"Beach in front of Sea Foam House, Old Orchard, Maine"

Ilargi: The US government is looking at possible solutions for the mess that Fannie Mae and Freddie Mac have long since become. There is, however, no solution available. Period. Simple as that. The government has dug itself into a hole when it comes to mortgages and mortgage-based securities that it cannot find a way out of.

If the government had any sense left, it would get out of the mortgage market by, let's say, yesterday morning. Take apart Freddie, Fannie and Ginnie Mae, along with the Federal Housing Administration, sell off all of their assets at whatever price is being offered (if any), and be done with it already.

But the government has no such sense. It will instead elect to insert more layers of Russian dolls, one after the other, to maintain the illusion that domestic real estate has some actual intrinsic value left. And sure, yes, this does make some sense, if you look at the situation in just the right sort of light.

Selling off all mortgage related assets would have a number of highly predictable consequences. First and foremost, housing prices would plunge like nothing you've ever seen. This would have happened slowly and in a more orderly fashion years ago if not for government guarantees for every dollar spent by homebuyers. Because of these guarantees, those same homebuyers have spent twice as many, if not more, dollars on their home purchases.

Yes, Fannie and Freddie are the ultimate in perversity. Not only does the government use every citizen's tax revenue to guarantee future losses on their neighbor's real estate purchases, both new and existing, it willingly causes that neighbor to pay two, three, four times more for their home than they would have without those guarantees.

Nor does the perversity stop there. No matter how many dolls you take away, there's always another one underneath. And the only thing that is ultimately 100% guaranteed by this system of goverment housing and mortgage guarantees is the very failure of the system itself. The government lures its citizens into buying highly overpriced properties, and then feeds those same citizen to the banking system, which entices them to take on huge amounts of debt in order to "own" the properties.

If the government were able to constantly produce new layers of gullible citizens, the US housing ponzi could endure until the end of time. But it can't. There will come a day when the last doll is lifted, and there will be no more dolls left. You can't have a factual unemployment rate of 15-20% (re: U6) and at the same time still keep the ponzi going. No matter what the government does to extend end pretend the scheme, the only possible end game is collapse.

The de facto nationalized carmaker GM spent $3.5 billion last week to acquire subprime lender AmeriCredit. That is, $3.5 billion in taxpayer funds were used to buy a lender that will be used to finance car purchases by those who would otherwise either have no access to credit at all or have to pay far higher interest rates. Yeah, sure, GM is planning an IPO, but for the moment the taxpayer owns the firm, a tiny detail that shines an eerily pale light on the acquisition.

GM will use AmeriCredit to borrow money at around 0% from the Fed (which means, once again, the taxpayer) so it can offer 0% financing to people who have no money to buy a vehicle but can still in this way be enticed to take on more credit and more debt. Courtesy of the American government. Which should perhaps help people get out of debt, not drag them in ever deeper. All this confirms once more whose side the government is on: anybody's but the people.

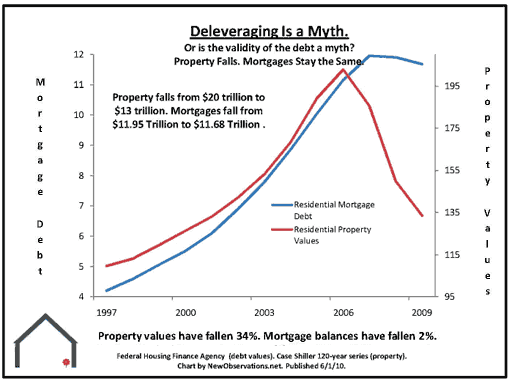

There are estimates floating out there that pretend that the government's losses so far on Fannie and Freddie add up to some $145 billion. In reality, these losses are far greater, and they're growing at an exponential rate. Another look at a graph posted here before, from Michael David White, indicates that accumulated losses in US domestic real estate, from 2006 to 2010, are around $7 trillion. Let's say that $2 trillion of that is on homes without mortgages. That leaves $5 trillion in losses on mortgaged homes. Fannie and Freddie hold about 50% of that (and up to 95% of new loans).

In other words, mortgages bought by Fannie and Freddie have lost at least $2.5 trillion in value. It may be true that the people who took out the loans are still on the hook for them, as the graph clearly shows, and we may continue to pretend that these are therefore not Fannie and Freddie's losses, but it's not all that hard to see that this is merely a matter of time.

If and when the government will have its hand forced, when it can no longer afford to pretend that the mortgage market is alive and well, home prices will start falling with a vengeance, until they reflect an actual market situation based on supply and demand. That will have very grave consequences. Any party that holds mortgage based securities, be it the government, the Federal Reserve, pension funds (domestic or abroad) and don't let's forget the Chinese, will suffer colossal losses on them.

In that light it's downright scary to see the FDIC now try to finance its daily job of closing banks by selling mortgage based securities it has obtained through closures, into the open market. Anyone purchasing the stuff will do so only because of yet another government guarantee, issued on the sole premise of kicking the canister down the road and down the mountain a little longer.

And in whose interest is all this? Not that of prospective homebuyers, who pay prices that are far higher than what a functioning market would be asking. Not that of the taxpayer, who gets shouldered with more debt guarantees on an almost daily basis. One might argue that it's in the interest of existing homeowners to keep prices artificially inflated, in order to keep their mortgage payments in some sort of line with the value of their properties, but then again, these payments are also much higher then they would be without the unlimited subsidies the Treasury has explicitly afforded Fannie and Freddie.

In the end, it all comes down to the same conclusion, time and again. The people who ultimately profit most from this seemingly never ending extending and pretending are the bankers and politicians who get to keep their money and their power for a few more days, months or years. Down the line, however, they would have to pay people to buy homes and take out mortgage loans if they wish to keep the system running. And since they're not going to do that, the system is doomed.

Washington runs on fumes only, the federal deficit is gigantic and rising (even if the goverment "predicts" otherwise), there are massive new lay-offs in the offing, starting with federal, state and municipal employees, all of which will shrink the pool of prospective buyers and hence market prices. Meanwhile, the "pretend" phase is kept alive with nonsensical drivel from politicians and media pundits alike about economic recovery and growth.

There will come a moment when the White House can no longer refuse to put Fannie and Freddie on the federal balance sheet. That will add so much debt to that sheet, both from the mortgages themselves and from the securities written on them, that anyone with a few pennies left will run away as fast as they can. The quest to keep the game going will down the line come at a very steep price. When the last doll is lifted, there will, for the vast majority of the population, be nothing left. At all. That is, except for the tens of trillions in debt. That will remain.

US federal budget deficit to exceed $1.4 trillion in 2010 and 2011

by Lori Montgomery - Washington Post

The federal budget deficit, which hit a record $1.4 trillion last year, will exceed that figure this year and again in 2011, the White House predicted Friday, providing fresh ammunition to Republicans who are hammering President Obama for all the red ink as they campaign to regain control of Congress in November. The latest forecast from the White House budget office shows the deficit rising to $1.47 trillion this year, forcing the government to borrow 41 cents of every dollar it spends. Contrary to official projections, the budget gap will not begin to narrow much in 2011, because of an unexpectedly big drop in tax receipts.

White House budget director Peter Orszag said in a conference call with reporters that Obama is still on track to cut the deficit in half by the end of his first term. But the forecast provides no relief from the gloomy outlook that has been forcing Obama to consider deeper cuts to defense and non-security programs as well as additional tax increases. This week, the administration also repeated its intention to let tax cuts for the wealthy expire in January.

With polls showing high public anxiety over the economy and government borrowing, Republicans wasted no time blasting the new forecast. They accused Obama and congressional Democrats of orchestrating a government expansion that threatens to push the nation toward a European-style debt crisis while failing to create jobs. "For more than a year and a half, the president and his Democrat allies on Capitol Hill have pushed an anti-business, anti-jobs agenda on the American people while adding trillions to the debt," Senate Minority Leader Mitch McConnell (R-Ky.) said in a statement. "It's time for a new approach, one that listens to the American people rather than forcing Washington-based mandates."Democrats sought to remind voters that persistently large budget gaps are primarily the result of a severe recession that depressed tax revenue and forced policymakers to spend hundreds of billions of dollars on economic rescue programs, such as last year's $862 billion stimulus package. Unemployment has nonetheless risen. The White House predicted Friday it will not dip below 8 percent until the end of 2012. Still, many economists say federal action probably saved the nation from a full-blown meltdown.

