targets, amid fears the eurozone’s second biggest economy could crumble if Italy’s debt crisis spirals out of control.

Mr Brown, speaking in Moscow, said: "France is in danger of being picked off by the markets in the coming weeks and months." [..]

"Let’s not have any illusions," said Jacques Attali, a former adviser to president François Mitterrand and head of the European Bank of Reconstruction and Development. "On the markets French debt has already lost its triple-A status."

One Elysée Palace official told Le Monde newspaper: "If Nicolas Sarkozy loses our triple-A, he is dead."[..]

Ilargi: While I have no desire to address Gordon Brown's level of credibility here, if we assume that the last statement is indeed true, then Sarkozy's career is over. Because there is no way France will keep its AAA rating. The only way that would be possible is if Germany (and/or the US, China) would guarantee anything French that's not bolted down. Not going to happen.

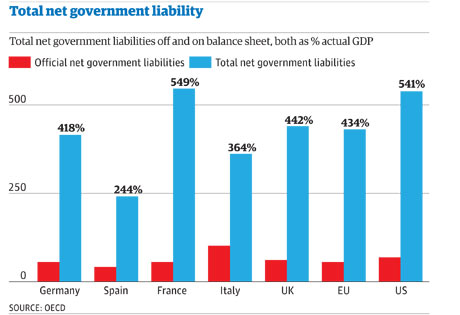

France's reality is clearly visible in this Société Générale graph, which I posted earlier this week:

Even if you would give Paris some benefit of the doubt, and assume that it can somehow handle the situation for an X amount of weeks/months/years longer, a country with liabilities running at 549% of GDP does not merit an AAA rating. No more than any CDO squared filled with toxic loans does. Which is why the US at 541% has already been downgraded.

This is a truth that every ratings agency will need to face up to at one point. Thursday's erroneous S&P report of a French downgrade could well be a gift from heaven for Sarkozy. After all, he gets the opportunity to angrily deny it all across the media, and plus he knows S&P will hesitate when it actually does want to downgrade the country. But it still must down the line.

France wants a core Euro group comprised of Germany, the Netherlands, Finland, Austria and itself. Not going to happen. If and/or when it came to a break-up, the other four would rather see France lead the "poor", mostly Latin group, for reasons the graph above spells out loud and clear. And that's a role France will not accept, ever.

Moreover, Austria also runs the risk of a downgrade, over its exposure to Italy and Eastern Europe. In other words, a rich core group would consist of Germany, the Netherlands and Finland. But the Netherlands has seen a major housing bubble that has yet to pop. Once it does, and it must, we'll be left with just Germany and Finland. And why would the Finns choose that over independence?

Every single scenario that has Europe either come closer together or break up in an orderly fashion is full of holes. What's left, then, is chaos. The rise to power of Papademos in Greece and Monti in Italy will not change this. What it will do is put a much harder squeeze on the people of the countries.

There should be mass protest against the developments in the streets of Athens and Rome, but people have not yet processed what is happening. When they do, it will in all likelihood be too late. Monti and Papademos are there to execute a short lived "transition" job, and to then vanish.

To sign a whole bunch of things into law which facilitate yet another round of bailouts and other support measures for their financial industries, and which will cause enormous hardship for the people (you ain't seen nothing yet). Afterwards, someone else can take over and claim it's not his/her fault.

We've come to a point where there is really only one major choice left to make. It's either to support the financial industry, which is irrevocably linked to both the financial and the political system, or to support the people. The fairy tale we've consistently been fed that they're one and the same, that saving the banks will save the people, should have been laughed away and wiped off the table long ago. But it’s 11-11-'11, and the fairy tale's still there. It's big fat lie that serves only to take hold of what scarce money you have left.

We find ourselves in a full blown credit crunch. Chris Whalen may call it a "slow motion" credit crunch, but that, however tempting the idea, is at best partly true. The reason why lies in the trillions in future taxpayer liabilities that governments have pushed into the banking sector. Without those trillions, hardly any lending would be taking place. And with the trillions, the whole house is still coming down anyway, no matter all the talk about a recovery.

It is slow motion only when you look at the stock markets, when you see the world through the eyes of an investor; in the streets of Athens or Detroit, for instance, there’s nothing slow motion about it. Not where the budget cuts and austerity measures are implemented that pay for bailing out banks silently drowning in as yet unrecognized but soon to be revealed losses.

Still, whether fast or slow, a giant credit crunch driven by debt deflation is irrevocably heading our way. Trying to stop it is entirely useless; using what scarce future wealth there will be to execute the futile attempt at doing so is extremely harmful. The world needs something better than finance industry henchmen like Papademos and Monti if we wish to minimize the upcoming suffering of the 99%.

Ashvin Pandurangi: As the financial and equity markets continue to gyrate back and forth with unprecedented volatility in response to the ongoing implosion of the European sovereign debt ponzi bubble, what better time to purge these daily doses of anxiety, confusion and frustration from our minds, and focus instead on what those of us who live in rural communities can start doing right now to revitalize those communities, their residents and surrounding areas.

Nathan Carey, the second winner of TAE Community’s "Diamonds in the Rough" project, has provided us with just that opportunity in the following article, which explores the ways in which small-scale agriculture can be reinvented in small towns or rural areas, bringing economic stability and vitality back to those communities. He shares his own personal experiences with this issue, and also gives us a specific example of where such an effort has been successfully undertaken so far, in the town of Hardwick, Vermont.

But first, in keeping with the growing tradition of the TAE Community’s "Diamonds" project, I would like to give a warm mention to the three Diamonds which did not win a majority of votes in the last poll, but which were all fascinating and deserving of further contemplation by our community. Here are those three ideas, in the order of the votes they received (highest to lowest), along with a few reference links to information and explanations for anyone who is interested in exploring them further.

1. The American Homestead Act of 2012, by Richard Elder [Basic Outline of the Idea]

2. Local Complimentary Currency Model, by Aki Järvinen [Detailed Overview of the Idea], [Video Presentations (in Finnish with English subtitles)]

3. State-Owned Grain and Flour Mills, by Tom Gibbs [Link to History of ND Mills]

And, now, on to today’s main course, which is a generous portion that has been prepared and served to us by Nathan Carey. Bon appetit!

Nathan Carey:

The Historical Trade-Off Between Efficiency and Resiliency

For several generations people have been tearing up their country roots and planting themselves in urban centers. It is one of the strongest and most ubiquitous migrations of this century across the world - the migration from rural areas to urban cities. In fact, "rural areas" have simply become the space between departure and arrival. They’re just exits off of the freeway that you have no reason to take. The reason for leaving is quite clear, though.

Starved of jobs and opportunities for socioeconomic "mobility", our rural towns are dying painfully slow deaths. This process is evident traveling through almost any small town two hours away from any urban center in North America. We see empty storefronts with yellowing "For Rent" signs, empty cracked streets with faded paint, empty crumbling grain silos and empty tilting barns. In the last few years, poverty has only gotten worse in America, and especially the rural portions that are largely ignored.

But, as our economy and the society it supports simplifies from the myriad of pressures bearing down on it, human populations will have to leave their energy and import hungry cities to once again fill the ‘empty’ spaces with life and labor. I believe there's a great way to revitalize and prepare these empty places now, while we still have the means to maneuver. Small-scale, resilient agriculture is a way to transform the rural landscape into the kind of place people want to visit and live in.

The starkness of these places became viscerally evident to me when I moved from my boyhood suburbs of Toronto to rural Ontario. My wife and I bought fifty acres of fertile soil that we fostered into a farm business. After many years of interning, living in trailers and seeking out farming know-how, we felt we were finally up for the challenge of running our own farm business and got started.

