"Heat wave. Free ice in New York"

Ilargi: The pressure on state and muni bonds is increasing, and we haven't even entered the first inning of that one, the players are still tossing balls in the outfield.

David Goldman writes in the Asia Times that everyone who needs to be, will eventually be bailed out:

The Bank-Insurance-Municipal Daisy Chain (Why the Federal Government Will Bail Out the States and Municipalities)If municipal debt actually defaulted, the capital position of the banking system would be impacted, bank preferred debt might stop paying, and the holders of bank preferred debt–starting with the insurers–would be in serious trouble. The $800 billion bailout package for Europe’s PIIGS (Portugal, Ireland, Italy, Greece, Spain) in May was in fact a bailout for the banking system, which holds hundreds of billions of dollars worth of such debt. [..]

It’s a pretty safe surmise that the global banking system’s holdings of non-US government debt is not much different than the profile of American banks’ purchases of US government debt.[..]

Why buy munis? For all of Warren Buffett’s dire warnings about municipal finances, the fact is that the federal government can’t let major municipal debtors (at the level of states, for example) go under without also bringing down the banking system and everything else.

If it goes, it all will go together. That’s why munis ultimately will be bailed out. A Democratic administration whose core constituency is public employee unions will do everything in its power to keep them happy (and a Republican Congress, which we likely will have in 2011, may frustrate this). But ultimately it’s a matter of survival.

Ilargi: Now that sounds nice and all, but it still has to be practically possible, just to name a minor detail. I for one would like to see explained what mechanism would be used for such a bail-out, who decides how much money to send to all 10,000+ places that will claim to need it etc. Or will the Fed and Treasury simply buy up all the paper it can find? There'd be a few issues with that one as well. Or will all counties and towns get to issue new paper and send it directly to Washington in exchange for cash? What would that mean for the value of existing bonds?

A second problem, of course, is the sheer amount of money involved in such purchases. Will a) the people and b) the Republican Party react favorably? In the run-up to such largesse, the lower level governments will still have to continue pink-slipping their employees on a grand scale. it will therefore become real obvious that the hundreds of billions spent are nothing but another bank bail-out, not exactly the easiest political topic anymore.

Bloomberg's Dakin Campbell notes that the state and local government debt market presently stands at $2.8 trillion. That's real money. And it doesn't have to go down that much either:

U.S. Banks Risk 'Untold Problem' as Muni Debt SwellsCitigroup had an unrealized loss of $1.8 billion in the third quarter of 2008, when the municipal market sank 3.8 percent. [..]

In 2009, state and local government debt rose 14.5 percent. U.S. states are likely to face $140 billion in cumulative budget gaps in the coming year, according to the Center on Budget and Policy Priorities. Last year, 187 tax-exempt issuers defaulted on $6.4 billion of securities, the most since 1992, according to data from Distressed Debt Securities in Miami Lakes, Florida.

“It’s a market where it’s clear that the underlying fundamentals are lousy,” said Michael Aronstein, chief investment strategist at Oscar Gruss & Son Inc.[..]. “People can say fundamentals don’t matter but I’ve been doing this for 32 years. They do.”

Ilargi: Campbell cites a lot of banks whose spokesmen declare that they have little exposure to the muni market, and what they have is only of the highest quality (Always is, after all; these are the smartest people in the world). He also says that lenders hold only 8% of the total $2.8 trillion market. So who holds the rest? Maybe you should ask your pension fund manager about that.

Warren Buffet said a month ago before the Financial Crisis Inquiry Commission that there would be a “terrible problem” for municipal bonds. He wasn't kidding. Tax revenues will keep on falling, forcing huge numbers of lay-offs, which in turn will lead to lower tax revenues as well as foreclosures, which in turn also lead to lower tax revenues.

This is a circle that won't be broken for years to come. And if the Federal government decides to bail out states and munis, will that raise those revenues, being back jobs, keep people in their homes? No, of course not, it will only (and only temporarily) help those who hold the bonds.

But if the government decides not to do another bail-out, markets will push banks and other large investors to take a giant haircut (think: lawn mower size), which will threaten to topple the entire financial system.

There is no way out of this. But step one should be to let investors take the losses that come with the risk of the assets they've invested in. Instead of loading the public up with those losses as well, on top of those incurred by their pension funds, and on top of all the lost jobs and services that now lie inevitably ahead of us, just around the corner. Given the history of the last few administrations nad their bail-outs, it's not hard to guess who will be forced to pay the piper. And still be left holding an empty bag.

Sovereign Debt: The Death of Nations vs. the Wealth of Nations

by Damon Vrabel - Zero Hedge

The gap between the truth vs. the lies that pass for truth in the media has never been so wide. But living a lie is very destructive, so it’s important to cross this gap. Today I want to clear up one of the most important lies reinforced by the media–the idea that we have sovereign countries.

No doubt most of you have heard of the sovereign debt crisis that so many countries are facing. We hear endless economists, reporters, and billionaire hedge fund raiders talk about it. But the phrase they use is fictitious. It is a fabrication of the Ivy League, Wall Street, and erudite periodicals like the Financial Times of London. Sovereign debt is an impossibility. It cannot exist.

It seems ridiculous to point this out, but sovereign debt implies sovereignty. Right? Well, if countries are sovereign, then how could they be required to be in debt to private banking institutions? How could they be so easily attacked by the likes of George Soros, JP Morgan Chase, and Goldman Sachs? Why would they be subjugated to the whims of auctions and traders?

A true sovereign is in debt to nobody and is not traded in the public markets. For example, how would George Soros attack, say, the British royal family? It’s not possible. They are sovereign. Their stock isn’t traded on the NYSE. He can’t orchestrate a naked short sell strategy to destroy their credit and force them to restructure their assets. But he can do that to most of the other 6.7 billion people of the world by designing attack strategies against the companies they work for and the governments they depend on.

The fact is that most countries are not sovereign (the few that are are being attacked by CIA/MI6/Mossad or the military). Instead they are administrative districts or customers of the global banking establishment whose power has grown steadily over time based on the math of the bond market, currently ruled by the US dollar, and the expansionary nature of fractional lending. Their cult of economists from places like Harvard, Chicago, and the London School have steadily eroded national sovereignty by forcing debt-based, floating currencies on countries. So let’s start being honest and stop describing their debt instruments as sovereign.

We long ago lost the free market envisioned by Adam Smith in the "Wealth of Nations." Such a world would require sovereign currencies, i.e. currencies that are well-regulated rather than floating, and an asset rather than an interest-bearing debt. Only then could there be a "wealth of nations." But now we have nothing but the "debt of nations." The exponential math of debt by definition meant that countries would only lose their wealth over time and become increasingly indebted to the global central banking network.

So thanks to debt-based, free-floating currencies, the "wealth of nations" transitioned to the "debt of nations" which is now transitioning to the "death of nations." The new world economic order with one currency, one banking system, one government, and one integrated corporate empire is on the horizon. Perhaps that’s a good thing, but if it were, why would the establishment concoct oxymorons like "sovereign debt" instead of telling the truth? That’s my only goal here–I think people can be trusted with the truth. Lies harm not only the population hearing them, but also the powerful people telling them.

Those powers have the best salesmen in the world, so why don’t they just sell the population on the truth? Apparently they don’t think you’d like it. Well now you have it. And it’s coming unless countries follow Iceland’s lead and recover their sovereignty. The choice is ours.