"That federal response -- including actions by the Federal Reserve, efforts to stabilize the financial sector started by the Bush administration, and last year's economic recovery package -- has successfully pulled the economy back from the brink," Senate Budget Committee Chairman Kent Conrad (D-N.D.) said in a statement. "Although the economy remains fragile and the unemployment rate is still far too high, economic and job growth have begun to return."

But they have not returned fast enough to improve the budget picture -- or the national mood. A CNN/Opinion Research Corporation poll released Friday found that Obama's economic approval rating has fallen to a new low, with 57 percent of those surveyed saying they disapprove of Obama's handling of the economy. In the same poll, 47 percent of respondents ranked the economy as the most important issue facing the country; the budget deficit followed at 13 percent.

In its semiannual fiscal outlook, the White House budget office acknowledged that "the U.S. economy still faces strong headwinds," including tight credit markets, too many unsold houses and state governments burdened by their own budget deficits. Christina Romer, chairman of the president's Council of Economic Advisers, said economic turbulence in Europe has also had an impact, "ever so slightly dampening growth prospects in 2011."

The report said that "despite these headwinds, the administration expects economic growth and job creation to continue for the rest of 2010 and to rise in 2011 and beyond." The updated forecast had a mixed impact on deficit projections. For 2010, lower spending than expected on unemployment benefits and bank deposit insurance led to a lower deficit projection; the White House had previously predicted a budget gap of $1.56 trillion this year. Meanwhile, lower tax receipts, primarily from capital gains taxes, raised deficit projections for 2011 and 2012.

But the long-term forecast stayed about the same, with the White House predicting additional borrowing of $8.5 trillion through 2020, a sum that would drive the national debt to more than 77 percent of annual economic output. That would be the highest percentage since 1950. Independent forecasters, such as the Congressional Budget Office, say that number will probably be significantly higher if current policies remain unchanged. Obama has created a bipartisan commission to develop a strategy for stabilizing the debt by 2015.

The White House and senior Democrats say cutting deficits too quickly would threaten the recovery. But Sen. Judd Gregg (R-N.H.), a member of the president's budget commission, called it "worrisome" that the administration seems to be relying solely on the commission. And some independent budget analysts agreed. "The White House has to use the bully pulpit to spotlight the nation's fiscal challenges," said Maya MacGuineas, president of the bipartisan Committee for a Responsible Federal Budget. "The president cannot afford to sweep this type of fiscal warning under the carpet, or we risk that policymakers will go on their merry way . . . ignoring the warnings and marching towards fiscal calamity."

US financial system support up $700 billion in past year

by David Lawder - Reuters

Increased housing commitments swelled U.S. taxpayers' total support for the financial system by $700 billion in the past year to around $3.7 trillion, a government watchdog said on Wednesday. The Special Inspector General for the Troubled Asset Relief Program said the increase was due largely to the government's pledges to supply capital to Fannie Mae and Freddie Mac and to guarantee more mortgages to support the housing market.

Increased guarantees for loans backed by the Federal Housing Administration, the Government National Mortgage Association and the Veterans administration increased the government's commitments by $512.4 billion alone in the year to June 30, according to the report. "Indeed, the current outstanding balance of overall Federal support for the nation's financial system...has actually increased more than 23% over the past year, from approximately $3.0 trillion to $3.7 trillion -- the equivalent of a fully deployed TARP program -- largely without congressional action, even as the banking crisis has, by most measures, abated from its most acute phases," the TARP inspector general, Neil Barofsky, wrote in the report.

The total includes Federal Reserve programs and a myriad of asset guarantees, including Federal Deposit Insurance Corp. protection for bank deposits. The increased government commitments more than offset about a $300 billion decline in the U.S. Treasury's TARP commitments in the past year as programs have closed and banks have repaid taxpayer funds.

Housing Programs Criticized

Barofsky also in the report ramped up his criticism of the Treasury's housing relief efforts, saying that its program to reduce monthly mortgage payments for struggling homeowners was showing "anemic" participation numbers and had failed to "put an appreciable dent in foreclosure filings." He said Treasury had refused his repeated recommendations to announce more effective goals and benchmarks for its mortgage modification program, which could reach up to $50 billion in TARP funds.

"Treasury's refusal to provide meaningful goals for this important program is a fundamental failure of transparency and accountability that makes it far more difficult for the American people and their representatives in Congress to assess whether the program's benefits are worth its very substantial cost," Barofsky wrote. Among other recommendations repeated in the report, Barofsky called for the Treasury to consider making its voluntary mortgage principal reduction program mandatory, saying this would make it less likely for "underwater" homeowners to abandon their properties.

The Treasury has declined to adopt the recommendation, citing the prospect that mandatory principal reduction would cause mortgage servicing firms to opt out of the program and fairness issues in reducing principal for both responsible homeowners hit by value declines and homeowners who overleveraged their properties in refinancings. U.S. Treasury officials defended the Home Affordable Modification Program, saying that it was still on track to reach its goal to keep 3 million to 4 million homeowners in their homes by the end of 2012 and was adapting to changing conditions by offering forbearance to unemployed people and extra funding for the hardest-hit markets.

Herbert Allison, Treasury assistant secretary for financial stability, said the Treasury often agrees with Barofsky's recommendations, "but once in a while, we differ on what type of policy will best carry out our mandate." The report provoked swift criticism of Obama administration housing policies from U.S. Rep. Darrell Issa, a California Republican who has taken every opportunity to blast the Treasury's handling of financial bailout programs.

"The fact that the Obama administration is treating TARP like its own personal slush-fund is beyond egregious and a complete betrayal of what the American people were told would be then when their tax-dollars were used to bailout Wall Street," Issa said in a statement, adding that the housing efforts were "dumping good money after bad".

2011: The Year Of The Tax Increase

by MIchael Snyder - Economic Collapse

Unless the U.S. Congress acts, there is going to be a massive wave of tax increases in 2011. In fact, some are already calling 2011 the year of the tax increase. A whole host of tax cuts that Congress established between 2001 and 2003 are set to expire in January unless Congress chooses to renew them. But with Democrats firmly in control of both houses that appears to be extremely unlikely. These tax increases are going to affect every single American (at least those who actually pay taxes). But this will be just the first wave of tax increases. Another huge slate of tax increases passed in the health care reform law is scheduled to go into effect by 2019. So Americans that are already infuriated by our tax system are only going to become more frustrated in the years ahead. The reality is that the U.S. government will soon be digging much deeper into our wallets.The following are some of the tax increases that are scheduled to go into effect in 2011....

1 - The lowest bracket for the personal income tax is going to increase from 10 percent to 15 percent.

2 - The next lowest bracket for the personal income tax is going to increase from 25 percent to 28 percent.

3 - The 28 percent tax bracket is going to increase to 31 percent.

4 - The 33 percent tax bracket is going to increase to 36 percent.

5 - The 35 percent tax bracket is going to increase to 39.6 percent.

6 - In 2011, the death tax is scheduled to return. So instead of paying zero percent, estates of $1 million or more are going to be taxed at a rate of 55 percent.

7 - The capital gains tax is going to increase from 15 percent to 20 percent.

8 - The tax on dividends is going to increase from 15 percent to 39.6 percent.

9 - The "marriage penalty" is also scheduled to be reinstated in 2011.

It is being estimated that the total cost of these tax increases to U.S. taxpayers will be $2.6 trillion through the year 2020.

Ouch!

But wait, there are even more tax increases coming.