Our vision of agriculture is small and diversified. We run a winter vegetable CSA where our members pay us in advance for vegetables that we dole out throughout the long Ontario winter. We also raise and sell various kinds of meat: lamb, pork, chicken, turkey and soon, beef. Neither of us come from farm backgrounds and we represent many in the ‘new farmer’ movement – young, educated, practical and willing to put the hard work in to transform the ideas floating around in our brains into reality.

The kind of farming we are practicing is based on resiliency. It is in direct contrast to industrial farming whose underlying strategy is efficiency. We don't plant one type of crop; we plant thirty. We don't have one income stream; we have several – including teaching and telecommuting employment from Toronto. We don't have one customer; as many wholesale producers do, we have hundreds.

But while we are resilient we also suffer some lack of efficiency. Our larger, more conventional neighbors can take an acre and turn it from sod to seed bed in less than an hour. It would take us a full ten hour day to do the same with our small walk-behind tractor. I think it's helpful to see these two strategies, resiliency and efficiency, as opposing points on a continuum of system building. To be too far towards one or the other is detrimental to the system's health.

Too efficient and you "find the straightest road to hell" (a quote from James H. Kunstler via Nicole Foss). If you are mired in resiliency, then you'll never really get anything accomplished. Resiliency is supple and adaptive. Efficiency is hard and effective. Too supple and you have no form. Too hard, though, and you become brittle and break. Our modern economy which has made a god of efficiency is ultra-efficient and ultra-brittle.

Small-scale agriculture is attempting to move back to the middle but hedging much closer to resiliency than efficiency – a hedge based on our uncertain future. What does resiliency look like? On our farm we have five different types of animals that all produce manure. This assures we are not dependent on outside sources for the garden’s fertility needs. We have been careful to scale our operation to be largely manageable by hand or with small tools.

This precaution assures that, while we can and do use diesel driven implements to help us, we are not completely reliant on them. Your average CSA market garden is going to have fifty different crops usually with a few varieties of each: 3 varieties of carrot, 5 squash, 8 tomato varieties, etc. This variety means that a single disease doesn’t wipe out a whole season’s worth of work. It may only wipe out one row. There must be a balance with efficiency though.

If local food systems are to feed whole regions, then they must also be of a scale to accomplish that. This balance is going to take many years and many kinds of farming to discover. The rural landscape is far ahead of the global economic turmoil we see crashing in slow-motion around us. It found it's 'bottom' and has been living there a long time. Most people living in small towns didn't go into debt to flip a 'fixer upper' on the housing market.

Maybe that’s because there was no housing market where they were, and there still isn't. Or maybe they can't get credit because of their low wage or lack of employment. The story of most rural towns is the same: its bottom arrived at the end of a short, straight road paved by a single, large employer. Maybe it was a textile-mill, a mining outfit, a car manufacturer, a power-station.

This large employer came, created jobs, created industry, created a community around them and then, just when life was being taken for granted, it all fell apart. Maybe a large company bought the local company out and moved it off-shore. Maybe the resources being extracted were no longer worth extracting. Maybe government regulation drove costs beyond the breaking point.

The Basic Drivers Underlying Small-Scale Agriculture

Whatever the specific details, most rural areas seem to have charted a familiar story all over the continent. I think it can be said that formerly resilient rural economies swung hard towards efficiency and then broke at an unexpected shock. Really, it's the story of the twentieth century writ small on town after town. So why should small-scale agriculture become the hero of this developing story about a North American Continent centered on local communities? That’s a big question to answer, but we can start with a few of the following reasons.

1. Filling a Non-Negotiable Gap - We must anticipate the demise of industrial food production as the complexity of society breaks down and liquid fuel prices rise becomes less affordable. Therefore, we need to work on an alternative, regardless of the specific scale of the crisis. Once complex, fragile chains of food production and distribution spanning the world begin to break, it will be our duty to make sure that our families and communities can still eat!

2. Human Scale - Small-scale agriculture is capable of being implemented by normal people in normal circumstances, without extraordinary infrastructure, technologies or budgets. It is a grass-roots revolution powered by the people for the people. While many people may hope for technology to save them, they would might do better to unclasp their wringing hands and put them to work turning compost.

3. Provides Meaningful Employment - Small-scale agriculture generally requires a lot of different types of human labor. Once the use of energy-hungry machines becomes too expensive unavailable for farming, people will also have to step back in to complete the necessary tasks themselves. And, yes, some of it is "back-breaking" and some of it is repetitive, but much of it is also joyful, soulful, and fun. All of the work is skillful and rewarding.

4. Crucible for Innovation - While the latest app for telling a person his/her horoscope is added to the latest iProduct, we are reinventing the process of growing food. Small-scale farmers must not only re-discover lost knowledge but adapt it to current circumstances. This includes a variety of innovative practices, such as creating new hand-tools, bicycle powered root washers, specialized tractor equipment, online customer checkout systems specifically designed for CSA farms, new seed varieties, new rotations, and efficient, natural ways of fighting plant diseases and weeds.

5. Uplifting and Empowering - Many people feel dis-empowered by a global financial system that has left their expectations in tatters. Learning and practicing the skills that provide for your basic needs brings pride and security.

6. No Externalizations - Unlike the industries of the past that sprouted up, inflated to unsustainable proportions and then crashed, devastating the towns built around them, small-scale agriculture is diffuse and resilient. It simply relies on the soil, the weather and the sun, and it is not nearly as affected by the vagaries of distant markets.

I'm sure there's easily another solid twelve reasons why small-scale agriculture is such a positive force for change. How to revitalize a rural economy through small-scale agriculture is a much harder question to answer. Asking for the revitalization of rural economies through the use of small-scale agriculture is nothing short of a call for a revolution in our food production and distribution systems.

The Precedent Has Been Set in Hardwick, VT

The best way to conceive of this revolution is by illustrating a place where the challenge of rebuilding our food systems from the soil up has begun in earnest - Hardwick, Vermont (pop. 3000). The town had its best days in the 1920s, as it was a primary source for granite. When Granite was replaced by concrete as a building material, the industry collapsed. Therefore, the town has been in a sort of stasis for generations.

According to the US Census Report in 2000, the per capita income for the town was $14,813 per year, and about 10.5% of families and 14.0% of the population were living below the poverty line. The town's current unemployment is 40 higher than the state average in Vermont and its average median income is 25% lower. Like most American towns, the supermarket is peoples’ main connection to the industrial food system.

However, there's a growing and well publicized movement happening in Vermont that could provide some clues to the rest of us on how to proceed in a systemic process of revitalizing rural economies. There are many small and medium sized agricultural businesses in Hardwick that popped up within a short time frame and have been growing and making their positive influence felt.

The New York Times wrote an article featuring this movement back in 2008, and, despite the worsening financial meltdown that is tearing many communities apart, it still remains a viable and thriving model for Hardwick.

Uniting Around Food to Save an Ailing Town"This town’s granite companies shut down years ago and even the rowdy bars and porno theater that once inspired the nickname "Little Chicago" have gone.

Facing a Main Street dotted with vacant stores, residents of this hardscrabble community of 3,000 are reaching into its past to secure its future, betting on farming to make Hardwick the town that was saved by food.

With the fervor of Internet pioneers, young artisans and agricultural entrepreneurs are expanding aggressively, reaching out to investors and working together to create a collective strength never before seen in this seedbed of Yankee individualism. [..]

Rian Fried, an owner of Clean Yield Asset Management in nearby Greensboro, which has invested with local agricultural entrepreneurs, said he’s never seen such cooperative effort.

"Across the country a lot of people are doing it individually but it’s rare when you see the kind of collective they are pursuing," said Mr. Fried, whose firm considers social and environmental issues when investing." The bottom line is they are providing jobs and making it possible for others to have their own business."

