"Samuel Clemens, a.k.a. Mark Twain, aboard the Bermudian after a trip to Bermuda, four months before his death"

Ilargi: Over the weekend, I wrote about Fannie Mae and Freddie Mac, and how they form the core of the biggest fraud and crime ever perpetrated upon the American people. And even though that was already the umptieth time I have addressed this particular topic, I want to return to it again.

After all, we're not talking about Jesse James or Billy the Kid or Charles Ponzi or Kenny-Boy Enron or any of that petty kiddy wannabe criminal stuff, this is the number one way Americans have ever been fleeced right across the entire nation. Maybe that status is best recognized by the fact that people to this day keep on begging for more of the same. Either that or another little fact: the government is at the center of the scheme.

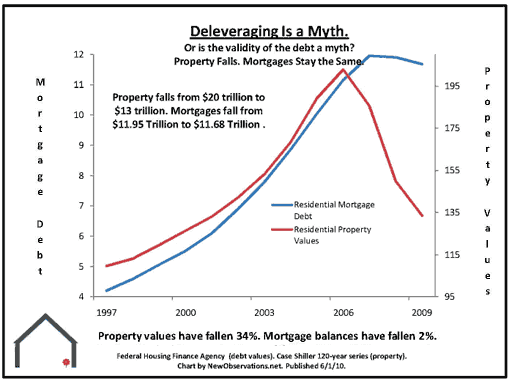

In the July 11 post at TAE, there was an article by Michael David White, a Chicago area real estate broker who a few years ago started calling on his clients to NOT buy a home. I’ve featured many of White's articles since; I like that kind of attitude. In last week’s piece by White Pending Homes Sales Crash in a Record Fall to a Record Low as Tax Break Expires, though, something was missing. There was a line that said "see the graph below", but there was no graph. Since I had a hunch which graph he meant. I sent him a mail. And yes, he came back to me with the graph (some 6 weeks old) that can hardly be surpassed in its definition and clarity of the depth of the US housing and credit crisis.

Take a look at this baby:

That is, what Americans' homes are worth, their equity, decreased by $7 trillion -from $20 trillion to $13 trillion-, from spring 2006 to spring 2010. In the same period, mortgage debt, what Americans owe on their homes, went down by only $270 billion. Yes, that's right: US homeowners lost more, by a factor of 26, than they "gained" through clearing mortgage debt. Thus, if we estimate that there are 75 million homeowners in America, they all, each and every one of them, lost $93,333.

Good morning America!!

And your own government is still trying to encourage homeownership? Now why would they want to do that in the face of numbers such as these? How much thought have you given that question? Over the past 4 years, the "right to own a home" has become synonymous with the "right" to lose some $25,000 a year. Why does Washington, through Fannie and Freddie, Ginnie Mae and the FHLB, continue to guarantee guaranteed losses for American citizens?

While these may seem separate issues, to me it all feels eerily in the same vein as Eric Sprott and David Franklin pointing out that every single US banking company but the 6 Too Big To Fail ones lost money in 2009, all 980 of them:

"Wither Green Shoots"Of the 986 bank holding companies in the US last year, a total of 980 of them LOST MONEY.

And that’s even after all the government bailouts the sector received. Hmmmm. Robust banking recovery? Not a chance. However, the remaining six banks, all of which are "too big to fail", did manage to earn a combined $51 billion in 2009, sending their stocks soaring as a result. So despite 980 out of 986 bank holding companies returning nothing but red, the sector actually fared pretty well from a market perspective.

Does this make any sense to you? Here we have an entire sector that is essentially broken; where a mere handful have maintained profitability not from their own strength but thanks to the taxpayers’ bailouts; and where the government is now aiming the most powerful of their regulatory reforms – and the market decides to pile into their respective equities?

And banking is not the only sector Sprott and Franklin say is completely out of whack. It all leads back, how could it not, to housing, Fannie and Freddie, and more losses for homeowners going forward, to add on to the $7 trillion already incurred.

The banking sector isn’t the only equity space that confounds us – the housing stocks are as equally absurd. Despite what you may have heard from your local real estate agent, the fundamentals for US housing are looking dismal. Ever since the tax credits have rolled off, new home sales are now running at 300,000 on a seasonally-adjusted annual rate ("SAAR"), representing a new all time low this past May. For comparison, this is down from an all time high of 1,389,000 new home sales made in July of 2004.3 Reading this, you may expect the home builder stocks to have performed poorly. But no, not in this market!

[..] from the day that Bernanke first saw his ‘green shoots’, the home builders index appreciated by 47% to June 30, 2010, peaking at 104% on April 23rd – all while new home sales were down 14% over the same time period on a SAAR basis.4 ‘The Market is Always Right’, as they say, but it simply can’t be with regard to these stocks. The housing ‘green shoots’ were the product of government initiative, rather than true fundamental improvement, and were thus short term in nature. Now that the government program has ended, the whole sector looks poised to fall apart.

And finally, for both the cherry and the icing on the cake, Bradley Keoun and David Henry at Bloomberg explain one of many ways in which banks keep the facade upright. They can book a profit when their own bonds lose value. How, you ask, why? Because it -in theory- allows them to buy back their own bonds at a lower price.

Bank Profits Depend on Debt-Writedown 'Abomination' in Forecast

The second-quarter results may include gains taken under a U.S. accounting rule known as Statement 159, adopted by the Financial Accounting Standards Board in 2007, which allows banks to book profits when the value of their bonds falls from par. The rule expanded the daily marking of banks’ trading assets to their liabilities, under the theory that a profit would be realized if the debt were bought back at a discount.

In practice, it’s an accounting "abomination" because fluctuations in the value of the debt don’t change the amount the banks owe, said Chris Kotowski, an analyst at Oppenheimer & Co. in New York. "Just because Morgan’s credit spreads widened out this quarter doesn’t mean that their ultimate interest and principal payments changed one iota," Kotowski said. "The market will back it out, both on the upside and the downside."

To summarize, all US banks would have lost money last year if it hadn't been for your taxpayer dollars, and, indeed, all but the 6 biggest did. They received many trillions in public funds, all of which are a loss to you, who have also lost those $7 trillion on your home values. The balance sheets of the big banks, however, still wouldn't look good even with all your funds; they need stupid accounting pet tricks for that. Just like the government.

The overall picture is one of a ridiculous patchwork of lies and tricks and fraud and ultimately for you, losses bigger than you can bear.

Is it time to storm the Bastille again?

Ilargi: As you may have guessed, Stoneleigh and I have recently run into some serious internet access issues. We are now sitting in a McDonald’s [sic!] half an hour from Milan, where the WiFi works only intermittently. And that took us about a day to find. Apologies for the delays, but we’ll keep on trying as hard as we can.

Tonight, July 14, Stoneleigh has a talk in Carimate. I understand the mayor has invited his entire city council. Hey, maybe one of them has reliable internet access in his/her office.

Wither Green Shoots

by Eric Sprott and David Franklin, Sprott Asset Management

With the summer now upon us, the "Sell in May and Go Away" adage has proven itself true once again. The major market indexes are all turning downward, and while they haven’t dropped enough yet to warrant panic, we certainly want to be positioned properly if this trend continues into the fall. The market tea leaves are no longer sending mixed signals either – most of the new data is decidedly bearish. So what happened to all the ‘green shoots’? What happened to the strong recovery the market rally was promising?

Economic data released over the past two weeks have decimated any remaining belief in a lasting economic recovery. Slowdowns are appearing in the US, Europe, Japan and even China. Auto sales, housing starts, employment, consumer confidence, factory orders, consumer purchase intentions - just about every aspect of the economy that can be measured, is showing decided weakness.

Of particular interest to us over the past year has been the GDP forecasts released by The Consumer Metrics Institute in Colorado ("CMI"). CMI caught our attention with their real time tracking of consumer retail sales data. Consumer spending represents 70% of GDP, and that spending can provide great insight into the workings of the underlying economy. CMI’s retail sales data has indentified a long, negative contraction in the economy based on their data set for the last 180 days. This was confirmed most notably in Walmart’s poor first quarter sales results when CFO Tom Schoewe stated, "More than ever, our customers are living paycheck to paycheck."1 If that sentiment applies to other large retailers, it doesn’t bode well for 2010 GDP.

