Christmas tree, Madison Square, New York City

Ilargi: Many people today feel happy and positive when they look at the stock markets, because they think these reflect the real economy, and since the markets are up, things must have changed for the better in the past year.

But they haven't, not below the surface. It's all veneer and no substance. What actually has happened is that -virtually- no debt has been paid off in our economies, in fact we’ve added trillions of dollars more in debt. What is different from a year ago is that a huge part of the old debt and all of the new debt has been transferred to the public, and away from private business, in particular financial institutions (and, to an extent, carmakers).

So it comes down to the fact that people feel happy for being deeper in debt, and quite a bit deeper. Being the humans we are, we focus on the short term gratification which can be found in the Dow and a whole slew of increasingly fabricated numbers and government reports, while we conveniently ignore the enormous increases in debts, both public and private, that we will have to pay off down the line.

But, you say, it's not as bad as it may look, because when the crisis is over, we will return to growth, and that will take care of the debt. That and shrewd dollar-inflation strategies by the wizards at the Fed and Treasury.

Really? What if the crisis lasts, let's say, ten years? All that needs to happen for that is for home prices to keep falling, or even stagnate. And that seems a near certainty.

The US has no private mortgage market left, or even a viable housing market. Neither do Canada, Britain, Holland and many other countries for that matter. Homes are sold and mortgages approved only because the state takes them off the lenders' hands and books the minute the deals are closed. The loans are then securitized and sold on to, in America's instance, the central bank. In other words, all of the risk for all of the entire loans processed in this fashion lies squarely with the taxpayer.

And that is not a good thing if prices keep dropping. When unemployment won't come down. When governments start raising taxes because sovereign debt goes through the various rooftops.

The main problem's not even paying off the principal of the debt. That won't start happening for years to come, if ever. It’s paying the interest on the debt that will become the most immediate headache.

In a world where money is lent at record low near zero interest rates, Britain pays close to 4% on its 10-year Gilts, the UK Treasury bonds. Why? Look here:

[..] Britain is nearing the eye of the storm as the Bank of England starts to unwind quantitative easing. "The Bank has bought more gilts over the last nine months than the Government has issued. It has magically eradicated the cost of financing the deficits, but this is going to twist dramatically the other way in early 2010. Markets know this. They are demanding a risk premium on sterling."

Many other nations face the same issues. And that includes the US. Borrowing money will become dramatically more expensive. It’s the market mechanism at work in its full glory. The global supply of sovereign bonds is way bigger than the demand.

Talking about US Treasuries, Canadian investor Eric Sprott has been trying to figure out who bought them in 2009. In a report entitled Is it all just a Ponzi scheme?, Sprott and David Franklin suggest that it's impossible to find who was the second largest buyer. Of the $1.885 trillion dollars in public debt the US added in 2009, $704 billion (annualized) was bought by "Other Investors", a collection of buyers they find defined in the Federal Reserve Flow of Funds Report as the "Household Sector". the $704 billion is 35 times more than this sector bought in the prior year, 2008, according to Sprott and Franklin. They phrase it like this:

Amazingly, we discovered that the Household Sector is actually just a catch-all category. It represents the buyers left over who can't be slotted into the other group headings. For most categories of financial assets and liabilities, the values for the Household Sector are calculated as residuals. That is, amounts held or owed by the other sectors are subtracted from known totals, and the remainders are assumed to be the amounts held or owed by the Household Sector. To quote directly from the Flow of Funds Guide,"For example, the amounts of Treasury securities held by all other sectors, obtained from asset data reported by the companies or institutions themselves, are subtracted from total Treasury securities outstanding, obtained from the Monthly Treasury Statement of Receipts and Outlays of the United States Government and the balance is assigned to the household sector."

So to answer the question - who is the Household Sector? They are a PHANTOM. They don't exist. They merely serve to balance the ledger in the Federal Reserve's Flow of Funds report.

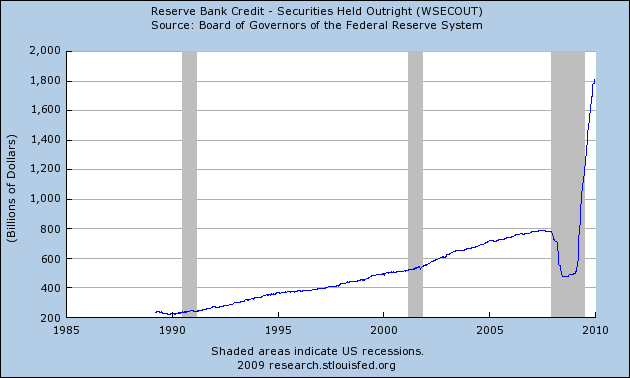

Our concern now is that this is all starting to resemble one giant Ponzi scheme. We all know that the Fed has been active in the market for T-bills. [..] they bought almost 50% of the new Treasury issues in Q2 and almost 30% in Q3. It serves to remember that the whole point of selling new US Treasury bonds is to attract outside capital to finance deficits or to pay off existing debts that are maturing. We are now in a situation, however, where the Fed is printing dollars to buy Treasuries as a means of faking the Treasury's ability to attract outside capital. If our research proves anything, it's that the regular buyers of US debt are no longer buying, and it amazes us that the US can successfully issue a record number Treasuries in this environment without the slightest hiccup in the market.

Translation: the Sprott report accuses the US Treasury and/or the Fed of buying US treasuries themselves, in much larger numbers than they acknowledge. Wonder what the Chinese will make of that. Then again, they may already know or suspect this. At this point, we should be wondering also what US taxpayers think of this. Alas, they've been lulled into another dream of growth and greatness from which they won't wake until it makes no difference anymore what they think.

The Christmas Eve zinger for 2009 (in the tradition of the Federal Reserve Act being pushed through the House exactly 96 years ago) is that the Treasury in a last-minute December 24 announcement has stated that is has removed any and all caps on financial support for Fannie and Freddie. If they weren't all yours before, with all the trillions in debt they carry, America, they sure are now. It's a fine American political tradition, inflicting the worst hurt when nobody‘s looking.

2009 has been the year in which "Moral Hazard" lost its meaning and then disappeared altogether, precisely at the moment when that meaning could have become obvious to everyone. Well done by the media. No morals, no hazard, right?

2010 will be the year of the Debt. It will bury entire nations like Greece and Ukraine, and states like California, and threaten to topple scores more. China will turn out to have built a thousand time more useless real estate than Dubai. And the US and other "rich" governments will need to choose between additional bail-outs, which this time will turn out to be even much more expensive, or come clean with their people and accept certain and instant political defeat.

Yes sir, of course ma’am, one round of bail-outs coming up.

They’re on the house.

Ilargi: The Automatic Earth Christmas and New Year’s fund (see top of page, left hand side) humbly and gratefully accepts your kind donations in the name of all the millions in need of spiritual and practical enlightenment.

Is it all just a Ponzi scheme?

by: Eric Sprott and David Franklin

In our May/June Markets at a Glance, "The Solution is the Problem", we discussed how much debt the US government would need to issue in order to balance the budget for fiscal 2009. We calculated they would need to sell $2.041 trillion in new debt - or almost three times the new debt that was issued in fiscal 2008. As a thought experiment, we separated all the various US Treasury owners and asked our readers whether each group could afford to increase their 2009 treasury purchases by 200%. In the end, we surmised that most groups couldn't, and prepared our readers for the worst.

Almost seven months later, however, nothing particularly bad has happened on the US debt front. There have been no failed auctions, no sovereign defaults, no downgrades of debt and no significant increase in rates not so much as a hiccup in the treasury market. Knowing what we discussed this past June, we have to ask how it all went so smoothly. After all it was pretty obvious there wasn't enough buying power to satisfy the auctions under 'normal' circumstances.