These businesses include names like "High-Mowing Seeds", "Clair's Restaurant", "The Vermont Soy Company", "Jasper Hill Farm", "Pete's Greens" and "Highfield's Center for Composting". All of these companies and more describe the beginnings of how we take back our food systems and our rural economies in the process. They all carry important lessons for us to take notice of and adopt in our rural communities throughout the upcoming years of both industrial collapse and alternative agricultural opportunities.

High-Mowing Seeds

Tom Stearns, Vermont local, is the owner and entrepreneur behind one of the few commercial organic seed producers in the country and one of the even fewer focusing on heritage or heirloom varieties. Heirloom varieties tend to pre-date the industrialization of our food supply. They are selected for flavor and nutrition, and adapted to local conditions instead of being selected to fit into a neat, efficient process. Mr. Stearns epitomizes the transition that is occurring in Hardwick, and its emphasis on cooperation and sharing.

NY Times (article linked above):"All of us have realized that by working together we will be more successful as businesses," said Tom Stearns, owner of High Mowing Organic Seeds. "At the same time we will advance our mission to help rebuild the food system, conserve farmland and make it economically viable to farm in a sustainable way."

Cooperation takes many forms. Vermont Soy stores and cleans its beans at High Mowing, which also lends tractors to High Fields, a local composting company. Byproducts of High Mowing’s operation — pumpkins and squash that have been smashed to extract seeds — are now being purchased by Pete’s Greens and turned into soup. Along with 40,000 pounds of squash and pumpkin, Pete’s bought 2,000 pounds of High Mowing’s cucumbers this year and turned them into pickles."

High-Mowing started out as a hobby for Stearns, who had a lifelong love of seeds, but soon it became a business. It's a $2 million/year concern that employs 30 people at reasonable wages. Besides providing employment, the business of growing seeds really gets to the heart of what it means to be resilient. Seeds and soil are obviously the basic foundations of agriculture and cannot be taken for granted, as most Americans tend to do.

The seed supply has become as inefficient and brittle as our money system and we risk more than we know by concentrating the breeding, growing and distribution of seed into the hands of a few. With men like Stearns at the forefront, who is more than willing to cooperate with other businesses in the community, the movement is in excellent hands. We enthusiastically buy our own seed from High-Mowing for some of our gardens.

Claire's Restaurant (Community Supported Restaurant)

CSRs are an adaptation of my farm's business model - Community Supported Agriculture. A group of five people started the restaurant and the funding model is as unique as the dishes you will find there. A holding company was created who bought the lease for the restaurant's building twelve years in advance. It turns out that pre-paying your lease for twelve years is a great way to negotiate a sweetheart rate!

NY Times:"Mr. Tasch is having a meeting in nearby Grafton next month with investors, entrepreneurs, nonprofit groups, philanthropists and officials to discuss investing in Vermont agriculture. Here in Hardwick, Claire’s restaurant, sort of a clubhouse for farmers, began with investments from its neighbors. It is a Community Supported Restaurant. Fifty investors who put in $1,000 each will have the money repaid through discounted meals at the restaurant over four years.

"Local ingredients, open to the world," is the motto on restaurant’s floor-to-ceiling windows. "There’s Charlie who made the bread tonight," Kristina Michelsen, one of four partners, said in a running commentary one night, identifying farmers and producers at various tables. "That’s Pete from Pete’s Greens. You’re eating his tomatoes."

The equipment that is needed to run a restaurant, and typically put a heavy burden on start-up capital, was purchased by the same holding company for use by the restaurant and any future food business that would take the place of Claire's Restaurant, should it fail. In this atmosphere of financial and social support, the chef, Steven Obranovich, is able to focus on cooking and, perhaps more importantly, the sourcing of ingredients.

That focus has led him to source an unheard of 80% of these ingredients from local farmers and businesses (it’s not just the garnish that is local). Here is both an outlet for the food being produced locally but also a place where people can meet, talk and spend time becoming ensconced in the spirit and vitality of eating food grown close to their homes.

Highfield's Center for Composting

This company provides a necessary service for any agrarian community. Good quality compost is in short supply and for many reason most new farmers take on market gardening as their initial venture into the world of agriculture. Without on farm fertility gardeners need a good non-chemical source of nutrients for their gardens. Thomas Gilbert, executive director and founder, is a composting guru and has a deep respect for what compost and fertility can mean to an agricultural community.

These are just three of the business’s that make up the incredible, unfolding story in Hardwick. Each enterprise is exciting on it's own but having so many agricultural business's so close together both in proximity and mission has the makings of big time change. As the NY Times article makes clear, the unprecedented level of cooperation between these businesses provides an atmosphere of economic stability and social cohesion.

NY Times:"For the past two years, many of these farmers and businessmen have met informally once a month to share experiences for business planning and marketing or pass on information about, say, a graphic designer who did good work on promotional materials or government officials who’ve been particularly helpful. They promote one another’s products at trade fairs and buy equipment at auctions that they know their colleagues need.

More important, they share capital. They’ve lent each other about $300,000 in short-term loans. When investors visited Mr. Stearns over the summer, he took them on a tour of his neighbors’ farms and businesses."

Center for an Agricultural Economy

The recently started Center for an Agricultural Economy is another organization in our community that will give shape and push this vision forward in a more organized and transparent way. Since the NYT article was written, this organization has remained strong and committed to Hardwick’s revitalization through small-scale agriculture, and the town’s residents, from farmers to business people to students, have benefited greatly as a result.

NY Times:"To expand these enterprises further, the Center for an Agricultural Economy recently bought a 15-acre property to start a center for agricultural education. There will also be a year-round farmers’ market (from what began about 20 years ago as one farmer selling from the trunk of his car on Main Street) and a community garden, which started with one plot and now has 22, with a greenhouse and a paid gardening specialist.

Last month the center signed an agreement with the University of Vermont for faculty and students to work with farmers and food producers on marketing, research, even transportation problems. Already, Mr. Meyer has licensed a university patent to make his Vermont Natural Coatings, an environmentally friendly wood finish, from whey, a byproduct of cheesemaking."

Hardwick's access to local food is unparalleled. It is likely that Hardwick could feed itself and the surrounding environs without any outside input. And while that may seem like a small thing, as all of us have become so used to the ubiquity of food, it bears remembering how incredible brittle our long food supply chains are. Most cities have about four days worth of food on hand at a time without constant delivery. A food system based on resilient parts - i.e. people and businesses - will itself be resilient as a whole.

Some Thoughts For You to Take Home

Agriculture is, of course, a primary industry, since it takes seed and soil and produces something of intrinsic value – food. This food, in turn, can result in a thousand secondary off-shoot industries. Think about a canning factory, a distillery, a community delivery service, or a candle manufacturer from Bee's wax? The possibilities boggle the mind, and every community will be different based on the needs and desires of its residents.

Small farms trade back the destructive relationship between fossil fuels and efficiency for the creative relationship between human labor and resiliency. Farms need year-round labor, and if you’re not riding the wave of a commodity grain, that means job stability. Stability means a stable local economy, but also stable families and households. There are as many opportunities in or around small-scale agriculture as you and your neighbors have energy for.

What does all of the above mean for you right this moment? Well, it certainly adds a lot of weight to the phrase, "buy local". The idea of buying local has allegedly been accepted and embraced by mainstream commentators, but they use it as little more than a catchy slogan. Instead, it should be understood as something radical and revolutionary! Resilient food producers out there are challenging the food system on all fronts.

So you’re not just reducing your carbon footprint and enjoying the tastiest, most nutritionally dense food, but you’re also -and perhaps most important of all- ensuring the long-term viability of your own community. If you're an investor, then why not put your money into a small-agricultural business or related industry? One of the largest barriers for new farm businesses is start-up capital. Banking institutions generally don’t understand the benefits of this kind of resilient endeavor, because they see no immediate profits to be gained.

