"Police raid on gamblers' den, E Street between 12 and 13th, Washington, D.C."

Ilargi: To order Stoneleigh's video presentation of "A Century of Challenges", the lecture that's receiving rave reviews across Europe and North America, CLICK HERE or click the button on the right hand side just below the banner.

For Jim Puplava's interview with Stoneleigh, choose your audio format:

RealPlayer WinAmp Windows Media MP3

For the transcript of the interview, see: Jim Puplava interviews Stoneleigh, Part 2

Ilargi: The answer to the question in the title is, as you may have guessed, a resounding NO.

Not that it won't be attempted, and not that too many people have understood that thus far, mind you. As the Financial Times notes:

Debt sales highlight abnormal conditionsThe abnormal state of the credit markets came into focus as the US Treasury sold bonds with negative interest rates for the first time and Goldman Sachs prepared to issue its first 50-year debt deal. Both developments on Monday highlighted the difficult choices facing investors at a time when interest rates are at historical lows and the Federal Reserve is moving towards more asset purchases aimed at boosting the economy and staving off deflation. Investors who believe the Fed will succeed in its efforts – which would lead to higher inflation – accepted a yield of minus 0.55 per cent on $10bn of Treasury Inflation Protected Securities – or Tips – which compensate holders if the consumer price index rises.

Ilargi: Now of course we must realize that in a market place where 70% of stocks are held for all of 11 seconds before being sold off again, things can happen that appear irrational, and we should ponder who purchases negative interest rate bonds and why. Still, there are those who feel that Bernanke's FOMC QE2 announcement next Wednesday will push up the consumer price index to levels which make these TIPS a profitable investment.

If they'd read through John Hussman's "Bernanke Leaps into a Liquidity Trap", they might come away with a whole lot of questions about that potential profit, though. Provided they intend to hold on to them for more than 11 seconds.

Ironically, Hussman explains why inflation does not mean rising prices, even as he uses it in exactly that meaning. He states that the monetary base can be enlarged without rising prices as a result, because the velocity of money will of necessity sink in the process, provided interest rates are low enough.

Just as ironic is it that it's Keynes himself who wrote about this fact, which should be a reminder for all Keynesian economists to go back and read his work once more. They might have missed a line or two. Sure, there may be a link to the realization that QE is but a swap of short-term for long-term debt, but the ground principle remains the same.

In her famous lecture A Century Of Challenges, The Automatic Earth's Stoneleigh uses the following image to explain what the liquidity trap is. The Fed can keep on pumping money, but it can't make it move. If you're fearful or uncertain, you will hold on to what you got, not spend it.

Stoneleigh compares it to "running your car with the oil light on". That is to say, the liquidity trap results in an economy without sufficient lubricant (credit, money) to run in a healthy fashion.

According to John Hussman, and we fully agree, this is an inevitable consequence of attempts, like QE2, to grow the money and credit supply in the face of -ultra- low interest rates. For which the Fed, -wait, more irony?!- is up to now single-handedly responsible. Obviously, this is not new: QE1 had the same effect, nothing reached the real economy it was ostensibly intended for, even though no such thing was ever admitted by either Bernanke, Geithner or Obama. QE1, like QE2, will only help, and both were indeed designed with this sole purpose in mind, to keep the broke broker broken banks standing for a while longer, at the cost of the taxpayer.

Here's a generous amount of quotes from Hussman on the topic, in order to get the idea through:

Bernanke Leaps into a Liquidity Trap"There is the possibility... that after the rate of interest has fallen to a certain level, liquidity preference is virtually absolute in the sense that almost everyone prefers cash to holding a debt at so low a rate of interest. In this event, the monetary authority would have lost effective control.”

John Maynard Keynes, The General Theory

Keynes himself did not focus much of his analysis on the idea, so much of what passes for debate is based on the ideas of economists other than Keynes, particularly Keynes' contemporary John Hicks.

In the Hicksian interpretation of the liquidity trap, monetary policy transmits its effect on the real economy by way of interest rates. In that view, the loss of monetary control occurs because at some point, a further reduction of interest rates fails to stimulate additional demand for capital investment.

Alternatively, monetary policy might transmit its effect on the real economy by directly altering the quantity of funds available to lend. In that view, a liquidity trap would be characterized by the failure of real investment and output to expand in response to increases in the monetary base (currency and reserves).

In either case, the hallmark of a liquidity trap is that holdings of money become "infinitely elastic." As the monetary base is increased, banks, corporations and individuals simply choose to hold onto those additional money balances, with no effect on the real economy.[..]

A related way to think about a liquidity trap is in terms of monetary velocity: nominal GDP divided by the monetary base. Velocity is just the dollar value of GDP that the economy produces per dollar of monetary base. You can also think of velocity as the number of times that one dollar "turns over" each year to purchase goods and services in the economy. [..]

Falling velocity implies that a given stock of money is being hoarded, so that nominal GDP is growing slower than the stock of money. If velocity falls, holding the quantity of money constant, you'll observe either a decline in real GDP or deflation.

The belief that an increase in the money supply will result in an increase in GDP relies on the assumption that velocity will not decline in proportion to the increase in money. Unfortunately for the proponents of "quantitative easing," this assumption fails spectacularly in the data - both in the U.S. and internationally - particularly at zero interest rates.[..]

... a Keynesian liquidity trap occurs at the point when interest rates become so low that cash balances are passively held regardless of their size. The relationship between interest rates and velocity therefore goes flat at low interest rates, since increases in the money stock simply produce a proportional decline in velocity,

One might argue that while short-term interest rates are essentially zero, long-term interest rates are not, which might leave some room for a "Hicksian" effect from QE - that is, a boost to investment and economic activity in response to a further decline in long-term interest rates. The problem here is that longer-term interest rates, in an expectations sense, are already essentially at zero. [..]

So QE at this point represents little but an effort to drive risk premiums to levels that are inadequate to compensate investors for risk. This is unlikely to go well. Moreover, as noted below, the precise level of long-term interest rates is not the main constraint on borrowing here. The key issues are the rational desire to reduce debt loads, and the inadequacy of profitable investment opportunities in an economy flooded with excess capacity.

One of the most fascinating aspects of the current debate about monetary policy is the belief that changes in the money stock are tightly related either to GDP growth or inflation at all. Look at the historical data, and you will find no evidence of it. [..]

You can see why monetary base manipulations have so little effect on GDP by examining U.S. data since 1947. Expand the quantity of base money, and it turns out that velocity falls in nearly direct proportion.[..]

Simply put, monetary policy is far less effective in affecting real (or even nominal) economic activity than investors seem to believe. The main effect of a change in the monetary base is to change monetary velocity and short term interest rates. Once short term interest rates drop to zero, further expansions in base money simply induce a proportional collapse in velocity.[..]

... if one examines economic history, one quickly discovers that just as lower nominal interest rates are associated with lower monetary velocity, negative real interest rates are associated with lower velocity of commodities (hoarding). [..] The tendency toward commodity hoarding is particularly strong when economic conditions are very weak and desirable options for real investment are not available.

Quantitative easing promises to have little effect except to provoke commodity hoarding, a decline in bond yields to levels that reflect nothing but risk premiums for maturity risk, and an expansion in stock valuations to levels that have rarely been sustained for long [..]

In 1978, MIT economist Nathaniel Mass developed a framework for the liquidity trap based on microeconomic theory[..]: The weak impact of monetary stimulus on real activity arises because additional money has little force in stimulating additional capital investment during a period of general overcapacity. Instead, money is withheld in idle balances when profitable investment opportunities are scarce."