The "health care reform law" contains over a dozen new taxes that will be implemented in stages over the next decade. When you add all of these taxes to the taxes that were mentioned earlier, the result is going to be absolutely devastating. According to an analysis by the Congressional Joint Committee on Taxation the health care reform law will generate $409.2 billion in additional taxes by the year 2019.

Double ouch!

So is it any wonder why the public has such a low opinion of the U.S. Congress?

Every single major poll done on the topic shows that approval ratings for Congress are at record lows.

For example, Gallup's 2010 Confidence in Institutions poll found Congress ranking dead last out of the 16 institutions rated this year.

Of course there are a whole host of reasons why the American people are upset with Congress, but one of the big ones is the fact that we are literally being taxed to death.

However, it is not just federal income taxes that are killing us.

In a previous article entitled "Taxed Enough Already!", we listed just a few of the taxes that Americans have to pay each year....

Accounts Receivable Tax

Building Permit Tax

Capital Gains Tax

CDL license Tax

Cigarette Tax

Corporate Income Tax

Court Fines (indirect taxes)

Dog License Tax

Federal Income Tax

Federal Unemployment Tax (FUTA)

Fishing License Tax

Food License Tax

Fuel permit tax

Gasoline Tax

Gift Tax

Hunting License Tax

Inheritance Tax

Inventory tax IRS Interest Charges (tax on top of tax)

IRS Penalties (tax on top of tax)

Liquor Tax

Local Income Tax

Luxury Taxes

Marriage License Tax

Medicare Tax

Payroll Taxes

Property Tax

Real Estate Tax

Recreational Vehicle Tax

Road Toll Booth Taxes

Road Usage Taxes (Truckers)

Sales Taxes

School Tax

Septic Permit Tax

Service Charge Taxes

Social Security Tax

State Income Tax

State Unemployment Tax (SUTA)

Telephone federal excise tax

Telephone federal universal service fee tax

Telephone federal, state and local surcharge taxes

Telephone minimum usage surcharge tax

Telephone recurring and non-recurring charges tax

Telephone state and local tax

Telephone usage charge tax

Toll Bridge Taxes

Toll Tunnel Taxes

Traffic Fines (indirect taxation)

Trailer registration tax

Utility Taxes

Vehicle License Registration Tax

Vehicle Sales Tax

Watercraft registration Tax

Well Permit Tax

Workers Compensation TaxAre you dizzy yet?

The reality is that the American people are being drained in dozens and dozens of different ways.

But what did you expect?

Did you think that our politicians would pile up the biggest debt in the history of the world and never ask you to pay for it?

Did you think that we could run deficits equivalent to about 10 percent of GDP without ever seeing tax increases?

The truth is that the U.S. government needs a whole lot more money than even these new tax increases will bring in.

After all, it is being projected that the U.S. government will be spending $2 trillion on the interest on the national debt alone by the year 2020.

To put that in perspective, the entire budget for the U.S. government is less than $4 trillion for 2010.

Are you starting to get the picture?

In the years ahead the IRS is going to be digging deeper and deeper into our pockets and a gigantic chunk of that money is going to go directly into the pockets of those who own our debt.

But very few Americans wanted to listen when this problem was actually somewhat fixable 20 or 30 years ago.

So now we are all going to pay the price - literally.

Lindsey: U.S. entering deflation trap, to ease more

by Rie Ishiguro - Reuters

Former Federal Reserve board member Lawrence Lindsey said on Thursday it will be "obvious" by the end of this year that the U.S. economy has entered a "deflationary trap." "We know from (Fed) Chairman (Ben) Bernanke's recent comments that it is now at least a concern ... By the end of this year I think it will be quite clear," Lindsey said in an economic forum in Tokyo. "I would expect by December we will see further quantitative easing" by the Fed, he said.

Former Bank of Japan Governor Toshihiko Fukui said in the same forum that Japan will need a "considerable time" to overcome deflation as growth expectations remain subdued. "Deflation is a difficult issue. It is not something that can be wiped out in one stroke," he said. Fukui said the Japanese public has low growth expectations not only because of the declining population but also bulging public debt, which will need to be repaid in the future. "Japan will need to make persistent efforts to improve productivity and rebuild public finances for a considerable period of time to achieve its target (of beating deflation)," he said.

U.S. bank failures reach 102 so far this year

by Corbett B. Daly - Reuters

U.S. bank failures reached 102 so far in 2010 on Friday as regulators seized six small banks, a faster pace of closures than last year when the century mark was not reached until October. Bank failures are expected to peak this quarter, with the industry slowly recovering from large portfolios of bad loans, many tied to commercial real estate.

The banks seized on Friday were Sterling Bank of Lantana, Florida; Crescent Bank and Trust Company of Jasper, Georgia; Williamsburg First National Bank of Kingstree, South Carolina; Thunder Bank of Sylvan Grove, Kansas; Community Security Bank, New Prague, Minnesota and SouthwestUSA Bank of Las Vegas, Nevada, according to the Federal Deposit Insurance Corp. The largest of the six banks was Crescent Bank and Trust with 11 branches and about $1.01 billion in total assets and $965.7 million in total deposits. The smallest was Thunder Bank with two branches and just $32.6 million in total assets and $28.5 million in deposits.

The FDIC estimated the six failures would add about $394 million to the tab for its deposit insurance fund. The FDIC late last month gave an update on the overall health of the bank industry, saying it sees improvements, but economic threats are still lurking. The agency, which insures individual accounts up to $250,000, updated its estimates of the cost of bank failures, now expecting a $60 billion hit to its insurance fund from 2010 through 2014. The recovery of the community bank industry has lagged the bounceback of Wall Street and the healing in the overall economy. Iberiabank Corp agreed to assume all of the deposits of Sterling Bank, the FDIC said.

Time for true debate on Fannie and Freddie

by Gillian Tett - Financial Times

When the results of bank stress tests are released on Friday in Europe, there will be a flurry of hand-wringing about the capital hole – and who is going to plug it, or bear losses. But on the other side of the Atlantic, there is another black hole which badly needs to be discussed – this time in America’s huge government-sponsored enterprises, such as the housing giants Fannie Mae and Freddie Mac, and the interlinked Ginnie Mae and the Federal Housing Administration.

So far this year, this GSE issue has attracted scant political attention. Indeed – and astonishingly – the 2,300 page financial reform bill that President Barack Obama signed this week barely mentions these institutions at all. But back in 2008 the US government effectively nationalised Fannie and Freddie, under the fig leaf of a "conservatorship" scheme. And it has now used some $145bn of taxpayers’ money to prop them up, more than was spent on direct injections into the US banks or car sector.

Worse still, that bill will almost certainly rise further in the coming years. After all, the volume of outstanding mortgages backed by Fannie and Freddie now stands at $5,500bn, around half the mortgage market. GSE entities have acquired private-label mortgage bonds too. In theory, this is limited to top quality loans. In practice, though, there is almost certainly plenty of rot there too.

Thus (guess)timates about the size of the future taxpayer bill now range from $390bn (the Congressional Budget Office) to almost a trillion dollars (from some private sector economists.) It makes the woes of Spanish savings banks seem almost tame. So is there any chance of seeing a proper "stress test" on this exposure? Or exit strategy? Don’t bet on that soon.

These days, the GSEs are the only thing keeping the US mortgage and housing sector afloat, because private sector securitisation has effectively collapsed: last year, for example, nine out of 10 mortgages were underwritten by Fannie and Freddie. And, unsurprisingly, the Obama administration does not want to upset that apple cart by implementing radical reform. Nor does it want to undermine the value of mortgage-backed bonds, given how many of these the Federal Reserve itself now holds.

Nevertheless, behind the scenes – and almost against the odds – there is now pressure building for a proper debate. That is partly because some Republican politicians are hoping to use the issue as another weapon to attack the Obama administration. However, some bank lobby groups are also keen to start a debate about the GSEs, partly because they hope this could deflect attention from the failures of private banks.