In the latest Treasury Bulletin published in December 2009, ownership data reveals that the United States increased the public debt by $1.885 trillion dollars in fiscal 2009. So who bought all the new Treasury securities to finance the massive increase in expenditures? According to the same report, there were three distinct groups that bought more than they did in 2008. The first was "Foreign and International Buyers", who purchased $697.5 billion worth of Treasury securities in fiscal 2009 representing about 23% more than their respective purchases in fiscal 2008. The second group was the Federal Reserve itself. According to its published balance sheet, it increased its treasury holdings by $286 billion in 2009, representing a 60% increase year-over-year.

This increase appears to be a direct result of the Federal Reserve's Quantitative Easing program announced this past March. Most of the other identified buyers in the Treasury Bulletin were either net sellers or small buyers in 2009. While the Q4 data is not yet available, the Q1, Q2 and Q3 data suggests that the State and Local governments and US Savings Bonds groups will be net sellers of US Treasury securities in 2009, while pension funds, insurance companies and depository institutions only increased their purchases by a negligible amount.

So who was the third large buyer? Drum roll please,... it was "Other Investors". After purchasing $90 billion in 2008, this group has purchased $510.1 billion of freshly minted treasury securities so far in the first three quarters of fiscal 2009. If you annualize this rate of purchase, they are on pace to buy $680 billion of US treasuries this year - or more than seven times what they purchased in 2008. This is undoubtedly the group that made the US deficit possible this year.

But who are they? The Treasury Bulletin identifies "Other Investors" as consisting of Individuals, Government-Sponsored Enterprises (GSE), Brokers and Dealers, Bank Personal Trusts and Estates, Corporate and Non-Corporate Businesses, Individuals and Other Investors. Hmmm. Do you think anyone in that group had almost $700 billion to invest in the US Treasury market in fiscal 2009? We didn't either.

To dig further, we turned to the Federal Reserve Board of Governors Flow of Funds Data which provides a detailed breakdown of the owners of Treasury Securities to Q3 2009. Within this grouping, the GSE's were small buyers of a mere $5 billion this year; Broker and Dealers were sellers of almost $80 billion; Commercial Banking were buyers of approximately $80 billion; Corporate and Non-corporate Businesses, grouped together, were buyers of $11.6 billion, for a grand net purchase of $16.6 billion. So who really picked up the tab?

To our surprise, the only group to actually substantially increase their purchases in 2009 is defined in the Federal Reserve Flow of Funds Report as the "Household Sector". This category of buyers bought $15 billion worth of treasuries in 2008, but by Q3 2009 had purchased a whopping $528.7 billion worth. At the end of Q3 this Household Sector category now owns more treasuries than the Federal Reserve itself.

So to summarize, the majority buyers of Treasury securities in 2009 were:

- . Foreign and International buyers who purchased $697.5 billion.

- . The Federal Reserve who bought $286 billion.

- . The Household Sector who bought $528 billion to Q3 which puts them on track purchase $704 billion for fiscal 2009.

These three buying groups represent the lion's share of the $1.885 trillion of debt that was issued by the US in fiscal 2009.

We must admit that we were surprised to discover that "Households" had bought so many Treasuries in 2009. They bought 35 times more government debt than they did in 2008.

Given the financial condition of the average household in 2009, this makes little sense to us. With unemployment and foreclosures skyrocketing, who could afford to increase treasury investments to such a large degree? For our more discerning readers, this enormous "Household" investment was made outside of Money Market Funds, Mutual Funds, ETF's, Life Insurance Companies, Pension and Retirement funds and Closed-End Funds, which are all separate reporting categories. This leaves a very important question - who makes up this Household Sector?

Amazingly, we discovered that the Household Sector is actually just a catch-all category. It represents the buyers left over who can't be slotted into the other group headings. For most categories of financial assets and liabilities, the values for the Household Sector are calculated as residuals. That is, amounts held or owed by the other sectors are subtracted from known totals, and the remainders are assumed to be the amounts held or owed by the Household Sector. To quote directly from the Flow of Funds Guide,"For example, the amounts of Treasury securities held by all other sectors, obtained from asset data reported by the companies or institutions themselves, are subtracted from total Treasury securities outstanding, obtained from the Monthly Treasury Statement of Receipts and Outlays of the United States Government and the balance is assigned to the household sector."

So to answer the question - who is the Household Sector? They are a PHANTOM. They don't exist. They merely serve to balance the ledger in the Federal Reserve's Flow of Funds report.

Our concern now is that this is all starting to resemble one giant Ponzi scheme. We all know that the Fed has been active in the market for T-bills. As you can see from Table A, under the auspices of Quantitative Easing, they bought almost 50% of the new Treasury issues in Q2 and almost 30% in Q3. It serves to remember that the whole point of selling new US Treasury bonds is to attract outside capital to finance deficits or to pay off existing debts that are maturing. We are now in a situation, however, where the Fed is printing dollars to buy Treasuries as a means of faking the Treasury's ability to attract outside capital. If our research proves anything, it's that the regular buyers of US debt are no longer buying, and it amazes us that the US can successfully issue a record number Treasuries in this environment without the slightest hiccup in the market.

Perhaps the most striking example of the new demand dynamics for US Treasuries comes from Bill Gross, who is co-chief investment officer at PIMCO and arguably one of the world's most powerful bond investors. Mr. Gross recently revealed that his bond fund has cut holdings of US government debt and boosted cash to the highest levels since 2008. Earlier this year he referred to the US as a "ponzi style economy" and recomended that investors front run Uncle Sam and other world governments into government debt instruments of all forms. The fact that he is now selling US treasuries is a foreboding sign.

Foreign holders are also expressing concern over new Treasury purchases. In a recent discussion on the global role of the US dollar, Zhu Min, deputy governor of the People's Bank of China, told an academic audience that "The world does not have so much money to buy more US Treasuries." He went on to say, "The United States cannot force foreign governments to increase their holdings of Treasuries. Double the holdings? It is definitely impossible."

Judging from these statements, it seems clear that the US cannot expect foreigners to continue to support their debt growth in this new economic environment. As US consumers buy fewer foreign goods, there are less US dollars available for foreigners to purchase future Treasury securities. Foreigners are the largest source of external capital that can be clearly identified in US Treasury data. If their support wanes in 2010, the US will require significant domestic support to fund future debt issuances. Mr. Gross's recent comments suggest that their domestic support may already be weakening.

As we have seen so illustriously over the past year, all Ponzi schemes eventually fail under their own weight. The US debt scheme is no different. 2009 has been witness to spectacular government intervention in almost all levels of the economy. This support requires outside capital to facilitate, and relies heavily on the US government's ability to raise money in the debt market. The fact that the Federal Reserve and US Treasury cannot identify the second largest buyer of treasury securities this year proves that the traditional buyers are not keeping pace with the US government's deficit spending. It makes us wonder if it's all just a Ponzi scheme.

Treasury removes cap for Fannie and Freddie aid

The government has handed its ATM card to beleaguered mortgage giants Fannie Mae and Freddie Mac. The Treasury Department said Thursday it removed the $400 billion financial cap on the money it will provide to keep the companies afloat. Already, taxpayers have shelled out $111 billion to the pair, and most analysts hadn't expected the companies to hit the limit. Treasury Department officials said it will now use a flexible formula to ensure the two agencies can stand behind the billions of dollars in mortgage-backed securities they sell to investors. The formula will provide the companies with a sufficient cushion based on projected losses over the next three years.

By making the change before year-end, Treasury sidestepped the need for an OK from a bailout-weary Congress. But the timing of the announcement on a traditionally slow news day raised eyebrows. "The companies are nowhere close to using the $400 billion they had before, so why do this now?" said Bert Ely, a banking consultant in Alexandria, Va. "It's possible we may see some horrendous numbers for the fourth quarter and, thus 2009, and Treasury wants to calm the markets."

Fannie Mae and Freddie Mac provide vital liquidity to the mortgage industry by purchasing home loans from lenders and selling them to investors. Together, they own or guarantee almost 31 million home loans worth about $5.5 trillion, or about half of all mortgages. Without government aid, the firms would have gone broke, leaving millions of people unable to get a mortgage. The biggest headwind facing the housing recovery has been the rise in foreclosures as unemployment remains high. Treasury said its latest move could allow Fannie and Freddie to play a bigger role in restructuring mortgages for troubled borrowers.