"Even aggressive monetary intervention can do little to correct excess capital.. Once excess capacity develops, the forces that previously led to aggressive expansion are almost played out. Efforts to prolong high investment can produce even more excess capital and lead to a more pronounced readjustment later."

Ilargi: One issue I left unaddressed before, of course, is that of commodity hoarding and money hoarding. Money hoarding is easy to see: bank reserves at the Fed have shot up with a vengeance. This is not because they’re afraid to lend, as we're told, but because they are aware of the losses that they haven't fessed up to, and that are just around the corner. Commodity hoarding is what takes place with gold, oil, food staples, anything investors feel can shield them from uncertainty and losses.

This may indeed lead to temporary price rises. But that's not inflation. It’s just rising prices. Inflation is the sum of money and credit supply multiplied by the velocity of money. And as we've just seen, that can't rise in times such as these. It can very much go down though, and that's what deflation means.

What can happen, and does, is that people choose to hold on to what they have, which lowers the velocity of money and temporarily raises -some- prices. This will end when they have to pay up their own debts.

And make no mistake: All that’s left is zombie money. The only "money" left is available solely because previously incurred debts haven't been paid off. That goes for all market participants: governments, companies, individuals.

Pension funds and other large investors wouldn’t have any money left to buy anything with, whether commodities, stocks or bonds, if the real estate related losses, including those on derivatives, were taken out of their deep dark moist and smelly hiding places. The only things that stand between banks, governments, large investors and oblivion are accounting gimmicks and perversely cheap credit provided at the behest of the taxpayer. Who, him/herself, need we extrapolate, only has plastic zombie "money" left as well.

But for now, sure, gold, stocks, bonds, everything that's not bolted down and then some, has this zombie money thrown at it.

Still, since this cheap credit is only possible at ultra-low interest rates, and these same interest rates in turn forbid any money-pumping from reaching the real economy, the Fed, and the American economy with it, is stuck in a dead-end street, with a steam roller heading its way.

The key point, or at least one of them, in Hussman's reasoning, is this:

"The weak impact of monetary stimulus on real activity arises because additional money has little force in stimulating additional capital investment during a period of general overcapacity."

There is no other possible conclusion then that all QE can possibly achieve today, effectively, is the transfer of public funds into private hands. And that that is all it's meant to do.

QE2 will be pushed through, whether it's to the tune of $2 trillion or $5 trillion or more, it has even already been priced in to a large extent, and conditions are being created as we speak that will seem to justify it to the public.

It will be pushed through exclusively for the benefit of the housing finance system, which consists of the big private banks as well as Fannie and Freddie, the FHA etc, all of whom are looking gigantic losses right in the eye.

However, if you listen to Bill Black, the notion creeps up that perhaps this one won’t be so easy to paper over, no matter how large QE2 turns out to be. Black gave us a taste in the Dylan Ratigan show:

Bill Black Wants BofA Nationalization, Firing Of Bernanke, Geithner And HolderCredit Suisse says that by 2006 49% of all mortgage originations were liars loans. When independent folks study fraud, it is in the 80-90% fraud range. That means there were millions of acts of fraud. Those loan frauds occurred because the banks created incentive structure for the loan brokers to bring them the absolute worst of the worst loans, and to lie on the application forms... These frauds came from the banks, and they propagated through the system through a series of echo epidemics...This fraud spread through the system and that's why we have a crisis in foreclosures. This stems from the underlying fraud by the lenders in mortgage loans to the tune of well over a million cases a year by 2005."

Ilargi: Also, Black and L. Randall Wray posted a second installment of their views at Huffington Post, in which they make a claim that's not overly recognized so far: the mortgage industry meant for homeowners to default. Which, when it comes to deception, is right up there with the Fed meaning for the QE2 trillions to go to the banks instead of the real economy.

Foreclose on the Foreclosure Fraudsters, Part 2: Spurious Arguments Against Holding the Fraudsters AccountableThere was fraud at every step in the home finance food chain: the appraisers were paid to overvalue real estate; mortgage brokers were paid to induce borrowers to accept loan terms they could not possibly afford; loan applications overstated the borrowers' incomes; speculators lied when they claimed that six different homes were their principal dwelling; mortgage securitizers made false reps and warranties about the quality of the packaged loans; credit ratings agencies were overpaid to overrate the securities sold on to investors; and investment banks stuffed collateralized debt obligations with toxic securities that were handpicked by hedge fund managers to ensure they would self destruct.

That homeowners would default on the nonprime mortgages was a foregone conclusion throughout the industry -- indeed, it was the desired outcome. [..]

When the overburdened homeowner began missing payments, late fees and higher interest rates kicked-in, boosting the stated income of mortgage servicers and the value of the securities. Not coincidentally, the biggest banks own the servicers and could maximize claims against the mortgages by running up the late fees. It was quite convenient to "misplace" mortgage payments, so even homeowners who were never delinquent could get hit with fees and higher rates. And when payments were received, the servicers would (illegally) apply them first to the late fees, meaning the homeowners were unknowingly still missing mortgage payments. The foreclosure process itself generates big fees for the SDI banks.

And, miracle of miracles, the banks would end up with the homes and get to restart the whole process again -- from resale of the home through the financing, securitizing, and fee-for-servicing juggernaut.[..]

We suggest an immediate moratorium on foreclosures and a requirement that all notes be produced by purported holders of mortgages within a reasonable length of time. If they cannot be found, the mortgages -- as well as the securities that pool them -- are no longer valid. That means that the homeowners are not indebted, and that the homes are owned free and clear. And that, dear bankers, is a big, big problem. It is also the law -- without evidence of debt, there is no debtor and no creditor.

An honest mortgage lender would not make "liar's loans" because absence of proper underwriting inherently produces loans that are expected to default. Yet, in 2006 just about half of all mortgages originated were liar's loans. Banks happily advertised specialization in "no doc" and NINJA loans. There can be no question about intent -- the intent was fraud, plain and simple. Fraud on the part of credit raters is equally easy to infer -- we have the internal emails that document intent to defraud securities purchasers by "pay to play" schemes. And the fraud committed by the investment banks that pooled the mortgages is also well documented. These entities committed tens of thousands and even millions of frauds each.

The "collateral damage" inflicted by the SDIs is now endangering tens of millions of American families -- most of whom played no role in the speculative euphoria. Almost half of American homeowners are already underwater or on the verge of going under. In short, it was Wall Street that turned our homes over to a financial casino -- and so far virtually all the losses have been suffered on Main Street.[..]

Closing the control frauds would actually benefit honest bankers by eliminating the "Gresham dynamics" created by fraudulent institutions -- a race to the bottom in underwriting. Since fraudulent banks use accounting fraud to manufacture high profits, they do not actually have to use a viable business model. By eliminating control fraud from the financial sector, it will be much easier for honest banks to succeed.

Further, the financial system has massive excess capacity -- as evidenced by the need to create bubble after bubble to find outlets for capacity. Almost all of the innovations in practice and instruments of the past two decades were spurred not by demand but rather by excess capacity. Downsizing the financial sector is critical to restoring it to a size that is commensurate with the needs of the economy.

The cost of not closing control frauds, by contrast, can be staggering. The business practices that maximize the fictional reported income (e.g., making "liar's loans to people who cannot repay their loans) maximize real losses and hyper-inflate financial bubbles. Control frauds destroy wealth at a prodigious rate. The one thing we certainly cannot afford is leaving the control frauds under the control of fraudulent CEOs.

Ilargi: Black is right in his proposals, every single one of them. He deserves all the kudos, respect and most of all support we can muster. Geithner, Bernanke and Eric Holder need to go, Bank of America and Citigroup need to be taken over, and all the paper needs to see daylight. Every single day that doesn't happen costs Americans billions of dollars, it really is as simple as that.