It remains to be seen whether any of this gets beyond political posturing. However, judging from a consultation exercise now being organised by the US Treasury, there are some interesting ideas floating around. These essentially fall into two camps. Parts of the Republican party – and some private sector banks – want to remove the state subsidy for the GSE altogether. One idea submitted to the Treasury, for example, calls for banks to organise a mutual, private sector insurance scheme to guarantee mortgages, without state support.

However, a second strand of ideas calls for the state subsidy to be maintained, both to ensure stability in the short term – and to guarantee that the mortgage market remains liquid and homogenous in the long term. Sifma, the banking lobby group, for example, says that it is crucial to maintain the so-called "to be announced" sector, to give the market depth. However, insofar as the government supports the sector, it wants this support to be explicit and limited – unlike the status quo. It likes the idea, for example, of a state scheme to provide reinsurance for mortgage bonds against catastrophic loss.

Personally, in an ideal world, I would favour the first set of ideas, namely full privatisation. After all, it seems profoundly bizarre to have the state underpinning housing so deeply, in a country that espouses free market ideals. But, in practical terms, the second route is probably the only realistic platform for reform now. And if the state subsidy could at least be defined – and limited – that would certainly be a vast improvement on the current status quo.

After all, if there is one thing we have learnt in the past two years, it is that sooner or later investors tend to panic when they see a bottomless black hole of losses and fiscal fudge. That is why Europe is doing these stress tests today. But the fact that Washington has not yet learnt that lesson in relation to the GSEs is disappointing, to say the least. There now badly needs to be a proper debate about Fannie and Freddie – if not a public stress test too.

Fannie Mae and Freddie Mac: Unfinished business

by The Economist

Can the American mortgage market survive without taxpayer support?

The hefty financial overhaul that Barack Obama signed into law on July 21st left behind one big piece of unfinished business. In 2008 Fannie Mae and Freddie Mac, mortally wounded from losses on loans acquired during the bubble, were placed in “conservatorship”, a halfway house between bankruptcy and outright nationalisation. There they remain, their losses duly covered with new injections of capital by the Treasury—$145 billion so far. Tim Geithner, the treasury secretary, has promised to address the matter of Fannie and Freddie by early next year but so far he has no answers, only questions (literally so: in April he asked the public to comment on seven of them).

The hesitancy is understandable. Millstones though they are, the two firms remain critical to the economy. In the first quarter they and Ginnie Mae (which unlike Fannie and Freddie has always enjoyed the explicit backing of the state) guaranteed 96.5% of all newly originated mortgages, according to Inside Mortgage Finance, a newsletter.It is almost certain that the companies will no longer be allowed to hold a substantial in-house portfolio of securities. Yet the Treasury must still decide what to do with the $5 trillion in mortgages the companies guarantee. It could continue to pump money into the companies to cover losses on the loans as they mature; it could take explicit responsibility for them, inflating the national debt; or it could sell them to private investors.

The cost is apt to be high, regardless. Most of the losses of Fannie and Freddie result from mortgages originated before 2008. Mortgages originated in 2006 and 2007 account for 24% of Fannie’s business but 67% of its credit losses. In 2008 both firms began tightening their underwriting criteria and raising the fees they charge to guarantee mortgage-backed securities (MBS). Between 2007 and 2009 the proportion of their loans with a loan-to-value ratio of 70% or less rose from 31% to 49%, while the share with a loan-to-value ratio above 95% fell from 10% to 1%, according to the Federal Housing Finance Agency, their regulator.

At Freddie Mac 3.9% of mortgages originated in 2008 were at least 90 days delinquent at the end of March 2010. For mortgages originated in 2009, the equivalent figure was barely 0.1%, although renewed signs of weakness in the housing market may yet cause that figure to worsen. “We’ll be paying for the sins of the past for a long time, even though the current book of business is generating positive economic value,” says one official.

If Fannie and Freddie are making money now that they are pricing their insurance differently, this suggests that the private sector could do their job. (Ginnie Mae would continue to back loans to low-income families.) Michael Lea of San Diego State University notes in a recent paper that most other countries get by with far less government backing of mortgage finance, yet their home-ownership rates are not appreciably lower and none suffered as bad a housing crash.

Most reform proposals to date, however, still envisage a permanent federal backstop. Donald Marron and Phillip Swagel, two economists who served in the administration of George Bush, say the federal government should sell an explicit guarantee at a rate designed to recoup future losses to Fannie, Freddie or a purely private competitor. Wayne Passmore and Diana Hancock, economists at the Federal Reserve, similarly propose a government insurance fund that would sell guarantees for any asset-backed security. The Mortgage Bankers Association, a trade group, proposes that the government charter a new set of purely private mortgage insurers who would then have to buy backup federal insurance.

In America 60% of mortgages are securitised rather than kept on banks’ balance-sheets. That partly reflects Americans’ preference for 30-year fixed-rate mortgages that can be pre-paid without penalty—a difficult sort of asset for banks to hedge. The securitisation rate is more than twice as much as that in Canada, Spain and Britain, the next-highest countries. Defenders of a federal backstop say this leaves the American system uniquely vulnerable during a crisis, when investors will refuse to buy any MBS that lacks a government guarantee. Mr Swagel and Mr Marron argue that investors will, probably correctly, assume that the government will always intervene, so it makes sense to charge for that guarantee explicitly.

Ruling out a private-sector solution may be premature. Guy Cecala of Inside Mortgage Finance says the government could start to revive the private-label MBS market by gradually rolling back expanded limits on the size of loans it will guarantee. Other changes to the mortgage market, such as better underwriting, greater use of covered bonds and more adjustable-rate mortgages, would help reduce the need for a guarantee. That said, the private sector is too weak to do much right now. However unnecessary in the long run, the government’s dominance of the mortgage market will not end soon.

The next big task of financial reform: dismantling Fannie and Freddie

by The Economist

Diagnosis is often much simpler than treatment. The failures of Fannie Mae and Freddie Mac, America’s housing-finance giants, are glaringly obvious. The two firms, which own or guarantee more than half of the country’s $10.7 trillion of mortgages, are awash in red ink. The Congressional Budget Office reckoned in August 2009 that the twosome’s cost to taxpayers could go as high as $400 billion. With housing showing renewed weakness, that number may rise.

It is also easy to see why the firms got into such a mess. These “government-sponsored enterprises” (GSEs) occupied a grey area between state and private ownership, benefiting from an implicit government guarantee on their own debt at the same time as they sought to maximise profits for shareholders. That hybrid model granted the GSEs access to cheap funding and gave them the incentive to load their retained portfolios with subprime mortgages whilst maintaining capital levels scanty enough to make investment banks blush.

Although everybody agrees on the need to overhaul Fannie and Freddie, nobody is rushing to do much about it. America’s thumping financial-reform bill, which was signed into law by Barack Obama on July 21st, found room in its 2,319 pages to create “Offices of Minority and Women Inclusion” in various federal agencies, but did nothing on Fannie and Freddie. The two were taken into “conservatorship”, a form of government ownership, in 2008 and have been put to work ever since.

Virtually the only mortgages investors will buy are those guaranteed by the GSEs and other federal agencies. More than nine in every ten new mortgages written in America during the first quarter of 2010 were government-backed. Policymakers are horrified by this level of intervention and terrified about withdrawing it. The Treasury says it will put out proposals on the future of Fannie and Freddie early next year but there are few signs that politicians are prepared to get rid of them altogether.

They should. The GSEs’ mission is to provide “liquidity, stability and affordability” to America’s mortgage market. Set aside the fact that these aims tend to conflict: cheerleading for cheap mortgages is likely to produce instability, for example. The bigger question is why Fannie and Freddie are needed to achieve them. America’s obsession with home ownership is itself questionable, especially now that the trap of negative equity has hampered workers’ ability to move in search of jobs. Even if it were a valid goal, there are plenty of countries (Australia, Britain and Canada among them) that have similar or higher levels of home ownership with far less, and in some cases no, systemic government support.