The bottom line may look decent, but the return on investment (ROI) is very long-term and the interest might come in the form of hams, lettuce mix and soup stock instead of cash. But if you’re a frequent reader of The Automatic Earth, then you probably understand why nutritional food is a much better ROI. Instead of looking for a quick monetary profit, we can be satisfied settling for delicious food security.

It is obviously important to learn the proper skills and gain experience. There are certainly a lot of folks out there trying to farm without the proper business sense or agricultural knowledge to succeed. With access to online or community resources, though, it is never too late for people to get started on their rural revitalization education. The cities of our nations are where we have focused our attention, but I believe it's in the "empty spaces" where the room for creativity and reinvention of a more equitable and prosperous society will find its roots.

Innovation at the "human scale" is happening at the end of hoes and around micro-brews in a small town watering hole. Food is a basic need, it is non-negotiable and come rain, shine, deflation or inflation, we must eat! As the uncertain future looms large over all our lives, we need to be prepared both to survive and to thrive. For now, it is clear that people in some rural economies are feeling hopeful about agriculture for the first time in a generation.

The fault lines are shifting, as the fastest growing segment among farmers is young women! What better statistic to reflect change from the "traditional farmer" in our culture’s iconography, and the agricultural landscape in general. "Eating is an agricultural act," Wendel Berry famously said, and we are all engaged in this agricultural act every single day. Whether those acts benefit a few multi-national corporate networks or our next door neighbors is entirely in our hands.

To end this discussion, then, I will turn to the extremely informative and insightful book, The Town That Food Saved, written about Hardwick by Ben Hewitt.

The Atlantic Magazine interviewed Mr. Hewitt about the book last year, and he made clear that none of the things happening in Hardwick came without great patience and effort from the people and businesses of the community.

It is not easy to revitalize our rural economies after decades and decades of mis-allocation and mismanagement of resources. Still, with enough effort and imagination, Hardwick proves that this revitalization can be done.

In Rural Vermont, From Famine to Fork"In the course of researching The Town That Food Saved, Hewitt found that the issue of food systems was far more complex than he had first thought. "I wanted to ask what it really means to create a localized food system," he told me over coffee, one of the few items on his daily menu he does not produce. "It's hard—culturally, economically, and in terms of people's habits. Readers looking for empirical answers should look elsewhere. In a way, this book is more about questions than answers."

Still, Hewitt comes away feeling that Hardwick's recent history may be providing a template for a food system that could save all of us. "The fact is that our nation's food supply has never been more vulnerable. And we, as consumers of food, share that vulnerability, having slowly, inexorably relinquished control over the very thing that's critical to our survival," Hewitt writes. What is at risk, he contends, is the entire model of the way we nourish ourselves. Fixing this broken model is a matter of national urgency.

Should our industrial food system collapse, the Hewitt family (which includes his wife and two young boys) will have far less to worry about than most of us. They raise 80 percent of the food they eat: in addition to all their vegetables, they produce milk, beef, lamb, pork, chicken, eggs, blueberries, raspberries, apples, and maple syrup. Their house, which they built with help from friends, gets its electricity from solar panels and its heat from wood stoves.

Where does that leave the rest of us? "For 100 years food production has been headed in one direction," Hewitt told me. "The people I profile [in Hardwick] are all articulating steps to get us going in a different direction."

Markets rise but contagion fears spread to Spain

by Jonathan Sibun, and Harry Wilson - Telegraph

Political progress in Italy and Greece pushed stock markets higher but economists warned of stormy weeks ahead as attention turned to Spain amid fears it could be the next economy to come under the spotlight.

The FTSE 100 rose 100.57 – or 1.9pc – to 5545.38, closing a turbulent week 1.3pc higher. In Italy the FTSE MIB was up 3.7pc on the day, while France's CAC rose 2.8pc, the German Dax gained 3.2pc and in the US the Dow Jones closed 2.2pc higher. The rally came as bond yields fell with Italian 10-year debt touching 6.4pc on signs that politicians are finally recognising the scale of the crisis.

In Italy, hopes are growing that a new government could be installed as early as tomorrow after the Senate approved an economic reform bill, paving the way for Silvio Berlusconi's resignation. The austerity package, seen as crucial to averting an Italian bail-out, will go before the country's lower house today before an emergency government is installed. Mario Monti remains the frontrunner to succeed Mr Berlusconi.

"The most important element to overcome this crisis is a trusted and able new Italian government that can really fulfill the structural changes that are needed," said Ewald Nowotny, a member of the governing council at the European Central Bank (ECB).

Markets also took cheer as Lucas Papademos was sworn into office in Greece after days of political wrangling. Inspectors from the International Monetary Fund (IMF), European Union (EU) and ECB are set to visit Athens next week, potentially leading to the release of €8bn (£6.9bn) in bail-out funds.

Ioannis Mourmouras, a new assistant finance minister, said the new government's sole task was to implement the necessary austerity reforms: "Greece is at a crossroads. What is at stake is the future of the country within the eurozone."

While traders took comfort from progress in Italy and Greece, fears were growing over the health of the Spanish economy after GDP data showed the country grinding to a halt in the third quarter. Economists are increasingly sceptical that the eurozone's fourth largest economy will be able to meet deficit reduction targets.

"The economic recovery in Spain has ground to a complete halt," said analysts at ING. "We fear that the Spanish economy might slip into recession soon – perhaps as soon as the current fourth quarter. Our base case scenario envisages no economic growth in 2012."

Spain's deficit plans are predicated on the economy growing 1.3pc this year and by 2.3pc in 2012, targets seen as increasingly optimistic. With the country set to hold elections on November 20, a new government would likely have to push through further austerity measures, potentially leading to political infighting or popular opposition. Spain's bond yields have moved higher in recent days, ending yesterday at 5.9pc.

Fears have also been raised over the country's banking system with analysts pointing to an alarming outflow in retail deposits this year. About half the 2012 funding requirements of Spanish banks are planned to be met through deposits. Analysts at Barclays Capital argue this means the country's banks will need to see 4% growth in deposits, but so far in 2011 there has been 2% shrinkage.

Weighing on the banks further is the prospect of property write-downs. French broker Cheuvreux estimates that 50% of Spanish construction companies have either already defaulted on their loans or are likely to do so. Speculation is growing that much of the land held on the books of Spanish banks will have to be marked down significantly before year-end.

Fears over Spain's future came as the IMF issued a report – prepared for last week's G20 summit but only released yesterday – warning that advanced economies could fall back into recession unless world leaders moved with greater urgency to boost growth. The organisation raised particular concerns over how fiscal stability would be achieved in countries including the US and Japan.

Invisible Run on Banks Becoming Conversation With Italian Yields Above 7%

by John Glover and Elisa Martinuzzi - Bloomberg

Italy’s highest bond yields since the birth of the euro are reverberating through the financial system of Europe’s biggest debt issuer, driving lenders to seek record amounts of central bank financing.

Italian banks borrowed 111.3 billion euros ($152 billion) from the European Central Bank at the end of October, up from 104.7 billion euros in September and 41.3 billion euros in June, Bank of Italy data show. The five biggest lenders -- UniCredit SpA, Intesa Sanpaolo, Banca Monte dei Paschi di Siena SpA, Banco Popolare SC and UBI Banca ScpA -- accounted for 61 percent of the country’s use of ECB resources in September, almost double the share in January.