Treasury officials will provide an updated estimate for Fannie and Freddie losses in February when President Barack Obama sends his 2011 budget to Congress. Though the administration has yet to disclose its long-term plans for the two companies, they are unlikely to return to their former power and influence. The news followed an announcement Thursday that the CEOs of Fannie and Freddie could get paid as much as $6 million for 2009, despite the companies' dismal performances this year.

Fannie's CEO, Michael Williams, and Freddie CEO Charles "Ed" Haldeman Jr. each will receive $900,000 in salary, $3.1 million in deferred payments next year and another $2 million if they meet certain performance goals, according to filings with the Securities and Exchange Commission. The pay packages were approved by the Treasury Department and the Federal Housing Finance Agency, which regulates Fannie and Freddie. That pay is far less than what their predecessors earned. Former Fannie CEO Daniel Mudd received $10.2 million in 2008 and former Freddie CEO Richard Syron pocketed $13.1 million. Both execs were ousted when federal regulators seized the companies in September 2008. The federal government blocked exit packages for the pair worth up to $24 million.

The chief executives' pay could spark new criticism about the government's numerous bailouts, but that may be unfounded, said Mark Borges, principal with management consulting firm Compensia. Haldeman and Williams each could command between $5 million and $10 million in a similar position in the private sector, Borges estimated, and without the notable challenges and public scrutiny they face at these companies. "I doubt too many people would look at these jobs and say, 'Gosh, I would love to go there for my next career move,'" Borges said. "The government is getting top notch executives to solve problems that are not easy to solve." The bulk of their pay is also not guaranteed, Borges said, so these executives can't pocket and run and must meet certain long-term goals or risk giving some of it back.

Freddie Mac's board sets the performance goals for the chief executive, which won't be disclosed until next year. Fannie Mae's filing outlined its corporate goals including "being a recognized leader in the housing recovery," "protecting taxpayers," and "managing risk more effectively." Fannie Mae and Freddie Mac declined to offer further details on CEO performance goals.

Public anger over Wall Street pay boiled over earlier this year. In response, the Obama administration imposed pay curbs on banks that received government bailouts. All the major banks have since repaid their federal money, largely to escape caps on executive pay. Former Bank of America Corp. CEO Ken Lewis, for example, agreed to forgo his salary and bonus this year under pressure from the government. Last year, he pocketed more than $9 million in total compensation. Bank of America received $45 billion in government assistance, which it has since repaid.

Freddie Mac hired Haldeman, a former mutual fund executive, in July. At the time, the company disclosed his annual salary of $900,000 but did not disclose other incentive payments. In September, the company hired a new chief financial officer, Ross Kari, and said his pay package would be worth up to $5.5 million. Williams, formerly Fannie Mae's chief operating officer, took over as CEO in April after the first government-appointed CEO, Herbert Allison, took a job at the Treasury Department. Williams earned a base salary of $676,000 last year, plus a retention award of $260,000. Washington-based Fannie Mae was created in 1938 in the aftermath of the Great Depression. It was privatized 30 years later to limit budget deficits during the Vietnam War. In 1970, the government formed its sibling and competitor McLean, Va.-based Freddie Mac.

2010: The Year to Focus on Sovereign Debt

by David Kotok

"Whatever it is, I fear the Greeks even when they bring gifts." This is one of the English translations of Virgil’s Aeneid. It refers to the Trojan horse that Greece used to deceive Troy and gain entry into the city. "During the Depression about half the population of Oklahoma moved to California and the intelligence level in both states went up." Will Rogers, the great American commentator from Oklahoma, hatched this quip decades ago in his analysis of California’s governmental policies and its finances.

If we were writing a play on the theme of sovereign debt, we might use the following characterization. The US and the EU are the setting: two currency zones. The Fed and the ECB are the dominant members of the cast: two central banks responsible for the two currencies. Greece and California are in leading roles: two states within the two currency zones.

In the United States, California constitutes about 13% of America’s GDP. If CA were a standalone economy, it would be about the seventh largest in the world. The currency in use in California is the US dollar. The CA government determines its own budget, has its own constitution, operates an internal legal system, and decides its own state tax structure. It is also one of the 50 sovereign members of the USA and has legally bound itself to the rules promulgated in Washington, while attempting to preserve some state rights within our highly federalized legal system.

CA and most other states have a requirement to balance an annual budget. There are provisions for emergencies in many of these states, and in the coming year we expect the concept of a financial emergency to be deployed and tested in various state courts. CA recently issued "script" during a short-lived budget crisis when it ran out of cash and until its legislature passed a revised budget. That was not the first time script has been used. We do not expect it will be the last.

In the euro zone, Greece is about 3% of the GDP. It is a sovereign state (country), one of the 16 members of the euro monetary system, and one of the 27 members of the European Union. GR maintains its own budget, although it has pledged to adhere to EU budget rules, which it is currently violating along with most other members of the EU. Under present agreements, penalties will occur if GR is not making a sufficient effort to improve its fiscal situation within a year. We do not expect those penalties to be imposed on GR nor on the other EU states in difficulty. Greece has its own tax structure, constitution, and internal legal system. GR is also covered by the newly developed EU Lisbon Treaty and, like other EU member states, is gradually moving into a Europe-wide economic structure.

California and Greece are both lowly rated by the agencies that appraise the creditworthiness of sovereign debt. CA and GR are also on the top of the list of possible default candidates in their respective currency zones. That list is prepared by CMA DataVision, a service that scrutinizes credit default swap pricing in order to determine market-based assessments of default probability over the next five years. CA and GR are both poorly rated, and their scores (default probabilities) are about the same

CA is a problem for the Federal Reserve because the state is a very large part of the US economy and because it is suffering from the financial crisis and the collapse of the housing bubble. If CA defaults, it will lose access to credit markets and contract a governmental economy that is 1/7 of the US. That would be a huge blow to the nascent American economic recovery. The Federal Reserve doesn’t directly place its funds in California’s debt; the Fed does function as the central banker for nearly all of the financial entities that underwrite and distribute CA debt. Commercial bank direct holdings of CA’s $76 billion debt are relatively small, due to the construction of the US tax code, which discourages banks from holding tax-free municipal bonds.

GR is a problem for the European Central Bank. The ECB doesn’t own Greek sovereign debt, but it does extend credit to Greece’s national banks in the euro zone, and they hold Greek debt. Furthermore, the ECB must consider the non-Greek euro zone banks, since they too hold Greek sovereign debt. There are rules in place that will disqualify the Greek sovereign debt from use as acceptable collateral in ECB lending operations to banks. These rules apply because of the credit rating downgrades of Greece and will take effect within a year if they are not suspended or deferred. This should motivate the Greek bank lobby to spur the government of Greece to action.

Moody’s (December 22, 2009) describes the Greece situation like this: "Government action has been swift. We believe they know what they need to do and are under a great deal of external pressure to deliver. Trend growth is likely to be slower than in recent years, which means that growth will not make a significant contribution to addressing the problem. The government is likely to meet its fiscal targets in 2010. What happens in 2011 and beyond is uncertain."

PMI reports that in California about one out of 20 (5%) of all prime mortgages are in foreclosure. Worse is that one out of five subprime mortgages are in foreclosure. CA house prices fell 8% in the year ending September 30. Payroll employment dropped 4.6% in the year ending October.