As for liquidity, the argument that America needs Fannie and Freddie because private securitisation markets do not exist to take their place is circular. The GSEs have guidelines for the types of home loans they can guarantee: these let Fannie and Freddie colonise the safest, “conforming” bits of the mortgage market (before expanding into dodgier bits), leaving private lenders to swerve around them into ever-riskier areas. If the GSEs were not there to securitise and guarantee prime American mortgages, private firms would take their place.

A long goodbye, but goodbye nonetheless

There is still the fear that investors would flee the market in times of stress if they did not have a federal guarantee, implicit or otherwise. But other changes can sharply reduce that risk. Tighter underwriting standards would ensure that originators of loans remain disciplined: Britain’s plans for a more intrusive mortgage-lending regime provide one source of guidance. Better loan disclosure would help investors in mortgage-backed securities to do their own homework rather than just relying on guarantees. Funding instruments like covered bonds would give investors recourse to banks’ balance-sheets as well as the mortgages themselves in times of crisis.

None of this means it makes sense to get rid of Fannie and Freddie in one go. A gradual withdrawal is needed. The first step is to run off or sell their retained portfolios of mortgages. A second would be to squeeze the definitions of conforming mortgages over time, so that bit by bit Fannie and Freddie lose control of chunks of the prime market. American housing would, unfortunately, still have lots of props—agencies such as the Federal Housing Administration and subsidies like tax relief on mortgage interest. But the GSEs should go.

Fed Holds Mortgage Securities and a Dilemma

by Binyamin Appelbaum - New York Times

The Federal Reserve provided most of the money for new mortgages in the United States last year, effectively lending more than $1 trillion to American homeowners. Now the legacy of that extraordinary intervention is hanging over the central bank as it faces growing demands for an encore to help revive the flagging economy. While officials and economists generally regard the program as successful in supporting the housing market, it has left the Fed holding a vast pile of mortgage securities — basically i.o.u.’s from homeowners — that it does not want and cannot sell.

Holding the securities could cost the Fed a lot of money and hamper its ability to fight inflation, while selling the securities could drain needed money from the still-weak economy. Fed officials have expressed confidence that they can finesse the dilemma by gradually selling the securities as the economy starts to recover. But they are not eager to expand the challenge they face by beginning a new round of asset-buying, one tool the Fed could use to try to stimulate growth.

“In my view, any judgment to expand the balance sheet further should be subject to strict scrutiny,” Kevin M. Warsh, a Fed governor, said in a speech last month in Atlanta. He warned that new purchases could undermine the Fed’s “most valuable asset”: its credibility. Some Democrats want the Fed to pump more money into the economy to help reduce unemployment, one of the central bank’s basic responsibilities. In testimony before Congress this week, Chairman Ben S. Bernanke said that the Fed retained that option, but did not now plan to expand on the steps it had already taken.

In part, Bernanke and other Fed officials say they believe that new asset purchases would be less effective now that private investors have returned to the market. The Fed became one of the world’s largest mortgage investors because no one else was interested. During the fall 2008 financial crisis, investors stopped buying the mortgage securities issued by the housing finance companies Fannie Mae and Freddie Mac. The two companies buy mortgages made by banks and other lenders, providing money for new rounds of lending, then package those loans into securities for sale to investors, replenishing their own coffers.

Two days before Thanksgiving 2008, the Fed announced that it would buy $500 billion in securities issued by the two companies. By the time the program wound down in March 2010, it had spent more than twice that amount. The central bank now owns mortgage securities with a face value of $1.1 trillion. A wide range of economists say the Fed’s program — so big that purchases outstripped the issuance of new securities in some months — helped to preserve the availability of mortgage loans and helped to hold interest rates near record lows. Rates that exceeded 6 percent in late 2008 remain below 5 percent today.

But the Fed now must deal with the cleanup. The central bank could hold the securities until the borrowers repaid or refinanced their loans. Brian P. Sack, an executive at the Federal Reserve Bank of New York, estimated in March that borrowers would repay $200 billion by the end of 2011. And in the meantime, the Fed is collecting regular interest payments. “We’ve been earning a fairly high income from our holdings and remitting that to the Treasury,” Mr. Bernanke told Congress on Wednesday.

But holding the securities could make it harder to control inflation as the economic recovery gains strength, said Vincent Reinhart, the former head of the Fed’s monetary policy division, now a resident scholar at the American Enterprise Institute. The Fed bought the securities by pumping new money into the economy, stimulating growth. It could be difficult to reverse that effect without draining the money from the economy by selling the securities, Mr. Reinhart said.

“They created reserves, and those reserves ultimately can be inflationary,” Mr. Reinhart said. “The chief risk of keeping the balance sheet big and raising rates is that you might not be able to raise rates successfully” because the impact would be mitigated by the effect of the extra money still sloshing around the system. Holding the securities also could cost the Fed a lot of money. The Fed paid some of the highest prices on record for mortgage securities, basically accepting very low rates of interest on its investments. As the economy recovers and interest rates rise, the Fed will need to accept increasingly large discounts to make the securities attractive to other investors.

David Zervos, head of global fixed-income strategy at the investment bank Jefferies & Company, estimates that the value of the portfolio will drop almost $50 billion each time interest rates increase by one percentage point. Selling the securities at a loss would reduce the Fed’s ability to transfer profits to the Treasury Department. Large enough losses could reduce the amount of capital held by the Fed, although it can always create more money.

But perhaps the greatest risk is that investors will begin to doubt the Fed’s willingness to raise interest rates, knowing that each increase will damage its own balance sheet. “It compromises their integrity and their inflation-fighting mandate, because fighting inflation would be a direct detriment to their portfolio,” Mr. Zervos said. The Fed could avoid these problems by selling the securities now, before interest rates start to rise. But doing so would reverse the benefits of the original program, draining money from the economy while it still is weak. It would also fly in the face of the demands for the Fed to do more for the economy.

A fire sale also could damage the banking industry by driving down the value of the comparable mortgage securities that banks hold in large quantities. So far the Federal Open Market Committee, comprising the board of governors and a rotating selection of presidents from the regional reserve banks, has chosen to wait. The approach favored by most of the committee, according to the minutes of its June meeting, is to start raising interest rates before beginning to sell the securities. By waiting “until the economic recovery was well established,” the minutes said, the Fed would limit the impact of the asset sales on the broader market.

FDIC to Issue Bonds Backed by Residential Mortgages

by Jody Shenn - Bloomberg

The Federal Deposit Insurance Corp. plans to issue securities backed by about $500 million of home mortgages acquired from failed banks, leaning again on guarantees to help sell the debt. The FDIC will back about 85 percent of bonds created for the offering and it may not sell the deal’s junior-ranked notes, which will lose principal first amid any defaults on the underlying loans, David Barr, an agency spokesman, said. "The decision hasn’t been made yet," he said today in a telephone interview. "We may sell all or a portion of the certificates at some point in the future,"

The FDIC, which has closed more than 250 banks since 2008, began raising cash in the bond market for the first time since the early 1990s in March. The Washington-based agency that month sold $3.8 billion of guaranteed notes in three deals. As of May 31, the agency held about $32 billion of assets from failed banks excluding about $7.9 billion of interests in limited liability companies that it has also been creating to help offload its holdings, Barr said. Two of the FDIC’s March bond sales were backed by its loans to such companies, while the other transaction was a repackaging of existing mortgage bonds. Barr declined to discuss the timing of the latest sale. RBS Securities Inc. is underwriting the transaction.

The FDIC-backed debt is probably most comparable to atypical types of so-called agency mortgage bonds carrying government-backed guarantees, such as Washington-based Fannie Mae’s securities tied to multifamily mortgages, said David Land, a money manager at St. Paul, Minnesota-based Advantus Capital Management Inc., which oversees about $18 billion. An investor may want to accept similar yields as found with those types of securities, "depending on how much you value liquidity," Land said in a telephone interview.