At the moment, for instance, Bank of America investigates its own loans, reluctantly comes up with some "errors", declares all else "sound", and resumes its foreclosures. That's just another joke: independent experts need to look at those loans. Why doesn't that happen? Why can BofA, Citigroup et al continue to be their own judge and jury? It's obviously not because of a lack of indications, or even proof, of questionable, illegal, fraudulent behavior. Just ask Bill Black.

At some point these questions will have to be answered, and the banks will have to reveal their true losses. Really, that time will come. Given the fact that right now the US election circus conveniently bogarts all media headlines, and that a likely Republican overall victory will paralyze the US political system afterwards, it looks more certain than ever that the ansers will not be provided by the government whose constitutional obligation it is to find them. The answers will need to come from the judicial system, from the non-mainstream media, and from the people themselves saying No Mas.

Bill Black Wants BofA Nationalization, Firing Of Bernanke, Geithner And Holder

Tyler Durden: Bill Black, who will soon, together with Neil Barofsky, be a guaranteed shoe-in for the POTUS/VP position (both as independents, of course), was on the Ratigan show today, following on his op-ed from last week calling for the long-overdue nationalization of Bank of America, and discussing the rampant fraud at the heart of mortgage gate. And contrary to ongoing lowball estimates from the like of JPM and Goldman, Black provides numbers about the bank liability that are simply stunning:"Credit Suisse says that by 2006 49% of all mortgage originations were liars loans. When independent folks study fraud, it is in the 80-90% fraud range. That means there were millions of acts of fraud. Those loan frauds occurred because the banks created incentive structure for the loan brokers to bring them the absolute worst of the worst loans, and to lie on the application forms... These frauds came from the banks, and they propagated through the system through a series of echo epidemics...This fraud spread through the system and that's why we have a crisis in foreclosures. This stems from the underlying fraud by the lenders in mortgage loans to the tune of well over a million cases a year by 2005."

Furthermore, Black points out the glaringly obvious, that the Fed should not be in charge of any investigation into mortgage fraud, due to its "massive" conflict of interest, to the tune of $1.5 trillion in MBS/agencies held on the Fed's books, which would be immediately null and voided if rampant MBS fraud is indeed uncovered. Which is precisely why the entitlement of the Fed as supreme regulator (as inspired by the financial generosity of the Wall Street lobby) as part of Frank-Dodd was the one single most destructive decision ever made, and equivalent in many ways with electing America's very own tyrannical despot, whose only interest is making the multi billionaires, into trillionaires, and leaving everyone else in the cold through the eliminating of the savings class and the destruction of the reserve currency.

And it goes much further... to the very top of the US ruling oligarchy in fact. Which is why, as we have claimed from day one, nothing less than a complete reset of the entire kleptocratic system can give any hope for a fresh start. The general public is starting to finally realize this, unfortunately with the dawning realization comes anger, and with anger comes aggression. And from there, broad civil "discontent" is merely a thin white line away. Which is why, we again reiterate our belief, now that America has completely missed its chance for a peaceful resolution, that the reset will have to go first and foremost through the Fed, whose end however will be precipitated by nothing less than an all out social upheaval. We agree with Black's conclusion: "fire Holder, fire Geithner, fire Bernanke, get people in who will enforce the rule of law."

Alas, it is too late. America has proven it has failed as a society in which checks and balances work when Wall Street dangles billion dollar bribes to corrupt and greedy individuals. And just like the market is stretched so far that it is always seconds away from a flash crash, so the entire US society is now mimicking our stock market, and the possibility for an all out social flash crash is no longer trivial.

Foreclose on the Foreclosure Fraudsters, Part 2: Spurious Arguments Against Holding the Fraudsters Accountable

by William K. Black and L. Randall Wray - Huffington Post

Our call for closing down control frauds and stopping the foreclosure frauds typically meets with three objections. First, it is claimed that while there were some bad apple lenders, much of the fraud was committed by borrowers. Our proposal would let fraudulent borrowers remain in homes to which they are not entitled, punishing the banks that were duped. Second, the biggest banks are too important to foreclose. And third, it is not possible to resolve a "too big to fail" institution.

Who is Guilty?

Let us deal with the "borrower fraud" argument first because it is the area containing the most erroneous assumptions.

There was fraud at every step in the home finance food chain: the appraisers were paid to overvalue real estate; mortgage brokers were paid to induce borrowers to accept loan terms they could not possibly afford; loan applications overstated the borrowers' incomes; speculators lied when they claimed that six different homes were their principal dwelling; mortgage securitizers made false reps and warranties about the quality of the packaged loans; credit ratings agencies were overpaid to overrate the securities sold on to investors; and investment banks stuffed collateralized debt obligations with toxic securities that were handpicked by hedge fund managers to ensure they would self destruct.

That homeowners would default on the nonprime mortgages was a foregone conclusion throughout the industry -- indeed, it was the desired outcome. This was something the lending side knew, but which few on the borrowing side could have realized. The homeowners were typically fraudulently induced by the lenders and the lenders' agents (the loan brokers) to enter into nonprime mortgages. The lenders knew the "loan to value" (LTV) ratios and income to debt ratios that they wanted the borrower to (appear to) meet in order to make it possible for the lender to sell the nonprime loan at a premium. LTV can be gimmicked by inflating the appraisal.

The debt to income ratios can be gimmicked by inflating income. "Liar's" loan lenders used that loan format because it allowed the lender to simultaneously loan to a vast number of borrowers that could not repay their home loans, at a premium yield, while making it look to the purchaser of the loan that it was relatively low risk. Liar's loans maximized the lender's reported income, which maximized the CEO's compensation.

The problem is that only the most sophisticated nonprime borrowers (the speculators who bought six homes) (1) knew the key ratios they had to appear to meet, (2) had the ability to induce an appraiser to inflate substantially the reported market value of the home, and (3) knew how to create false financial information that was internally consistent and credible. The solution was for the lender and the lender's agents to (1) instruct the borrower to report a certain income or even to fill out the application with false information, (2) suborn an appraiser to provide the necessary inflated market value, and (3) create fraudulent financial information that had at least minimal coherence.

When the overburdened homeowner began missing payments, late fees and higher interest rates kicked-in, boosting the stated income of mortgage servicers and the value of the securities. Not coincidentally, the biggest banks own the servicers and could maximize claims against the mortgages by running up the late fees. It was quite convenient to "misplace" mortgage payments, so even homeowners who were never delinquent could get hit with fees and higher rates. And when payments were received, the servicers would (illegally) apply them first to the late fees, meaning the homeowners were unknowingly still missing mortgage payments. The foreclosure process itself generates big fees for the SDI banks.

And, miracle of miracles, the banks would end up with the homes and get to restart the whole process again -- from resale of the home through the financing, securitizing, and fee-for-servicing juggernaut. Unfortunately, it did not go quite as smoothly as planned. The SDIs were supposed to act like neutron bombs -- killing the homeowners but leaving the homes standing, to be resold. The problem is that wiping out borrowers lowered the value of real estate, crushing not only the real estate market but also construction and through to all associated sectors from furniture and home restoration supplies to big ticket purchases that rely on home equity loans. It also led to questions about the value of the securitized toxic waste manufactured and held directly or indirectly by financial institutions.

Next, a few judges began to question the foreclosures, as they saw case after case in which the banks claimed to have lost the paperwork or submitted amateurishly forged documents. Or, several banks would go after the same homeowner, each claiming to hold the same mortgage (Bear sold the same mortgage over and over). Insiders began to offer depositions exposing fraud and perjury. It became apparent that in many and perhaps most cases, the trusts responsible for the securities (often these are "special purpose" subsidiaries of the banks) never received the "notes" signed by the borrowers -- as required by both IRS tax code and by 45 of the US states. Without the notes, billions of dollars of back taxes could be due, and the foreclosures violate state law. Finally, the Attorneys General of all fifty states called for a foreclosure moratorium.