U.S. Banks Risk 'Untold Problem' as Muni Debt Swells

by Dakin Campbell - Bloomberg

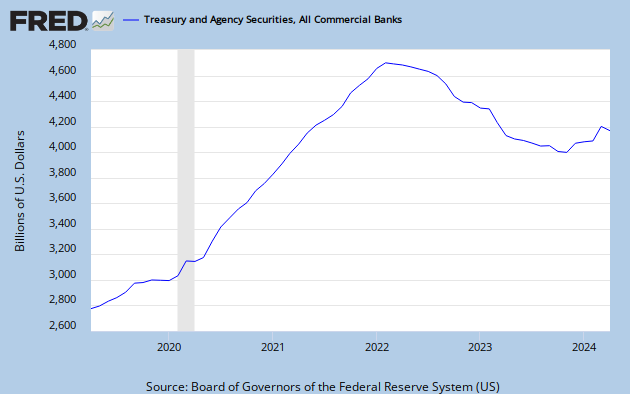

Citigroup Inc., State Street Corp. and U.S. Bancorp are among U.S. banks whose municipal bond holdings have reached a 25-year high just as state budget deficits swell to $140 billion, the most since the start of the recession. Commercial lenders added more than $84 billion to their holdings since 2003, according to the Federal Reserve, pushing total investments to $216.2 billion at the end of the first quarter. Bank regulators and ratings companies are ramping up scrutiny of banks most at risk of being forced to raise more capital should debt prices slide.

"There is a huge untold problem here," said Walter J. Mix III, a former commissioner of the California Department of Financial Institutions who closed 30 banks during the last banking crisis in the 1990s. "The economics lead to the conclusion that there will be downward pressure on these bonds." At Cullen/Frost Bankers Inc., the biggest Texas lender, holdings of municipal debt exceeded Tier 1 capital, a key measure of a bank’s ability to absorb losses, by $491 million at the end of the first quarter, data compiled by Bloomberg show. For State Street, based in Boston, the holdings make up 50 percent of Tier 1 capital. U.S. Bancorp, the Minneapolis lender, has a ratio of 28 percent. It’s 11 percent at Citigroup, the data show.

Municipal Bond Yields

Default speculation and a move by investors to the safest securities drove municipal bond yields to a 13-month high relative to U.S. Treasuries in the first half of the year. Now, the Federal Deposit Insurance Corp. has asked analysts to look into the issue, according to spokeswoman Michele Heller. The 9.5 percent U.S. unemployment rate and slump in property prices have slashed local governments’ ability to pay bills. Billionaire investor Warren Buffett, speaking at a June 2 hearing of the Financial Crisis Inquiry Commission in New York, predicted a "terrible problem" for municipal bonds. Buffett has said a U.S. state facing default may need a federal rescue.

Analysts and investors remain divided about the level of risk. Lenders hold just 8 percent of the $2.8 trillion state and local government debt market, and municipal bonds are only about 2 percent of total bank assets, according to the Fed.

‘Train Wreck’

"The open issue is whether it’s a slowly emerging train wreck," said Jeff Davis, an analyst at Guggenheim Securities LLC, a unit of Guggenheim Partners LLC, whose executive chairman is former Bear Stearns Cos. Chief Executive Officer Alan D. Schwartz. "It’s hard to paint all general obligation and all revenue bonds with the same brush. The portfolios won’t go to zero." Municipal defaults are a slender risk, according to Moody’s Investors Service, which said in a February report that the investment-grade rate during the past four decades was 0.03 percent, compared with 0.97 percent for similar corporate issues. Investors eventually recoup an average of 67 cents on the dollar for defaulted municipal bonds.

While the historical default-rate risk for municipal debt is below corporate obligations, sudden declines in prices have already created losses at some banks. Citigroup had an unrealized loss of $1.8 billion in the third quarter of 2008, when the municipal market sank 3.8 percent, the biggest quarterly decline since 1994, company filings and Bank of America Merrill Indexes show. The loss was deducted from the firm’s equity.

Citigroup

"Citi’s exposure to the municipal market is of the highest quality," Danielle Romero-Apsilos, a spokeswoman for the New York-based firm, said in a statement. "We conduct rigorous stress tests under a variety of scenarios and are comfortable with our position." Citigroup had the largest municipal holdings among the biggest banks as of March 31, with $13.4 billion of state and local government bonds, according to FDIC call reports. That’s down from $13.8 billion at the end of last year. Bank of America Corp. held $8.5 billion, Wells Fargo & Co. owned $7.6 billion and JPMorgan Chase & Co. held $4.5 billion. Each accounted for less than 8 percent of Tier 1 capital, according to the FDIC.

Bank of America, based in Charlotte, North Carolina, has made "significant progress" boosting capital and reducing risk-weighted assets, spokesman Jerry Dubrowski said. The lender trimmed its municipal investments by more than $800 million in the first quarter. JPMorgan spokeswoman Jennifer Zuccarelli didn’t return a call for comment.

Wells Fargo

Wells Fargo, based in San Francisco, boosted its municipal holdings by more than $2 billion in the first quarter, data compiled by Bloomberg show. The investments are in municipalities "we know very well," Chief Financial Officer Howard Atkins said on May 13. State Street, the second-largest independent custody bank, owned $6.2 billion of state and local government debt at the end of March, the data show. State Street is "very comfortable" with its portfolio and has had no material credit issues, spokeswoman Carolyn Cichon said. At Minneapolis-based U.S. Bancorp, which owned $6.6 billion of municipal bonds, spokeswoman Jennifer Wendt also declined comment.

Cullen/Frost, which says it’s the only one of the 10 biggest Texas banks to survive the 1980s savings-and-loan crisis, is "extremely comfortable" with the municipal investments, CFO Phillip Green said in a July 1 interview. The 142-year-old lender, based in San Antonio, bought $1 billion of municipal bonds in the 12 months through February, Green said that month. Most were issued by Texas school districts and insured by the state’s Permanent School Fund guarantee program, he said in last week’s interview. Municipal debt gained 2 percent in the second quarter underperforming Treasuries by 2.7 percentage points, according to Bank of America Merrill indexes. In 2009, state and local government debt rose 14.5 percent.

U.S. states are likely to face $140 billion in cumulative budget gaps in the coming year, according to the Center on Budget and Policy Priorities. Last year, 187 tax-exempt issuers defaulted on $6.4 billion of securities, the most since 1992, according to data from Distressed Debt Securities in Miami Lakes, Florida. "It’s a market where it’s clear that the underlying fundamentals are lousy," said Michael Aronstein, chief investment strategist at Oscar Gruss & Son Inc., a New York- based brokerage. "People can say fundamentals don’t matter but I’ve been doing this for 32 years. They do."

The Bank-Insurance-Municipal Daisy Chain (Why the Federal Government Will Bail Out the States and Municipalities)

by David Goldman - Asia Times

Bank preferred debt, I argued on March 1, 2009, would not be allowed to go under after the fashion of Fannie and Freddie preferred, because shutting off payment on bank preferreds would ruin the insurance industry. Credit protection on the insurers was trading at over 1,000 basis points above LIBOR that week, which marked the nadir for the banks. As I wrote then,…the global insurance industry took down 40% or more of the commercial bank "hybrid" Tier I capital securities issued in the past six years, or over $320 billion of the $800 billion float. That’s not counting preferred stock and other yield-hog favorites. Haircut these bonds, and the insurers will do the dead man’s float. AIG isn’t the only insurance company that wrote protection for the banks (although it was the most aggressive).That’s why the federal government has no choice but to bail out AIG, and no choice but to bail out the banks — unless it wants to let the insurers go down, or separately bail them out. Banks and insurers are tied together in a daisy-chain in which all survive or all fail.

Of course, were insurers to let it be known that whole life insurance policies aren’t paying quite what they expected to, or that they might have to stagger life insurance payouts over time, the result would be a level of panic that the Obama administration doesn’t want to think about. Pension plans already are cutting payments because of the commercial mortgage disaster. Word is getting around: nothing is safe. Your bank deposits might be safe, but not your pension, or your insurance policy, or your annuity.

The same applies with a vengeance to the banks and municipal debt. As Bloomberg reported yesterday, the banking system owns well over $200 billion in municipal bonds:Citigroup Inc., State Street Corp. and U.S. Bancorp are among U.S. banks whose municipal bond holdings have reached a 25-year high just as state budget deficits swell to $140 billion, the most since the start of the recession.Commercial lenders added more than $84 billion to their holdings since 2003, according to the Federal Reserve, pushing total investments to $216.2 billion at the end of the first quarter. Bank regulators and ratings companies are ramping up scrutiny of banks most at risk of being forced to raise more capital should debt prices slide.