CMI also predicted 2010 Q1 GDP growth at 2.62% all the way back in November 2009. It took nearly seven months for the actual US GDP data to eventually be released, but when it finally did (after three revisions, no less) it turned out that CMI’s prediction was bang on. Interestingly, when the real data came out, CMI founder Rick Davis noted that the inventory component underlying the 2.7% Q1 GDP growth figure had moved from 1.65% up to 1.88% – meaning that the bulk of GDP growth, almost 66%, actually came from inventory swings rather than consumer demand.

No wonder factory orders fell out of bed this past week! With the re-stocking complete, there aren’t enough new orders to clear the fresh inventory. And if two thirds of Q1 growth came from inventory swings (or just plain re-stocking etc.), it makes us wonder what we can realistically expect from the next two GDP announcements. CMI provided the following guidance for the balance of the year, stating that "We expect GDP growth to be flat for the second quarter, but with inventory adjustment reversals absolutely killing the reported ‘growth’ number just four days before the U.S. mid-term elections." If that turns out to be correct, it will be unfortunate timing for the elections.

An important question to ask is whether the March ’09 rally was really justified at all. Were the green shoots real? Or was the market just looking for a way to justify the effects of government-induced ‘easy money’? The stock market is supposed to be an efficient, forward-looking indicator after all – and the rally that began in March ’09 was supposed to signal a robust recovery. So where’s the recovery? From the time the term ‘green shoots’ was first uttered by Ben Bernanke on March 15, 2009, the S&P 500 rallied 36% to June 30, 2010 and by as much as 60% to April 26, 2010. If the green shoots were really just the early indications of weeds, was the market wrong to appreciate so dramatically?

There is little doubt that much of the stock market action during the past 12 months has defied traditional market rules. Nowhere is this more evident to us than in the banking stocks. We’re still scratching our heads on the whole sector. Readers may remember an article we wrote in November 2009 entitled "Don’t Bank on the Banks" in which we discussed the hazard of leverage in the banking system. If you gauge our conclusions by what actually transpired in the banking sector as a whole, we were essentially correct.

Of the 986 bank holding companies in the US last year, a total of 980 of them LOST MONEY.

And that’s even after all the government bailouts the sector received. Hmmmm. Robust banking recovery? Not a chance. However, the remaining six banks, all of which are "too big to fail", did manage to earn a combined $51 billion in 2009, sending their stocks soaring as a result. So despite 980 out of 986 bank holding companies returning nothing but red, the sector actually fared pretty well from a market perspective. Does this make any sense to you? Here we have an entire sector that is essentially broken; where a mere handful have maintained profitability not from their own strength but thanks to the taxpayers’ bailouts; and where the government is now aiming the most powerful of their regulatory reforms – and the market decides to pile into their respective equities?

The banking sector isn’t the only equity space that confounds us – the housing stocks are as equally absurd. Despite what you may have heard from your local real estate agent, the fundamentals for US housing are looking dismal. Ever since the tax credits have rolled off, new home sales are now running at 300,000 on a seasonally-adjusted annual rate ("SAAR"), representing a new all time low this past May. For comparison, this is down from an all time high of 1,389,000 new home sales made in July of 2004.3 Reading this, you may expect the home builder stocks to have performed poorly. But no, not in this market!

As you can see in Chart A, from the day that Bernanke first saw his ‘green shoots’, the home builders index appreciated by 47% to June 30, 2010, peaking at 104% on April 23rd – all while new home sales were down 14% over the same time period on a SAAR basis.4 ‘The Market is Always Right’, as they say, but it simply can’t be with regard to these stocks. The housing ‘green shoots’ were the product of government initiative, rather than true fundamental improvement, and were thus short term in nature. Now that the government program has ended, the whole sector looks poised to fall apart.

At the end of the day, nobody should be surprised by the recent economic data. The stock market rally that began in March ’09 was driven by monetary phenomena rather than anything fundamental, and based on data from CMI for 2010 it appears that we have already entered an economic contraction phase. The market is now beginning to reflect the fact that the green shoots were actually just the early signs of weeds, and it would suffice to say that virtually all the major world governments have some serious gardening to do. The recent contractions don’t necessarily mean that we’ll experience a repeat of 2008’s stock market performance in 2010, but it does suggest that investors should question the real fundamentals underlying their investments, lest the market begins to trade on them again.

Bank Profits Depend on Debt-Writedown 'Abomination' in Forecast

by Bradley Keoun and David Henry - Bloomberg

Bank of America Corp. and Wall Street firms that notched perfect trading records in the first quarter are now depending on an accounting benefit last used in the depths of the credit crisis to prop up their results. Bank of America, the biggest U.S. bank by assets, may record a $1 billion second-quarter gain from writing down its debts to their market value, Citigroup Inc. analyst Keith Horowitz estimated in a June 23 report. The boost to earnings, stemming from an accounting rule that allows banks to book profits when the value of their own bonds falls, probably represented a fifth of pretax income, Horowitz wrote.

Investor fears of a Greek default, stalled U.S. economic recovery and tougher industry regulations have rattled markets, snapping banks’ trading streaks and rekindling doubts about their creditworthiness. Prices for Bank of America’s credit derivatives -- used by traders to bet on the likelihood of the firm’s default -- rose by 34 percent during the second quarter, while Morgan Stanley’s doubled and Goldman Sachs Group Inc.’s surged 86 percent.

"What’s on investors’ minds are the macroeconomic issues, as reflected by the interbank market in Europe, the very low yields on U.S. Treasuries and recent data on economic growth, jobs and housing," Credit Agricole Securities USA analyst Michael Mayo said in an interview. "To the extent that the earnings power is less, the banks would not generate as much capital, so there’s less capital available to absorb future losses."

Statement 159

In the first quarter, the four biggest U.S. lenders -- Bank of America, JPMorgan Chase & Co., Citigroup and Wells Fargo & Co. -- produced combined profit of $13.5 billion, the most since the second quarter of 2007. That figure probably fell by 28 percent in the second quarter, based on a Bloomberg survey of analysts’ estimates. The banks are scheduled to announce results over the next two weeks, led by JPMorgan on July 15.

The second-quarter results may include gains taken under a U.S. accounting rule known as Statement 159, adopted by the Financial Accounting Standards Board in 2007, which allows banks to book profits when the value of their bonds falls from par. The rule expanded the daily marking of banks’ trading assets to their liabilities, under the theory that a profit would be realized if the debt were bought back at a discount.

Accounting ‘Abomination’

In practice, it’s an accounting "abomination" because fluctuations in the value of the debt don’t change the amount the banks owe, said Chris Kotowski, an analyst at Oppenheimer & Co. in New York. "Just because Morgan’s credit spreads widened out this quarter doesn’t mean that their ultimate interest and principal payments changed one iota," Kotowski said. "The market will back it out, both on the upside and the downside."

Kotowski has been covering the banking industry since 1987 and returns on his stock recommendations over the past year have outperformed the average of peer analysts, according to data compiled by Bloomberg. He has been discounting the valuation gains from his analysis since at least the third quarter of last year, and wrote in an October 2009 report that the "after- effects of a hundred-year storm are not shaken off in a couple quarters."

Morgan Stanley probably recorded $1 billion in such debt- valuation adjustments in the second quarter, Citigroup’s Horowitz wrote. That represents 60 percent of the analyst’s forecast for the firm’s pretax income. Morgan Stanley booked $5.1 billion of gains in fiscal 2008 as its bond spreads widened, then reversed them in 2009 as markets improved and spreads tightened.

Goldman Sachs may have had $375 million of gains in the second quarter, while JPMorgan had $300 million, Horowitz wrote.

DVA Gains

Including Bank of America, the four banks probably had debt-valuation adjustments, or DVAs, amounting to an average of 18 percent of pretax income, based on Horowitz’s estimates.

