"Morris Levine, 212 Park Street, Burlington, Vermont. 11 years old and sells papers every day -- been selling five years. Makes 50 cents Sundays and 30 cents other days"

Ilargi: To order Stoneleigh's video presentation "A Century of Challenges", which keeps drawing rave reviews across Europe and North America, CLICK HERE or click the button on the right hand side just below the banner.

Ilargi: Master graph-maker Doug Short requested I do a guest post for his site, dshort.com, after he saw my alterations of his work regarding the Consumer Metrics Institute data. This post appears on both sites simultaneously.

Ilargi: In anticipation of tomorrow's announcement of Q3 GDP by the BEA, here's a comparison of the BEA numbers with a series of other data.

Let’s start with a bit of "history". I first published on the Consumer Metrics Institute's CMI growth Indices in August '10, after seeing Doug Short's graphs in which he combined the CMI 91-day index with BEA's GDP numbers and the S&P 500.

While the comparison is inviting, as is obvious to anyone who sees it, it's not perfect. So I began to tinker with Doug's work. The first step was to move the CMI 91-day data forward vs GDP by roughly one quarter. Not only does this line up peaks and troughs with remarkable accuracy, it also addresses the fact that the 91-day index is a leading indicator, something that’s easy to see when you realize that it's updated daily, while this week’s Q3 GDP numbers are published a full 4 months after Q3 began. It looks like this:

I then also shifted the S&P data, something that's a bit harder to explain as both an act in itself and as a phenomenon. What I can say is that the S&P is highly volatile and follows the GDP numbers with, again, remarkable accuracy, only it does so with about a one quarter delay. Now, most of us will feel that the markets have a leading role in the economy, and they do, but it's not the only role they play. They are very much followers too, something I’m convinced we'll see confirmed when in Q4, our present point in time, economic numbers will deteriorate. The result is:

The problem of course remains the same: we won't be allowed to know what happened in the past 4 weeks until 3 months from now. At least not by the BEA. However, if we can build a sufficiently solid case for CMI data as a leading indicator for "official" GDP numbers, perhaps we won't have to wait that long. We won't be able to offer 100% certainty, since we have no crystal ball, but we might yet be able to make you give this some serious thought.

Friday's Q3 GDP numbers are not all that important. As Doug has previously noted, the “real" data won’t be known until well after the November 3 mid-term elections, when the BEA publishes its first revision. Note that the Q2 numbers only recently went through a second revision, which was down 33% from the first one, lowering GDP growth from 2.4% to 1.6%. That is, more than 5 months after the start of Q2, the BEA still needed to revise its data by a third.

Back to CMI. The 91-day growth index is not the only index they publish, and in fact I find it gets a bit too much attention compared to the others. Which are the 183-day and the 365-day index. Since I had never seen these in a graph, I contacted RIck Davis at CMI in September, and he provided one, saying that they'd never done this graph before, and that it does indeed look interesting. Here's the graph that Doug made which adds these two indices, both with the same one-quarter shift as the 91-day:

I first contacted Doug last week, and I think that was the first time he saw my versions of his own graphs. He called them "fascinating" and asked me for the post you're reading. The reason I wrote to him, as well as to Rick Davis at CMI, was a question Doug fielded from a dshort.com reader, who wondered how it was possible that the US Census Bureau reported a +7.3% y-o-y rise in retail sales in September '10, while the CMI 91-day index is tumbling.

Earlier, I had seen a Gallup report on consumer spending that showed a drop of -10.6% over that same period.

These are the kinds of things that make me itchy. All parties involved, Gallup, Census Bureau, BEA and CMI, may have different survey methods, and they may measure somewhat different areas of spending. But an 18% difference in findings is simply too much, it lacks credibility.

So who's right? At a certain point it comes down to one's own trust in the various methods. I did ask Gallup for their thoughts on the gap between their data and the government's, but they've unfortunately failed to respond to date. Which is a shame, since even with a bucketful of caveats, the Census Bureau seems to make Gallup look grossly incompetent. And not only Gallup, CMI too.

It would be interesting if Doug can, for a future post, obtain the complete Gallup and Census Bureau files, and incorporate them in a graph. For now, though, we still have to interpret the possible CMI indices. This is no easy matter. As I said, we have no crystal ball. However, we can't deny that the CMI 91-day index, when shifted, has that eery compliance with the BEA GDP numbers. Still, when we look at the 183 and 365-day graphs, we see a much smoother "motion". They take away much of the volatility that's inherent in the 91-day.

We need to recognize that this also means that the 365-day can shift us away, whether up or down, from more recent events, in that it averages out an entire year. And there lies a big clue as to why it is much smoother than the BEA GDP numbers, which measure only 91-day increments. This means that the 365-day then becomes a very solid and reliable index, potentially much more so than the GDP, even if, as I said, it can miss out on very real, more extreme moves.

The expectation among "experts" is that the initial report on Q3 GDP will come in around +2%. Remember, this can undergo strong revisions later on. If we look at the 365-day index in the graph above, we can make a preliminary "prediction" (remember, no crystal ball) for GDP going forward.

As the graph is right now, that is with the 3-month shift forward, Q3 GDP according to the CMI 365-day index comes at around +1.25%. And if I can be bold for a moment, I would say chances are that no matter what number is published tomorrow, the BEA Q3 GDP will be very close to that after all revisions have been done. Sadly, we won't know until say, Christmas. If we look at what the 365-day would appear to say about Q4, I would say we come to about -0.5% (average the graph over the 3-month window).