What to do? We suggest an immediate moratorium on foreclosures and a requirement that all notes be produced by purported holders of mortgages within a reasonable length of time. If they cannot be found, the mortgages -- as well as the securities that pool them -- are no longer valid. That means that the homeowners are not indebted, and that the homes are owned free and clear. And that, dear bankers, is a big, big problem. It is also the law -- without evidence of debt, there is no debtor and no creditor.

Commentators are horrified that a foreclosure moratorium would let "deadbeat" borrowers remain in their homes while delinquent in their payments. The speculators that purchased "MacMansions" and stated on six separate loan applications that each house was their principal dwelling are frauds. The moratorium would (briefly) reward fraudulent borrowers while (briefly) punishing the fraudulent banks. This is true.

It is not possible to separate "worthy" borrowers who were duped by banks from all "unworthy" borrowers who knew the loan applications were false. Indeed, given the millions of borrowers that received liar's loans, even if the borrowers were all frauds we could not possibly prosecute all of them due to lack of resources. We currently prosecute roughly 1,000 mortgage fraud cases annually at the federal level. If we used all of our resources to investigate and prosecute fraudulent mortgage borrowers exclusively we would be able to prosecute less than one-tenth of one percent of those frauds.

The losses that the fraudulent nonprime lenders caused are vastly greater than the losses caused by fraudulent borrowers, so no rational prosecutor would use his scarce resources to prosecute individual nonprime borrowers. Moreover, prosecutions of individual borrowers for alleged fraud in the applications would be difficult to win against competent defense counsel because it will not be possible to infer the borrower's intent and knowledge and whether the loan agent instructed him to enter specified information on the application. We are not arguing that the speculator who committed fraud while buying six homes should be allowed to walk free. We are simply arguing that it makes no sense to use limited judicial resources to go after owner-occupier households where it will be almost impossible to prove intent to defraud.

On the other hand, we can infer a lender's fraudulent intent because it is financially sophisticated and has expertise in lending. An honest mortgage lender would not make "liar's loans" because absence of proper underwriting inherently produces loans that are expected to default. Yet, in 2006 just about half of all mortgages originated were liar's loans. Banks happily advertised specialization in "no doc" and NINJA loans. There can be no question about intent -- the intent was fraud, plain and simple. Fraud on the part of credit raters is equally easy to infer -- we have the internal emails that document intent to defraud securities purchasers by "pay to play" schemes. And the fraud committed by the investment banks that pooled the mortgages is also well documented. These entities committed tens of thousands and even millions of frauds each. For obvious efficiency reasons, that is where our judicial resources ought to be directed.

Macro Effects and Culpability

There is one other consideration that biases the case in favor of borrowers. Many homeowners were sold on the idea that "real estate values only go up" -- and quite a few planned to refinance on better terms, or even to flip the house at a price that would allow them to pay-off a mortgage they could not otherwise afford. We realize that it is not easy to shed tears for speculators foiled by the market, and that is not our point.

What is important to understand, however, is that the financial sector is largely culpable for the generation of speculative frenzy, the creation of the "financial weapons of mass destruction", and the transformation toward financial fragility that finally collapsed in 2007. In the aftermath we lost 10 million jobs and millions of homeowners lost their homes. The "collateral damage" inflicted by the SDIs is now endangering tens of millions of American families -- most of whom played no role in the speculative euphoria. Almost half of American homeowners are already underwater or on the verge of going under. In short, it was Wall Street that turned our homes over to a financial casino -- and so far virtually all the losses have been suffered on Main Street.

This culpability is at the aggregate scale and of course no individual bank can be held liable in court for the collapse of the financial system. Rather, each bank's guilt must be assessed according to its own fraud. However, a national moratorium on foreclosures must be evaluated at the macro level, and justified on the basis of the aggregate costs, benefits, and moral implications. And certainly at the aggregate level that must be considered by President Obama, the benefits to the majority of Americans clearly outweigh the costs imposed on the relatively few. And the morality is also on the side of homeowners and clearly against the banks.

Closing the control frauds would actually benefit honest bankers by eliminating the "Gresham dynamics" created by fraudulent institutions -- a race to the bottom in underwriting. Since fraudulent banks use accounting fraud to manufacture high profits, they do not actually have to use a viable business model. By eliminating control fraud from the financial sector, it will be much easier for honest banks to succeed.

Further, the financial system has massive excess capacity -- as evidenced by the need to create bubble after bubble to find outlets for capacity. Almost all of the innovations in practice and instruments of the past two decades were spurred not by demand but rather by excess capacity. Downsizing the financial sector is critical to restoring it to a size that is commensurate with the needs of the economy.

The cost of not closing control frauds, by contrast, can be staggering. The business practices that maximize the fictional reported income (e.g., making "liar's loans to people who cannot repay their loans) maximize real losses and hyper-inflate financial bubbles. Control frauds destroy wealth at a prodigious rate. The one thing we certainly cannot afford is leaving the control frauds under the control of fraudulent CEOs.

Can the Frauds be Foreclosed?

The assertion that the SDIs cannot be resolved because of their size is unsupported. Very large institutions have already been resolved both in this country and abroad. The "too big to fail" (TBTF) doctrine has always been unproven, dangerous, and counter to the law. An institution that is not permitted to fail faces obvious adverse incentive problems. It also destroys healthy competition with institutions that are not considered TBTF. It encourages risk-taking and fraud. And it subverts the law, which requires that insolvent institutions must be resolved.

As we write this piece, the markets are taking it upon themselves to begin to close down the control frauds -- with homeowners fighting the foreclosures and investors demanding that the banks take back the toxic waste. Unfortunately, following the market solution will be a long-drawn-out and costly process -- both in terms of tying up the judicial system but also in terms of the uncertainty and despair that will persist. At the end of that process, the banks will have to be resolved. No matter how much the politicians dislike it, they will end up with the banks in their hands -- either now or later. Taking them now is the right thing to do.

To fix the economy, let bad banks die

by Nicole Gelinas - LA Times

Bad banks, and their bad business model of willful incompetence, are still alive, and dragging down the recovery.

Since the housing market peaked in 2006, the nation has suffered through nearly half a decade of financial and economic hell. It's past time for the politicians to do what they should have done in the first place. That is, protect the nation's priceless assets: the rule of law and free markets. Instead, the pols are protecting the worthless assets of zombie banks that do not know how to be banks.

Two years ago, many of the nation's largest banks should have failed — because their business model failed. That business model was willful incompetence. Back then, banks, including Countrywide Financial, now part of Bank of America, showcased this incompetence in helping homeowners borrow money they could never repay. Today, thanks to Washington's bailouts, the bad banks are still alive. So is their disastrous business model. The banks now showcase their incompetency in their inability to foreclose on defaulted homeowners in an orderly, timely and non-fraudulent fashion.

In the past two weeks, Bank of America, JPMorgan Chase and some competitors temporarily halted most foreclosures. The banks stopped foreclosing as employees came forward to say that they had defrauded courts — that is, falsely attested that they knew the facts of thousands of foreclosure cases when they did not. Often, the banks cannot locate the documents that confirm a lender's right to foreclose. Even as banks resume foreclosures, as Bank of America did this week, they have a motive to proceed slowly because they do not want to book the losses that come with property sales.

But the banks' dawdling imperils economic recovery, in ways prosaic and profound.