Citigroup may have booked $400 million under the accounting rule, estimated Bank of America analyst Guy Moszkowski. "It’s deja vu to 2008," said Credit Agricole’s Mayo. "DVA gains are back."

In the first quarter, an unbroken string of profitable trading days helped Charlotte, North Carolina-based Bank of America post higher profit than analysts estimated, even as unemployment stayed close to a 27-year high. Goldman Sachs, JPMorgan and Citigroup also reported perfect trading quarters, while Morgan Stanley was profitable on 57 of 61 trading days. All four firms are based in New York. "The credit cycle is clearly behind us," Bank of America Chief Executive Officer Brian Moynihan told investors in April following the bank’s first-quarter earnings report.

‘Prevailing Winds’

In the ensuing months, corporate-bond yields widened, leading to a "pullback in client participation" and lower fixed-income trading results, Steve Stelmach, an Arlington, Virginia-based analyst at FBR Capital Markets, wrote in a June 30 report. Non-investment-grade bonds lost 0.7 percent last quarter, compared with a total return of 4.82 percent in the first, based on the Bank of America Merrill Lynch U.S. High Yield Master II Index. "When the prevailing winds of credit spreads tighten, they make a lot of money, and when spreads widen, they can’t make as much," said David Hendler, a senior analyst at New York-based research firm CreditSights Inc.

The Standard & Poor’s 500 Index fell by 15 percent from a 19-month high in April, curbing stock-trading revenue and prompting companies to cancel or postpone new share offerings and hold off on mergers and acquisitions that Wall Street bankers advise on to generate fees. U.S. bond sales fell to $335.8 billion in the second quarter, down 37 percent from both the first quarter and the second quarter of 2009, according to Bloomberg data. It was the lowest amount since the fourth quarter of 2008.

Lackluster Demand

The weaker trading environment highlights how banks are suffering from lackluster demand for their basic products: loans to companies and consumers. Loans and leases held by U.S. banks shrank for the sixth consecutive quarter to $6.88 trillion as of June 30, according to Federal Reserve data, which include an accounting change. Delinquencies on commercial real estate loans rose to 7.5 percent in May from 6.42 percent in March, according to Moody’s Investors Service.

Citigroup, which is 18 percent owned by the U.S. Treasury Department, probably had net income of $1.54 billion in the second quarter, the average of eight analysts’ estimates in a Bloomberg survey, down 65 percent from the prior quarter and 64 percent from a year earlier. "Our near-term performance will continue to reflect the pace of economic recovery and the level of activity in capital markets," Citigroup CEO Vikram Pandit, 53, said in April after the bank’s first-quarter profit almost tripled from a year earlier.

Goldman, Morgan Stanley

Profit probably fell 25 percent at Bank of America from the second quarter of the previous year, 18 percent at San Francisco-based Wells Fargo and 47 percent at Goldman Sachs, the Bloomberg survey shows. JPMorgan’s profit, which probably rose 17 percent from a year earlier, may be 4.5 percent lower than it was in the first quarter. Morgan Stanley’s second-quarter profit, depressed a year ago by a $2.3 billion debt-valuation charge when its CDS spreads were tightening, probably rose sevenfold, according to the survey. Compared with the first quarter, Morgan Stanley’s profit probably fell by 35 percent.

At the same time, banks are adding jobs for the first time in two years in a bet that recent market turmoil will prove temporary and fewer U.S. consumers may fall behind on loan payments. In New York, 6,800 financial-industry positions were added from the end of February through May, the largest three- month increase since 2008, according to the New York State Department of Labor.

‘Unusually Weak’

JPMorgan last month reported that credit-card loans more than 30 days late fell to 4.22 percent from 4.4 percent the previous month. That was the lowest since July 2009. None of the six largest banks is forecast to report a loss for the second quarter, a contrast with the fourth quarter of 2008 when they had combined net losses of $25.3 billion.

Any optimism was lost on the market for bank stocks. The KBW Bank Index, which tracks the 24 biggest U.S. banks, fell 11 percent in the second quarter after climbing 22 percent in the first three months of the year. "The first quarter was unusually strong, and the second quarter feels like it is going to be unusually weak," Moshe Orenbuch, an analyst at Credit Suisse Group AG in New York, said in an interview.

States Can’t Count on Bailout, Obama Appointees Say

by Michael McDonald - Bloomberg

States can’t count on the federal government for more budget bailouts, the heads of President Barack Obama’s debt commission told governors. States expecting Congress to authorize more assistance are "going to be left with a very large hole to fill," said Erskine Bowles, co-chairman of the National Commission on Fiscal Responsibility and Reform. States including New York and California have urged Congress to extend stimulus spending authorized to combat the recession, including extra Medicaid funding and money to pay public school teachers.

"I don’t think we can count on the federal government again," Bowles, White House chief of staff under former President Bill Clinton, said yesterday at the National Governors Association meeting in Boston. "They just do not have the financial resources." While the economy has been expanding, states have yet to recover from the longest recession since the Great Depression. The rout cut into tax collections and led them to raise taxes and slash spending on schools, social services and other expenses. States have projected total budget deficits of $127 billion through 2012, according to a report last month by the governors association and the National Association of State Budget Officers.

Call for Help

The governors of New York, Pennsylvania and Michigan on June 30 led states pressing Congress to extend higher financing for Medicaid, the health-care program for the poor whose use surged during the economic crisis. David Paterson of New York, Edward Rendell of Pennsylvania and Jennifer Granholm of Michigan and three other governors, all Democrats, traveled to Washington to appeal for funds after the Senate failed to approve $16 billion in extra financing for Medicaid and extended jobless benefits. Congressional Republicans opposed the measure’s cost.

"We need more help from Washington to protect against job cuts and health-care cuts," Illinois Governor Pat Quinn, a Democrat, said on July 10 at the Boston gathering. "If we don’t do that, we’re following Herbert Hoover economics." Earlier this year, 47 Republican and Democratic governors urged Congressional leaders to extend the Medicaid help, signing a letter asking for a six-month extension. Fewer are demanding a bailout now because the stimulus is unpopular, West Virginia Governor Joe Manchin said in an interview yesterday. "People are concerned that the amount of debt we’ve incurred hasn’t really stimulated the economy," said Manchin, a Democrat.

Recommendations Due

Forty-three percent of voters think the American Recovery and Reinvestment Act hurt the economy while 29 percent think it helped, according to a national telephone survey of 1,000 likely voters conducted July 1 by Rasmussen Reports, which has a margin of error of plus or minus 3 percentage points. After championing deficit spending to counter the economic downturn, Obama this year formed a commission to recommend ways to reduce the federal debt, which is projected to reach 90 percent of the U.S. economy by 2020. The panel’s recommendations are due Dec. 1, after the midterm elections in November.

Former Republican Senator Alan Simpson of Wyoming, the panel’s other co-chairman, told governors yesterday that the depth of the federal government’s spending imbalance is "shocking," which limits the help it can provide for strained state budgets. "The pig is dead," said Simpson, referring to so-called pork-barrel spending that Congress directs to states. "There’s no more bacon."

Tax Collections Drop

State fiscal woes will be "just as tough" next year because the economy is on pace to grow at a "lackluster" rate of about 3 percent a year, Yolanda Kodrzycki, an economist at the Federal Reserve Bank of Boston, told governors July 10 at the gathering. The budget pressure will be compounded by the need to help cities and towns faced with a drop in property-tax collections, she said. Property-tax collections fell in the first quarter for the first time since the onset of the real-estate market’s crash, to $107.7 billion from $108.4 billion a year earlier, the Census Bureau said on June 29.

South Carolina Governor Mark Sanford said the "worst is yet to come" for the states because the economy is bound to fall back into a recession as government spending contracts both in the U.S. and elsewhere. Kodrzycki said researchers at the Fed have become "much more sensitive" to the prospect of a so-called double-dip recession. She said the economy needs to grow at an annual average rate of about 4 percent in order for the unemployment rate to fall back to 5 percent by 2015. "The road to economic recovery is a long one," she said. "It’s a sobering picture."