FDIC insurance coverage upped permanently to $250K

by Sue Chang - MarketWatch

The Federal Deposit Insurance Corp.'s deposit insurance has been permanently raised to $250,000 per depositor as part of the Dodd-Frank Wall Street Reform and Consumer Protection Act. The insurance had been temporarily raised from $100,000 to $250,000 on Oct. 3, 2008. It was originally scheduled to expire on Dec. 31, 2010 but was temporarily extended to Dec. 31, 2013. "With this permanent increase of deposit insurance coverage to $250,000, depositors with CDs above $100,000 but below $250,000 will no longer have to worry about losing coverage on those CDs maturing beyond 2013," said FDIC Chairman Sheila Bair.

Seeing vs. Doing

by Gretchen Morgenson - New York Times

"What did they know, and when did they know it?" Those are questions investigators invariably ask when trying to determine who’s responsible for an offense or a misdeed. But for the Wall Street banks whose financing of the subprime mortgage machine placed them at the center of the credit crisis, it’s becoming clear that a third, equally important question must be asked: "What did they do once they knew what they knew?"

As investigators delve deeper into the mortgage mess, they are finding in too many cases that Wall Street firms did nothing when they learned about problem loans or improprieties in lending. Rather than stopping practices of profligate originators like New Century, Fremont and Ameriquest, Wall Street financiers, which held the purse strings for these companies, apparently decided to simply look the other way.

Recent cases have provided glimpses of this conduct. Last week, the Financial Industry Regulatory Authority accused Deutsche Bank Securities, a unit of the huge German bank, of misleading investors about how many delinquent loans went into six mortgage securities worth $2.2 billion that the firm underwrote. Deutsche Bank underreported the delinquency rates among loans when it created the securities in 2006, Finra contends, and then sold them to investors.

Deutsche Bank also understated historical delinquency rates in 16 subprime securities it packaged in 2007, Finra said. Even after it discovered the errors, the authority added, Deutsche Bank continued to report the misstated figures on its Web site, where investors checked the performance of past mortgage pools. Deutsche Bank settled without admitting or denying the allegations; it paid $7.5 million. The firm said Friday that it had cooperated and was pleased to have the matter behind it.

James S. Shorris, acting chief of enforcement at Finra, said that this was just the first of such cases and that he oversees a team of more than a dozen people investigating firms involved in mortgage securities. While the Finra case showed Deutsche Bank failing to report problem loans in its securities, investigators in other matters are learning that some firms used information about lending misconduct to increase their profits from the securitization game — without telling investors, of course.

Here is what investigators have learned, according to two people briefed on the inquiries who spoke anonymously because they were not authorized to discuss them publicly. The large banks that provided money to mortgage originators during the mania hired outside analytics firms to conduct due diligence on the loans that Wall Street bought, bundled into securities and sold to investors.

These analysts looked for loans that failed to meet underwriting standards. Among the flagged loans were those in which appraisals seemed fishy or the mortgages went to borrowers with credit scores far below acceptable levels. Loans on vacation properties erroneously identified as primary residences were also highlighted. The analysts would take their findings back to the Wall Street firms packaging the securities; the reports were not made available to investors. In 2006-07, amid the mortgage craze, more loans didn’t meet the criteria. But instead of requiring lenders to replace these funky mortgages with proper loans, Wall Street firms kept funneling the junk into securities and selling them to investors, investigators have found.

Cases brought against Wall Street firms by Martha Coakley, attorney general of Massachusetts, have brought some of these practices to light. "Our focus has been on the borrower," she said in an interview last week, "but as we’ve peeled back the onion we’ve gotten the picture of the role Wall Street played through the financing of these loans."

But some on Wall Street went further than simply peddling loans they knew were bad, according to the people briefed on some investigators’ findings. They say the firms used these so-called scratch-and-dent loans to increase their profits in the securitization process. When due-diligence reports turned up large numbers of defective loans — known as exceptions — the banks used this information to negotiate a lower price on the mortgages they bought from the original lenders.

So, instead of paying 99 cents on the dollar for the problem loans, the firm would force the lender to accept 97 cents or perhaps less. But the firm would still sell the mortgage pool to investors at 102 cents or higher, as was typical on high-quality loan pools. Wall Street enjoyed the profits these practices generated. And because lenders were financed by the Wall Street firms bundling the mortgages into securities, they were hesitant to reject too many dubious loans because doing so would slow the securitization machine.

For their part, Wall Street loan packagers were loath to imperil their relationship with lenders like New Century; as long as Wall Street’s lucrative mortgage factories were humming, it needed loans to stoke them. Forcing New Century to eat its bad loans might prompt it to take its business elsewhere. The bottom line: the more problematic the loans, the better the bargaining power and the higher the profits for Wall Street.

To be sure, the securities’ offering statements noted, in legalese, that the deals might contain "underwriting exceptions" and those exceptions could be "material." But as investigators get closer to understanding how Wall Street used these exceptions to jack up its earnings, that disclosure defense may ring hollow.

Muni ‘Race to Bottom’ May Cost Over $1 Trillion, Ex-L.A. Mayor Says

by Andy Fixmer and Christopher Palmeri - Bloomberg

U.S. cities and states may need more than $1 trillion of federal assistance in the next three years to stave off financial failure, former Los Angeles Mayor Richard Riordan said. Local governments are in a “race to the bottom” and U.S. taxpayers will inevitably be called on to bail them out, Riordan said in an interview at Bloomberg News’s Los Angeles office. The federal government should make pension, health-care and school reform a condition of receiving the aid, he said yesterday. “It’s not just L.A., it’s not just California, it’s all over the country, you’re going to see all these entities become totally insolvent,” Riordan said. “I think the federal government has to come in and have a list of what the states have to do to be saved.”

Riordan envisions incentives modeled on President Barack Obama’s “Race to the Top” aid to school districts. To receive funds, state and city officials should be prodded to cut public- employee pension benefits, renegotiate union work rules and add charter schools to improve student performance and save on costs, he said. Riordan said the need for federal help will be unavoidable and when it comes Obama will have to demand concessions from unions. “I think he would have zero chance of getting reelected if he didn’t,” Riordan said. States, recovering from the longest recession since the Great Depression, have projected budget deficits of $116 billion for fiscal 2011 and 2012, according to a report last month by the National Governors Association and the National Association of State Budget Officers.

Pension Funds

State public-employee pensions are underfunded by $438 billion and estimates using different accounting methods suggest a number as large as $3 trillion, according to an April report from theAmerican Enterprise Institute for Public Policy Research.States can't count on the federal government for more aid,Erskine Bowles, co-chairman of the National Commission on Fiscal Responsibility and Reform, said at the governors association meeting in Boston this month.

Investors won’t keep buying municipal debt to help cash- strapped cities and states finance operations, Riordan said. The 80-year-old Republican, who predicted insolvency for Los Angeles by 2014 in a Wall Street Journal commentary in May, said the city will have to declare bankruptcy to reduce its pension and health-care obligations to public employees. Politicians understand they won’t succeed in raising taxes to dig out of deficits, Riordan said. “If a government can’t sell bonds, they might as well close the door,” Riordan said. “If you can’t do that, you’re out of cash, you’re out of business.”

Borrowing Costs

Los Angeles paid a higher yield on $1.16 billion in short- term notes issued three weeks ago than it did on similar debt a year earlier, Riordan said. The notes were sold at yields of 0.55 percent to 0.85 percent, and underwriter J.P. Morgan Securities bought $252 million of the securities after buyers balked, City Administrator Miguel Santana said in a July 2 memo. California may experience similar difficulty in coming months when it seeks to borrow, Riordan said. He said he supports Republican Meg Whitman for governor in November over Democrat Edmund G. “Jerry” Brown. Riordan served as the mayor of Los Angeles from 1993 to 2001. Prior to entering public service, he started a law firm, Riordan & McKinzie, which was acquired by Los Angeles-based Bingham McCutchen in 2003, and private-equity company Riordan, Lewis & Haden, in 1982.