The prosaic: Borrowers stay stuck in homes they can't afford, meaning they can't get on with their lives. Prospective home buyers still can't afford property, and those who can remain wary because until lenders clear their backlog of foreclosures, house prices won't fall to realistic levels. At the same time, small businesses cannot create jobs because banks and investors stuck with old, bad loans don't want to make new ones.

The profound: Botched foreclosures erode the property rights on which the nation's prosperity rests. When a person buys a home, he must know that he enjoys the legal right to keep and sell that property. Property rights break down if, three years from now, a former owner can say that she did not get her day in court and therefore a sale should be invalidated.

Thankfully, regulators, including the Federal Reserve, have the power to act. Banks, after all, must operate safely and soundly. By definition, a financial institution cannot be safe and sound if its executives have no idea who owns what and who owes what. Nor can a bank operate safely and soundly if it cannot properly value its or its customers' assets, something it cannot do if it has not mastered the work of asserting legal rights to those assets.

Here's what Washington should do: Regulators should require banks to promptly fulfill their safety and soundness duties. Banks would do so, obviously, by foreclosing on defaulted homeowners in a timely, consistent and honest fashion, even if it means that the firms must shell out big money to hire enough qualified people. Alternatively, the banks could choose —in the same timely fashion— to reduce the amount of money that borrowers owe so that borrowers could afford to stay. One way or the other, it's time to get it over with.

Here's what Washington will do, though: nothing. Regulators know that if they force banks to foreclose quickly, legally and consistently, the firms would have to take significant, perhaps crippling, losses on the loans on their books. Fannie Mae and Freddie Mac, which hold and insure many loans, would have to take fresh losses too. Further, investors who purchased mortgage securities could sue, alleging, among other things, that underwriters misrepresented third parties' capacity to ensure that someone would oversee mortgage paperwork on a day-to-day basis.

In other words, big banks could fail. And that's the problem. Despite having signed into law the Dodd-Frank financial reform bill three months ago, the White House still has not created a predictable way in which large financial firms can go under, with investors taking warranted losses. Instead, the new law directs regulators to make up the job as they go along. Regulators are terrified of testing their discretion and of precipitating a 2008-style panic.

Smart bankers feel this fear. They know that regulators will not cause markets to question a large bank's viability, even if it means enabling the slow strangulation of economic recovery. This knowledge explains the banks' casual attitude toward their public trust. Banks remain permanent wards of the state, immune from full market and legal discipline.

As for the politicians, their policy is ignorance. President Obama doesn't want to have to ask for his own TARP. Congressional Republicans want no reminder of Bush-era bailouts. They maintain the fiction that the financial crisis is in the past.

Someday, reality will intrude, and it won't discriminate over whether a Democrat or a Republican is in the White House. In the meantime, Washington's policy of ignoring irretrievably broken banks could inflict another half-decade of "housing" crisis on the rest of us.

Bernanke Leaps into a Liquidity Trap

by John Hussman - Hussmanfunds

"There is the possibility... that after the rate of interest has fallen to a certain level, liquidity preference is virtually absolute in the sense that almost everyone prefers cash to holding a debt at so low a rate of interest. In this event, the monetary authority would have lost effective control.”

John Maynard Keynes, The General Theory

One of the many controversies regarding Keynesian economic theory centers around the idea of a "liquidity trap." Apart from suggesting the potential risk, Keynes himself did not focus much of his analysis on the idea, so much of what passes for debate is based on the ideas of economists other than Keynes, particularly Keynes' contemporary John Hicks. In the Hicksian interpretation of the liquidity trap, monetary policy transmits its effect on the real economy by way of interest rates. In that view, the loss of monetary control occurs because at some point, a further reduction of interest rates fails to stimulate additional demand for capital investment.

Alternatively, monetary policy might transmit its effect on the real economy by directly altering the quantity of funds available to lend. In that view, a liquidity trap would be characterized by the failure of real investment and output to expand in response to increases in the monetary base (currency and reserves). In either case, the hallmark of a liquidity trap is that holdings of money become "infinitely elastic." As the monetary base is increased, banks, corporations and individuals simply choose to hold onto those additional money balances, with no effect on the real economy.

The typical Econ 101 chart of this is drawn in terms of "liquidity preference," that is, desired cash holdings, plotted against interest rates. When interest rates are high, people choose to hold less cash because cash doesn't earn interest. As interest rates decline toward zero (and especially if the Fed chooses to pay banks interest on cash reserves, which is presently the case), there is no effective difference between holding riskless debt securities (say, Treasury bills) and riskless cash balances, so additional cash balances are simply kept idle.

Velocity

A related way to think about a liquidity trap is in terms of monetary velocity: nominal GDP divided by the monetary base. (The identity, which is true by definition, is M * V = P * Y. The monetary base times velocity is equal to the price level times real output).

Velocity is just the dollar value of GDP that the economy produces per dollar of monetary base. You can also think of velocity as the number of times that one dollar "turns over" each year to purchase goods and services in the economy. Rising velocity implies that money is "turning over" more rapidly, so that nominal GDP is increasing faster than the stock of money.

If velocity rises, holding the quantity of money constant, you'll observe either growth in real output or inflation. Falling velocity implies that a given stock of money is being hoarded, so that nominal GDP is growing slower than the stock of money. If velocity falls, holding the quantity of money constant, you'll observe either a decline in real GDP or deflation.

The belief that an increase in the money supply will result in an increase in GDP relies on the assumption that velocity will not decline in proportion to the increase in money. Unfortunately for the proponents of "quantitative easing," this assumption fails spectacularly in the data - both in the U.S. and internationally - particularly at zero interest rates.

How to spot a liquidity trap

The chart below plots the velocity of the U.S. monetary base against interest rates since 1947. Since high money holdings correspond to low velocity, the graph is simply the mirror image of the theoretical chart above.

Few theoretical relationships in economics hold quite this well. Recall that a Keynesian liquidity trap occurs at the point when interest rates become so low that cash balances are passively held regardless of their size. The relationship between interest rates and velocity therefore goes flat at low interest rates, since increases in the money stock simply produce a proportional decline in velocity, without requiring any further decline in yields. Notice the cluster of observations where interest rates are zero? Those are the most recent data points.

One might argue that while short-term interest rates are essentially zero, long-term interest rates are not, which might leave some room for a "Hicksian" effect from QE - that is, a boost to investment and economic activity in response to a further decline in long-term interest rates. The problem here is that longer-term interest rates, in an expectations sense, are already essentially at zero. The remaining yield on longer-term bonds is a risk premium that is commensurate with U.S. interest rate volatility (Japanese risk premiums are lower, but they also have nearly zero interest rate variability).

So QE at this point represents little but an effort to drive risk premiums to levels that are inadequate to compensate investors for risk. This is unlikely to go well. Moreover, as noted below, the precise level of long-term interest rates is not the main constraint on borrowing here. The key issues are the rational desire to reduce debt loads, and the inadequacy of profitable investment opportunities in an economy flooded with excess capacity.

One of the most fascinating aspects of the current debate about monetary policy is the belief that changes in the money stock are tightly related either to GDP growth or inflation at all. Look at the historical data, and you will find no evidence of it. Over the years, I've repeatedly emphasized that inflation is primarily a reflection of fiscal policy - specifically, growth in the outstanding quantity of government liabilities, regardless of their form, in order to finance unproductive spending. Look at the experience of the 1970's (which followed large expansions in transfer payments), as well as every historical hyperinflation, and you'll find massive increases in government spending that were made without regard to productivity (Germany's hyperinflation, for instance, was provoked by continuous wage payments to striking workers).