"There is a huge untold problem here," said Walter J. Mix III, a former commissioner of the California Department of Financial Institutions who closed 30 banks during the last banking crisis in the 1990s. "The economics lead to the conclusion that there will be downward pressure on these bonds."

At Cullen/Frost Bankers Inc., the biggest Texas lender, holdings of municipal debt exceeded Tier 1 capital, a key measure of a bank’s ability to absorb losses, by $491 million at the end of the first quarter, data compiled by Bloomberg show. For State Street, based in Boston, the holdings make up 50 percent of Tier 1 capital. U.S. Bancorp, the Minneapolis lender, has a ratio of 28 percent. It’s 11 percent at Citigroup, the data show.

If municipal debt actually defaulted, the capital position of the banking system would be impacted, bank preferred debt might stop paying, and the holders of bank preferred debt–starting with the insurers–would be in serious trouble. The $800 billion bailout package for Europe’s PIIGS (Portugal, Ireland, Italy, Greece, Spain) in May was in fact a bailout for the banking system, which holds hundreds of billions of dollars worth of such debt. We don’t know quite how much, because European banks don’t have the same reporting requirements as American banks (and American banks’ overseas branches don’t have the same reporting requirements as their domestic branches).It’s a pretty safe surmise that the global banking system’s holdings of non-US government debt is not much different than the profile of American banks’ purchases of US government debt.

Banks are shedding non-government, i.e., corporate risk in their securities portfolios at the same time:

Why buy munis? For all of Warren Buffett’s dire warnings about municipal finances, the fact is that the federal government can’t let major municipal debtors (at the level of states, for example) go under without also bringing down the banking system and everything else.

If it goes, it all will go together. That’s why munis ultimately will be bailed out. A Democratic administration whose core constituency is public employee unions will do everything in its power to keep them happy (and a Republican Congress, which we likely will have in 2011, may frustrate this). But ultimately it’s a matter of survival.

Expect lots of government layoffs at state, local level

by Paul Davidson, USA TODAY

Here's another headwind for a sputtering job market: State and local governments plan many more layoffs to close wide budget gaps. Up to 400,000 workers could lose jobs in the next year as states, counties and cities grapple with lower revenue and less federal funding, says Mark Zandi, chief economist for Moody's Economy.com. The development could slow an already lackluster recovery. Friday, the Labor Department said employers cut 125,000 jobs, mostly because 225,000 temporary U.S. Census workers completed their stints. The private sector added 83,000 jobs, fewer then expected, as the jobless rate fell to 9.5% from 9.7%.

Layoffs by state and local governments moderated in June, with 10,000 jobs trimmed. That was down from 85,000 job losses the first five months of the year and about 190,000 since June 2009.

But the pain is likely to worsen. States face a cumulative $140 billion budget gap in fiscal 2011, which began July 1 for most, says the Center on Budget and Policy Priorities. While general-fund tax revenue is projected to rise 3.7% as the economy rebounds in the coming year, it still will be 8%, or $53 billion, below fiscal 2008 levels, according to the National Association of State Budget Officers.

Meanwhile, federal aid is shrinking. Money for states from the economic stimulus is expected to fall by $55 billion, says the National Governors Association. And the Senate last week failed to pass a measure to provide states $16 billion for extra Medicaid funding, an initiative that would have extended benefits from last year's stimulus. The House approved $25 billion in enhanced Medicaid funding. Philippa Dunne, who surveys state financial officials for a newsletter, the Liscio Report, says most plan to intensify layoffs the coming year after relying largely on furloughs. "The downturn has gone on so long, all the low-hanging fruit has been taken," says Scott Pattison, head of the state budget officers group.

Wells Fargo economist Mark Vitner expects state and local governments to cut about 200,000 workers this year if Medicaid benefits aren't extended. That's largely why Wells Fargo cut forecasts for third-quarter economic growth to 1.5% from 1.9%. Even if Congress extendsMedicaid subsidies, Zandi expects 325,000 job cuts the next year, though Vitner says losses could be far less.

Among cuts planned and made:

- New York City is planning 4,500 layoffs, and more if the Medicaid subsidies aren't approved, says the Center on Budget and Policy Priorities.

- Washington state would have to chop 6,000 jobs without the Medicaid money.

- The city of Maywood, Calif., laid off all 68 of its employees July 1 and is contracting out police services, partly because of a $450,000 budget deficit.

It's Time For A Marshall Plan To Save Disastrous State Budgets

by The Mad Hedge Fund Trader

On a map, it appears that the United States is made up of 50 states. The fiscal reality is that we have 20 Portugal's, 15 Italy's, 10 Irelands, 3 Greece's, and 2 Spain's. In Q1, state and local GDP shrank by 3.8%, chopping growth at the national level by 0.5%, the sharpest drop since that last year from hell, 1981. States are shoveling money out of the economy nearly as fast as Obama is shoveling it in.During the bubble, the states thought incomes were higher than they really were, were richer than they really were, and bulked up on services as if the party would go on forever. As a result, services grew faster than the economy for many years, especially when it came to building new prisons. Because of the ephemeral nature of property and stock gains, that movie now has to run in reverse, and state services have to shrink down to what they can afford. During the last two recessions, state and local governments hired, easing some of the pain at the local level.

Not this time. Teachers, policemen, and firemen have been laid off with reckless abandon, the oldest and most expensive usually targeted to go first. Obama is going to have to come up with some sort of "Marshall Plan" for the states to enable them to transition out of their structural deficits towards fiscal soundness. Target number one is going to have to be entitlements, primarily state employee pension payments, which in many cases now exceed those in the private sector. The headache is so huge that it is mathematically impossible for any tax increase to address the shortfall alone.

No action now brings slower economic growth, fewer jobs, and a paucity of votes in November. This is all one reason why I am pounding the table for a long term growth rate of 2%-2.5% which the financial markets have only recently started to embrace.

Richard Suttmeier: US Home Prices Could Fall Another 50%

by Peter Gorenstein - Yahoo

The housing market continues to deteriorate. Thursday's report on May pending home sales was down 30% from the prior month and nearly 16% vs. a year ago. The market weakness spans the country. Sales in the Northeast, Midwest and South fell more than 30%, the bright spot, the West, only fell 21%. The news comes after last week's record low new home sales in May, which plummeted nearly 33%. Experts say the expiration of the new homebuyer tax credit is to blame for the sudden market softness.

Unfortunately, the market could get worse and prices could fall further, says Richard Suttmeier of ValuEngine.com. High unemployment and struggling community banks are two main causes. Saddled with bad housing and construction loans, local banks will continue to restrict lending. Plus, the failure of the Obama administration's mortgage modification program means a steady flow of short sales. "People are going to be surprised when they see there have been short sales," which negatively impact appraisals in the local community, says Suttmeier.

How low can prices go?

Using the S&P/Case-Shiller index as his guide, Suttmeier suggests homes across the country could lose half their value. "If it gets back, like stocks, back to the 1999-2000 levels, that’s another 50% down in home prices," he says.

Why British house prices must fall by 25% or more

by Ian Cowie - Telegraph

An increase in the supply of properties for sale helped reduce house prices marginally by 0.6 per cent this month, according to Halifax. But, while Britain’s biggest mortgage lender predicts prices will end the year "broadly unchanged" much bigger falls are likely as the coalition government presses ahead with the biggest spending cuts in living memory and rising unemployment brings tens of thousands of new forced sellers into the market.

Some estate agents report that the number of properties for sale has already increased by more than a fifth since last year. Nigel Lewis, property analyst at online estate agents FindaProperty.com, said: "It is no surprise that the latest Halifax house price index shows a dip in house prices; our own figures show that there has been an influx of stock over the past few months which has served to drive prices down.

"There are currently 23 per cent more properties for sale on our site than there were a year ago and this imbalance between supply and demand is now affecting pricing. We are reverting back to a buyer’s market and therefore sellers must vie for their attention with more competitive prices." That makes a change from estate agents trying to talk prices up. But, confronted supply rising more rapidly than demand, most market commentators remain determined to avoid the obvious conclusion about what this must mean for prices.