Froth and stagnation

by The Economist

In recent months several countries have experimented with measures to cool bubbly property markets. Yet since The Economist’s global round-up of housing markets was last published in April, house-price inflation has accelerated in some of the very countries where the authorities have intervened to slow its rise. Asia has been at the forefront of such interventions. In February Singapore’s government raised down-payment requirements and imposed stamp duties on all residential properties sold within a year of purchase in a bid to curb speculation. Despite these steps prices in the island nation rose by nearly 40% in the year to the end of the second quarter, after a rise of just over 25% in the year to the end of the first quarter.Singapore has overtaken Hong Kong to become the frothiest housing market among those we monitor. House prices in Australia rose by 20% in the year to the end of the first quarter, faster than the 13.5% recorded in the 12 months to late 2009.

More concerning, however, is our analysis of "fair value" in housing, which is based on comparing the current ratio of house prices to rents with its long-term average. By this measure Australian property is the most overvalued of any of the 20 countries we track. A frothy property market was one of the reasons for the Reserve Bank of Australia raising interest rates six times between October and May. Since then, the bank has become more sanguine about the state of the market. It cited "some signs that the earlier buoyancy in the housing market was easing" when keeping interest rates on hold in June.

China’s property-cooling measures, meanwhile, which were similar to Singapore’s, were announced in April. Our house-price figures for China now extend to the end of May. They help explain why the Chinese government had become more concerned. Year-on-year house-price inflation peaked in April at 12.8%, but has since moderated a bit.The prospect that house prices in China are about to fall sharply worries some. Kenneth Rogoff, a Harvard professor, said this week: "You’re starting to see that collapse in property and it’s going to hit the banking system." But Sun Mingchun, chief economist for China at Nomura, an investment bank, reckons that high down-payment requirements and the preponderance of cash purchases by Chinese homebuyers will help to limit the effects of any falls on the real economy.

For America the balance of evidence points to a renewed housing slowdown. Although both the Case-Shiller national and ten-city indices are up year-on-year, the national index fell during the three months to the end of March. The FHFA index, which excludes houses that are financed with large mortgages, was still down compared with a year earlier. More recent home-sales data have been similarly downbeat. Sales of new homes declined by 33% from April to May, thanks to the expiry of a tax credit. Just 28,000 new units were sold during May, the lowest total on record for that month. In Asia policymakers are trying to prick a bubble. In America they are still dealing with the consequences of the last one.

The IMF Is Coming for Your Social Security

by Dean Baker - Huffington Post

A few years back, there was a fear in some parts about black UN helicopters that were supposedly taking part in the planning of an invasion of the United States. While there was no foundation for this fear, there is basis for concern about the attack of another international organization, the International Monetary Fund (IMF). Last week, the IMF told the United States that it needs to start getting its budget deficit down. It put cutting Social Security at the top of the steps that the country should take to achieve deficit reduction. This one is more than a bit outrageous for two reasons.

First, the IMF deserves a substantial share of the blame for the economic crisis that gave us big deficits in the first place. The IMF is supposed to oversee the operations of the international financial system. According to standard economic theory, capital is supposed to flow from rich countries like the United States to poor countries to finance their development. In other words, the United States should be having a trade surplus, which would correspond to the money that we are investing in poor countries to finance their development.

However, the IMF messed up its management of financial crises so badly in the last 15 years that poor countries decided that they had to accumulate huge amounts of currency reserves in order to avoid ever being forced to deal with the IMF. This meant that capital was flowing in huge amounts in the wrong direction. One result of this reverse flow was that the United States ran a huge trade deficit instead of a trade surplus.

The trade deficit in the United States was a big part of the story of the housing bubble. The trade deficit cost millions of workers their jobs. This was one of the main reasons that economy was so weak coming out of the 2001 recession. This weakness led the Fed to keep interest rates at 50-year lows, until the growth of the housing bubble eventually began to generate jobs in the fall of 2003.

The IMF both bears much of the blame for the imbalances in the world economy and then for failing to clearly sound the alarms about the dangers of the bubble. While the IMF has no problem warning about retired workers getting too much in Social Security benefits, it apparently could not find its voice when the issue was the junk securities from Goldman Sachs or Citigroup that helped to fuel the housing bubble.

The collapse of this bubble has not only sank the world economy, it also destroyed most of the savings of the near retirees for whom the IMF wants to cut Social Security. The vast majority of middle-income retirees have most of their wealth in their home equity. This home equity largely disappeared when the bubble burst. Maybe the IMF doesn't have access to house price series and data on wealth, because if they did, it's hard to believe that they would advocate further harm to some of the main victims of their policy failure.

The other reason that the IMF's call for cutting Social Security benefits is infuriating is the incredible hypocrisy involved. The average Social Security benefit is just under $1,200 a month. No one can collect benefits until they reach the age of 62. By contrast, many IMF economists first qualify for benefits in their early 50s. They can begin drawing pensions at age 51 or 52 of more than $100,000 a year. This means that we have IMF economists, who failed disastrously at their jobs, who can draw six-figure pensions at age 52, telling ordinary workers that they have to take a cut in their $14,000 a year Social Security benefits that they can't start getting until age 62. Now that is real black helicopter material.

Chinese rating agency strips Western nations of AAA status

by Ambrose Evans-Pritchard - Telegraph

China's leading credit rating agency has stripped America, Britain, Germany and France of their AAA ratings, accusing Anglo-Saxon competitors of ideological bias in favour of the West. Dagong Global Credit Rating Co used its first foray into sovereign debt to paint a revolutionary picture of creditworthiness around the world, giving much greater weight to "wealth creating capacity" and foreign reserves than Fitch, Standard & Poor's, or Moody's. The US falls to AA, while Britain and France slither down to AA-. Belgium, Spain, Italy are ranked at A- along with Malaysia.

Meanwhile, China rises to AA+ with Germany, the Netherlands and Canada, reflecting its €2.4 trillion (£2 trillion) reserves and a blistering growth rate of 8pc to 10pc a year. Dominique Strauss-Kahn, chief of the International Monetary Fund, agreed on Monday that the rising East is a transforming global force. "Asia's time has come," he said. The IMF expects Asia to grow by 7.7pc in 2010, vastly outpacing the eurozone at 1pc and the US at 3.3pc. Emerging nations hold 75pc of the world's $8.4 trillion (£5.6 trillion) of reserves. Dagong rates Norway, Denmark, Switzerland, and Singapore at AAA, along with the commodity twins Australia and New Zealand.

Chinese president Hu Jintao said in April that the world needs "an objective, fair, and reasonable standard" for rating sovereign debt. Dagong appears to have stepped into the role, saying its objective was to assess countries using methods that would "not be affected by ideology". "The reason for the global financial crisis and debt crisis in Europe is that the current international credit rating system does not correctly reveal the debtor's repayment ability," said Guan Jianzhong, Dagong's chairman.

The agency, known in China for rating companies, said its goal is to "correct the defects" of the existing system and offer a counter-weight to Western agencies. Dagong appears to base growth potential on past performance but this can be misleading, especially in states enjoying technology catch-up. Japan was a high-flyer in 1970s and 1980s before stalling when the Nikkei bubble burst. It has been trapped in near perma-slump ever since.

China may start to face some of Japan's demographic problems by the middle of this decade when the working age population peaks. The Western rating agencies put a high value on a long-established rule of law and government institutions that have proved resilient over many decades, or even centuries. China's political system may appear strong – as did the Soviet Union's – but only time will tell whether its foundations are brittle. The violent upheavals of the Cultural Revolution are still a very fresh memory.

Chinese credit firm says US worse risk than China

by Joe McDonald - AP

A Chinese firm that aims to compete with Western rating agencies declared Washington a worse credit risk than Beijing in its first report on government debt Sunday amid efforts by China to boost its influence in global markets. Dagong International Credit Rating Co.'s verdict was a break with Moody's, Standard & Poors and Fitch, which say U.S. government debt is the world's safest. Dagong said it rated Washington below China and 11 other countries such as Switzerland and Australia due to high debt and slow growth. It warned the U.S. is among countries that might face rising borrowing costs and risks of default.