‘No Out-Sized Risk’

Los Angeles faced a financial crisis in April after the Department of Water & Power withheld a payment to the city and Controller Wendy Greuel said the nation’s second-largest metropolis by population would run out of cash in a month. Mayor Antonio Villaraigosa, a Democrat, has said Los Angeles will not declare bankruptcy as long as he is mayor. Some investors and analysts say odds of a wave of municipal defaults is low. “Even in a Draconian scenario such as the Great Depression, we believe that there is no out-sized risk in the municipal bond market,” Bijan Moazami, an insurance analyst with FBR Capital, said in a July 20 research note.

The Young and Jobless

Today marks the first anniversary of Congress's decision to raise the federal minimum wage by 41% to $7.25 an hour. But hold the confetti. According to a new study, more than 100,000 fewer teens are employed today due to the wage hikes. Economic slowdowns are tough on many job-seekers, but they're especially hard on the young and inexperienced, whose job prospects have suffered tremendously from Washington's ill-advised attempts to put a floor under wages. In a new paper published by the Employment Policies Institute, labor economists William Even of Miami University in Ohio and David Macpherson of Trinity University in Texas find a significant drop in teen employment as a direct result of the minimum wage hikes.

The wage hikes were implemented in three stages between 2007 and 2009, and not all states were affected because some already mandated a minimum wage above the federal requirement. But for the 19 states affected by all three stages of the federal wage increase, "there was a 6.9% decline in employment for teens aged 16 to 19," write the authors. And for those who had not completed high school, "we estimated that the hikes reduced employment by 12.4%," which translates to about 98,000 fewer teens in the work force.

After isolating for other economic factors and broadening their analysis to include all 32 states affected by any stage of the federal wage increase, the authors conclude that "the federal minimum-wage hikes reduced teen employment by 2.5% translating to approximately 114,400 fewer employed teens." Minimum wage proponents often claim that a higher wage floor will reduce poverty, ignoring that most minimum wage earners aren't poor. "A small fraction of minimum-wage workers are the sole breadwinner for their family," said Mr. Macpherson in an interview. "Historically, the number is one-in-six. So five-in-six are either secondary earners, or kids living with mom and dad, or kids living alone, such as college students."

Research by economists David Neumark and William Wascher has shown that minimum wage hikes also fail as an antipoverty measure because workers who receive the higher wage are counterbalanced by others who get laid off. Minimum wage laws are especially detrimental to black workers, who tend to be less experienced or have been trapped in failing public schools. The overall teen unemployment rate in June was 25.7%, versus 39.9% for black teens.

The NAACP and Congressional Black Caucus have been busy of late calling for various groups and government officials to apologize for perceived racial slights. Their energies would be put to better use urging the White House and Congress to lower the federal minimum wage, or at least to install a sub-minimum for teenagers. Our guess is that blacks of all ages would prefer a job to an apology.

G.M.’s Free Ride on the Government’s Dime

by Steven M. Davidoff - New York Times

Extra cash is not always a good thing for a corporation. This may be the case with General Motors. The theory is that managers should act in a disciplined manner in spending and operations. By limiting the amount of cash that a company has on hand, managers remain more focused and are less likely to take undue risks with their excess cash. This theory has been documented in a number of academic studies. Managers with too much cash to burn will burn too much cash. If you want a real-life example, simply read the beginning of "Barbarians at the Gate" and Ross Johnson’s epic struggle to spend all of the money that RJR Nabisco was throwing off in the 1980s.

G.M.’s announcement on Thursday that it was acquiring the subprime lender AmeriCredit for $3.5 billion may show that the automaker has stepped into this trap. With more than $35.7 billion in cash and marketable securities on its balance sheet as of the end of the first quarter of this year, G.M. is paying cash for AmeriCredit, something it certainly could not have done without the tens of billions of dollars that it received in government assistance. G.M. is also paying a 24 percent premium to AmeriCredit’s closing stock price on the day before the deal was announced.

If I were an owner of G.M., and I suppose I am in part as a taxpayer, I would wonder if that cash might not be better used as a special dividend to G.M.’s shareholders. Certainly, the fact that G.M. is spending $3.5 billion will be noticed by its unions and seen as a sign that there is cash available for them too. Still, many thought this was a good move by G.M. Only 4 percent of G.M’s buyers have subprime scores and it leases only 7 percent of its cars, The Wall Street Journal reports.

The acquisition allows G.M. to offer additional financing to subprime buyers and expand into a market that is now estimated to be 40 percent of American borrowers. Many analysts saw this as a particularly good move to beef up G.M.’s prospects in advance of a planned initial public offering of its stock. This would be all well and good were G.M. a private company. But it is not. Once you take into account the government ownership element, even more issues and problems emerge.

First, when G.M. owns a captive lender, it subsidizes the plants, labor unions and dealers. Captured finance means nonmarket financing for buyers when they receive a loan. Think zero percent financing. In connection with the acquisition, AmeriCredit will also re-enter the lease financing business, raising similar issues. Lease financing for automobiles usually results in artificial residual pricing for the buyout price at the end of the lease. All of this helps empty dealer lots and keeps plants running. But it oversupplies cars. The problem of artificially oversupplying new cars (like new houses) is put off for another day.

Second, the subsidy ensures that people who may not otherwise qualify to buy new cars do so. They overconsume and overspend as they shift their buying from used cars to new cars. This may be an immediate net gain for an economy in distress, but it may be a drag as well, as consumers divert income that could be used for other things that would perhaps create more wealth over all.

This problem for consumers is exacerbated by the fact that often these consumers do not fully understand the loans they are taking or the financing they receive for leases. G.M.’s maneuver highlights the importance of credit in car-buying decisions and also the problem of excluding auto dealers from the purview of the new consumer financial protection bureau in the just-enacted financial regulations. This was a clear mistake caused by political expediencies. The G.M. purchase of AmeriCredit underscores this.

Providing such cheap credit also ensures that subprime borrowers will continue to leverage up and borrow money when their best interests may be to deleverage. This may also conflict with the general attitude that the government should encourage in the long term: frugality versus debt. Instead, the American love affair with debt and cars is perpetuated. This cheap credit is also likely to subsidize the worst-selling automobiles (which are often the cars with the worst gas mileage) with the most favorable financing deals.

Third, this deal was done as an alternative to an acquisition of Ally Financial, the former GMAC. What prevented G.M. from buying Ally? Probably it was the cost of the deal and the complications of G.M. acquiring a large bank holding company. Normally, this would be Ally’s problem, but both companies are majority controlled by the government. The decision of G.M. not to buy Ally leaves the government in perhaps a stronger position with the automaker, but Washington is left with a $17.6 billion investment in Ally that looks more at risk.

This highlights the complications of government ownership and the conflicts that can emerge. It also highlights the hands-off approach that the government is taking. To those who accuse the Obama administration of socialism, if the government were really active here it would probably have pushed G.M. into a deal with Ally.

These problems show the issues associated with government ownership. Individual decisions may be good for G.M., but not as good for the country as a whole, throwing the dictate "what’s good for General Motors is good for the country" on its head.

The government has attempted to resolve this issue by taking a hands-off approach to General Motors. It has agreed with the company that its directors will be independent and The Journal reports that the Treasury Department was not involved in G.M.’s decision to acquire AmeriCredit. This may be for the best, since it allows G.M. to function independently and without the weight of these wider issues, which frankly should best be dealt with on a national level — to the extent that an increasingly sclerotic federal government can do so. The question still has to be asked: Would G.M. be doing this deal at all if it did not have government financing? The answer is an almost certainly no.

In the end, though, people should assess the deal as if the government’s stake in G.M. did not exist and instead the automaker was simply like any other private company. The acquisition of AmeriCredit makes more sense for G.M. in the near term and may even result in a greater near-term returns to the government as a shareholder if investors perceive this as enhancing the company’s future in any initial public offering. Some of this, though, is merely I.P.O. optics and P.R.

Whether it is in the long-term interest of G.M. to own a captive finance subsidiary and continue the debt-financed subsidizing of consumers so that they can overconsume new cars is less clear. G.M. may be again postponing a full resolution of its own problems. This may be a case of cash misspent.