As usual at market turning points, the most comforting option is to forecast a soft landing. For example, Catherine Penman, head of research at property consultants Carter Jonas, said: "What is clear from the latest Halifax figures and last week’s figures from Nationwide, is that any thoughts being entertained that the housing market was through the worst and well on the road to recovery were a touch premature. "The price gains at the start of the year were never likely to continue, with a market underpinned by a scarcity of good stock rather than a healthy flow of buyers and sellers, and with public sector cuts and higher taxes looming on the horizon, we are likely to see price stagnation for the remainder of the year."

Similarly, Martin Ellis, housing economist at Halifax, said: "House prices fell by 0.6% in June following a similar decline in May. Prices in the April to June quarter were largely unchanged compared with the first three months of the year. This pattern is in line with our view that house prices will be broadly unchanged over 2010 as a whole. "A shortage of properties for sale in 2009 contributed to an imbalance between supply and demand and was a key factor driving up house prices last year. An increase in the number of properties available for sale in recent months has helped to reduce the imbalance, relieving the upward pressure on prices. The low level of interest rates, however, continues to support housing demand."

Nobody expects interest rates to rise soon. But what will happen to demand when they do rise? More importantly, what will happen to supply when tens of thousands of new public sector jobs created by the last government are cut by the coalition as it struggles to reduce budget deficits? Even if we suffer a double-dip recession, most homeowners will sit out this downward correction, comforting themselves with the knowledge that their properties often gained more in value than their owners earned after tax in the good years. But rising numbers of buyers will no longer have that option if their income is terminated and they cannot afford to meet monthly bills. Some may feel forced to sell at almost any price; others will simply send the keys back.

House prices have fallen by less than a fifth – 17 per cent to be precise, as measured by Halifax – from the all-time peak they reached in August, 2007. The obvious conclusion is that they have much further to fall. A decrease of about 25 per cent in prices would bring them into line with the increase in supply we have already seen. But government spending cuts mean more sellers look set to enter the market, depressing prices further.

Initial claims drop last week but remain high

by Christopher S. Rugaber - AP

New claims for unemployment benefits dropped sharply last week, signaling that layoffs are slowing but not enough to signal strong job creation. The Labor Department said Thursday that requests for jobless aid dropped by 21,000 to a seasonally adjusted 454,000. The decline takes claims to their lowest level since early May, erasing the increases of the last two months. But even as first-time claims fall, the number of unemployed Americans receiving benefits is dropping sharply because their aid is ending.

About 350,000 people saw their benefits cut off in the week of June 19 after Congress left for weeklong recess without extending federal jobless aid. That brings the total to about 1.6 million people who have had their benefits end since May. Those numbers could reach 3.3 million by the end of the month if Congress doesn't pass an extension when it returns from recess. Initial claims have fluctuated in recent weeks. They have remained stuck near 450,000 all year, after dropping steadily last year from a peak of 651,000 in March 2009.

The four-week average of claims dropped slightly to 466,000. In a healthy economic recovery with rapid hiring, claims usually fall below 400,000. The tally of people continuing to claim benefits plunged by 224,000 to 4.4 million, the department said. But that doesn't include another 4.6 million people who received extended benefits paid for by the federal government in the week ended June 19, the latest data available.

The number of people receiving extended benefits is dropping quickly. During the recession, Congress added up to 73 weeks of extra benefits on top of the 26 weeks typically provided by states. But those extensions expired in late May, leaving about 1.6 million people without unemployment insurance, according to the Labor Department. That figure is expected to grow to 3.3 million by the end of this month. Democrats in the House and Senate are seeking to renew the extended benefits and continue them through November. But Senate Republicans have blocked the extension, citing deficit concerns.

Federal Reserve weighs steps to offset slowdown in economic recovery

by Neil Irwin - Washington Post

Federal Reserve officials, increasingly concerned over signs the economic recovery is faltering, are considering new steps to bolster growth. With Congress tied in political knots over whether to take further action to boost the economy, Fed leaders are weighing modest steps that could offer more support for economic activity at a time when their target for short-term interest rates is already near zero. They are still resistant to calls to pull out their big guns -- massive infusions of cash, such as those undertaken during the depths of the financial crisis -- but would reconsider if conditions worsen.

Top Fed officials still say that the economic recovery is likely to continue into next year and that the policy moves being discussed are not imminent. But weak economic reports, the debt crisis in Europe and faltering financial markets have led them to conclude that the risks of the recovery losing steam have increased. After months of focusing on how to exit from extreme efforts to support the economy, they are looking at tools that might strengthen growth. "If the economic situation changes, policy should react," James Bullard, president of the Federal Reserve Bank of St. Louis, said in an interview Wednesday. "You shouldn't sit on your hands. . . . I think there's plenty more we could do if we had to."

One pro-growth strategy would be to strengthen language in Fed policy statements that the central bank's interest rate target is likely to remain "exceptionally low" for an "extended period." The policymakers could change that wording to effectively commit to keeping rates near zero for even longer than investors now expect, perhaps adding specifics about which economic conditions would lead them to raise rates. Such a move would be opposed by many members of the Fed policymaking committee who are wary of the "extended period" language, arguing that it limits their flexibility.

Another possibility would be to cut the interest rate paid to banks for extra money they keep on reserve at the Fed from 0.25 percent to zero. That would give banks slightly more incentive to lend money to customers rather than park it at the Fed, although it also could cause technical problems in the functioning of certain credit markets. A third modest possibility would be to buy enough new mortgage securities to replace those on the Fed balance sheet that are paid off as people take advantage of low interest rates to refinance.

Role of mortgage rates

None of those steps amounts to the kind of massive unconventional effort to drive down mortgage rates and prop up growth that the Fed took in late 2008 and early 2009, when the economy was in a deep dive. Then, the Fed began buying Treasury bonds, mortgage securities and other long-term assets -- more than $1.7 trillion worth by the time the purchases concluded in March. Some economists have encouraged the Fed to launch a new asset-purchase program, saying that with the unemployment rate at 9.5 percent and little apparent risk of inflation, the Fed should use every tool at its disposal to get the economy back on track.

Fed leaders view such a strategy as likely to have only a small impact on the economy and as carrying a risk of slowing growth. One of the key ways the earlier securities purchases stimulated the economy was by driving down mortgage rates, which in turn propped up the housing market. But with mortgage rates near all-time lows, it is not clear that actions to lower rates another, say, quarter percentage point would result in much additional home sales or refinancing activity.

Moreover, the Fed's purchases of mortgage securities have reduced the role of private buyers in that market, and some leaders at the central bank fear that further intervention could delay the resumption of normal market functioning. "The Fed probably believes that unconventional policy does not have much traction as market functioning gets better," said Vincent Reinhart, a resident fellow at the American Enterprise Institute and a former Fed official.

Asset-purchase plan

Another risk is that global investors could lose faith that the Fed will be able or willing to pull money out of the economy in time to prevent inflation. That would lead the investors to demand higher interest rates on long-term loans, which could reverse the rate-lowering effects of the Fed's asset purchases. When the Fed was buying $300 billion in Treasurys in mid-2009, part of its try-everything approach to dealing with the crisis, rates on 10-year bonds temporarily spiked amid concerns that the Fed was "monetizing the debt," or printing money to fund budget deficits. With deficit concerns having deepened in the past year, such fears could be even more pronounced now.

All that said, Fed officials do not rule out launching a major new asset-purchase program. Rather, they say they would consider one only if their basic forecast -- of continued steady expansion in the economy -- proves to be wrong. A key factor that would build support for new asset purchases would be a rise in the risk of deflation, or a dangerous cycle of falling prices -- which has become more of a concern as the world economy slows.

Fed officials express confidence that they have tools to address the economy further if conditions worsen. "I think we do have a variety of tools available, and we shouldn't rule any tool out," Eric Rosengren, president of the Federal Reserve Bank of Boston, said in an interview. "If we're uncomfortable with how long it's going to take us to reach either element of our dual mandate [of maximum employment and stable prices], we'll have to make some adjustments to policy."