The continuing saga of California’s budget crisis is well-known, so we won’t recount details here. In a recent report (November 23, 2009) Moody’s said: "Last Wednesday, the California Legislative Analyst’s Office (LAO) released a report stating that California’s current-year budget gap is approximately $6 billion and that the gap for next year is $14.4 billion. Gaps of this magnitude were expected, however, and were built into our current rating for the State of California (currently rated Baa1, with a stable outlook). This new report, therefore, does not affect California’s long-term or short-term rating. Although the size of the budgetary gap is important in determining the state’s rating, actions taken by the state to resolve the gap are even more critical because it is within the state’s power to address these large imbalances. If the gaps were to grow significantly from what has been announced by the LAO, however, or if the state cannot execute a plan to address these gaps in a timely fashion, this difficult situation could signal credit deterioration beyond our expectations. Downward pressure on the state’s ratings could result."

To sum this up: these are two central banks, the Fed and the ECB, with two currencies, the euro and the dollar, operating within two federations of sovereign states, the USA and the EU. The EU is new and only recently became the world’s largest economy, if you add up the entire 27 member states’ GDP. The 27 states are divided into three groups: those in the euro zone, those that want to be in and are trying to get in; and those that have elected not to go in or cannot qualify to get in. The US has a seasoned 50-state membership and is over 200 years old. It started as a loose and weak federation of strong sovereign states and has gradually and solidly tested a constitutional structure of strong central government, which now dominates its states.

About 75% of the combined debt of the entire world is pegged to one of these two currencies. The benchmark interest rate on the euro is the 10-year German government bond; it is paying about 3.25% interest. The benchmark debt of the US dollar is the 10-year US Treasury note; it is paying about 3.75% interest. Both the EU and the Fed are central banks whose jurisdictional boundaries have involved them in episodes of hyperinflation and depression. Both civil and international wars are parts of that history.

Both banks have the same problem. What do they do with policy when they have weakening credit among their sovereign member states? Greece is not the only problem for the ECB. It has to also keep an eye on other weak member states, like Ireland, Portugal, Italy, and Spain. California is not the only problem for the Fed. It has to deal with issues that are surfacing in places like Michigan, New Jersey, and Florida. Both central banks face huge issuance of more sovereign debt, as the budgets within their jurisdictions are in large deficit.

Can any of these states in either system default? Of course they can. California actually flirted with it when it issued script for a brief period. Will the action of a state cause the federal currency to collapse? That is the key question plaguing the markets. We think the answer is no, but acknowledge that this is an untested question. Can the currency’s relative value be maintained by the monetary authority when a state within the currency zone defaults? We think the answer is yes, but with a qualifier.

At Cumberland, we do not expect to see a mass of sovereign defaults. The issues involved are political, and the political price of default is more severe than that of toughening up budget standards. In the end, politics will raise taxes and restrict spending to avert defaults. And actual default comes about when economic pressures cause it and when they leave the political body without a choice. In our view defaults are rarely politically expedient, because default threatens a change in the political regime. Therefore, we expect both Greece and California will pay their debts.

Furthermore, we do not expect the sovereign debt of any of these mature economies to default. The 27 EU member countries and the 50 US states are not anywhere near the same types of cases as Argentina or Venezuela. Those possible defaults are driven by economics and are a result of desperate politicians who have run out of room. Argentina and Venezuela are isolated, not in a currency zone and are victims of terrible politically driven policies. It is in no neighbor’s interest to help them financially.

History shows that most governments do not pay off their debts. They refinance them indefinitely, and their governing central bank applies its directives and mandates and accommodates its sovereign states within that context. It is in the difference between the Fed and the ECB that we may find the outcomes for 2010 and beyond. The ECB is a governmental entity structured under a treaty that clearly established its independence and directs it to maintain inflation under and close to 2%. The Fed is a creature of Congress and is under the most intense political pressure we have seen in the US in a very long time. The Lisbon Treaty did not affect the independence of the ECB. All of the various proposed legislation in the US Senate or the House removes or diminishes some aspect of Fed independence. None enhances it.

Since governments do not pay off their debt and, instead, use their political mechanisms to refinance it, that is what we should expect to see in 2010 and beyond as this large post-crisis infusion of sovereign debt is issued. Here is where the central banks come in and assist with the issuance. And here is where the market may be misjudging the impact. Debt service is the key issue, not the debt aggregate. And since the principal is not paid off, it is the interest burden alone that constitutes the debt service item. So the market-related issue is, how much of the annual budget will be consumed in paying the interest, since that is where the debt-service cost will be applied. Furthermore, this burden is placed in the cash market only and not as an accrual. Markets seem to ignore accrued liabilities until they become real payments.

Another aspect of this construction about sovereign debt is that it is deflationary. Rising debt burdens consume greater and greater portions of income. They restrain spending. That is why the assumption that the increasing debt will bring on a large inflation is not necessarily correct. Japan is testimony to this outcome. In order to get the inflation that can accompany large sovereign debt issuance, the central bank has to monetize the debt at very fast and accelerating rates for a prolonged time. In Japan, that policy shift is now a subject of debate, since they are weary of fifteen years of deflation. In Europe the ECB has a clear mandate to avoid an inflationary outcome. Only in the US is this a question, and the Federal Reserve continues to say it will provide liquidity for as long as is needed but will withdraw it slowly and after the economy achieves a more sustainable growth path. The Fed is counting on a new policy-management tool for this purpose. The Fed’s own quarterly FOMC long range forecasts confirm its commitment to avoid a rising inflation rate over the next several years.

The pressures on the Fed will intensify as the sovereign debt loads in the US rise, and especially as the difficulties of finance expand in many of the sovereign 50 states. Rising interest rates hurt the economic recovery, and particularly in the troubled states. Higher mortgage rates slow the incipient housing recovery, and they raise the debt burden of refinance. Help from the US federal government will certainly be forthcoming for the states, as it already has been, but the federal deficit is quite large and not likely to shrink. Remember that federal aid to a state is merely the substitution of one type of sovereign debt for another.

In sum, we expect government bond issuance and higher debt burdens to slow the recovery and to dampen inflation tendencies. That means the Federal Reserve is likely to have the room to continue its "extended period" construction for most of 2010. Hence, we believe the short-term interest rate in the US will remain quite low. The same is true in most of the rest of the world and certainly in the euro zone, the UK, and Japan. 90% of the world’s debt is linked to one of these four currencies: the US dollar, the euro, the British pound, or the Japanese yen. For 2010, the average short-term rate of the four is projected to be between zero and 1%.

Bond portfolios are best deployed in spread products and not in the debt of these sovereigns. Forward rate analysis helps in determining where on the yield curve to position. And individual credit work is needed to ascertain and select the single issues that are desired. Sovereign debt issues will drive markets in 2010. We think they will dominate the headlines all year. It is a fascinating time to manage bonds.

We wish all our readers the very best for the New Year.

China tightening could undo risk markets

The key decision for global markets in 2010 will very likely not be made in Washington but Beijing, where emerging inflation and a property bubble may push China to begin reining in expansionary policies earlier than will suit the developed world.

After returning to a breakneck pace of growth with amazing speed, there are already signs that China is weighing steps to curtail the bank lending that has been a huge source of stimulus, helping to drive property and other asset prices sharply higher. "We emphasize the role of the reserve-requirement ratio, although the ratio was internationally seen as useless for years and it was thought central banks could abandon the tool," Chinese central bank Governor Zhou Xiaochuan said at a Beijing conference on Tuesday. "Besides benchmark interest rates, we also put emphasis on managing the gap between deposit and lending rates", Zhou said.

Put simply, that implies that China may take steps to limit the amount of money banks are allowed to lend and to drive the margins between what they pay in interest and what they charge higher, both steps which will cool growth and speculation. China's central bank on Wednesday followed up by promising to exercise tighter control over bank lending next year while reaffirming a long-standing pledge to maintain "appropriately loose" monetary policy. Even if you don't own a million dollar apartment investment in Shanghai kept empty of course because cash flows are for the little people this could spell trouble.

Zhou "today signaled the end of the global market bounce that has been in progress since the end of last winter," Lombard Street Research economist Charles Dumas wrote in a note to clients. "The only major addition of liquidity in the world economy over the past year has been in China. That is about to be withdrawn. Risk assets look like an unwise place to be in early 2010, especially commodity futures and the government bonds of countries with large deficits and/or debts. For risky investments worldwide, this could mark a turning point from 2009's massive rally."