The report comes amid complaints by Beijing that Western rating agencies fail to give China full credit for its economic strength, boosting borrowing costs — a criticism echoed by some foreign analysts. At June's G-20 summit in Toronto, President Hu Jintao called for the creation of a more accurate system. Dagong, founded in 1994 to rate Chinese corporate debt, says it is privately owned and pledges to make its judgments impartially. But in a sign of official support, its announcement Sunday took place at the headquarters of the Xinhua News Agency, the ruling Communist Party's main propaganda outlet.

Dagong's chairman, Guan Jianzhong, said the current Western-led rating system is to blame for the global crisis and Europe's debt woes. He said it "provides the wrong credit-rating information" and fails to reflect changing conditions. "Dagong wants to make realistic and fair ratings," he said. Beijing has more than $900 billion invested in U.S. Treasury debt and has appealed to Washington to avoid hurting the value of the dollar or China's holdings as it spends heavily on its stimulus.

Dagong's report covered 50 governments and gave emerging economies such as Indonesia and Brazil better marks than those given by Western agencies, citing high growth. Along with the United States, some other developed nations such as Britain and France also received lower ratings than those of other agencies. Dagong rated U.S. government debt AA with a negative outlook, below the firm's top AAA rating. It warned that Washington, along with Britain, France and some other countries, might have trouble raising more money if they allow fiscal risks to get out of control. "The interest rate on debt instruments will run up rapidly and the default risk of these countries will grow even larger," its report said.

Dagong said it hopes to "break the monopoly" of Moody's Investors Service, Standard & Poors and Fitch Ratings. Their reputation suffered after they gave high ratings to mortgage-linked investments that soured when the U.S. housing market collapsed in 2007. Manoj Kulkarni, head of credit research for SJS Markets in Hong Kong, said that despite the possibility China's government might try to influence Dagong's decisions, there is room in the market for a Chinese agency because Western firms' credibility is badly tarnished.

"As long as there is another opinion and it is backed up, I don't really think a China-based company will have an incentive to rate, say, Indonesia any better than a U.S.-based rating agency," Kulkarni said. "If it comes to Chinese government-related companies, maybe there might be a conflict of interest, and investors would have to be aware of that fact," he said. Chinese leaders have appealed repeatedly to Washington to safeguard their country's U.S. holdings and avoid taking steps in response to the global crisis that might weaken the dollar or the value of American assets.

Dagong rated China AA-plus with a stable outlook — higher than Moody's A1 and S&P's A-plus — due to rapid growth and relatively low debt. Ahead of it were seven countries including Switzerland, Australia and Singapore that received the top rating of AAA, the same as those from Western agencies. Canada and the Netherlands also ranked above China. Dagong's stronger ratings for emerging economies echoed market sentiment toward some countries such as China and India. They are seen as better risks than their credit ratings suggest and pay lower rates. SJS Markets' Kulkarni noted that Western agencies give the two Asian giants a lower credit rating than Spain, despite their strong growth and the Spanish government's debt problems. Developing countries "tend not to get full credit" for their economic performance, he said. "Ratings are basically lagging."

Small Investors Flee Stocks, Changing Market Dynamics

by E.S. Browning - Wall Street Journal

Many individual investors were tiptoeing back into stocks in the spring. Now, they're running for cover again. Karen and Roger Potyk, a comfortably retired couple in San Antonio, Tex., had clung to some stock mutual funds despite their anxiety following the financial crisis of 2008. But the renewed market volatility following the "flash crash" of May 6 proved too much to bear.

"We just didn't want to put up with it any more," says Karen Potyk. She and her husband sold the last of their stock holdings on May 20, moving the money to bonds, certificates of deposit and bond-like annuities.

Small investors' faith in stocks, which surged in the 1990s, has collapsed since the technology-stock debacle and the Enron and WorldCom scandals of 2000-2002. The 2007-2009 financial crisis only made things worse. Now, the pullback among ordinary investors means they are a declining force in a market that is increasingly dominated by professionals. Some were tantalized by equities during the 70% rally that began in March 2009 and ran through April. But mutual-fund data and other clues suggest that that brief infatuation has ended.

In 2002, investors withdrew more money from mutual funds that invest in U.S. stocks than they put in. Then from 2007 through 2009 they withdrew money for three consecutive years. That marked the first three-year period of withdrawals since 1979-1981, according to the Investment Company Institute, a mutual-fund trade group. This year, U.S.-stock funds saw inflows in January, March and April, but net withdrawals resumed in May.

Investors talk of a growing disillusionment with big institutions, including corporations, government, banks and political parties—as well as fears about the nation's heavy debt. Some people's confidence in stocks was seriously shaken by the volatility that returned in May. They worry that the May 6 flash crash, when the Dow Jones Industrial Average fell 700 points in eight minutes before rebounding, is a sign that ordinary people are increasingly at the mercy of anonymous companies that trade with powerful computers.

Individual investors were important market pillars in the 1990s, but their flight from stocks is changing the market dynamic. By adding money to mutual funds, individuals helped push stocks higher in the 1990s and to a lesser extent from 2003 through 2006. Now they are moving money out again on balance, making them a drag on the market. Ordinary investors are returning to the cautious mentality they developed during the 1970s. That was the last extended period of stock weakness, after which it took many people a decade or more to get comfortable with stocks again. "I feel like the tail of the dog that is being wagged by institutional investors who are taking a lot of risk, playing a lot of games and just have these computerized orders that affect me a lot," says Simeon Thibeaux, a semi-retired businessman from Alexandria, La.

History suggests that individuals eventually will return to stocks, as they did in the 1980s and, even more strongly, in the 1990s. But rebuilding their confidence could take time, says Brian Reid, chief economist of the Investment Company Institute. Historically, it has taken an extended period of stock success to lure individuals back after long periods of disaffection. Rebounding after a two-month slump, the Dow Jones Industrial Average jumped 511 points, or 5%, to 10198.03 last week, its biggest weekly gain in almost a year, although it remains down 9% since topping out on April 26.

"We have gone through two of the worst bear markets since the Great Depression, and it has given investors a better sense of the risks and dangers of investing" in stocks, Mr. Reid says, referring to the bear markets of 2000-2002 and 2007-2009. The gradual dissipation of investor confidence can be seen in mutual-fund investing patterns.

After getting hurt in the 2000 tech-stock crunch, individuals came back to U.S.-stock funds in 2003, as stocks were entering a new bull market, ICI data show. But the buying proved tepid and turned to net selling in the latter part of 2006, even before the bull market ended in 2007. Despite occasional periods of inflows to U.S.-stock funds, the selling trend has continued since then. Individuals removed a net $7 billion from stock funds in the seven days ending May 12 and $13 billion two weeks later, eclipsing the deposits from earlier in the year.

Recent volatility has certainly shaken the Potyks' confidence. Mr. Potyk, a 68-year-old pharmacist, spent 25 years as an army officer and 11 years with Pfizer before retiring. His wife, 63, is a retired real-estate broker. The Potyks stuck with their stocks through the tech wreck, the Sept. 11 attacks and Enron. They were willing to take risks to get stock-market returns. By 2006, he and his financial adviser say, the Potyks' portfolio was 50% stocks and 50% bonds and other fixed-income investments.

The big blow to their confidence was the 2008 collapse of brokerage-firm Lehman Brothers, in which they lost $75,000 on a Lehman bond. Although it was a bond that hurt them, the Potyks' faith in all potentially risky investments was shattered. "In the military, you learn that you want people you can respect, trust—who have integrity," Mr. Potyk says. "Over the last five years or so, I find that our financial institutions have no shred of the character I describe."

The last straw was the May market volatility, accompanied by widespread fears about European government debt. On May 20, the Potyks asked their financial adviser to sell the last of their stock mutual funds. Now that their portfolio consists entirely of fixed-income investments, "I won't make 8% on my money. I will make 4% or 5%, but the money will be there," says Mr. Potyk.