Jobless Numbers Are Worse Than You Think

by Paul Godek - Wall Street Journal

In terms of employment, how bad is this recession? Last month's unemployment rate was 9.5%, according to the Bureau of Labor Statistics (BLS). But the jobs picture is even worse than that rate suggests. The BLS defines the jobless rate as the number of unemployed as a fraction of the labor force. If one person in a labor force of 10 people is unemployed, the unemployment rate is 10%. The problem is how the BLS counts the jobless. It defines the unemployed as those who are "out of work but have been seeking and are available for work."

Those out of work but not "seeking work" are not considered to be unemployed—and are thus not counted in the labor force. As one might imagine, the definition of "seeking work" is less than precise. According to the BLS, you are seeking work if you "have actively looked for work in the prior 4 weeks" (See the BLS Web site for the definition of "actively looking" for work.) Those without jobs and not seeking work—the people not considered to be in the labor force—are often referred to as "discouraged workers."

If people without jobs become discouraged and stop seeking work, the unemployment rate will decline (other things being equal). On the other hand, if people become hopeful about future employment, job seeking will go up—as will the unemployment rate. This way of measuring job availability is clearly flawed. One simple alternative would be to measure the labor force as the number of people with jobs. Unemployment would be determined based on increases or decreases in the number of people employed relative to historic job growth.

The number of nonfarm private jobs has been growing steadily since the 1950s. That number reached a peak at the end of 2007. Between 1958 and 2007, the number of U.S. jobs grew to 115.4 million from 43.5 million—about 2% per year on average. The steady upward trend reflects the long-run growth of the economy and increased participation in the labor force. The nearby chart compares employment and that trend. It shows the percentage difference between employment and the trend line generated from monthly employment figures over the past 50 years (July 1960 through June 2010).

What we see is astounding. For almost 25 years—between 1984 and late 2008—the level of employment never fell to more than 3% below the trend line. Over that period, total employment grew by more than 36 million. Employment fell briefly to about 6% below the trend during two previous recessions: in 1975 and again in 1982-1983. During those periods, the unemployment-rate peaks were 9% (in 1974) and 10.8% (in 1982). The unemployment rate in 2009 peaked at 10.1%.

By 2010, however, employment had fallen to about 10% below the trend, far below any previous level in the last half-century. These figures indicate that as of the first half of 2010, the economy has generated about 12 million fewer jobs than expected. In other words, things are not as bad now as they were in the early 1980s; they are much worse. Recall as well that the unemployment rate of the early 1980s was the result of the ultimately successful battle against inflation.

One message we're hearing often from Washington is that recent increases in government spending have averted another Great Depression. That's nonsense. If such policies had any coherence there would have been no Great Depression (when government spending grew); the U.S. economy would have collapsed following World War II (when government spending plummeted); and the U.S., not to mention Greece, would now be experiencing a boom like no other. As many observers of the economic scene have noted, private investment and hiring are suppressed by economic and political uncertainty. Such uncertainty is generated by unprecedented government intervention, massive increases in government spending, and anticipated tax increases. This is what the policies undertaken during the 1930s, those that sustained the Great Depression, should have taught us.

![[godek]](http://sg.wsj.net/public/resources/images/ED-AL908A_godek_NS_20100722182105.gif)

Seven European Banks Fail Stress Tests With $4.5 Billion Shortfall

by Jann Bettinga and Charles Penty - Bloomberg

Seven of the 91 European Union banks subject to stress tests failed with a combined capital shortfall of 3.5 billion euros ($4.5 billion), stirring concern the evaluations were too lenient. Hypo Real Estate Holding AG, Agricultural Bank of Greece SA and five Spanish savings banks have insufficient reserves to maintain a Tier 1 capital ratio of at least 6 percent in the event of a recession and sovereign-debt crisis, lenders and regulators said today.

The banks are in "close contact" with national authorities over the results and the need for more capital, said the Committee of European Banking Supervisors, which coordinated the tests. Governments are seeking to reassure investors about the health of financial institutions after the debt crisis pummeled the bonds of Greece, Spain and Portugal. "The amount of capital needed is much lower than the market expected," said Mike Lenhoff, London-based chief strategist at Brewin Dolphin Securities Ltd., whose parent company oversees $33 billion. "The amount does seem quite trivial considering the concerns about losses from the sovereign crisis."

Part of the reason the amount of capital needed was lower than analysts predicted may be because the evaluations took into account potential losses only on government bonds the banks trade, rather than those they are holding to maturity. That means the tests ignored the majority of banks’ holdings of sovereign debt. What’s more, European banks have raised 220 billion euros in the last 15 to 18 months, which dwarfs the amount of money that U.S. banks raised following their stress tests, Credit Suisse Group AG analysts said in a note this week.

Test Criteria

Still, estimates for the amount banks would need to raise ranged from 30 billion euros at Nomura Holdings Inc. to as much as 85 billion euros at Barclays Capital. Tests carried out in the U.S. last year found 10 lenders including Bank of America Corp. and Citigroup Inc. needed to raise $74.6 billion of capital. "The long awaited stress tests do not seem to have been that stressful after all," said Gary Jenkins, an analyst at Evolution Securities Ltd., in a note. "The most controversial area surrounds the treatment of the banks’ sovereign debt holdings." The results were released after the close of European stock markets. The euro was little changed against the dollar, falling 0.02 percent to $1.2896 as of 7:39 p.m. in London.

Bond Losses

Regulators tested portfolios of sovereign five-year bonds, assuming a loss of 23.1 percent on Greek debt, 12.3 percent on Spanish bonds, 14 percent on Portuguese bonds and 4.7 percent on German state debt, according to CEBS. The tests also assessed the impact of a four-step credit rating downgrade on securitized debt products, a 20 percent slump in European equities in both 2010 and 2011 and 50 other macroeconomic parameters, including an economic contraction in the EU, according to CEBS.

In Germany, Hypo Real Estate, the commercial-property lender rescued by the government following the financial crisis, was the only bank to fail among the 14 that were tested. Its capital ratio dropped to 4.7 percent in the most severe scenario, said the Bundesbank and the nation’s financial regulator, BaFin. The German bank has a capital shortfall of about 1.25 billion euros. An "immediate need for capital would arise only if the hypothetical stress scenario actually did materialize," the Bundesbank and BaFin said. Germany’s Soffin bank-rescue fund already provided Hypo Real Estate with more than 7 billion euros in funds through the end of June.

Spanish Banks

Agricultural Bank of Greece, 77 percent owned by the Greek state, reported a shortfall of 242.6 million euros and said it would proceed with a share capital increase. Spain, with 27 tested banks, makes up the biggest portion of the exams. The savings banks that failed were CajaSur; a merger group led by Caixa Catalunya; a group led by Caixa Sabadell; Caja Duero-Caja Espana, and Banca Civica. Spain’s largest bank, Banco Santander SA, maintained its Tier 1 capital ratio at 10 percent under the most stringent scenario.

The savings banks have a combined capital shortfall of about 2 billion euros, according to documents posted on the CEBS website. Bank of Spain Governor Miguel Angel Fernandez Ordonez said the central bank will set a deadline for savings banks to raise new capital privately, before turning to public funds. The end of the year would be a reasonable deadline, although it could be brought forward, he said. Banca Civica today announced plans to raise 450 million euros by selling bonds convertible into shares to J.C. Flowers & Co., a U.S. buyout firm.

Near the Threshold

Banks that showed a drop in capital to near the 6 percent threshold include Greece’s Piraeus Bank SA, with a ratio of 6 percent, Allied Irish Banks Plc, with 6.5 percent, Italy’s Monte Dei Paschi di Siena SpA, with 6.2 percent, and Nova Ljubljanska Banka in Slovenia, with 6.3 percent. Norddeutsche Landesbank, a German state-owned lender, and Deutsche Postbank AG, the German retail bank partially owned by Deutsche Bank AG, reported ratios of 6.2 percent and 6.6 percent, respectively, in the sovereign-shock scenario.