China's banks will lend about $1.4 trillion in 2009, roughly double 2008's allocation. Official estimates put inflation at a tepid 0.6 percent for the year to November, but this is in contrast to media reports about bulk-buying by Chinese consumers concerned about a rapid rise in the price of staple foods.

Reflationary efforts in China have almost certainly had a positive impact on global economic conditions, possibly affecting market prices for securities more than fundamental demand. On the broadest measure, money supply in China is growing at an astonishing 30 percent annual clip, more or less double its usual rate of growth this decade. By Lombard Research's reckoning, China has been doing the heavy lifting. Even with a range of extraordinary policies such as quantitative easing, combined money growth in the United States, euro zone, Japan and Britain is barely positive. But adding in China's efforts, this rises to a more normal 6 percent range.

But China could be cutting back through loan controls, interest rates and ultimately by allowing the yuan to rise in value just as other sources of liquidity such as the U.S. quantitative easing program are withdrawn. Perhaps this is all part of the grand plan, and perhaps the rise in asset prices over the past nine months will be confirmed by a self-sustaining recovery even without further growth in stimulus.

There are at least three other possibilities. First, it may be that tighter policy in China retards a recovery and hurts asset prices. But there is also a chance that China genuinely needs tighter policy but the United States, Europe and Britain do not. If so, further signs that China is serious about addressing its nascent property bubble and inflation should be quite nasty news for equities and other risky assets. Finally, there is the possibility that China is the bellwether for inflationary issues that will crop up elsewhere soon, though this seems a long shot.

Risk assets could get hit if it looks like the Fed's hand is being forced regardless of what the U.S. central bank does about interest rates and its exit plan. Withdrawing monetary stimulus will hurt, but what might hurt even worse is if the Fed were forced to extend measures to the point at which it starts looking desperate rather than masterful. We are operating under a common narrative in markets: that the authorities are both willing and able to do what it takes. This may or may not be true, but it gains tremendous force simply because people subscribe to it. China may make this simple narrative quite a bit more complicated.

Gilts (UK bonds) sell-off as Britain joins Italy in debt house

The cost of borrowing for the British Government has surged to within a whisker of Italian levels as global markets issue their punishing verdict on the Government’s spending plans. The yield on 10-year gilts spiked Wednesday to 3.97pc, 46 basis points higher than costs on French bonds. Britain and France were neck and neck as recently as last month, before Labour’s pre-Budget report raised deep concerns among Chinese, Arab, and Russian investors about the credibility of British state. But what has caught market attention is the narrowing gap with Italian bonds, once mocked as the symbol of an ill-governed nation in thrall to the Dolce Vita.

Yields on 10-Italian treasuries have been hovering just above 4pc despite the eurozone’s Greek crisis, dropping as low as 3.98pc earlier this week. Julian Callow, Europe economist at Barclays Capital, said Britain is nearing the eye of the storm as the Bank of England starts to unwind quantitative easing. "The Bank has bought more gilts over the last nine months than the Government has issued. It has magically eradicated the cost of financing the deficits, but this is going to twist dramatically the other way in early 2010. Markets know this. They are demanding a risk premium on sterling."

"On top of this you have all the uncertainty over the election. We have the highest deficit in the EU as a share of GDP after Latvia and Ireland. It is not clear whether the next government will have the nerve to push through the tremendous fiscal tightening we need," he said. Britain is vulnerable to a "gilts strike" because foreign investors own £217bn of UK debt, or 28pc of the total. These are footloose funds and likely to sell large holdings if Britain loses its AAA rating. They have other tempting places to park their money, such as Turkey, Brazil, or India, where demography is healthy and growth prospects are better. Chile has already undercut British debt yields on some maturities.

Simon Derrick, currency chief at the Bank of New York Mellon, said global markets are unimpressed by the pre-Budget report and do not believe the UK Treasury forecast for 3.5pc growth in 2011. "The Government will have borrowed an extra £700bn by 2014. And the national debt will reach £1.5 trillion, which is equal £48,000 per head of the working population. The market response is entirely rational," he said Italy has its own problems, of course. Public debt was much higher before the crisis began. The IMF expects it to reach 120pc of GDP next year. However, this debt is mostly owned by high-saving Italians, who are less fickle than foreign funds.

Italy’s household debt was 34pc of GDP in 2007, compared to 100pc in the UK. "If you look at private and public debt together, they are in better shape," said Marc Ostwald from Monument Securities. "Unless our Government gets a grip soon were going to see Gilt spreads widen to 120 basis points over Bunds, with the risk of 150 if there is no clear winner in the election," he said. For Italy, this may just be the calm before the storm. Markets assume that Germany will ultimately bail out Greece if necessary, preventing contagion to the rest of the Club Med bloc.

This is a questionable judgement. Volker Wissing, head of the finance committee of the German Bundestag, said it must be made explicit that "Germany will not take responsibility for Greek debts". Mr Wissing said that ex-finance minister Peer Steinbruck was speaking for himself – not for the German state – when he hinted at rescues for eurozone laggards. His comments should be repudiated.

Banks Bundled Bad Debt, Bet Against It and Won

by Gretchen Morgenson and Louise Story

In late October 2007, as the financial markets were starting to come unglued, a Goldman Sachs trader, Jonathan M. Egol, received very good news. At 37, he was named a managing director at the firm. Mr. Egol, a Princeton graduate, had risen to prominence inside the bank by creating mortgage-related securities, named Abacus, that were at first intended to protect Goldman from investment losses if the housing market collapsed. As the market soured, Goldman created even more of these securities, enabling it to pocket huge profits.

Goldman’s own clients who bought them, however, were less fortunate. Pension funds and insurance companies lost billions of dollars on securities that they believed were solid investments, according to former Goldman employees with direct knowledge of the deals who asked not to be identified because they have confidentiality agreements with the firm.

Goldman was not the only firm that peddled these complex securities — known as synthetic collateralized debt obligations, or C.D.O.’s — and then made financial bets against them, called selling short in Wall Street parlance. Others that created similar securities and then bet they would fail, according to Wall Street traders, include Deutsche Bank and Morgan Stanley, as well as smaller firms like Tricadia Inc., an investment company whose parent firm was overseen by Lewis A. Sachs, who this year became a special counselor to Treasury Secretary Timothy F. Geithner.

How these disastrously performing securities were devised is now the subject of scrutiny by investigators in Congress, at the Securities and Exchange Commission and at the Financial Industry Regulatory Authority, Wall Street’s self-regulatory organization, according to people briefed on the investigations. Those involved with the inquiries declined to comment. While the investigations are in the early phases, authorities appear to be looking at whether securities laws or rules of fair dealing were violated by firms that created and sold these mortgage-linked debt instruments and then bet against the clients who purchased them, people briefed on the matter say.

One focus of the inquiry is whether the firms creating the securities purposely helped to select especially risky mortgage-linked assets that would be most likely to crater, setting their clients up to lose billions of dollars if the housing market imploded. Some securities packaged by Goldman and Tricadia ended up being so vulnerable that they soured within months of being created.

Goldman and other Wall Street firms maintain there is nothing improper about synthetic C.D.O.’s, saying that they typically employ many trading techniques to hedge investments and protect against losses. They add that many prudent investors often do the same. Goldman used these securities initially to offset any potential losses stemming from its positive bets on mortgage securities. But Goldman and other firms eventually used the C.D.O.’s to place unusually large negative bets that were not mainly for hedging purposes, and investors and industry experts say that put the firms at odds with their own clients’ interests.

“The simultaneous selling of securities to customers and shorting them because they believed they were going to default is the most cynical use of credit information that I have ever seen,” said Sylvain R. Raynes, an expert in structured finance at R & R Consulting in New York. “When you buy protection against an event that you have a hand in causing, you are buying fire insurance on someone else’s house and then committing arson.”