Hedge Funds 'Frozen in Headlights' Cut Trading

by Saijel Kishan and Katherine Burton - Bloomberg

Hedge-fund managers, Wall Street’s best compensated and supposedly smartest investors, are dazed and confused. Reeling from the worst second-quarter performance in a decade, hedge funds have scaled back trading as they struggle to figure out where markets are headed amid sometimes vicious crosscurrents in stock, commodities and other markets, according to brokers and managers. "There’s a degree of being frozen in the headlights, of not knowing what sectors to emphasize, of what securities to emphasize," said Tim Ghriskey, chief investment officer of Solaris Asset Management LLC, a firm in Bedford Hills, New York, with $2 billion in hedge funds and conventional stock funds.

Hedge-fund managers, who oversee $1.67 trillion in assets, are reluctant to put money to work as they are buffeted by a wide range of often conflicting political and economic forces, from fiscal policy in Europe and the U.S., to what regulations will be imposed on the financial-services and energy industries, to the growth prospects in China. In turn, smaller and fewer trades may make it harder for funds to rebound from losses incurred since May, when the industry suffered its worst decline in 18 months. "For many people, it’s a frustrating market given the high volatility and low volumes," said Aaron Garvey, portfolio manager at MKP Capital Management LLC, a New York-based hedge fund overseeing $3.5 billion. "We are seeing strong opposing forces in the markets, which makes generating strong convictions difficult for the medium- and long-term."

Holding Cash

Prime brokers such as Credit Suisse Group AG and JPMorgan Chase & Co. that service hedge funds report that managers are borrowing less money and are sitting on more cash. Credit Suisse’s hedge-fund clients held 24 percent of their assets in cash in June, compared with 19 percent three months earlier, according to the Zurich-based bank’s prime brokerage unit. "People are in cash for the most part and nobody’s really taking out any big bets," said Blaze Tankersley, chief market strategist at Bay Crest Partners LLC, a brokerage firm in New York. "Nobody wants to take risk in either direction. It’s a weird time in the market."

U.S. stock market trading last month had its steepest June decline in at least 13 years. Daily trading volume for the Standard & Poor’s 500 Index of the largest U.S. companies averaged 1.09 billion shares in June, 20 percent less than in May. The 15 percent decrease last year was the second-biggest slump between May and June in Bloomberg data going back to 1997.

No ‘Summer Lull’

Hedge funds account for 20 percent of the equities volume in the U.S., according to Tabb Group LLC, a New York-based adviser to financial-service companies. Trading of options on stocks, indexes and exchange-traded funds on the eight U.S. exchanges also fell in June, declining 2 percent from last year to 309 million contracts for the month, according to the Chicago-based Options Clearing Corp. Options are contracts that give the right to buy or sell assets at a set price by a specific date.

"This is much more than a summer lull," said Sam Hocking, global head of prime brokerage sales at BNP Paribas SA. "Given the uncertainty out there, many hedge funds have felt it wise to pull back and take risk off the table." Credit Suisse says its hedge-fund clients have cut their borrowing, or gross leverage, to about 2.5 times assets in June compared with 2.8 times assets in March.

Stock Market Decline

"We’re trying to reduce risk by downsizing of our trades," said Max Trautman, a former Goldman Sachs Group Inc. proprietary trader and co-founder of Stoneworks Asset Management LLP, a $460 million macro hedge fund based in London. "It’s not that we have stopped taking views but we’re just putting less risk in them." Global stocks posted the biggest losses in the second quarter since the bull market began last year, as the sovereign- debt crisis in Greece threatened to spread to other European countries.

Chinese government restrictions on lending and real estate, intended to prevent the world’s third-largest economy from overheating, added to concerns global growth may slow. In the U.S., slowing growth in manufacturing, an unexpected jump in jobless claims and a slump in home sales have fueled concern the economic recovery is faltering.

Biggs Sells

Barton Biggs, whose purchase of stocks in March 2009 gave Traxis Partners LLC a 38 percent gain last year, said last week he sold about half his stock investments because of concern governments around the world are curtailing stimulus measures too soon. "I’m not wildly bearish, but I don’t want to have a lot of risk at this point," Biggs, who manages $1.4 billion, said in a telephone interview. "I’m not putting my money into anything. I’m raising cash."

Hedge-fund managers say they’re also worried about the impact of financial reform being introduced as a result of the Wall Street meltdown, and energy regulation following the BP Plc oil spill in the Gulf of Mexico, the largest in U.S. history. Among managers sticking to convictions is John Paulson, who is betting on a U.S. economic recovery after making $15 billion with a wager against home mortgages during the financial crisis. Paulson lost 6.9 percent in June in his Advantage Plus hedge fund and 4.4 percent in his Advantage fund, according to two investors briefed on the returns.

Paulson’s Convictions

The funds were positioned to profit from a jump in stocks including financial-services companies, said the clients, who asked not to be named because the fund is private. Paulson, who runs the $33 billion New York-based Paulson & Co., hasn’t changed his bullish views after the stock market’s decline and last week’s data showing weaker-than-expected private-sector employment in June, according to the investors. Almost two-thirds of the firm’s assets are in his Advantage funds, which invest in corporate events such as bankruptcies and mergers.

Paulson, 54, has told clients he expects inflation to increase over the next three to five years, which is why he has also been buying gold and mining shares, including AngloGold Ashanti Ltd. and Kinross Gold Corp. Gold has risen about 10 percent this year. Paulson’s Gold Fund climbed 7.3 percent in June and 13 percent for the year, the investors said. Armel Leslie, a spokesman for the fund firm, declined to comment.

‘High Correlation’

Hedge funds declined 0.94 percent in June and 2.79 percent in the three months ended June, the worst second-quarter performance since 2000 when the industry lost 3.42 percent, according to Hedge Fund Research’s HFRX Global Hedge Fund Index. The index dropped 1.2 percent in the first half of this year. There’s "a high degree of correlation among stocks, so it’s not the best environment for stock picking, or sector allocation," said Solaris’s Ghriskey. "Investors are not moving money around between sectors, nor are they aggressively moving between fixed income and equities."

Trading of U.S. corporate bonds fell 4 percent in June from the previous month, the first decline between May and June since 2006, according to data compiled by the Financial Industry Regulatory Authority. Some hedge-fund investors prefer that managers don’t place large bets to offset losses this year.

‘Capital Preservation’

"It’s all about capital preservation at the moment," said Amit Shabi, a Paris-based partner at Bernheim Dreyfus & Co., which farms out client money to hedge funds. "The losses of 2008 are still fresh in investor’s memories and so managers should be cautious." Hedge funds lost an average 19 percent in 2008, the worst returns since Chicago-based Hedge Fund Research started tracking data in 1990. While the industry rebounded 20 percent last year, almost half of the 2,000 funds that make up the HFRI Fund Weighted Composite Index ended the first quarter of 2010 below their high-water mark, or peak net asset value, meaning they can’t charge investors performance fees.

Some hedge-fund managers say the outlook for the U.S. economy will become clearer after companies report second- quarter earnings in the latter half of July, and executives talk about their outlook for the rest of the year. Investors are also looking to results from European banks’ stress tests, due out later this month, and data on U.S. economic growth scheduled to come out on July 30.

‘Cogs in the Wheel’

Companies in the S&P 500 Index increased profit by 34 percent during the second quarter, according to the average analyst estimates collected by Bloomberg. The U.S. economy will grow at a 3.2 percent annual rate this quarter, down from a prior estimate of 4 percent, JPMorgan said in a July 1 note to clients. Sylvan Chackman, global co-head of prime brokerage at Bank of America Corp. in New York, said he expects hedge funds to increase trading this quarter. "They need to put their capital to work to generate returns," he said.

John Trammell, chief executive officer of New York-based Cadogan Management LLC, said it might take until the end of the year or the start of 2011 for managers to get clarity about the direction of markets. "There are so many cogs in the wheel," said Trammel, whose firm invests about $2.7 billion of client money in hedge funds. "We need more details on the fiscal positions in Europe and then have to wait to see whether the policies will work or not."

EMU break-up risks global deflation shock that would dwarf Lehman collapse, warns ING

by Ambrose Evans-Pritchard - Telegraph

A full-fledged disintegration of the eurozone would trigger the worst economic crisis in modern history, devastate every country in Europe including Germany, and inflict a deflationary shock on the US. There would be no winners, warns the Dutch bank ING in a new report "Quantifying the Unthinkable".