Likewise, real economic growth has no observable correlation with growth in the monetary base (the correlation is actually slightly negative but insignificant). Rather, economic growth is the result of hundreds of millions of individual decision-makers, each acting in their best interests to shift their consumption plans, saving, and investment in response to desirable opportunities that they face. Their behavior cannot simply be induced by changes in the money supply or in interest rates, absent those desirable opportunities.

You can see why monetary base manipulations have so little effect on GDP by examining U.S. data since 1947. Expand the quantity of base money, and it turns out that velocity falls in nearly direct proportion. The cluster of points at the bottom right reflect the most recent data.

[Geek's Note: The slope of the relationship plotted above is approximately -1, while the Y intercept is just over 6%, which makes sense, and reflects the long-term growth of nominal GDP, virtually independent of variations in the monetary base. For example, 6% growth in nominal GDP is consistent with 0% M and 6% V, 5% M and 1% V, 10% M and -4% V, etc. There is somewhat more scatter in 3-year, 2-year and 1-year charts, but it is random scatter. If expansions in base money were correlated with predictably higher GDP growth, and contractions in base money were correlated with predictably lower GDP growth, the slope of the line would be flatter and the fit would still be reasonably good. We don't observe this.]

Just to drive the point home, the chart below presents the same historical relationship in Japanese data over the past two decades. One wonders why anyone expects quantitative easing in the U.S. to be any less futile than it was in Japan.

Simply put, monetary policy is far less effective in affecting real (or even nominal) economic activity than investors seem to believe. The main effect of a change in the monetary base is to change monetary velocity and short term interest rates. Once short term interest rates drop to zero, further expansions in base money simply induce a proportional collapse in velocity.

I should emphasize that the Federal Reserve does have an essential role in providing liquidity during periods of crisis, such as bank runs, when people are rapidly converting bank deposits into currency. Undoubtedly, we would have preferred the Fed to have provided that liquidity in recent years through open market operations using Treasury securities, rather than outright purchases of the debt securities of insolvent financial institutions, which the public is now on the hook to make whole. The Fed should not be in the insolvency bailout game. Outside of open market operations using Treasuries, Fed loans during a crisis should be exactly that, loans - and preferably following Bagehot's Rule ("lend freely but at a high rate of interest"). Moreover, those loans must be senior to any obligation to bank bondholders - the public's claim should precede private claims. In any event, when liquidity constraints are truly binding, the Fed has an essential function in the economy.

At present, however, the governors of the Fed are creating massive distortions in the financial markets with little hope of improving real economic growth or employment. There is no question that the Fed has the ability to affect the supply of base money, and can affect the level of long-term interest rates given a sufficient volume of intervention. The real issue is that neither of these factors are currently imposing a binding constraint on economic growth, so there is no benefit in relaxing them further. The Fed is pushing on a string.

Toy blocks

Certain economic equations and regularities make it tempting to assume that there are simple cause-effect relationships that would allow a policy maker to directly manipulate prices and output. While the Fed can control the monetary base, the behavior of prices and output is based on a whole range of factors outside of the Fed's control. Except at the shortest maturities, interest rates are also a function of factors well beyond monetary policy.

Analysts and even policy makers often ignore equilibrium, preferring to think only in terms of demand, or only in terms of supply. For example, it is widely believed that lower real interest rates will result in higher economic growth. But in fact, the historical correlation between real interest rates and GDP growth has been positive - on balance, higher real interest rates are associated with higher economic growth over the following year. This is because higher rates reflect strong demand for loans and an abundance of desirable investment projects.

Of course, nobody would propose a policy of raising real interest rates to stimulate economic activity, because they would recognize that higher real interest rates were an effect of strong loan demand, and could not be used to cause it. Yet despite the fact that loan demand is weak at present, due to the lack of desirable investment projects and the desire to reduce debt loads (which has in turn contributed to keeping interest rates low), the Fed seems to believe that it can eliminate these problems simply by depressing interest rates further. Memo to Ben Bernanke: Loan demand is inelastic here, and for good reason. Whatever happened to thinking in terms of equilibrium?

Neither economic growth nor the demand for loans are a simple function of interest rates. If consumers wish to reduce their debt, and companies do not have a desirable menu of potential investments, there is little benefit in reducing interest rates by another percentage point, because the precise cost of borrowing is not the issue. The current thinking by the FOMC seems to treat individual economic actors as little unthinking toy blocks that can be moved into the desired position at will. Instead, our policy makers should be carefully examining the constraints and interests that are important to people and act in a way that responsibly addresses those constraints.

A good example of this "toy block" thinking is the notion of forcing individuals to spend more and save less by increasing people's expectations about inflation (which would drive real interest rates to negative levels). As I noted last week, if one examines economic history, one quickly discovers that just as lower nominal interest rates are associated with lower monetary velocity, negative real interest rates are associated with lower velocity of commodities (hoarding). Look at the price of gold since 1975.

When real interest rates have been negative (even simply measured as the 3-month Treasury bill yield minus trailing annual CPI inflation), gold prices have appreciated at a 20.7% annual rate. In contrast, when real interest rates have been positive, gold has appreciated at just 2.1% annually. The tendency toward commodity hoarding is particularly strong when economic conditions are very weak and desirable options for real investment are not available. When real interest rates have been negative and the Purchasing Managers Index has been below 50, the XAU gold index has appreciated at an 85.7% annual rate, compared with a rate of just 0.1% when neither has been true. Despite these tendencies, investors should be aware that the volatility of gold stocks can often be intolerable, so finer methods of analysis are also essential.

Quantitative easing promises to have little effect except to provoke commodity hoarding, a decline in bond yields to levels that reflect nothing but risk premiums for maturity risk, and an expansion in stock valuations to levels that have rarely been sustained for long (the current Shiller P/E of 22 for the S&P 500 has typically been followed by 5-10 year total returns below 5% annually). The Fed is not helping the economy - it is encouraging a bubble in risky assets, and an increasingly unstable one at that. The Fed has now placed itself in the position where small changes in its announced policy could have disastrous effects on a whole range of financial markets. This is not sound economic thinking but misguided tinkering with the stability of the economy.

Implications for Policy

In 1978, MIT economist Nathaniel Mass developed a framework for the liquidity trap based on microeconomic theory - rational decisions made at the level of individual consumers and firms. The economic dynamics resulting from the model he suggested seem strikingly familiar in the context of the recent economic downturn. They offer a useful way to think about the current economic environment, and appropriate policy responses that might be taken.

"The theory revolves around a set of forces that for a period of time promote cumulative expansion of capital formation, but eventually lead to overexpansion of capital production capacity and then into a situation where excess capacity strongly counteracts expansionary monetary policies.

"The capital boom followed by depression runs much longer than the usual short-term business cycle, and is powerfully driven by capital investment interactions. The weak impact of monetary stimulus on real activity arises because additional money has little force in stimulating additional capital investment during a period of general overcapacity. Instead, money is withheld in idle balances when profitable investment opportunities are scarce."

In one illustration of the model, Mass introduces a monetary stimulus much like what Alan Greenspan engineered following the 2000-2002 recession (which was also preceded by an unusually large buildup of excess capacity, leading to an investment-led downturn). Though Greenspan's easy-money policy didn't prompt a great deal of business investment, it did help to fuel the expansion in another form of investment, specifically housing. Mass describes the resulting economic dynamics:

"Following the monetary intervention, relatively easy money provides a greater incentive to order capital... But now the overcapacity that characterizes the peak in the production of capital goods reaches an even higher level than without the stimulus. This overcapacity eventually makes further investment even less attractive and causes the decline in capital output to proceed from a higher peak and at a faster pace. Due to persistent excess capital which cannot be reduced as fast as labor can be cut back to alleviate excess production, unemployment actually remains higher on the average following the drop in production."