Investment banks were not alone in reaping rich rewards by placing trades against synthetic C.D.O.’s. Some hedge funds also benefited, including Paulson & Company, according to former Goldman workers and people at other banks familiar with that firm’s trading. Michael DuVally, a Goldman Sachs spokesman, declined to make Mr. Egol available for comment. But Mr. DuVally said many of the C.D.O.’s created by Wall Street were made to satisfy client demand for such products, which the clients thought would produce profits because they had an optimistic view of the housing market. In addition, he said that clients knew Goldman might be betting against mortgages linked to the securities, and that the buyers of synthetic mortgage C.D.O.’s were large, sophisticated investors, he said.

The creation and sale of synthetic C.D.O.’s helped make the financial crisis worse than it might otherwise have been, effectively multiplying losses by providing more securities to bet against. Some $8 billion in these securities remain on the books at American International Group, the giant insurer rescued by the government in September 2008. From 2005 through 2007, at least $108 billion in these securities was issued, according to Dealogic, a financial data firm. And the actual volume was much higher because synthetic C.D.O.’s and other customized trades are unregulated and often not reported to any financial exchange or market.

Goldman Saw It Coming

Before the financial crisis, many investors — large American and European banks, pension funds, insurance companies and even some hedge funds — failed to recognize that overextended borrowers would default on their mortgages, and they kept increasing their investments in mortgage-related securities. As the mortgage market collapsed, they suffered steep losses.

A handful of investors and Wall Street traders, however, anticipated the crisis. In 2006, Wall Street had introduced a new index, called the ABX, that became a way to invest in the direction of mortgage securities. The index allowed traders to bet on or against pools of mortgages with different risk characteristics, just as stock indexes enable traders to bet on whether the overall stock market, or technology stocks or bank stocks, will go up or down.

Goldman, among others on Wall Street, has said since the collapse that it made big money by using the ABX to bet against the housing market. Worried about a housing bubble, top Goldman executives decided in December 2006 to change the firm’s overall stance on the mortgage market, from positive to negative, though it did not disclose that publicly. Even before then, however, pockets of the investment bank had also started using C.D.O.’s to place bets against mortgage securities, in some cases to hedge the firm’s mortgage investments, as protection against a fall in housing prices and an increase in defaults.

Mr. Egol was a prime mover behind these securities. Beginning in 2004, with housing prices soaring and the mortgage mania in full swing, Mr. Egol began creating the deals known as Abacus. From 2004 to 2008, Goldman issued 25 Abacus deals, according to Bloomberg, with a total value of $10.9 billion. Abacus allowed investors to bet for or against the mortgage securities that were linked to the deal. The C.D.O.’s didn’t contain actual mortgages. Instead, they consisted of credit-default swaps, a type of insurance that pays out when a borrower defaults. These swaps made it much easier to place large bets on mortgage failures.

Rather than persuading his customers to make negative bets on Abacus, Mr. Egol kept most of these wagers for his firm, said five former Goldman employees who spoke on the condition of anonymity. On occasion, he allowed some hedge funds to take some of the short trades. Mr. Egol and Fabrice Tourre, a French trader at Goldman, were aggressive from the start in trying to make the assets in Abacus deals look better than they were, according to notes taken by a Wall Street investor during a phone call with Mr. Tourre and another Goldman employee in May 2005.

On the call, the two traders noted that they were trying to persuade analysts at Moody’s Investors Service, a credit rating agency, to assign a higher rating to one part of an Abacus C.D.O. but were having trouble, according to the investor’s notes, which were provided by a colleague who asked for anonymity because he was not authorized to release them. Goldman declined to discuss the selection of the assets in the C.D.O.’s, but a spokesman said investors could have rejected the C.D.O. if they did not like the assets.

Goldman’s bets against the performances of the Abacus C.D.O.’s were not worth much in 2005 and 2006, but they soared in value in 2007 and 2008 when the mortgage market collapsed. The trades gave Mr. Egol a higher profile at the bank, and he was among a group promoted to managing director on Oct. 24, 2007. “Egol and Fabrice were way ahead of their time,” said one of the former Goldman workers. “They saw the writing on the wall in this market as early as 2005.” By creating the Abacus C.D.O.’s, they helped protect Goldman against losses that others would suffer.

As early as the summer of 2006, Goldman’s sales desk began marketing short bets using the ABX index to hedge funds like Paulson & Company, Magnetar and Soros Fund Management, which invests for the billionaire George Soros. John Paulson, the founder of Paulson & Company, also would later take some of the shorts from the Abacus deals, helping him profit when mortgage bonds collapsed. He declined to comment.

A Deal Gone Bad, for Some

The woeful performance of some C.D.O.’s issued by Goldman made them ideal for betting against. As of September 2007, for example, just five months after Goldman had sold a new Abacus C.D.O., the ratings on 84 percent of the mortgages underlying it had been downgraded, indicating growing concerns about borrowers’ ability to repay the loans, according to research from UBS, the big Swiss bank. Of more than 500 C.D.O.’s analyzed by UBS, only two were worse than the Abacus deal.

Goldman created other mortgage-linked C.D.O.’s that performed poorly, too. One, in October 2006, was a $800 million C.D.O. known as Hudson Mezzanine. It included credit insurance on mortgage and subprime mortgage bonds that were in the ABX index; Hudson buyers would make money if the housing market stayed healthy — but lose money if it collapsed. Goldman kept a significant amount of the financial bets against securities in Hudson, so it would profit if they failed, according to three of the former Goldman employees.

A Goldman salesman involved in Hudson said the deal was one of the earliest in which outside investors raised questions about Goldman’s incentives. “Here we are selling this, but we think the market is going the other way,” he said. A hedge fund investor in Hudson, who spoke on the condition of anonymity, said that because Goldman was betting against the deal, he wondered whether the bank built Hudson with “bonds they really think are going to get into trouble.”

Indeed, Hudson investors suffered large losses. In March 2008, just 18 months after Goldman created that C.D.O., so many borrowers had defaulted that holders of the security paid out about $310 million to Goldman and others who had bet against it, according to correspondence sent to Hudson investors. The Goldman salesman said that C.D.O. buyers were not misled because they were advised that Goldman was placing large bets against the securities. “We were very open with all the risks that we thought we sold. When you’re facing a tidal wave of people who want to invest, it’s hard to stop them,” he said. The salesman added that investors could have placed bets against Abacus and similar C.D.O.’s if they had wanted to.

A Goldman spokesman said the firm’s negative bets didn’t keep it from suffering losses on its mortgage assets, taking $1.7 billion in write-downs on them in 2008; but he would not say how much the bank had since earned on its short positions, which former Goldman workers say will be far more lucrative over time. For instance, Goldman profited to the tune of $1.5 billion from one series of mortgage-related trades by Mr. Egol with Wall Street rival Morgan Stanley, which had to book a steep loss, according to people at both firms.

Tetsuya Ishikawa, a salesman on several Abacus and Hudson deals, left Goldman and later published a novel, “How I Caused the Credit Crunch.” In it, he wrote that bankers deserted their clients who had bought mortgage bonds when that market collapsed: “We had moved on to hurting others in our quest for self-preservation.” Mr. Ishikawa, who now works for another financial firm in London, declined to comment on his work at Goldman.

Profits From a Collapse

Just as synthetic C.D.O.’s began growing rapidly, some Wall Street banks pushed for technical modifications governing how they worked in ways that made it possible for C.D.O.’s to expand even faster, and also tilted the playing field in favor of banks and hedge funds that bet against C.D.O.’s, according to investors.

In early 2005, a group of prominent traders met at Deutsche Bank’s office in New York and drew up a new system, called Pay as You Go. This meant the insurance for those betting against mortgages would pay out more quickly. The traders then went to the International Swaps and Derivatives Association, the group that governs trading in derivatives like C.D.O.’s. The new system was presented as a fait accompli, and adopted.