"Complete break-up would have effects that dwarf the post Lehman Brothers collapse. Governments would find themselves having to bail out banks again, worsening already fragile government finances. The risk of at least a temporary break-down in payments systems would be enormous, " said the report by Mark Cliffe, Maarten Leen, and Peter Vanden Houte. "Initial trauma is sufficiently grave to give pause for thought to those who blithely propose EMU exit as a policy option," it said, a rebuke to those German politicians and economists who have talked openly of shaking out weaker members.

The new Greek drachma would crash by 80pc against the new Deutschemark. The currencies of Spain, Portugal, and Ireland would fall by 50pc or more, causing inflation to soar into double-digits. "The impact is dramatic and traumatic," it said. ING has attempted to unpick the complex consequences of break-up scenarios, concluding that even a surgical exit by Greece alone would hurt everybody, and be suicidal for Greece. Both weak and strong states would suffer violent downturns if EMU unravelled altogether, though each in very different ways. "In the first year, output falls by between 5pc and 9pc across the various former member states," it said.

The German sphere would face a "deflationary shock". The US dollar would rocket to 85 cents against the euro equivalent, with a "temporary overshoot" to near 75 cents. This would tip the US into acute deflation, threatening North America with a double-dip recession. East Europe would contract 5pc in 2011 alone. Safe-haven flows to core debt markets would drive down yields on 10-year US, German, and Dutch bonds to near 0.5pc, by far the lowest ever. Club Med yields would decouple brutally, rising to between 7pc and 12pc, "capital controls, notwithstanding."

This is the picture of a world falling apart. It is an outcome that Angela Merkel, the German Chancellor, now seems determined to avoid, after dragging her feet over the Spring. The Bundestag has backed Germany's share of the €110bn rescue for Greece, and the €750bn EU-IMF bail-out for future casualties should they need it. The Bundesbank has lifted its de facto veto on purchases of Club Med bonds by the European Central Bank. Yet markets have failed to stabilise. Spreads on 10-year Greek bonds are still 750 basis points over Bunds. Investors clearly doubt whether the Greek austerity policy of wage deflation can ever work, or whether EU states will back their words with money, or both. The spreads are 285 for Portgual, 272 for Ireland, and 213 for Spain.

The markets perhaps sense that the bail-out battles in Germany are not yet over. There are four complaints lodged at the German constitutional court arguing that the rescues breach EU treaty law and therefore German basic law. While the court has refused an immediate injunction to block aid, it has not yet ruled on the cases. A group of five professors has just expanded its original complaint against the Greek rescue to cover the EU's €440bn Stability Facility, describing the methods used to ram through the measures as "putschist" and anti-democratic. "This course is leading Germany to ruin," they said.

Germany's Centre for European Politics in Freiburg has joined the fray with a report arguing that the use of €60bn of EU money under Article 122 of the Lisbon Treaty to support the rescue package is illegal. "It is a complete violation of our constitutional law and the judges at the court will have to say so if a case reaches them, even though they are afraid of the economic consequences," said the author, Dr Thiemo Jeck. Bavarian politician Peter Gauweiler aims to file a fresh case along these lines.

ING's global strategist Mark Cliffe said any Anglo-Saxon Schadenfreude at a euro break-up would be short-lived. The UK economy would shrink by 4.5pc from 2011-2012. "It would be a very unpleasant experience," he said. Safe-haven flows pouring into Britain would drive sterling through the roof. Eurozone demand for UK exports would contract viciously. Pension funds would suffer fat losses on eurozone assets. UK lenders would face havoc again though a web of cross-border linkages.

The Dutch bank does not make any judgement on the merits of EMU, or on whether it is an 'optimal currency area', nor does it explore half-way options such as a split into a hard Teutonic euro and a weak Latin euro. The report said break-up talk is "no longer just a figment of fevered Anglo-Saxon imaginations". It has spread into top policy-making circles in the eurozone and must now be analysed as a serious tail-risk. A survey of 440 heads of global banks and companies by RBC Capital Markets found that 50pc expect at least one country to leave EMU by 2013, and a quarter expect a complete collapse.

ING said heavily indebted states such as Greece would not gain relief by escaping EMU and devaluing since their debt burden would remain, even if government bonds are switched into the new currency. This is a controversial point. If Greece devalues and defaults as well, the calculus is different. Many big bust-ups entail both, such as the Argentine crisis in 2001. Some Argentines argue that their trauma proved cathartic, pulling the country out of a destructive downward spiral. If Greek, Portuguese or Spanish leaders ever start to ask their own Argentine questions as austerity grinds on, and unemployment grinds higher, events will run their ineluctable political course regardless of the greater risks.

As World Cup ends, Europe's stress tests loom

by David Callaway, MarketWatch

The unique ability of sports to bring people together and make them forget -- at least for a spell -- their troubles with each other is never more on display than during the World Cup soccer tournament every four years -- even more so than the Olympics. And this summer has been no exception. The last four weeks marked a welcome relief from the climate of fear that gripped world markets in April and May, as names like Villa, Sneijder, Kaka, and Muller rose to prominence in the headlines and action photos, replacing the tired old shots of names like Trichet, Blankfein, Geithner, or Hayward, entering hearing rooms or press conferences.

People gathered throughout Europe -- from the Villa Borghese Park in Rome to the Santiago Bernabeu stadium in Madrid -- not to light fires and protest the dreaded "austerity" measures from their governments, but to watch "the football" on big screen televisions together. Predictably, the games caused more heartbreak and controversy than joy. After all, 31 countries have to lose before one can win it all.

But the excitement everywhere on game days was palpable, one of the reasons I've been here the last few weeks, conducting my own special series of "stress tests" on the great bars of Europe. Markets reflect public perception and were quick to fall in step with the sports-induced lull. The plunging euro recovered a bit against the dollar during the tournament. So did the British pound. Credit markets were calm while stocks in Europe -- and indeed globally -- were flat, rising earlier in the tournament then falling back to end a terrible quarter weaker. But lack of fear and nervousness about China's economy or the future of the euro helped pave the way for some feel good stories that have the bulls rearing their bruised heads again.

Europe's banks survived a deadline for repaying short-term loans to the European Central Bank last week, and borrowed far less than expected going forward. Agricultural Bank of China got its massive initial public offering launched this week amid high hopes from investors tied to the China growth story. And bankers from London to New York took advantage of the break in hostilities toward their industries to make a series of bold, new money grabs. Three ex-Goldman Sachs bankers in London priced a money-losing online grocery service called Ocado Ltd. this week, and hope to make away with some 90 million pounds ($136 million) in an initial public offering before investors realize the company is simply Webvan with a British accent.

And two of the co-founders of Kohlberg Kravis Roberts -- the original barbarians at the gates -- hope to throw open the doors and make a dash for it in a public stock offering to investors next week, a la Blackstone Group's success.

But the stress of the last six months in global markets, particularly in Europe, is set to resume almost immediately after the final whistle at Sunday's World Cup final in South Africa. Earnings season in the U.S and in Europe begins on Monday, and with it expectations for some dire forecasts on business conditions for the rest of the year. Oil giant BP remains in critical condition as investors bet heavily on its future ahead of its earnings at the end of the month. But the most important event for the market right now at least is the coming stress tests for banks in Europe, results of which are set to be announced in about two weeks.

There is great concern that some of the 100 or so banks tested -- particularly the regional German landesbanks or the Spanish cajas -- will reveal enough weakness to trigger more concerns about larger bailouts and sovereign debt defaults in places like Greece, Portugal, and Spain. These concerns are likely unfounded. Anybody that remembers the U.S. stress tests on banks last year will recall that they were designed by the Treasury specifically not to add to the stress levels of investors. Indeed, weeks of concern about the U.S. stress tests ended with a rally in the market after Wall Street realized the last thing the Treasury was going to do was announce a major fault line in the banking system. Expect the ECB to finesse the European stress tests in the same way, causing a rally in stocks and bonds in Europe later this month.