After punishing Greece, Ireland and Portugal for their rising debt loads, the bond market is now targeting Italy, pushing bonds yields in the euro zone’s third-largest economy above 7 percent as the nation’s lenders prepare to refinance $120 billion of debt maturing next year. Italy’s $2 trillion in liabilities exceed those three countries combined, plus Spain.

"The banks are deleveraging on a tightrope," Alberto Gallo, a credit strategist at Royal Bank of Scotland Group Plc (RBS) in London, said in an interview. The slump in Italy’s bonds, which sent the 10-year yield soaring to as high as 7.48 percent Nov. 9, is reducing the value of fixed-income securities held by banks, eroding their value as collateral for loans, Gallo said.

Bill Rates

Bond investors charged the nation an interest rate of 6.087 percent yesterday to buy 5 billion euros of one-year bills, the highest in 14 years. Greece, Ireland and Portugal sought a bailout from the ECB, the European Union and the International Monetary Fund after their bond yields rose above 7 percent amid the region’s sovereign debt crisis.

As Italy’s government faces collapse after Prime Minister Silvio Berlusconi promised to resign once Parliament approves austerity measures, deputy finance ministers meeting at the Asia-Pacific Economic Cooperation forum in Hawaii this week expressed concern over the danger Europe poses to the world economy.

U.S. Treasury Undersecretary for International Affairs Lael Brainard said European officials must speed up construction of a "firewall" to protect countries that have sound policies. The 17-nation euro has fallen as much as 5.4 percent since Oct. 27.

International Monetary Fund fiscal monitors are due to visit the Italian capital, and European Union Economic and Monetary Affairs Commissioner Olli Rehn says he wants answers to "very specific questions" on economic pledges by the weekend. U.K. Prime Minister David Cameron said Italian interest rates are "getting to a totally unsustainable level."

Yield Spreads

The extra yield investors demand to hold Italian 10-year debt rather than German bunds rose to a euro-era record 5.53 percentage points on Nov. 9 before falling back to 5.12 percentage points.

Italy’s top 32 banking firms have about 88 billion euros, or 3.2 percent of their liabilities, maturing in 2012, according to the Bank of Italy. Next year’s maturities coincide with about 307 billion euros of the government’s debt coming due, the most ever, according to data compiled by Bloomberg.

Italian lenders are seeking to broaden their sources of funding. Corrado Passera, the chief executive officer of Intesa Sanpaolo SpA (ISP), said on Nov. 8 the bank can do without wholesale funding for all of next year, and rely on deposits and bonds it sells to individual customers.

Rising Cost

Retail funding made up 54.1 percent of the Italian banking system’s total as of June, compared with 48.8 percent in the rest of the euro zone, according to the Bank of Italy. The cost of that money increased 0.4 percentage point, or 40 basis points, to 1.7 percent in the nine months ended Sept. 30 as the funding mix shifted to products such as repurchase agreements and fixed-term deposits that pay clients more, central bank data show.

Italian banks’ share of ECB lending rose to about 19 percent of the total in October, according to the Bank of Italy. That’s up from 15 percent, or 91 billion euros, in September, the data show.

"The Italian banks are trapped," said Roger Doig, a London-based analyst at Schroders Plc, which manages about $58 billion in fixed-income assets. "They are where they are and that’s with the Italian sovereign. The austerity required if the sovereign wants to remain in the euro zone means there’s going to be a recession, which will mean losses for the banks."

Default Swaps

Credit-default swaps tied to the senior debt of UniCredit, a proxy for the cost of funding at Italy’s biggest lender, jumped 150 basis points this month to 502 basis points, approaching the record 504 reached in September. Contracts on Intesa Sanpaolo, the second-largest, jumped 129 to 467, also close to an all-time high, according to CMA in London. Five-year contracts on Italy were little changed at a record 570 basis points, up from 239 at the beginning of the year, according to CMA.

Credit-default swaps typically decrease as investor confidence improves and rise as it deteriorates. They pay the buyer face value if a borrower fails to meet its obligations, less the value of the defaulted debt. A basis point equals $1,000 annually on a contract protecting $10 million of debt. "The market is pricing in an Italy event and assuming that Italy fails," said Patrick Lemmens, a senior money manager who helps oversee about $13 billion, including Intesa Sanpaolo shares, at Robeco Groep in Rotterdam.

Deposit Growth

Household deposits in Italy still are expanding "at a moderate pace," according to the Bank of Italy. That’s a contrast to withdrawals seen in Greece, Ireland and Portugal.

The annual rate of decline in Irish private-sector deposits was 10.5 percent at the end of September, according to that nation’s central bank. In Greece, deposits fell 2.9 percent in September for a net outflow of 6.29 billion euros, the biggest one-month drop since the start of the crisis, according to Manos Giakoumis, research director at Euroxx Securities SA, an Athens- based brokerage.

Italy’s lenders started increasing their reliance on the ECB in July, when end-of-month borrowings from the central bank minus the amount deposited reached 58.8 billion euros, according to John Raymond, an analyst at CreditSights Inc. in London. Before that, net borrowings from the ECB ranged from 9 billion euros to 30 billion euros, he said.

The amount surged to a record 87 billion euros at the end of October, according to Raymond, citing Bank of Italy figures. "This is all symptomatic of what’s going on around the banks," Raymond said. "Everything hinges on the sovereign."

Contracting Economy

RBS economists forecast a recession in Italy in the fourth quarter, and expect the economy to contract 0.2 percent in 2012. The government’s austerity packages, totaling 124 billion euros and including cuts to health care, pensions and regional subsidies, are adding to the recession risk, said RBS’s Gallo.

Italian institutions can borrow what they need in the ECB’s refinancing operations, paying the current policy rate of 1.25 percent as long as they have the required collateral. Lenders have "ample availability" of ECB-eligible assets, according to the Frankfurt-based central bank, and can help themselves by ensuring the assets are suitable as security. Intesa Sanpaolo said it’s looking to increase ECB-eligible assets to 100 billion euros from the current 83 billion euros.

The ability to fund at the ECB is vital for Italy’s banks that can’t access markets, though the central bank is keen to wean borrowers from its support. The ECB applies a discount on securities used as collateral to protect itself against loss. "Italian banks have been crushed in the carnage in the government bond market," said Suki Mann, a strategist at Societe Generale SA in London. "It could get worse."

Europe’s Banks Turned to Safe Bonds and Found Illusion

by Liz Alderman and Susanne Craig - New York Times

As the bets that European banks made on United States mortgage investments went bust a few years ago, bankers piled into what they saw as a safe refuge: bonds issued by countries in Europe’s seemingly ironclad monetary union.

Now, the political and financial crisis engulfing the Continent has turned much of that European sovereign debt into the latest distressed asset, sending tremors through global financial markets not seen since the demise of the investment bank Lehman Brothers more than three years ago.

This week, shortly after European leaders formally conceded that Greece could not pay its debts and forced banks to accept losses, the shock waves reached Italy, the third-largest economy in the euro zone after France and Germany. And despite frantic efforts by politicians to contain the damage, market analysts said that France, one of the strongest countries in the euro zone, may soon feel the impact.

"When people started buying more European sovereign debt, there was not a cloud in the sky," said Yannis Stournaras, director of the Foundation for Economic and Industrial Research, based in Athens. Now, he said, "This crisis is going to last because the perceptions of risk have changed dramatically."

European banks face tens and possibly hundreds of billions of dollars in losses on loans to nations that use the euro. Worried about even greater losses if the crisis worsens, the banks have been scrambling to reduce their holdings of an investment that, like triple-A-rated subprime mortgage bonds, was once thought to be bulletproof.

The French bank Société Générale, for instance, this week marked down 333 million euros of its Greek sovereign debt holdings and in October slashed its exposure to that country to 575 million euros, from 2.4 billion euros at the beginning of 2011. Another French bank, BNP Paribas, has cut its holdings of Italian government debt 40 percent since July, to 12.2 billion euros.