Stocks had developed an almost cult-like following in the 1980s and 1990s, when they were among the best investments available. But in the past decade, big U.S. stocks have had the worst performance of nine major investment classes tracked by investment research firm Morningstar. The Standard & Poor's 500 stock index has fallen at an annualized rate of 3% a year over the past 10 years, including dividends and controlling for inflation. Long-term Treasury bonds show a gain of 5% a year during that same period, after inflation. Gold is up 10% a year and real-estate investment trusts 8% a year. The S&P 500 index itself, without adjusting for inflation and dividends, is stuck today at a level it first reached 12 years ago, meaning it has gone nowhere in more than a decade, scaring a legion of people in the process.

Reflecting their flight from risk, individual investors appear to be losing faith in an investment strategy called buying on the dips. In times of stock strength, people learn to buy stocks after a decline, when they are cheaper, because the stocks have a tendency to recover. Lately, investors have been reversing that behavior, selling on dips for fear the declines will continue. The Yale School of Management maintains an index, designed by Professor Robert Shiller, that tracks individuals' willingness to buy on dips, based on a monthly survey of wealthy investors. The index topped out in 2002. While it has moved up and down since then, it has been falling since the start of 2009.

Some investors, haunted by the continuing credit crunch and unemployment fears, are being driven to pull money out of stock funds to make up budget shortfalls. Also eating away at risk tolerance is demographics: Baby boomers are aging, making them think more about preserving their holdings' value. This is only part of the story, however: The Investment Company Institute data show lower risk tolerance among younger people, too. In surveys of mutual-fund owners, the ICI found that just 30% said in 2009 that they were willing to take above-average or substantial risk in the stock market, down from 37% in 2008. The number willing to take only below-average risk or no risk at all rose to 20% from 14%.

Mr. Thibeaux of Alexandria, La., sold one-third of his stock mutual funds late in April at the suggestion of an investment adviser, who warned him that stocks were due for a pullback. The problem was where to put the cash. A money-market fund at his mutual-fund company or a short-term certificate of deposit at his bank would yield almost nothing, he says. He finally decided simply to pay off the mortgage on a second home, on which he was paying 5% interest. "I think there is no investment strategy now except to buckle up and hope that you don't get hit too hard," Mr. Thibeaux says.

Long-term investors have been showing a distinct change in behavior since 2008. Jay Pestrichelli, who monitors client behavior at online brokerage firm TD Ameritrade, has noted a change in the traditional buy and hold strategy. "People who once made few changes to their accounts have begun trading more frequently," he says. He saw the trend especially clearly on May 6, when there was an uptick of selling.

"A higher percentage of our trading was coming from our longer-term investor base," he says. People who might log into their accounts regularly, but not necessarily trade, were selling heavily that day, he says. "The next day, those clients were all buying back in," he says, often losing money on a trade where they had sold low and bought higher. "To see that kind of a move in such a short period of time, it certainly can shake their trust."

James Rotenstreich, a businessman in Birmingham, Ala., says the May flash crash damaged his confidence in stocks as a store of wealth. Mr. Rotenstreich has received offers for some real estate he owns in the Birmingham area, but so far has been reluctant to sell, he says, in part because he doesn't know what he would do with the money. He notes that corporate bonds and other alternatives also suffered severely in the market decline.

Reflecting on his options, he says that if he sold the real estate, "I really think I would put it in the bond market. So maybe I have lost some faith in the future of the stock market." Some investment advisers are telling clients that, for long-term investors, this summer will turn out to have been a great time to buy stocks on the cheap. So far, not many clients are listening.

Deutschland über alles does not mean a trickledown recovery in EMU

by Ambrose Evans-Pritchard - Telegraph

Germany is sizzling, for now. Manufacturing output grew at an annual rate of 26pc from March to May. Mercedes, BMW, and Audi are ramping up overtime. Economic growth in the second quarter may top 5.2pc. Jean-Claude Trichet, head of the European Central Bank, last week cited thisWirtschaftswunder as evidence of durable recovery in Europe. It is no such thing. The OECD's leading indicators for June rolled over in Italy and France, as well as China and India. The IMF expects Spain's economy to contract by 0.4pc this year. It has lowered its forecast for the eurozone from 1.5pc to 1.3pc in 2011.

"Downside risks to the recovery have risen sharply," it said. The ECB is barely on speaking terms with the IMF – the "Inflation Maximizing Fund" as it was dubbed in a Bundesbank memo. "The IMF has not caught up to the reality in Europe," said ECB über-hawk Jürgen Stark on Friday. Beware, this is the same insular ECB that raised rates in July 2008 on the eve of the Lehman crisis when half of Europe was already in recession, mistaking the deflationary oil spike for an incipient 1970s inflation spiral. Can one ever trust their judgment again?

Yes, Germany is on the cusp of EMU "outperformance", but that is more curse than cure for Club Med laggards. Germany is benefiting from a currency that is as misaligned as China's yuan, though this mercantilist advantage is disguised within Europe's monetary union. Crudely, Germany is doing to Spain, Italy, and increasingly France, what China has been doing to the rest of the world – but more so – by holding down its exchange rate. In Europe's case, this captive arrangement is written into EU Treaty law. This is not a German conspiracy. The German people never desired the euro. The countries that are now caught in the EMU trap were the ones that foisted the project onto Berlin.

Be that as it may, we now have an untenable socio-strategic situation in which German unemployment has been falling for 12 months in a row to 7.5pc, while Spain's unemployment has vaulted upwards to just under 20pc. This immense gap – with everything it implies about the state of a society – has surfaced in little over two years. The delayed effect of German wage discipline over the years has at last hit EMU with volcanic force. The same time-lag is underway in Spain with opposite effect as the property slump grinds deeper. Wishful thinking lingers, but the harsh truth is that the Spain's housing crash has barely begun. The Madrid consultancy RR de Acuna sees an implicit overhang of 1.6m housing units. It will take six years to clear.

By cruel contrast, Hans Werner Sinn from Germany's IFO Institute said his country is on the cusp of a property boom. "Germany is the winner of this crisis," he said. This contrast will become even crueller because Germany is also benefiting from a devalued euro against the dollar, yuan, yen, rouble, and even sterling (lately). The euro has fallen by 20pc or so. This has rescued Germany's 80,000 strong solar industry – for example – from annihilation by Chinese competitors. The EMU effects of a weak euro are asymmetric. Germany's export machine is highly-geared to Asia and America. Spain has low gearing.

With a closed economy, it would require a euro at 80 cents to enjoy much relief. We are seeing a mirror-image of 2008 when ECB hawks drove the euro to $1.60 against the dollar. That episode led to a sharper fall of industrial output in Germany than in Spain or France. Besides, Germany makes products for the rich, a profitable niche in a world of asset bail-outs. Statistically, the rich are better off now than two years ago. Mercedes enjoyed its best month ever in June. Sales in the US jumped 25pc from a month earlier. The S-Class model was up 106pc. Meanwhile, a million people have dropped out of the US labour force in the last two months alone. Labour arbitrage under globalisation has not been good for Western workers.

The Gini Coefficient measuring income inequality is at or near all-time high in almost every Western country. Democracy will correct this as the political pendulum swings, but for now Germany is the ultimate Gini export play. A vibrant Germany must, in the end, lift Spain and Italy as German firms source contracts their way, but process will be painfully slow. The risk is that the North-South gap widens further before the stimulus trickles down. Much political mayhem can occur in the meantime. The ECB's German members are not inclined to do any favours for Club Med. Dr Stark swept aside the IMF's call for "scaling up" ECB bond purchases after buying €59bn (£49bn) of Greek and Iberian bonds so far. "If the situation improves further there is not a reason any more to continue with this programme," he said. I

f so, he dooms Spain to deeper depression. The IMF is frankly in a muddle as well on the big picture. Its World Economic Outlook said the surpluses of Germany, China, and Japan, will rise from $586bn (£377bn) last year to $758bn by 2015, perpetuating the imbalances that led to the credit crisis. Brian Reading from Lombard Street Research said that if this occurs, it assures a global slump because the deficit states of the Anglosphere and Club Med cannot keep the game going by adding further debt. They must retrench, and therefore global demand must implode.