Other changes also increased the likelihood that investors would suffer losses if the mortgage market tanked. Previously, investors took losses only in certain dire “credit events,” as when the mortgages associated with the C.D.O. defaulted or their issuers went bankrupt. But the new rules meant that C.D.O. holders would have to make payments to short sellers under less onerous outcomes, or “triggers,” like a ratings downgrade on a bond. This meant that anyone who bet against a C.D.O. could collect on the bet more easily.

“In the early deals you see none of these triggers,” said one investor who asked for anonymity to preserve relationships. “These things were built in to provide the dealers with a big payoff when something bad happened.” Banks also set up ever more complex deals that favored those betting against C.D.O.’s. Morgan Stanley established a series of C.D.O.’s named after United States presidents (Buchanan and Jackson) with an unusual feature: short-sellers could lock in very cheap bets against mortgages, even beyond the life of the mortgage bonds. It was akin to allowing someone paying a low insurance premium for coverage on one automobile to pay the same on another one even if premiums over all had increased because of high accident rates.

At Goldman, Mr. Egol structured some Abacus deals in a way that enabled those betting on a mortgage-market collapse to multiply the value of their bets, to as much as six or seven times the face value of those C.D.O.’s. When the mortgage market tumbled, this meant bigger profits for Goldman and other short sellers — and bigger losses for other investors.

Selling Bad Debt

Other Wall Street firms also created risky mortgage-related securities that they bet against. At Deutsche Bank, the point man on betting against the mortgage market was Greg Lippmann, a trader. Mr. Lippmann made his pitch to select hedge fund clients, arguing they should short the mortgage market. He sometimes distributed a T-shirt that read “I’m Short Your House!!!” in black and red letters.

Deutsche, which declined to comment, at the same time was selling synthetic C.D.O.’s to its clients, and those deals created more short-selling opportunities for traders like Mr. Lippmann. Among the most aggressive C.D.O. creators was Tricadia, a management company that was a unit of Mariner Investment Group. Until he became a senior adviser to the Treasury secretary early this year, Lewis Sachs was Mariner’s vice chairman. Mr. Sachs oversaw about 20 portfolios there, including Tricadia, and its documents also show that Mr. Sachs sat atop the firm’s C.D.O. management committee.

From 2003 to 2007, Tricadia issued 14 mortgage-linked C.D.O.’s, which it called TABS. Even when the market was starting to implode, Tricadia continued to create TABS deals in early 2007 to sell to investors. The deal documents referring to conflicts of interest stated that affiliates and clients of Tricadia might place bets against the types of securities in the TABS deal. Even so, the sales material also boasted that the mortgages linked to C.D.O.’s had historically low default rates, citing a “recently completed” study by Standard & Poor’s ratings agency — though fine print indicated that the date of the study was September 2002, almost five years earlier.

At a financial symposium in New York in September 2006, Michael Barnes, the co-head of Tricadia, described how a hedge fund could put on a negative mortgage bet by shorting assets to C.D.O. investors, according to his presentation, which was reviewed by The New York Times. Mr. Barnes declined to comment. James E. McKee, general counsel at Tricadia, said, “Tricadia has never shorted assets into the TABS deals, and Tricadia has always acted in the best interests of its clients and investors.” Mr. Sachs, through a spokesman at the Treasury Department, declined to comment.

Like investors in some of Goldman’s Abacus deals, buyers of some TABS experienced heavy losses. By the end of 2007, UBS research showed that two TABS deals were the eighth- and ninth-worst performing C.D.O.’s. Both had been downgraded on at least 75 percent of their associated assets within a year of being issued. Tricadia’s hedge fund did far better, earning roughly a 50 percent return in 2007 and similar profits in 2008, in part from the short bets.

Are Big Banks Pumping Up Stock Prices?

Even though big banks have received untold billions in bailout funds, banks are not lending. Where did all the money go? Much of it went right back to the government as banks have loaded up on all sorts of Treasury bonds. But where did the rest go?

Real estate prices are still falling, unemployment is sky-high, consumer spending is down and corporate profits are nowhere near to last year's levels. The only thing that provides comfort for the masses is rising stock prices. The S&P 500, Dow Jones and Nasdaq have gained in excess of 65% in less than ten months against a backdrop of continuously less than stellar news. The government, banks and other financial institutions have a vested interest in rising stock prices.

Things would look grim if it wasn't for the hope provided by the Dow and S&P's of the world. But more than hope is at stake. Another drop in investor's perception would send real estate and equity prices tumbling. It could also push many financial institutions to the brink of ruin and discredit all government efforts. Looking at what's at stake and the motivations involved, could it be that some of the big players are manipulating the market to keep prices artificially afloat?

A secret committee

Don't you hate it when juicy news is making its rounds but you are kept out of the loop? Welcome to the club. Already back in 1988, Ronald Reagan signed an executive order to establish a specific committee designed to prevent major market collapses. As per this order, the Secretary of the Treasury, the chairman of the Federal Reserve, the chairman of the SEC and the chairman of the commodity futures trading commission make up the core of this team. By extension, major financial institutions like JP Morgan Chase and Goldman Sachs are used to execute their orders.

The existence of this team is said to have been confirmed by former Clinton advisor George Stephanopoulos on Good Morning America. Last year, former Treasury Secretary Hank Paulson called for this 'financial fraternity' to meet with greater frequency and set up a command center at the U.S. Treasury designed to track global markets and serve as headquarter for the next crisis. There is much more to this unique arrangement designed to keep a lid an potential market meltdowns and use major Wall Street firms as marionettes to accomplish this goal. A detailed report about this secret team is available in the most recent issue of the ETF Profit Strategy Newsletter.

Artificially inflating prices, how?

Supply and demand drives prices. Where the demand comes from does not matter. In emergency situations, the Federal Reserve is said to lend money to major banks, which serve as surrogates who will take the money and buy markets, predominantly futures, through large unknown accounts. The timing of those buys will be such that those shorting the market will be forced to buy back shares. In theory, this eliminates the most pessimistic investors and causes others to buy. Soon sideline money from mutual and hedge funds comes in and the rally gathers a life of its own.

A close ally

One of the obvious suspects to serve as surrogate and carry out the government's plan would be Goldman Sachs. For years, the ties between the U.S. government and Sachs have been too close for comfort. Earlier this year the ETF Profit Strategy Newsletter touched on a case of 'indiscretion' which never received much publicity. Stephen Friedman, the chairman of the New York Fed was instrumental in orchestrating the multi-billion bailout for Goldman and AIG. AIG used nearly $10 billion of the initial $85 billion to pay Goldman.

Chairman of the New York Fed was not the only title Mr. Friedman held. He also happened to be on Goldman's board during that time and was Goldman's CEO in the 1990s. Also during that time, Mr. Friedman was actively buying Goldman stock and generated profits worth millions of dollars. Other ties between government and Sachs include Hank Paulson, former Secretary of the Treasury and former Goldman CEO. When Mr. Paulson needed someone to oversee see the government's first $700 billion bailout, Paulson recruited an inexperience, 35-year old, former Goldman investment banker. The list continues, but we'll stop here.

Putting the odds in your favor

The Financial Times reported that Goldman Sachs suffered only one losing day during the 65 business days of the third quarter. On 36 separate days during the quarter, the firm's trades netted more than $100 million. In addition, Bloomberg reported that Goldman Sachs' effective income tax rate for 2008 was 1%. In dollars, Goldman's tax liability was $14 million. For the same year, Goldman reported a $2.3 billion profit and paid out $10.9 billion in bonuses. One could argue that a record of 90%+ winning trades and a 1% tax rate could only be accomplished with certain connections to high-ranking government personnel.

Is it possible?

The notion that prices can be inflated artificially makes sense and sounds good in theory. Based on the evidence, this kind of maneuvering even seems to be more common than we think. But a simple look at the chart shows that even the government and big banks do not have superhuman powers, at least not unconditionally. In 2000, 2002, 2008 and 2009, the major indexes a la S&P 500, Dow Jones and Nasdaq declined 30% or more. It is now known, as it was back then, that the nation's most powerful financiers got together on October 24, 1929 to prevent a major meltdown. Their plan succeeded on that very day which came to be known as Black Thursday. The recovery on Black Thursday was as remarkable as the selling that made it so Black.