In what reads today as a further warning against Bernanke-style quantitative easing, Mass observed:

"Even aggressive monetary intervention can do little to correct excess capital.. Once excess capacity develops, the forces that previously led to aggressive expansion are almost played out. Efforts to prolong high investment can produce even more excess capital and lead to a more pronounced readjustment later."

Mass concluded his 1978 paper with an observation from economist Robert Gordon:

"Why was the recovery of the 1930's so slow and halting in the United States, and why did it stop so far short of full employment? We have seen that the trouble lay primarily in the lack of inducement to invest. Even with abnormally low interest rates, the economy was unable to generate a volume of investment high enough to raise aggregate demand to the full employment level."

I've generally been critical of Keynes' willingness to advocate government spending regardless of its quality, which focused too little on the long-term effects of diverting private resources to potentially unproductive uses. His remark that "In the long-run we are all dead" was a reflection of this indifference. Still, I do believe that fiscal responses can be useful in a protracted economic downturn, and can include projects such as public infrastructure, incentives for research and development, and investment incentives in sectors that are not burdened with overcapacity. Additional deficit spending is harmful when it fails to produce a stream of future output sufficient to service the debt, so the expected productivity of these projects is the essential consideration. Given present economic conditions, it appears clear that Keynes was right about the dangers of easy monetary policy when an economic downturn results from overcapacity.

Scary New Wage Data

by David Cay Johnston - Tax.com

Now for some really scary breaking news, from the latest payroll tax data.

Every 34th wage earner in America in 2008 went all of 2009 without earning a single dollar, new data from the Social Security Administration show. Total wages, median wages, and average wages all declined, but at the very top, salaries grew more than fivefold. Not a single news organization reported this data when it was released October 15, searches of Google and the Nexis databases show. Nor did any blog, so the citizen journalists and professional economists did no better than the newsroom pros in reporting this basic information about our economy.

The new data hold important lessons for economic growth and tax policy and take on added meaning when examined in light of tax return data back to 1950. The story the numbers tell is one of a strengthening economic base with income growing fastest at the bottom until, in 1981, we made an abrupt change in tax and economic policy. Since then the base has fared poorly while huge economic gains piled up at the very top, along with much lower tax burdens.

A weak foundation cannot properly support a massive superstructure, as the leaning Tower of Pisa shows. The latest wage data show the disastrous results some of us warned about, although like the famous tower, the economy only lists badly and has not collapsed. Measured in 2009 dollars, total wages fell to just above $5.9 trillion, down $215 billion from the previous year. Compared with 2007, when the economy peaked, total wages were down $313 billion or 5 percent in real terms.

The number of Americans with any wages in 2009 fell by more than 4.5 million compared with the previous year. Because the population grew by about 1 percent, the number of idle hands and minds grew by 6 million. These figures show, far more powerfully than the official unemployment measure known as U3, how both widespread and deep the loss of jobs was in 2009. While the official unemployment rate is just under 10 percent, deeper analysis of the data by economist John Williams at http://www.shadowstats.com shows a real under- and unemployment rate of more than 22 percent.

Only 150.9 million Americans reported any wage income in 2009. That put us below 2005, when 151.6 million Americans reported wages, and only slightly ahead of 2004, when 149.4 million Americans held at least one paying job. For those who did find work in 2009, the average wage slipped to $39,269, down $243 or 0.6 percent, compared with the previous year in 2009 dollars. The median wage declined by the same ratio, down $159 to $26,261, meaning half of all workers made $505 a week or less. Significantly, the 2009 median wage was $37 less than in 2000.

To give this some perspective, from 1992 to 2000 the number of people earning any wages grew by 21 million, but nine years later just 2.8 million more people had any work. These wage data, based on the Medicare flat tax on all compensation, tell us only about the number of people who earned wages and how much. They tell us nothing about whether these individuals were underemployed, had to work more than one job, earned fringe benefits, or were employed at a level commensurate with their abilities.

But they do give us a stunning picture of what’s happening at the very top of the compensation ladder in America. The number of Americans making $50 million or more, the top income category in the data, fell from 131 in 2008 to 74 last year. But that’s only part of the story. The average wage in this top category increased from $91.2 million in 2008 to an astonishing $518.8 million in 2009. That’s nearly $10 million in weekly pay!

You read that right. In the Great Recession year of 2009 (officially just the first half of the year), the average pay of the very highest-income Americans was more than five times their average wages and bonuses in 2008. And even though their numbers shrank by 43 percent, this group’s total compensation was 3.2 times larger in 2009 than in 2008, accounting for 0.6 percent of all pay. These 74 people made as much as the 19 million lowest-paid people in America, who constitute one in every eight workers.

Average Median Wages, 1990 to 2009 (in 2009$)

Back in 1994, when the top category the government reported on was $20 million or more of compensation, only 25 people were in that rarefied atmosphere, and their average earnings came to just under $45 million in 2009 dollars.

What does this all mean? It is the latest, and in this case quite dramatic, evidence that our economic policies in Washington are undermining the nation as a whole.We have created a tax system that changes continually as politicians manipulate it to extract campaign donations. We have enabled ""free trade’’ that is nothing of the sort, but rather tax-subsidized mechanisms that encourage American manufacturers to close their domestic factories, fire workers, and then use cheap labor in China for products they send right back to the United States. This has created enormous downward pressure on wages, and not just for factory workers.

Combined with government policies that have reduced the share of private-sector workers in unions by more than two-thirds — while our competitors in Canada, Europe, and Japan continue to have highly unionized workforces — the net effect has been disastrous for the vast majority of American workers. And of course, less money earned from labor translates into less money to finance the United States of America.

This systematic destruction of the working class and middle class has come during an era notable for celebrating the super-rich just for being super-rich. From the Forbes 400 launch in 1982 and Robin Leach’s Lifestyles of the Rich and Famous in 1984 to the faux reality of the multiplying Real Housewives shows, money voyeurism has grown in tandem with stagnant to falling incomes for the vast majority. There has also been huge income growth at the top and the economic children of income inequality: budget deficits and malign neglect of our commonwealth.

This orgy of money exhibitionism has created a society in which commas — it takes three to be a billionaire — count more than character. We have gone so far down this path that we bailed out bankers, allowing them to keep the untaxed wealth in their deferral accounts and, with a few exceptions, retaining shareholder value, while wiping out investors in General Motors and Chrysler as a condition of their bailouts. And while autoworkers had to take severe pay cuts, bonus time on Wall Street is at new record levels.

The American economy in the three decades before Ronald Reagan’s election did not produce a mass audience for celebrating wealth. In that era, books that emphasized character sold better than today. During the years from 1950 to 1980, the share of total income going to those at the top declined, and the real incomes of the vast majority grew much more quickly than did nearly all incomes at the very top. In those years, America had the money, and vision, to invest in the future through education, research, and infrastructure.

In nearly three decades of Reaganism, however, we have become a society of mine-here-and-now. Now what we hear from Washington is about today, not tomorrow. War without sacrifice (or a congressional declaration). Savings without interest. More government services while lowering taxes.

In this era, the incomes of the vast majority have barely grown while incomes at the top have soared. Reaganism has trimmed the base of the income ladder while placing a much heavier weight on the top. Narrowing the base while adding weight to the apex does not make a stable structure. Here are some numbers that may surprise those ages 50 and under, taken from the latest analysis of tax return data by Emmanuel Saez and Thomas Piketty, who have won worldwide praise for their groundbreaking work examining changes in income distribution:

Bottom 90 Percent Income Share Changes

So a three-decade era in which the bottom 90 percent increased their share of all income slightly was followed by a 28-year period at whose end income had fallen sharply. The 2009 data show that it has only gotten worse since then. While the vast majority must get by on a much smaller share of the national income pie, the re-slicing resulted in concentrated benefits at the top. The top 10 percent enjoyed a nearly 40 percent increase in their share of the income pie. But within the top 10 percent, the re-slicing of the income pie between 1980 and 2008 was also heavily weighted to the top.