The IMF evades the conclusions of its own logic. As for Berlin, it eyes the world through a provincial lens, as a pseudo-morality tale. This childish view did not matter as long as market forces could impose a currency revaluation on Germany every few years to keep relations with the rest of Europe in kilter. It matters a great deal now. EMU has shut the escape valve.

European Banks Poised to Win Reprieve on Basel III Capital Rules

by Yalman Onaran and Simon Clark - Bloomberg

European banks, rattled by investor uncertainty about their ability to withstand a sovereign-debt crisis, are poised to win a reprieve in Basel, Switzerland, this week as regulators from 27 countries shape new capital rules.

A push to water down stringent standards proposed last year by the Basel Committee on Banking Supervision, and to allow more time to implement them, is led by France and Germany, according to bankers, regulators and lobbyists involved in the talks. Representatives from the U.S. and the U.K., who have sought to rein in risk-taking, are willing to compromise on how capital is defined to reach an agreement at a committee meeting that begins tomorrow, the people said.

Another concession may involve granting transition periods of up to 10 years to ease concerns of some member countries that their banks and economies won’t be able to bear the burden of tougher capital requirements until a recovery takes hold. As a result, the amount of capital European banks will be forced to raise in the next two years won’t be as much as investors fear.

"Politicians in France and Germany are worried about the impact of the rules on their economies," said Chris Bates, a regulatory lawyer at Clifford Chance LLP in London. "Basel has managed to bring diverging banking systems and economies together. It’s more than just a capital regime. It’s a showcase of global cooperation. So the U.S. and the U.K. cannot let it break down."

G-20 Request

The 36-year-old Basel committee, a body of central bankers and regulators that sets capital standards for banks worldwide, was asked by the Group of 20 nations to draft new rules after the worst financial crisis in 70 years caused firms to write off $1.8 trillion. G-20 leaders urged the committee to improve the quantity and quality of bank capital, strengthen liquidity requirements and discourage excessive leverage. They set a deadline of December for making the rules and originally gave countries until the end of 2012 to implement them.

Three months ago, European leaders and finance ministers, including those from Germany and France, were as adamant as their American and British counterparts in pushing back against banks’ objections to proposed rules that UBS AG estimated could force banks to raise $375 billion of capital, according to the regulators and bankers, who asked not to be identified because they weren’t authorized to speak. Fifty-five percent of that would have to be raised by European banks, UBS said. Then Greece’s debt woes unnerved investors, making European leaders more receptive to what the banks were saying, according to the people.

‘Wiggle Room’

At their meeting in Toronto last month, G-20 leaders hinted at delays. While continuing to urge stricter capital and liquidity standards, they said implementation could take economic conditions of member states into account. "The challenge of the eurozone crisis clearly played into the Toronto document," said Barbara Matthews, a former bank lobbyist and now managing director of BCM International Regulatory Analytics LLC in Washington. "It gave wiggle room on implementation."

Even if they’re softened and delayed, the new capital rules, known as Basel III, will force banks to take fewer risks and be better capitalized, said Paul Miller, an analyst for FBR Capital Markets Corp. based in Arlington, Virginia. "There’s a misperception out there that Basel III isn’t going to happen, or if it does it will be so watered down it won’t matter," Miller said. "Even with the tweaks in the next few months, they’ll come up with a pretty strong framework."

Fixing Basel II

The Basel III proposal attempts to fix the shortcomings of an earlier revision, known as Basel II, which was initiated by lenders in the late 1990s and lowered capital requirements by as much as 29 percent for some banks. The new rules would tighten control of what goes into the banks’ calculation of risk, redefine what counts as capital and impose higher charges against holdings such as derivatives.

The committee is expected to decide on the definition of capital this week and defer issues such as capital ratios until its meetings in September and October, according to members.

One part of the definition would exclude minority interests that banks hold in other financial institutions when calculating common equity on the theory that they can’t readily withdraw the capital. Many European lenders, which have lobbied against the rule, have non-controlling stakes in emerging-market banks that would no longer count as the highest level of capital, while the assets of the subsidiaries would have to be included in the banks’ risks.

BNP Paribas, HSBC

The change would have the largest impact on European lenders of all the proposed capital rules, UBS said in a March report. BNP Paribas SA, France’s largest bank by assets, would see its capital lowered by $10.7 billion, more than any lender, if it couldn’t count minority interests, analysts at JPMorgan Chase & Co. wrote in February. London-based HSBC Holdings Plc would have its capital reduced by $6.9 billion, and Societe Generale SA, the third-biggest French bank, $4.7 billion.

European banks are likely to win a concession on the minority-stakes rule, according to the people involved in the talks. One possible compromise would allow a bank to count part of its stake in relation to the risk the capital is supposed to cover at the entity in which it invested, the people say. The fight over whether to count minority stakes comes as the Basel committee is trying to counter an attack by bankers who have said that harsh rules come with costs. Investors will pay with lower returns from owning securities in their firms, and Main Street will suffer as economic growth and lending slow and fewer jobs are created, bankers say.

‘Never Free’

A study released in June by the Institute of International Finance, which represents more than 375 financial companies, said the regulations could erase 3.1 percent of gross domestic product in the U.S., the euro region and Japan by 2015. About 9.7 million fewer jobs could be created over the five-year period than would otherwise be the case, the IIF said. Regulation is "never free," said Bank of New York Mellon Corp. Chief Executive Officer Robert Kelly, who visited London and Brussels in June to meet lawmakers and regulators with the Financial Services Roundtable, a Washington-based industry group. "There has to be some impact on growth and jobs."

The Basel committee, whose members have touted the benefits of financial stability, is preparing its own economic impact study with the help of the Bank for International Settlements in Basel and the International Monetary Fund. "Preliminary results do not point to a growth problem coming from the regulation," Jaime Caruana, general manager of the BIS, said in Basel on June 28. "On the contrary, it would support resilience relatively rapidly."

The Basel committee may publish the study later this month or in August, according to a person with knowledge of the matter. The report is expected to show an impact on economic growth of about one-third what the IIF calculated, another person familiar with the research said. U.S. regulators also have been dubious about the banks’ analysis. The Federal Reserve, which is collecting data from banks for a separate impact study, has rejected some of the lenders’ assumptions and asked for changes, according to people familiar with the discussions.

The Basel committee plans to announce its rules by the time G-20 leaders gather in Seoul in November. In addition to defining capital, the group needs to determine three ratios before then: one on common equity as a percentage of risk- weighted assets; one involving Tier 1 capital, which includes securities that could help a lender cover unexpected losses; and one on Tier 2 capital, which incorporates a broader range of securities that would protect depositors and creditors in case of insolvency.

Defining Capital

Banks currently need to hold capital equal to a minimum of 8 percent of risk-weighted assets. Half of that must be Tier 1 and half of the Tier 1 needs to be common stock. The Basel committee might triple the common ratio requirement and double Tier 1, FBR’s Miller estimates. How the committee defines what counts as capital is as important as what the ratios are. In addition to the fight over whether to exclude minority stakes, there is a debate over deferred tax assets, past losses that lenders use to offset tax charges in future years.

The proposed Basel rules would prevent banks from counting these assets as part of their core capital. Japanese banks, which rely on deferred tax assets more than their counterparts in Europe and the U.S., are leading the campaign to block the exclusion, according to people involved in the talks. While the proposal might not change, the Basel committee may accept a phase-in period of between 5 and 10 years, the people say.

Liquidity Requirements

The committee may also relax the implementation of other rules by giving national regulators two years from the beginning of 2012 to come up with plans to put the regulations into effect, the people involved in the discussions say. Each part of the proposal might have its own time horizon. Final versions of some Basel rules, including new liquidity requirements for how much cash banks need to hold, may not be agreed upon before the November G-20 meeting.

A liquidity coverage ratio is designed to ensure that all of a bank’s liabilities coming due in a month can be paid with cash and other assets, such as Treasuries, that can be sold easily for cash. A net stable funding ratio extends the same concept to a year, incorporating other holdings, such as short- term loans and stocks. Banks objected to the long-term rule, which could result in new debt issuance of $5.4 trillion, Barclays Plc analysts estimated in June. The target date for publishing the rule may be pushed back to the middle of next year, four committee members said.