How European sovereign debt became the new subprime is a story with many culprits, including governments that borrowed beyond their means, regulators who permitted banks to treat the bonds as risk-free and investors who for too long did not make much of a distinction between the bonds of troubled economies like Greece and Italy and those issued by the rock-solid Germany.

Banks had further incentive to overlook the perils of individual euro zone countries because of the fees they earned for underwriting sovereign debt sold to other investors. Since 2005, several dozen banks in Europe and the United States have earned $1.1 billion in fees from selling bonds for European governments, according to Thomson Reuters and Freeman Consulting Services.

Like other investors, banks clung for a long time to the seemingly inviolable belief that all the countries using the euro would make good on their debts. For years, Greek and Italian bonds did not pay much more than German ones, but banks were always hungry to chase even a fraction of additional profit. For much of the last decade, they bought the higher-yield bonds, ignoring the growing political and fiscal problems of those countries as well as other peripheral euro zone nations like Ireland, Spain and Portugal.

Regulators bear much of the responsibility. Before 1999, when Europe forged its monetary union, regulators permitted banks to treat as risk-free the debt of any country that belonged to the Organization for Economic Cooperation and Development, a club of developed nations that includes the United States and most of Europe.

"There was encouragement from European authorities for banks to load up on more debt, because it was seen as safe," said Nicolas Véron, a senior fellow at Bruegel, a research firm in Brussels. "In hindsight, it was unwise risk management."

Some regulators realized that allowing banks to set aside no capital for sovereign defaults could be a problem and moved to address it in a 2006 accord known as Basel 2. They mandated that big, complex banks use their own models to determine if individual countries were at risk and hold some capital against them. But the European Union never enforced the stiffer regime. And amid the subprime mortgage crisis, Europe’s regulators added to the problem by demanding that banks hold more safe assets, much of it sovereign debt.

As a result, banks were not discouraged from placing their most liquid assets "into the worst possible government debt," Achim Kassow, a former Commerzbank board member, wrote in a study published by the European Parliament.

Now, Société Générale, Commerzbank and other banks cannot get rid of the shaky debt fast enough. In the last several months, they have booked billions of euros in losses from unloading it, although their exposure remains substantial. Including the effect of hedges, European banks had a net exposure of about $120 billion to Greek government borrowings and private debt at the end of June, according to the Bank for International Settlements. Even more worrisome, analysts say, is the banks’ exposure of $643 billion to Spain and $837 billion to Italy.

Banks in the United States are also caught in the crossfire. For Italy alone, they had $47 billion in net exposure to government borrowings and private debt at the end of June, the B.I.S. data show. Goldman Sachs has $700 million in exposure to Italy, according to a regulatory filing released this week, and could feel the fallout if the bonds were marked down.

The loss from a write-down similar to that on the Greek debt — 50 cents on the dollar — would erase 10 percent of the $3.43 billion in profit Goldman earned in the first nine months of the year.

Regulators are requiring European banks to raise 106 billion euros in new capital by next summer to protect themselves against further losses. Banks insist the risks are manageable. But the big fear is that they do not have enough capital to cover potential losses from the euro zone. That kind of crisis of confidence drove MF Global, the large New York brokerage firm, into bankruptcy last week after its $6.3 billion bet on European debt alarmed investors.

While the markets are now being brutally efficient in telegraphing the differing debt risks among European countries, they failed in that function for a long time, just as they failed to reflect the risks of subprime mortgage loans as a real estate bubble formed in the United States.

For most of the last decade, bond yields among Germany, Greece, Portugal, Ireland, Italy and Spain traveled in a tight pack. That meant investors buying and selling those bonds acted as if the countries were almost equally safe simply because they were members of the euro zone, despite shaky finances in Greece, real estate bubbles in Ireland and Spain and high debt in Italy.

The phenomenon rang alarm bells as far back as 2005, when banks, national treasuries and the European Commission held intense internal debates on why the spreads between Germany and other countries did not seem to reflect the differing risks, said a senior Brussels official involved with bank regulation. When the subprime crisis started to buffet Wall Street in 2007, banks sought shelter by turning even more to European sovereign debt, especially countries with the best returns.

The B.I.S. data show that bank lending to the governments of Portugal, Ireland, Italy, Greece and Spain, largely through bond purchases, rose faster than usual, by 24.2 percent, to $827 billion, between the second quarter of 2007 and the third quarter of 2009, when the crisis in Greece first started to taint European sovereign debt.

Banks across the world joined in this lending binge as they chased higher yields. Emblematic of those that took the plunge was Komercni Bank, a large bank in the Czech Republic that is majority-owned by Société Générale.

As the subprime crisis in America began mounting, Komercni veered into the seemingly safe Greek government bonds. The bank’s entire board, more than half of whom were long-time veterans of Société Générale, signed off on Greek debt purchases from 2006 through 2008. Now the bank is expected to write down an additional 2 billion koruna, or $111 million, on its Greek debt this year, after taking a 1.66 billion koruna hit in the second quarter. That is a manageable amount, but the bank would have been barely affected if it had bought the safer German bonds.

As the subprime crisis peaked on Wall Street, banks sharply increased their underwriting of European sovereign debt. In 2007, the world’s big banks made $113.9 million in underwriting fees; by 2009, that number had more than doubled to $273 million.

Société Générale went from issuing no Greek debt in 2005 to being the world’s eighth-largest underwriter just a year later. The bank has made $61.5 million in fees from underwriting debt for euro zone countries since 2005, according to Thomson Reuters. Deutsche Bank, the top underwriter of euro zone debt in that period, took in $87 million in fees.

Banks in the United States also profited. Since 2005, Goldman Sachs has earned $44.5 million in fees underwriting euro zone debt, and Morgan Stanley has earned $47.4 million, according to Thomson Reuters. Their special relationship with governments sometimes also presented a unique dilemma: it gave banks little incentive to publicize red flags even if they were suspicious about sovereign debt.

In 2005, Marc Flandreau was a senior adviser in Paris at Lehman Brothers, one of several banks selling sovereign bonds for the French government. He suddenly wondered whether France’s finances were solid enough to merit the low interest rates at which it and the other members of the euro zone were selling their bonds. He wrote a memo to the French Treasury expressing his concerns.

"They went totally ballistic," Mr. Flandreau recalled. "They said, ‘You guys should shut up, you’re selling our stuff.’ "

Benoît Coeuré, an official at France’s debt-issuing agency at the time, insisted that the policy was not to discourage the banks from analysis. But "if it had a negative tone on French policies," he said bluntly, "my role was to object to it."

Today, with Europe’s sovereign debt crisis seemingly spinning out of control, regulators are pressing governments and banks to divulge as much risk as they can and are asking banks to set aside billions of euros to protect against possible losses.

"Sovereign debt has lost its apparent risk-free status," Hervé Hannoun, deputy director general of the Bank for International Settlements, said in a recent speech in which he called for an end to "the fiction." To restore confidence, he concluded, the world needs to move "from denial to recognition."

Which eurozone country's debt has been most volatile over the last two days? No, not Italy's

by Nils Pratley - Guardian

While the yield on Italian bonds stabilised at just below 7%, France's has been rising to a record spread over the German bund

Question: whose 10-year bond yields have risen more in the past two days' trading: Italy or France?

The answer is France, which has travelled from 3.15% on Wednesday morning to 3.48% Thursday afternoon (as at 6pm). Italy has gone from 6.75% to 6.95%. Of course, that's not the main story of the week, since Italy ended last week at 6.3% and touched 7.5% during Wednesday's drama. Even so, the blow-out in France's spread over Germany – a record in the euro era of 168 basis points – illustrates how the crisis is spreading.