Those in the 90th to 95th percentile income category saw their income share rise by just 0.24 percentage points. The 95th to 99th income category got 2.43 percentage points more slice of the national income pie. That means that of the 13.59 percentage points of increased pie going to the top 10 percent of Americans, the top 1 percent earned almost 11 percentage points of it. Now look at how the pie was sliced within the top 1 percent:

Income Share Gains, in Percentage Points, in 2008 Over 1980 for Top 1% of Earners

Notice that as you move to the right, the numbers of taxpayers shrink, but the percentage points grow. The theme: more and more for fewer and fewer. Income shares tell us about how groups are doing relative to one another. But you can’t spend income shares, so let’s look at incomes.

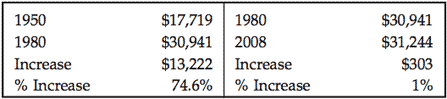

From 1950 to 1980, the average income of the bottom 90 percent grew tremendously. Not so since then:

Had income growth from 1950 to 1980 continued at the same rate for the next 28 years, the average income of the bottom 90 percent in 2008 would have been 68 percent higher, instead of just 1 percent more. That would have meant an average income for the vast majority of $52,051, or $21,110 more than actual 2008 incomes. How different America would be today if the typical family had $406 more each week - less debt, more savings, and more consumption.

So how about the top? This is where the changes in incomes in these two eras become interesting, very interesting. What the figures below show is that the closer you got to the top of the ladder in the era from 1950 to 1980, the smaller your relative increase in income, except for the very top, whose gains were slightly more than those of the bottom 90 percent. Since 1980, however, the bottom 90 percent of Americans have seen their incomes go nowhere, while on the highest steps of the income ladder, the further up you are, the greater your gains.

Add in today’s decreased number of jobs, and all these data add up to policies that can be described with one word: failed.

The 99ers

"60 Minutes" profiles the underemployed and unemployed.

70% Of All Stock Market Trades Are Held for An Average of 11 SECONDS

by Washington's Blog

The Fourteenth Banker writes today:In the stock market, program trading dominates volume. I heard recently that 70% of trade positions are held for an average of 11 seconds.He's correct.

As the New York Times dealbook noted in May:

These are short-term bets. Very short. The founder of Tradebot, in Kansas City, Mo., told students in 2008 that his firm typically held stocks for 11 seconds. Tradebot, one of the biggest high-frequency traders around, had not had a losing day in four years, he said

Similarly, FT's Martin Wheatley pointed out last month:I know of one HFT firm operated out of the west coast of the US that boasts its average holding period for US equities is 11 seconds

And market analyst Peter Cohan writes at AOL's Daily Finance:70% of trading volume on the major exchanges is conducted by high-frequency traders who hold a stock for an average of 11 seconds.

The fact that the vast majority of stock market trades are held for 11 seconds shows that the stock market is not a real market with real traders governed by the law of supply and demand, and that there is no real price discovery.

But as Tyler Durden points out, alot can happen in 11 seconds when the players are high-powered computers:07-29-10

BATS "Flag Repeater". 15,000 quotes in 11 seconds, dropping the ASK price 1 penny each quote from $9.36 to $8.58 and back up again.

Debt sales highlight abnormal conditions

by Aline van Duyn, Michael Mackenzie and Nicole Bullock - Financial Times

The abnormal state of the credit markets came into focus as the US Treasury sold bonds with negative interest rates for the first time and Goldman Sachs prepared to issue its first 50-year debt deal. Both developments on Monday highlighted the difficult choices facing investors at a time when interest rates are at historical lows and the Federal Reserve is moving towards more asset purchases aimed at boosting the economy and staving off deflation. Investors who believe the Fed will succeed in its efforts – which would lead to higher inflation – accepted a yield of minus 0.55 per cent on $10bn of Treasury Inflation Protected Securities – or Tips – which compensate holders if the consumer price index rises.

At the same time, retail investors looking for higher yields in the current low interest-rate environment were targeted by Goldman, which prepared to sell $250m of 50-year bonds that are expected to pay interest of up to 6.25 per cent. “The Fed has been sending the message that its cheque book is ready and it will do what it takes to reflate the economy,” said Jan Loeys, head of global asset allocation at JPMorgan Chase. “What no one knows is whether inflation will start to show in two weeks or two years.”

Mr Loeys added: “We are seeing longer-term thinking clients becoming increasingly wary of bonds and hedging against inflation. Shorter-term thinkers are still willing to still buy bonds, on the presumption that they are nimble enough to get out when inflation comes to push yields up.” Long-term institutional buyers purchased 39 per cent of the $10bn Tips sale, up from an average share of 30 per cent for the prior six Tips sales.

The negative rate for Tips is a boon for the Treasury as it lowers its financing costs. But it may herald problems for bondholders in the future, since higher inflation would erode the value of fixed-income securities without inflation protection. Expectations for inflation over the next five years – based on comparing Treasury yields and those for Tips – have risen as high as 1.75 per cent this month, up from 1.13 per cent in August.

Analysts say they doubt the current environment of low nominal Treasury yields and strong demand for Tips with negative rates can last. “If inflation protection is in such strong demand that investors will buy aggressively at negative real yields, then surely at some point investors have to question the wisdom of buying nominal Treasuries with such low yields,” said Richard Gilhooly, strategist at TD Securities. With official interest rates at close to zero per cent, investors also have been buying longer-dated corporate bonds or debt sold by riskier companies in search of higher yields.

U.S. home prices drop 0.2% in August

by Greg Robb - MarketWatch

Home prices fell 0.2% in August, according to the Case-Shiller home price index released Tuesday by Standard & Poor’s, in a report labelled “disappointing” by its compilers. This is the first drop in the index after four straight monthly gains as demand spiked by the homebuyer tax credit that expired at the end of April. Prices fell in 15 of the 20 metropolitan areas tracked by Case-Shiller in August compared with July. Annualized price growth slowed to 1.7% from 3.2% in July.

Chicago, Detroit, Las Vegas, New York and Washington, D.C. were the only five cities that recorded small improvements in home prices over July. David Blitzer, chairman of the index committee at Standard & Poor’s, called the report “disappointing.” “At this time, it does not seem that any of the markets are hanging on to the temporary momentum caused by the homebuyers’ tax credits,” Blitzer said in a comment that accompanied the report.

Economists are concerned that there may be additional downward pressure on prices as demand slows in cooler months. The expiration of the tax credit combined with the cooler temperatures may create “a downside double-whammy for prices,” Josh Shapiro, chief U.S. economist at MFR Inc, wrote in a research note. On a year-over-year basis, 12 of the 20 metropolitan areas posted negative growth rates. Seventeen of the regions showed a deceleration in growth rates. Only Charlotte, Cleveland and Las Vegas saw improvement in year-over-year growth rates.The Case-Shiller index is based on repeat sales of the same properties.

One Mess That Can’t Be Papered Over

by Gretchen Morgenson

Lawyers representing delinquent homeowners have been shouting for years about documentation problems in residential mortgages. Now that their complaints have gained traction with investors, attorneys general and some state court officials, the question of consequences looms large. Is the banks’ sloppy paperwork a matter of simple technicalities that are relatively easy to cure, as the banks contend? Or are there more far-reaching consequences for banks and the institutions that bought mortgage-backed securities during the mania? Oddly enough, the answer to both questions may be yes.