On Friday, the Times reported that the financial community felt 'secure in the knowledge that the most powerful banks in the country stood ready to prevent a recurrence of panic.' In a concerted advertising campaign in Monday's papers, stock market firms urged to pick stocks at bargain prices. The rest is history and the Great Depression unfolded in all its cruel ways. One of the flaws of artificial buying is that all the money used to buy stocks will eventually have to be taken out. As we know, banks are not immune to greed and once prices start declining, banks are likely to be the first to cut their losses and flee the sinking ship.

What goes up ...

In summary, we can conclude that there seems to be an organized committee with the job description of lifting markets. Quite likely, their efforts have contributed to the protracted rally in stock prices. However, as we've seen, the market is too wild to be contained. Normal market forces still apply. One of those age-old forces is investor sentiment, possibly the best known and most accurate contrarian indicator around. Extreme levels of pessimism tend to signal market bottoms while extreme levels of optimism tend to signal tops.

The ETF Profit Strategy Newsletter used this contrarian indicator as a foundation to issue the March 2nd Trend Change Alert which foretold a massive rally with a target range of Dow 9,000 - 10,000 a mere seven days before the March lows were reached. Now once again, we see an extreme of investor sentiment - this time it's optimism. According to the Investors Intelligence survey, this week saw the highest percentage of bulls since December 2007. More importantly, the major indexes are butting up against levels of resistance that have been years, even decades in the making. Those different resistance levels converge in the Dow 10,100 - Dow 10,500 range, which is the very range the Dow has been stuck in for over three months.

The ETF Profit Strategy Newsletter includes an analysis of predominant, and probably formidable, levels of resistance along with a short, mid and long-term forecast, and a target range for the ultimate market bottom. If history is a guide, and it usually is, the market will do what it wants, regardless of the government's efforts. The question is this: Who are you putting your trust in, the market or big banks?

Taxpayer Burden Eases to $8.2 Trillion as Obama Supplants Fed

Congress and the Obama administration are taking a bigger role in the rescue of the economy from the Federal Reserve, shifting the strategy to stimulus spending from central bank lending. The amount the Fed and U.S. agencies have lent, spent or guaranteed has fallen 15 percent since September to $8.2 trillion, the lowest in a year, based on data compiled by Bloomberg. Spending on infrastructure, tax breaks and other fiscal measures account for 52 percent of the total, up from 39 percent in March, as central bank loan programs are phased out.

The change marks a new phase of public intervention in the economy. Congress and the administration’s $4.2 trillion portion, which amounts to 30 percent of everything produced in the country this year, also complicates any future exit strategy. It may be tough for elected officials to quit spending, prolonging the bailout and adding to the federal budget deficit. “There’s a danger of getting addicted to fiscal stimulus programs,” said David Wyss, chief economist with New York-based Standard & Poor’s, in an interview. “The Fed can print money. Government has to raise taxes or borrow more.”

The U.S. House of Representatives last week increased the federal government’s debt ceiling $290 billion to $12.4 trillion. It also passed a $154 billion economic aid package to pay for extended unemployment benefits, new infrastructure projects and help to state governments. Commitments by Congress to spend more than $984 billion, or about 8 percent of the national debt, include stimulus packages championed by President Barack Obama and President George W. Bush and a November 2008 change in the tax code to encourage large banks to buy smaller ones.

The U.S. has run 14 consecutive monthly budget deficits and 7.3 million people have lost their jobs since the beginning of the recession in December 2007, according to the Treasury Department. Monthly budget shortfalls have outnumbered surpluses almost 2 to 1 this decade, according to Treasury data. “We can’t continue to spend as if deficits don’t have consequences, as if waste doesn’t matter, as if the hard-earned tax dollars of the American people can be treated like Monopoly money,” Obama said Dec. 21 at the White House.

The Obama administration still has about half its $787 billion stimulus package to spend, according to the Office of Management and Budget. The Fed has shut or is phasing out the 10 support programs it created after August 2007 as the financial system recovers from the longest recession since the 1930s.

As the economy improves, policy makers are pulling back liquidity to prevent inflation and asset bubbles. The European Central Bank last week raised the interest rate on its tender of 12-month loans to the one-year average of the bank’s benchmark, a departure from its policy of offering the money at a fixed 1 percent. The ECB said it will also cease lending for six months at the end of the first quarter. The S&P 500 Index has climbed 24 percent this year, its second-biggest annual percentage gain this decade. That has helped banks make money outside of Fed programs. In the first nine months of the year, Goldman Sachs Group Inc.’s trading revenue doubled to a record $27.3 billion, while JPMorgan Chase & Co.’s climbed 122 percent to $17.9 billion, according to company reports.

Spreads on U.S. corporate debt, which show the risk premium that investors demand to own them instead of government bonds, have plunged to below 2 percentage points from more than 6 percentage points at the start of the year, according to the Merrill Lynch U.S. Corporate Master Index. That’s the most spreads have narrowed this decade, the data show. The Fed’s plan to buy $1.25 trillion of mortgage-backed securities is its largest spending program. The Fed holds $901.2 billion of the securities and is scheduled to complete the purchases in the first quarter.

That will leave the central bank “walking a tightrope” between blocking economic recovery and sparking a rise in prices, according to Dan Greenhaus, chief economic strategist at Miller Tabak & Co. in New York. The Fed’s balance sheet ballooned to $2.24 trillion in assets as of last week, up 142 percent from the beginning of 2008. Selling some of those assets to take money out of the economy has its risks, Greenhaus said. “You have to ensure economic expansion without fanning inflation and assess prospects for asset bubbles while bringing down the unemployment rate,” Greenhaus said in an interview. “The difficulties can’t be easily dismissed.”

Consumer prices rose 1.8 percent in November compared with a year ago and have increased by an average 2.6 percent over the last decade, according to the U.S. Bureau of Labor Statistics. As U.S. banks have rebuilt their balance sheets after taking $1.1 trillion of losses and writedowns, according to data compiled by Bloomberg, they’ve tapped the central bank less. The Fed said there’s been no borrowing from the Term Securities Lending Facility since mid-August and from the Primary Dealer Credit Facility since mid-May. The central bank will phase out both programs. The Asset-Backed Commercial Paper Money Market Fund Liquidity Facility hasn’t attracted customers since May. The Fed has indicated it will expire Feb. 1.

The Fed will shorten the maturity dates of primary credit loans at the discount window to 28 days from 90 days starting Jan. 14 as banks are better able to find funding themselves. The central bank said it will close the Commercial Paper Funding Facility, the Primary Dealer Credit Facility and swap lines with foreign central banks on Feb. 1 and the Term Asset-Backed Securities Loan Facility, or TALF, on June 1. The Money Market Investor Funding Facility, known as MMIFF, was shuttered on Oct. 30. The Fed’s planned purchase of $300 billion of longer-term Treasury securities was also completed at the end of October.

US state unemployment funds going ‘absolutely broke’

The recession's jobless toll is draining unemployment-compensation funds so fast that according to federal projections, 40 state programs will go broke within two years and need $90 billion in loans to keep issuing the benefit checks. The shortfalls are putting pressure on governments to either raise taxes or shrink the aid payments. Debates over the state benefit programs have erupted in South Carolina, Nevada, Kansas, Vermont and Indiana. And the budget gaps are expected to spread and become more acute in the coming year, compelling legislators in many states to reconsider their operations.

Currently, 25 states have run out of unemployment money and have borrowed $24 billion from the federal government to cover the gaps. By 2011, according to Department of Labor estimates, 40 state funds will have been emptied by the jobless tsunami. "There's immense pressure, and it's got to be faced," said Indiana state Rep. David Niezgodski (D), a sponsor of a bill that addressed the gaps in Indiana's unemployment program. "Our system was absolutely broke."