Standard & Poor's, which erroneously dispatched a message on Thursday that France's credit rating had been downgraded, can't take all the blame (though the "technical error" was appalling). The deeper reasons include:

- French banks are carrying more Italian debt than anybody else – about €300bn worth. That's on top of the writedowns they are currently taking on their large Greek exposures.

- Within the worsening outlook for eurozone growth published by the European commission on Thursday, France came off badly. Don't expect growth of 2% next year: the new figure is just 0.6%.

- A credit rating change now seems more likely, even if S&P has fixed its computer. In the tail-wags-dog world of ratings agencies, higher yields tend to make downgrades more likely.

- There is the worry that any attempt at bailing out Italy would put intense pressure on France. The European financial stability facility is backed by guarantees from member states. Italy obviously couldn't give guarantees on loans to itself, so a greater burden would fall on others. Alternatively, any officially sanctioned "haircut" for holders of Italian debt would rebound on French banks.

Valérie Pécresse, the French budget minister, is entitled to argue that France is "not at all in the same situation" as Italy. The trouble is, in the eyes of some investors, betting against French bonds has suddenly become two bets for the price of one. It's a cheap way to bet against the eurozone finding a painless solution to the Italian muddle; and it's a way to gamble that the latest French austerity package, a mix of tax rises and spending cuts, won't be enough to hit the deficit targets and thus satisfy ratings agencies.

'France will be the next to crumble', warns Gordon Brown

by Henry Samuel - Telegraph

France risks becoming the next victim of the sovereign-debt crisis "in the coming weeks", Gordon Brown, the former prime minister, has warned.

Mr Brown’s prediction came as the difference between French borrowing costs and those of Germany hit record levels. EU leaders urged France to draw up further austerity measures to meet its deficit reduction targets, amid fears the eurozone’s second biggest economy could crumble if Italy’s debt crisis spirals out of control.

Mr Brown, speaking in Moscow, said: "France is in danger of being picked off by the markets in the coming weeks and months." He urged Nicolas Sarkozy, the French president and current G20 chairman, to draw up a "global growth agreement" with major powers such as China. Such a deal could help to support the EU, whose bail-out mechanisms are not big enough to prop up a major nation.

Mr Brown’s speech echoed Olli Rehn, the EU economics commissioner. Mr Rehn urged France to take further steps to cut its public deficit to a limit of 3 per cent of gross domestic product in 2013 from an estimated 5.7 per cent this year. He said it was set to miss those targets by a wide margin. "We believe that it is best that France announces, as early as possible, the measures that are needed to keep its deficit in line with the official targets for 2012 and 2013," he said.

The "spread" or difference between German and French 10-year government bond rates – the cost of state borrowing which reflects investor confidence – hit a high of 170 basis points yesterday before falling back. At the close, the interest rate or yield on a 10-year French bond was 3.46 per cent, while its German equivalent was 1.78 per cent.

On Monday France announced a €65 billion austerity package over five years – its second in three months – to retain the triple-A credit rating, which allows it to borrow at the lowest rates.

The credit agency Moody’s put France under "observation" last month and could revise its rating in January. Mr Sarkozy announced a €12 billion package in August consisting mostly of small tax rises and the abolition of tax breaks. That was to respond to it revising down its growth forecast for next year from an optimistic 1.75 per cent to 1 per cent.

The European Commission yesterday scaled down its forecast for French growth to just 0.6 per cent next year as it warned that the debt crisis risked dragging the entire bloc into recession.

With presidential elections in France just six months away, the unpopular Mr Sarkozy is staking his credibility on deficit reduction, as he tries to convince voters he is a safer pair of hands than his Socialist rival, François Hollande. This in part explains why his government dismissed the suggestion it needed more austerity measures yesterday. But a chasm appeared to be opening between Europe’s two big economies.

"Let’s not have any illusions," said Jacques Attali, a former adviser to president François Mitterrand and head of the European Bank of Reconstruction and Development. "On the markets French debt has already lost its triple-A status."

One Elysée Palace official told Le Monde newspaper: "If Nicolas Sarkozy loses our triple-A, he is dead." In a sign of market jitters, the ratings agency Standard and Poor’s mistakenly announced to some clients a downgrade of France’s credit rating to AA. It later apologised for a "technical error".

Eurozone crisis threatens to spread to France as Paris is warned over its debts

by Phillip Inman - Guardian

Nicolas Sarkozy's government told to do more to cut state spending as figures reveal a slump in the country's industry

France is under pressure to reassure markets that it can cope with the deteriorating situation in the eurozone, after official figures showed a slump in industrial production that could wipe out any chance of growth next year.

The eurozone's second largest economy came under fire from the European Union and international investors for not doing more to cut government spending amid fears the debt crisis would escalate and ensnare the French economy.

Bond yields, which determine the interest rate for government borrowing, rose as France snubbed the EU call for more austerity measures, saying the country's latest round of belt tightening would be enough to bring its deficit within EU limits. The gap between French and German bond yields hit a new record as German yields fell to 1.78% and French yields rose to 3.48% on 10-year bonds.

The febrile atmosphere surrounding Paris was heightened after the ratings agency Standard & Poor's mistakenly issued a notice stripping France of its coveted AAA rating. The agency has threatened to issue a downgrade, which would push up bond yields further, but said the document was a mistake. Some economists said the gloomy picture in France meant the country had fallen out of the first rank of euro nations.

Much of its success in recent years had depended on making loans to peripheral eurozone countries, many of which were now in deep trouble and possibly unable repay all their loans. French banks have written off most of their loans to Greece, but would need a big bailout by French taxpayers if their loans to Italy suffered a similar fate.

Estimates French banks have lent around €300bn to the Italian government and Italian banks meant Paris could struggle to avoid being drawn into the debt crisis. President Nicolas Sarkozy's government announced on Monday a second savings drive in three months, as it battles to keep its deficit targets within reach in AAA rating as one of the world's safest borrowers.

Forecasting lower growth in France than the government, EU economic and monetary policy commissioner Olli Rehn urged further steps to ensure France is able to cut its public deficit to an EU limit of 3% of GDP in 2013 from an estimated 5.7% this year.

"We believe that it is best that France announces, as early as possible, the measures that are needed to keep its deficit in line with the official targets for 2012 and 2013," Rehn said. But French finance minister Francois Baroin and budget minister Valerie Pecresse said the latest saving measures had built in leeway to offset the impact of lower than expected growth both in 2012 and 2013.

French industrial production slumped 1.7% month on month in September, coming in lower than expected. The poor figures were compounded by a Bank of France business sentiment indicator that fell back to 96 in October, from 97 in September and a prediction by the EU that France would grow at 0.6% next year instead of the previous estimate of 2%.

Michael Derks, Chief Strategist at currency trader FxPro, said a break-up of the euro would leave France outside the top rank. "The 'outs' will likely consist of Greece, Portugal, Ireland, Italy and Spain, while the 'ins' would definitely be Germany, Austria, the Netherlands and Finland. France would be aghast at not being an automatic inclusion in this 'in' group, but the way its bond yields are headed, membership is definitely not guaranteed. Likewise, Belgium is also in danger of being cast adrift."

Stephen Lewis, chief economist at Monument Securities said: "The Mediterranean nations' economies almost certainly diverge too far from the German template for them to sustain the fiscal discipline that the new arrangements would demand. The question is whether even France would be able to keep up.

Doubtless, the Franco-German negotiators would maintain the presumption that it could, seeing that divergence between France and Germany would defeat the purpose of the EU. But that political imperative might still run counter to economic reality.