Counterparty Risk

Another source of disagreement between European and U.S. regulators is a change that would increase capital charges on banks to cover counterparty credit risk, or the likelihood of trading partners going bust, the people said. That portion of Basel III would create a buffer against the kind of danger posed by American International Group Inc. during the credit crisis. U.S. and European banks thought they had hedged their mortgage investments through derivatives contracts with AIG, which couldn’t keep up with increased cash demands as the values of the bonds declined. The U.S. government bailed out the insurer, concerned that its collapse would bring down banks that bought the derivatives.

The Basel committee probably won’t make a decision about counterparty risk this week, deferring the issue until October, members say. At least one said he expected the matter will be delayed to next year. Issues that can’t be resolved by the Basel committee may be settled by the G-20 leaders in November, members say. "The regulatory space has been far more politicized than I’ve ever seen it," said BCM’s Matthews, who has been involved with Basel rulemaking for two decades. "Heads of state care, have opinions and are aware of decisions at very granular levels."

One proposal European banks and regulators tried to get rid of -- and that U.S. Treasury Secretary Timothy F. Geithner advocated -- has survived and made it into the Toronto G-20 statement. That’s a plan to cap bank leverage by setting a ratio of assets to capital. While current Basel rules allow banks to assign weights to assets based on their risks, the leverage ratio would look at all assets without a risk assessment. European banks appear more highly levered than their U.S. counterparts partly because U.S. accounting rules allow more assets to be kept off balance sheets than European standards do. The two systems differ on which types of securitizations are included on the books and how derivatives contracts are netted.

Lower Returns

As envisioned in the Basel proposal, the leverage ratio will initially be used to provide guidance to national regulators in their assessments of banks’ soundness. Only later, after accounting differences between countries are resolved, would it become a requirement. BNY Mellon’s Kelly said the original Basel proposals would have forced some banks’ return on equity, a measure of profitability, to mid-single digits. "If that was true, then they effectively become government utilities, because you couldn’t really raise capital in the private markets after that," he said.

Bankers worried about maintaining existing returns may be missing the point, according to Basel committee Chairman Nout Wellink, who is also president of the Dutch central bank. The purpose of the new rules is to change the business model of banks, he said at an IIF meeting in Vienna last month. "More stable, less leveraged banks would raise average ratings, improve the terms on which banks could raise funds, and lower the required return on equity," Wellink said.

That view was reinforced in the Bank for International Settlements’ latest annual report, published June 28. "High shareholder returns in the sector were unsustainable because they were generated by high leverage and risk-taking that proved to be unmanageable in a period of stress," the report said. "Lower returns on equity could actually be a desirable outcome for the long-term investor as well as for the economy at large."

Secret gold swap has spooked the market

by Garry White and Rowena Mason - Telegraph

It takes a lot to spook the solid old gold market. But when it emerged last week that one or more banks had lent 380 tonnes of gold to the Bank of International Settlements in return for foreign currencies, there was widespread surprise and confusion. The news that a mystery bank has just pawned the family jewels gave traders a jolt – nervous about the sudden transfer of almost 20pc of the world's annual gold production and the possibility of a sell-off.

In a tiny footnote in its annual report, the bank disclosed its unusually large holding of gold, compared with nothing the year before. The disclosure was a large factor in the correction of the gold price this week, which fell below $1,200 for the first time in more than a month. Concerns hinged on whether the BIS could potentially sell on this vast cache of bullion in the event of a default, flooding the market with liquidity. It appears to have raised $14bn for whoever's been doing the swapping – small fry on the currency markets, but serious liquidity in the gold market. Denominated in euros, gold has fallen 8pc since the beginning of the month and is now trading at a seven-week low of €937 per troy ounce.

The big gold exchange traded funds (ETFs) – having peaked at record inflows in May – have also been showing net outflows over the past few days. Meanwhile, economists and gold market-watchers were determined to hunt down which bank is short of cash – curious about who is using their stash of precious metal for what looks suspiciously like a secret bailout. At first it looked like the BIS was swapping gold with a troubled central bank. After all, the institution is the central bankers' bank and its purpose to conduct transactions with national monetary authorities.

Central banks in the troubled southern zone of Europe were considered the most likely perpetrators. According to the World Gold Council, central banks in Greece, Spain and Portugal held 112.2, 281.6 and 382.5 tons of gold respectively in June – leading analysts to point fingers at Portugal, or a combination of the three. But Edel Tully, an analyst from UBS, noted that eurozone central banks would be severely limited with what they could do with the influx of extra cash – unable to transfer it straight to governments or make use of the primary bond markets. She then listed the only other potential monetary authorities with enough gold as the US, China, Switzerland, Japan, Russia, India and Taiwan – and the International Monetary Fund.

This led to musings that the counterparty was the IMF, making sense because the lender of last resort is historically prone to cash shortages and has been quietly selling off gold in the first half of the year. Renowned gold expert Jim Sinclair adopted this explanation. The panic came when people mistook a lease for a swap, he argues. Far from being a big release of gold into the market, it is simply a commercial arrangement between the IMF and BIS with a favourable rate of interest paid for the foreign currency. "Gold swaps are usually undertaken by monetary authorities," he writes on his industry blog, MineSet.

"The gold is exchanged for foreign exchange deposits with an agreement that the transaction be unwound at a future time at an agreed price. "The IMF will pay interest on the foreign exchange received. Historically swaps occur when entities like the IMF have a need for foreign exchange, but do not wish to sell the gold. In this case, gold is a leveraging device for needed currency to meet requirements. "The many reports that characterise the large IMF gold swap as a sale of gold into the markets do not understand the difference between a swap and a lease." However, the day after original reports about the swaps, BIS emailed a statement saying that the swaps had not been conducted with monetary authorities but purely with commercial banks.

This did nothing to quell the sense of mystery surrounding the deal or deals. It is almost inconceivable that a single commercial bank could have accumulated so much gold alone. And cynics have suggested that the whole affair still looks like a secretive European bailout that a single country wants to keep quiet. In this case, one or more of the so-called bullion banks – which act as wholesale market-makers and include Goldman Sachs, Deutsche Bank, JP Morgan, HSBC, Barclays, UBS, Societe Generale, Mitsui and the Bank of Nova Scotia – would have agreed to act on behalf of a monetary authority.

This would add an extra layer of anonymity. "So the BIS swaps look like a tripartite transaction," writes Adrian Douglas of the Gold Anti-Trust Association. "The commercial bank or banks made a swap with a central bank or banks and then the commercial bank or banks made a swap with the BIS." Analysts for Commerzbank note that in the meantime, "The price of gold is tending weaker at present."

Baltic Dry Index still falling

The Baltic Dry Index, a measure of commodity shipping costs, has fallen for the longest period in nine years, due to lower volumes of iron ore being shipped to China. Surplus steel means manufacturers are relying on stockpiles, rather than shipping in iron ore from abroad. The index of freight rates on international trade routes fell 38 points, or 2pc, to 1,902 points on Friday in its 31st straight decline. Charter rates for all types of ships fell.

Buyers angry at 'excessive' cocoa speculation

European cocoa buyers are so concerned about potential speculation in the market that they have written to the London commodities exchange threatening to move their trade to America. Talks between industry participants and Liffe, the London exchange operator, will take place this week, following concerns about the price spike in June. Futures hit a 32-year high, amid lower production due to diseased crops in Africa and higher demand. Those who signed the letter claim there has been excessive speculation by hedge funds and want greater transparency about who is buying what and how much.

Support for European spending cuts strong

by Tony Barber - Financial Times

European governments have solid public support, at least for now, for the spending cuts they are making in an effort to boost economic recovery, according to the latest Financial Times/Harris opinion poll. The survey also indicates that a majority of people in the European Union’s five largest countries disagree with the decision of governments to let their budget deficits rise in order to combat the financial crisis that erupted in 2008. The poll’s results point to a fiscal conservatism among the European public that contrasts with the eagerness with which most governments ran up high deficits to protect jobs and living standards as the crisis unfolded.