But after that artificial event, there is indeed real reason for concern in Europe. Indeed, my personal stress tests revealed beneath the veneer of World Cup fever a deep fear about the economic future in specific countries. In Spain, a series of transportation strikes in Madrid layered on pain to a population suffering 20% unemployment, and facing a restructuring of its financial services system, with thousands of more job losses. In Italy, residents spoke of tourism being down noticeably and of concern that the contagion in other parts of Southern Europe could spread there. In the U.K., financial engine to Europe if not the world, the new government's emergency budget has staved off debt concerns for now.

But nobody is under the illusion about the challenges that Prime Minister David Cameron's new coalition government faces in turning the economy around while also cutting billions of pounds in costs. So while the true European holiday season begins this month, it's unlikely the lull in the markets will make it until September. Market historians note that August is one of the worst months on record for stocks, something to remember before heading to the beach.

Still, any trip around Europe, its museums and its landmarks, reminds the observer that it's an ancient place, which has survived countless wars, crisis and lately, terrorist attacks, specifically in Madrid and London. This morning in London, commuters were quietly reminded of the fifth anniversary of the July 7 tube and bus bombings that killed 52 innocent people and injured more than 700. A heightened police presence around Trafalgar Square and the Houses of Parliament, combined with a surge in auto traffic in the city's already jammed streets to reflect a society that remains cautious, but steadfast in its desire to move ahead.

That's a pretty good way for investors to look at opportunities in Europe and globally in the markets in the coming months. There are many reasons to be cautious, but keep looking ahead. The economic recovery is still coming; it just might take a while longer. Alas, after Sunday we can no longer count on the World Cup for help. The next one isn't for four years, in Brazil.

'Soft as butter' European stress tests draw lukewarm response

by Simon Kennedy - MarketWatch

European plans to test the financial strength of the region's 91 biggest banks got a lukewarm reception Thursday amid worries they aren't tough enough, with one analyst calling the tests "soft as butter." The stress tests are intended to check whether banks would be able to withstand another sharp economic downturn and European regulators have promised to publish the results of the tests later this month.

However, regulators reportedly spent much of their time arguing over what level of decline should be factored into the tests and whether they should publish full details of the assumptions, amid worries that they might be seen as an economic prediction and further undermine confidence in the markets. In the end the Committee of European Banking Supervisors, which is overseeing the tests, listed the 91 banks that will be tested and said the assumptions include that economic output will be three percentage points below current European Union estimates.

In May, the European Commission forecast 1% GDP growth in 2010 and 1.5% in 2011 in European Union countries. CEBS didn't give any details on the losses banks would have to be able to withstand on their sovereign debt holdings, but the tests are widely reported to assume a 17% loss on Greek sovereign debt, 3% on Spanish government bonds and no losses on German debt.

"If the delay of the announcement suggests any tensions among individual regulators in the euro zone on the test then this is even more the case with the content released. What we got is only fragmental information, hardly suitable to spark confidence," said UniCredit analyst Stefan Kolek. "The assumptions look soft as butter," said Kolek, who added that the tests aren't even looking at an extreme scenario such as the break-up of the euro zone, which would result in both much greater losses on periphery government bonds as well as a bigger drop in GDP.

Haircuts

Seymour Pierce analyst Bruce Packard said that, in comparison the loss -- or haircut -- on Argentina's bonds earlier this year was 66%. In other recent crises, haircuts ranged between 44% for Russia and less than 15% in Ukraine and Pakistan, he added. "Credible stress tests in the U.K. and U.S. generated confidence in the banking system last year. However, there is a fine line between tests that are suitable demanding, and reverse engineering a testing process so that everyone passes the test," Packard said in a note to clients.

Still, bank stocks got a lift from the CEBS announcement, with the sector rallying late Wednesday and continuing to gain Thursday. Shares in BNP Paribas rose 2.9%, Societe Generale rose 2.2% and Barclays added 2.7%. While some analysts argued the tests won't be tough enough, others said the assumptions could easily have been even less strict. "Overall we regard the release as a mild disappointment, if not quite as bad as we feared," said Matt Spick, an analyst at Deutsche Bank.

Spick said he believes that most European banks will pass the tests, with National Bank of Greece and Allied Irish Banks the most likely to fail among the banks he covers. Shares in National Bank of Greece and AIB rose along with the rest of the banking sector Thursday, with both stocks adding around 3% in early trading.

Spick said there remains a risk there could be a capital shortfall in selected German banks or Spain's unlisted savings banks, known as cajas. This could be due to either low capital levels or greater-than-expected losses on sovereign bonds. He added that in total that would likely require less than 100 billion euros of new capital and that it would largely be in the unlisted sector. See earlier story on unlisted banks.

European banks use gold reserves to raise cash in swaps

by Jack Farchy - Financial Times

European commercial banks have begun using their holdings of gold to raise cash with the Bank for International Settlements, in a further sign of strains in the money markets on which many rely for funding. The BIS, the so-called "central banks’ central bank", took 346 tonnes of gold in exchange for foreign currency in "swap operations" in the financial year to March 31, according to a note in its latest annual report.

In a gold swap, one counterparty, in this case a bank, sells its gold to the other, in this case the BIS, with an agreement to buy it back at a later date. In the past the BIS has occasionally engaged in gold swaps. There has been no mention, though, of any such operation in recent years. The gold swaps detailed in the annual report began in December last year, according to monthly data from the International Monetary Fund, and have surged since January, when the Greek debt crisis erupted.

The amount raised in the operations, just over $13bn at current prices, is small compared with the wholesale money markets. But the fact that banks are using their gold holdings to raise capital is a further indication of the stress in the sector. Euribor, the rate at which eurozone banks lend to each other, has risen for 27 successive days, while markets are nervous about the impending release of bank stress tests in Europe, scheduled to be published at the end of the month.

The BIS annual report says the gold received in the swaps was held "at central banks". Talk of the swaps caused a stir in the gold market, with some traders citing it as a reason for gold’s fall to a five-week low below $1,200 a troy ounce.

Greece Pushes Through Pension Overhaul Despite Protests

by Niki Katsantonis - New York Times

The Greek government took a major step forward in overhauling its debt-plagued economy by forcing through, in principle, a pension bill that would dramatically cut the cost of Greece’s welfare state by increasing the retirement age and slashing benefits. For Prime Minister George Papandreou, who commands a seven member majority in his country’s fractious parliament, the bill’s many provisions represent the beginning of end of the cradle-to-grave state compact that his father put in place in the early 1980s.

The plan was approved in principle by a vote of 159-137 late Wednesday. Individual provisions were to be voted on Thursday before a final vote on the whole package. Three months into an historic bail program worth 110 billion euros — about $140 billion or half of Greece’s annual gross domestic product — the government has so far exceeded the deficit cutting benchmarks set by the International Monetary Fund. Government officials here see the bill’s passage as further evidence for still-skeptical international investors that Greece is committed to pushing through painful reform measures.

"This is our passport out of hell," said Yannis Stournaras an Athens-based economist who has advised past Socialist governments. "It represents the toughest challenge for Papandreou and goes to the very heart of his party. No politician has ever been able to do this." Greece’s generous pension system has allowed many employees to retire before they turn 50 and earn the right to rich payouts calculated on the basis of bonus-laden salaries. The bill would unify the retirement age at 65 years of age for both men and women and would reduce payouts by calculating salaries on lifetime income as opposed to a worker’s highest, most recent pay.

It would also make it easier for Greek companies to fire workers. Athens was to a large extent shut down Thursday as public sector workers gathered in protest before the parliament building in Syntagma square. According to police estimates, the numbers were between 5,000 and 10,000 and despite a few challenges by hooded youths carrying sticks and axes, riot police with gas masks and shields seemed to be in control of the situation.

"Nobody expected this — this is worse than the occupation under the Germans," said Nikos Stathas, 60, a plumber who is just retiring now. He says he has just got his pension, but he is worried about his children and grandchildren. "This will demolish their retirement," he added. Such strong sentiments aside, by most accounts protests have been relatively restrained since three people was killed in an attack on a bank in May — a sign perhaps that Greeks, while angry and unhappy at the sacrifices forced upon them, understand that they face little other choice than to tighten their belt.