Austria seeks to calm investors as debt yields rise

by Tracy Alloway - FT

Fears over Europe’s intensifying debt crisis have spread to the Austrian bond market, with the interest rate premium demanded by investors to hold the country’s debt over that of Germany rising to a euro-era record. A sell-off in Austrian debt on Friday prompted the country’s finance ministry to insist that its top-tier triple A bond rating was not in jeopardy.

Austria is regarded by investors as having close financial ties to Italy, where Rome’s debt has sold off this week amid political turmoil and following a decision by one of Europe’s largest clearing houses to require traders to post more collateral to buy and sell Italian debt. That, in turn, sparked a sell-off of French government bonds, where yields on 10-year government bonds have increased almost 39 basis points since the start of the week.

On Friday, even as French and Italian bond yields traded below this week’s highs, investors began selling heavily the triple A-rated bonds issued by Austria. "Austrian debt has basically gravitated with France," said Marc Ostwald of Monument Securities. "People have always perceived France and Austria to be vulnerable – Austria in particular because of its exposure to Italy and also eastern Europe."

Austria is one of a dwindling number of countries in the eurozone that are still triple-A rated. These include Germany and France. The country is also one of the more significant guarantors of Europe’s €440bn rescue fund, the European Financial Stability Facility.

There has been speculation in the markets that Austria might lose its coveted AAA-rating because of worsening market conditions for Italy. No rating agency has acted. "Friday rumours about rating downgrades have become regular occurences," said Mr Ostwald.

The yield on 10-year Austrian debt has surged at least 42 basis points since the start of the week, reaching 3.44 per cent on Friday. German debt, meanwhile, has barely moved despite the deepening eurozone crisis, with 10-year yields at 1.79 per cent. The spread between the two countries’ debt rose to 165 bp.

Austria has largely avoided the spotlight since the 2009 market turmoil in central and eastern Europe, when markets fretted over the strength of the region’s and possible contagion to countries like Austria. However, Moody’s, the rating agency, said earlier this month it had put Austria’s Erste Bank on review for a possible credit rating downgrade.

Vienna sought to reassure nervous investors, with the finance ministry publishing a statement saying that the country’s credit rating was "secure".

Slovenian Bond Yield Breaks 7%, First Time Since Euro Entry

by Boris Cerni - Bloomberg

Slovenia’s 10-year government bonds slid for a fourth day with the yield topping 7 percent for the first time since the nation adopted the euro in 2007 as the debt crisis in Europe roils markets.

The yield rose to 7.045 percent at 11:46 a.m. in Ljubljana, according to Bloomberg data. The difference, or spread, investors demand to hold the securities instead of similar maturity German debt also advanced to a euro-era record of 535 basis points. A basis point is a hundredth of a percentage point.

Slovenia, which holds early elections next month, was cut by Standard & Poor’s, Moody’s Investors Service and Fitch Ratings on the government’s collapse, the poor economic outlook and a weak banking industry. The former Yugoslav republic is also a victim of its "proximity" to Italy, which is struggling to fend off an investors’ crisis of confidence.

"The worry is that turmoil in Italy will last for some time, pushing Slovenian bond yields even higher," Michal Dybula, an economist at BNP Paribas in Warsaw, Poland, said in a phone interview yesterday."However, even if they breach the 7 percent mark that would not be the same evil as in Italy."

Slovenian bond yields started to advance since voters rejected pension changes in a June referendum. The spread versus German debt at the time was 147 basis points. The export-driven economy will expand 1.1 percent this year, down from a previous estimate of a 1.9 percent expansion, the European Commission said in a report yesterday.

Gross domestic product growth slowed to an annual 0.9 percent in the second quarter from a 2.3 percent pace in the first three months. The central bank sees GDP expanding 1.3 percent this year. Slovenia’s outgoing Finance Minister Franc Krizanic declined to comment on the yield advance today at a bankers forum in Brdo near the capital Ljubljana. He said the country shouldn’t have financing problems until 2014.

Permanent Bailout Fund Said to Face Delay on Bond Loss Clash

by James G. Neuger - Bloomberg

European efforts to speed the setup of a permanent rescue fund have lost momentum amid a clash between Germany and France over provisions to force bondholders to share losses, three people involved in the negotiations said.

Finance ministers failed to bridge divisions this week over the European Stability Mechanism, lessening the chances of activating its 500 billion-euro ($680 billion) war chest next July, said the people, who declined to be identified because the talks are in progress. Officials had hoped to bring the ESM’s start date forward to mid-2012 from its ultimate deadline of July 2013, the people said.

Germany and the Netherlands are resisting pleas by France, Spain, Portugal and Ireland for the bondholder-loss provisions to be stripped from the ESM treaty, the people said. It’s possible that officials will still beat the July 2013 deadline, the officials said.

"You have different political entities that have to come together and that’s very hard to do," Alexander Friedman, Zurich-based chief investment officer at UBS Wealth Management, told Bloomberg Television’s "The Pulse" with Maryam Nemazee.

European officials are scrambling to pull together as much money as they can to show investors they can stamp out the region’s worsening debt crisis. Operating the ESM in combination with the 440 billion-euro temporary fund next year would potentially boost Europe’s anti-crisis resources to 940 billion euros.

'Exceptional and Unique'

"Private sector involvement" was foreseen in a first version of the ESM treaty, signed July 11. Ten days later, euro government leaders negotiated writedowns on Greek debt, declaring that treatment as "exceptional and unique."

The opponents of bondholder-loss provisions seized on that declaration to press for amendments to the ESM treaty. The July 21 summit also foresaw additional powers for the temporary rescue fund, and for the ESM as well. They include bond purchases and extending emergency credit lines to distressed European nations. As a result of the new powers, the freshly inked ESM treaty had to be rewritten before being sent to national parliaments for ratification.

In parallel, the European Commission and governments including Finland called for the ESM to be set up a year earlier. The clash at the Nov. 7 meeting of finance ministers also made it impossible to ready the new treaty by Nov. 19, when Spain’s parliament dissolves before elections.

That means the euro zone will miss a self-imposed end- November deadline for signing the new version. The earliest that can now happen is January, one of the people said. It’s also possible that earnest discussions of the revised version at ministerial level won’t resume until January or February, another said.

Market volatility limits EFSF firepower

by Peter Spiegel - FT

This week’s market upheaval in Europe has made it difficult to increase the firepower of the eurozone’s €440bn rescue fund to the €1,000bn that the bloc’s leaders had hoped for, the fund’s chief executive said on Thursday.

Investors have fled from bonds issued by highly indebted countries. Luring them back by offering insurance on losses – the centrepiece of a plan agreed in Brussels on October 26 – would now probably use up more of the fund’s resources, Klaus Regling, head of the European financial stability facility, said.

His concerns underline Europe’s difficulties in putting in place mechanisms to contain the sovereign debt crisis and, if necessary, help Italy cope with soaring refinancing costs. "The political turmoil that we saw in the last 10 days probably reduces the potential for leverage," Mr Regling told reporters. "It was always ambitious to have that number, but I’m not ruling it out."

The European Commission sharply downgraded its forecast for eurozone growth next year from 1.8 per cent to 0.5 per cent. The global ramifications of Europe’s economic woes became clearer with the growth in China’s exports to the EU slowing in October and a sell-off in Asian equities markets.

The loss-guarantee programme aims to leverage the €250bn ($340bn) remaining in the EFSF to cover more than four to five times the value of bonds than if the fund purchased the bonds outright. But Mr Regling said heightened investor skittishness meant the guarantees would now have to be bigger in order to convince investors to participate, meaning the fund was likely to have only three to four times the firepower.

Leveraging the EFSF’s dwindling resources is the cornerstone of a plan to increase so-called "firewalls" to prevent the turmoil in Greece from spreading to European banks and its largest economies, particularly Italy.