Mr. Papandreou, a life-long Socialist, has managed to keep control of his party despite protests among influential advisers like his economy minister, Louka Katseli. A team from the I.M.F. and the European Union is due in Athens next month to examine the government’s progress, before the next 9 billion euro tranche is to be released. Mr. Stournaras pointed out that the Greek economy performed better than expected in the first quarter, sustained by a surprisingly robust showing for private consumption, which was up by 1.5 percent.

A sharp cutback in public investment caused growth to decline by 2.5 percent for the quarter, but Mr. Stournaras expects the economy to shrink by less than the I.M.F. estimate of 4 percent and he forecasts a budget deficit this year of about 7 percent. According to a presentation by the government’s debt management agency, sharp decreases in public sector wages and investment, plus an increase in taxes have driven the improved deficit picture.

"The government's popularity is holding up very well," said Paul Mylonas, chief economist at the National Bank of Greece. "But after several years of reform, adjustment fatigue may set in if light does not appear at the end of the tunnel." Indeed, senior government officials concede that they have yet to win back the confidence of foreign bond investors, many of whom believe that some form of a debt restructuring is inevitable, as the 10 percent-plus yields on the government’s long term debt show.

"No one in Greece is looking at a debt restructuring. It’s just not going to happen," said Petros Christodoulou, the head of the debt management agency insisted last month at an investor conference in London. Still, doubts abound that the economy can survive the dramatic public sector retrenchment and continue to generate needed tax revenues to make a dent in a debt that even within three years will still be at around 120 percent of G.D.P.

Europe's Got Balls

by Randall Lane - Daily Beast

It’s Management 101: Employees act in accordance with how you pay them. Managers with long-term contracts stick around. Executives compensated in stock act like owners. Salespeople paid commission-only hock their first-born. Wall Street reacts that way, too. If you want to trace virtually every stupid risk, every trend that’s turned the markets into a casino, every root cause for the meltdown that nearly imploded the global economy, just follow the tyrannical path of the five sweetest letters on Wall Street: the almighty bonus.

Europe, collectively, seems to understand this. On Wednesday, the European Parliament voted overwhelmingly, 625-28, to limit to 30 percent the amount of a bonus that can be paid in cash. The rest of the loot, pending a rubber stamp from the continent’s finance ministers next week, will essentially be deferred over three years, to ensure that the risks taken to get the bonus don’t subsequently blow up the bank or the economy.

Yet on this side of the pond, we seem to be entirely unwilling to address the destructive nature of the bonus system head-on. The tepid financial-reform package that continues to weakly stumble through Congress doesn’t tackle the topic directly. And while the Federal Reserve issued guidelines last month that make it clear it agrees with the actions in Europe, its enforcement boils down to vague threats about vetoing compensation plans that don’t meet "standards." The obscene numbers don’t make the Wall Street bonus system destructive. Paying a 25-year-old commodities trader $20 million a year is no more inherently stupid or illogical than paying 25-year-old LeBron James $20 million. It’s how bonuses get paid.

At a typical Wall Street bank, 80 or 90 percent of annual compensation arrives in one giant check, generally determined before Christmas and then paid in February. All that pent-up uncertainty—a "bonus," by definition, is discretionary—creates paranoia pretty much all year. For those on the lower rungs, each bank and fund has compensation committees that divide the loot by group based on how the firm did overall, and how much each unit contributed to it, and then the head of each desk, like a Mafia boss, divides the spoils among his crew, based on individual performance and other intangibles. While I was making calls for my book, The Zeroes, one manager, who determines the bonuses of a few dozen traders, put it to me this way: "I have some guys who work for me, who I take $50,000 from just because I think they’re a dick."

So much money. All in one check. All dependent on how much you make managing other people’s money. This warped system corrupts even good people. "If I’m going to get paid zero," another money manager told me about his autumn mindset during down years, "I might as well take some risk and try to make some money." The only risk to his bonus, in other words, is not taking risks. A dangerous way to think when you can borrow roughly 20 times the amount of your initial bet to really raise the stakes.

In this system, long-term performance is irrelevant. Bonuses deal with the year at hand, and if that means buying or selling junk that explodes later, that hasn’t been an issue. "All you worried about was whether you could sell it," says one Wall Street sales executive, describing the attitude pre-meltdown. Wall Street’s musical chairs meant you’d be at another firm, or somewhere else in your current firm, when the song stopped. And stop it did.

Why does our country tip-toe around this problem, while Europe hits it over the head with a hammer? A lot of it has to do with entitlement. Try to muck with a Wall Streeter’s bonus, and you’ll get a reaction similar to what you’d hear after telling a 70-year-old you’d like to reform Social Security. No matter that bonuses are a recent phenomenon. Until 1971, almost every single major bank was a private partnership. At the end of the year, the partners simply divided the profits among themselves; the vast majority of employees got regular paychecks like schoolteachers and firemen and other normal working people. Only once the big banks went public—and faced shareholder pressure for consistent bottom-line performance—did the talent demand fat checks at year-end.

There’s also something slightly un-American about the idea of capping salaries. And rightly so. But what Europe is launching isn’t a cap; it’s just a glorified escrow account. And banks are different. When a hedge fund blows up, whether Amaranth or Madoff, it makes headlines, but really only affects the rich people or institutions that willingly chose to invest or deal with them. Ever since the bone-headed repeal of Glass-Steagall, and the ensuing co-mingling of the Jimmy Stewart/It’s a Wonderful Life bank ideal with the Al Pacino/Dog Day Afternoon version, the risky casino half of the bank can take out the essential deposits-and-loans side. (See Lehman Brothers, Bear Stearns, and Merrill Lynch.) That’s why the way bankers get paid affects all of us. America generally leads on this kind of stuff—for once, it’s time to follow.

Cap on Bank Bonuses Clears Hurdle in Europe

by Liz Alderman - New Yoek Times

As Wall Street drags its feet on reining in bonuses, the European Union is forcing its banks — by law — to show some self-restraint. The European Parliament on Wednesday approved one of the world’s strictest crackdowns on exorbitant bank pay, going beyond some of the limits that many banks were pressed to adopt in the wake of the financial crisis.

The action comes as the Federal Reserve accuses U.S. banks of not moving fast enough to change compensation practices that stoke excessive risk-taking. While American and British regulators have adopted the principles of Europe’s new measure, officials here are going a step further by legislating minimum caps for cash bonuses and other changes to compensation.

Bankers in the 27-nation bloc will be barred from taking home more than 30 percent of their bonus in cash starting next year, and risk losing some of the remainder if the bank’s performance erodes over the next three years. Banks that don’t curb the salaries of their biggest earners will have to set aside more capital to make up for the risk. "The exercise here is to make sure that bonuses are not a one way bet, so that if you take risks and lose in a big way that will affect what you get," said Nick Dent, an employment law partner at Barlow Lyde & Gilbert LLP who monitors financial compensation.

Large cash bonuses have been blamed for encouraging the type of excessive risk taking that stoked the global financial crisis. Under political pressure, banks in Britain, Germany and France had already moved to limit bonuses last year. The legislation, passed by a vote of 625-28, codifies a compromise clinched last week between European governments and lawmakers. National finance ministers are expected to endorse it on Tuesday, and it then will take effect Jan. 1.

The measure reflects agreements among Group of 20 leaders about how to limit bank pay, and is intended to affect high-bonus cultures at banks with operations in Europe like Deutsche Bank, Barclays and Goldman Sachs, and at some hedge funds. About 70 percent of a bonus would have to be deferred for up to three years and paid in a new class of security, called contingent capital, that would decline in value if the bank’s financial performance deteriorates -- and potentially even be forfeited.

For particularly large bonuses, cash could constitute only 20 percent of the payout. "If within that three years something happens with the performance of the bank or a staff member, he won’t get the payments that were deferred," said Guido Ravoet, secretary-general of the European Banking Federation. "And the clawback means that even if he had been paid the full bonus, he must reimburse the bonus."