While it's still all too close to crystal ball territory for (my) complete comfort, I am convinced that this is a far more solid way of interpretation of the data then the "bare" comparison of BEA and the CMI 91-day index, because both, on account of their limited timeframes, are subject to high volatility.

NOTE: it is for instance entirely possible that we will decide at some point that the 365-day needs to be shifted forward a little more, which would move the fall in GDP also further into the future. But that is not the most important thing here: we're not aiming for details, but for trendlines. And the CMI 365-day index, which as of this morning stands at -2.86% (even as the 91-day shows signs of "recovery"), looks like a solid indicator for such a trendline, far too solid to ignore. Also, seeing that in the most pronounced part of the last downturn, Q4 2008, the 365-day never went below -2%, while BEA GDP scraped -7%, we may well have something worse than -2.86% ahead of us.

Lastly, I remain curious about the discrepancy found in the Gallup and CMI vs the "official" data. And I’m not ashamed to state that I, like many others, have strong doubts about just about any number the US government publishes these days, whether it's GDP or unemployment.

In the latter case, we have a "second opinion" available in U6 vs U3 data, which indicate a US unemployment rate of 17.1% instead of 9.6%. What we try to do with the CMI data is seeking to find a similar "second opinion", this time for GDP and consumer spending.

To be continued, no doubt.

Previous articles on CMI and related data:

A Paralyzed Fed Defers Decision On Monetary Policy To Primary Dealers In An Act That Can Only Be Classified As Treason

by Tyler Durden - Zero Hedge

As if there was any doubt before which way the arrow of control, and particularly causality, points in America's financial system, the following stunner just released from Bloomberg confirms it once and for all. According to Rebecca Christie and Craig Torres, the New York Fed has issued a survey to Primary Dealers, which asks for suggestions on the size of QE2 as well as the time over which it would be completed.

It also asks firms how often they anticipate the Fed will re-evaluate the program, and to estimate its ultimate size. This is nothing short of a stunning indication of three things:

- That the Fed is most likely completely paralyzed due to the escalating confrontation between the Hawks and the Doves, and that not even Bernanke believes has has sufficient clout to prevent what Time magazine has dubbed a potential opening salvo into a chain of events that could lead to civil war: in effect Bernanke will use the PD's decision as a trump card to the Hawks and say the market will plunge unless at least this much money is printed,

- That the Fed is effectively asking the Primary Dealers to act as underwriters on whatever announcement the Fed will come up with, and thus prop the market, and, most importantly,

- That the PDs will most likely demand the highest possible amount, using Goldman's $2-4 trillion as a benchmark, and not only frontrun the ultimate issuance knowing full well what the syndicate of 18 will decide in advance of what the final amount will be, but will also ramp stocks on November 3 to make the actual QE announcement seem like a surprise.

This also means that the Primary Dealers of America, which include among them such hedge funds as Goldman Sachs, such mortgage frauds as Bank of America, such insolvent foreign banks as Deutsche, RBS, UBS and RBS, and such middle-market excuses for banks as Jefferies, are now in control of US monetary, and as we explain below fiscal, policy.It also means that the Fed has absolutely no confidence in its actions, and, more importantly, no confidence in how its actions will be perceived by the market which is why it is not only telegraphing its decision to the bankers, but is having its decision be dictated by them, an act so unconstitutional it would be seen as treason in any non-Banana republic!

This is the last straw confirming that the only ones left trading the market are the Fed and the PDs, passing hot potatoes to each other, and the HFTs, churning the shit out of everything else to pretend someone is still trading.And the saddest conclusion is that this is the definitive end of US capital markets: not only is the Fed's political subordination a moot point, but the Fed, and the middle class' purchasing power via the imminent dollar destruction that is sure to follow as the PDs seek to obliterate their underwater assets by raging inflation, is now effectively confirmed to be a bitch of Lloyd Blankfein and his posse.

The official explanation for this unprecedented incursion by the banking crime syndicate in US monetary policy is as follows:

Avoiding Disruption

Treasury officials say they want to avoid any disruption to the $8.5 trillion market in U.S. government debt, the world’s most liquid, as the Fed weighs restarting large-scale asset purchases. The Treasury also doesn’t want to give any impression to investors, particularly those based overseas, that it might be coordinating with the Fed to finance the national debt.

“Treasury debt-management decisions are designed to deliver the lowest cost of borrowing over time and are entirely independent from monetary-policy decisions made by the Federal Reserve,” Mary Miller, assistant secretary for financial markets, said in an e-mail to Bloomberg News yesterday. Before joining the Treasury last year, Miller was head of global fixed- income portfolio management at T. Rowe Price Group Inc. in Baltimore.

The Treasury is scheduled to hold its quarterly meetings with bond dealers tomorrow, ahead of the department’s Nov. 3 refunding announcement.Fill in the blank: the Fed has essentially given PDs the option of $250BN, $500BN or $1 trillion in monetization over six months. It is now absolutely clear that the PDs will pick the biggest number possible... which incidentally amounts to $2 trillion per year, and is precisely what Goldman's downside case was, as we presented previously.

The New York Fed surveyed primary dealers required to bid in U.S. debt auctions. It asked dealers to estimate changes in nominal and real 10-year Treasury yields “if the purchases were announced and completed over a six-month period.” The amounts dealers can choose from are zero, $250 billion, $500 billion and $1 trillion.

Of course, since a $2 trillion purchase over 1 year means the Fed will have to monetize every single bond issued, the SOMA limit will have to be raised, another prediction we made months ago:

The Fed is unlikely to buy up the entire supply of new securities, although it may adjust its internal guidelines of how much it can hold of any given issue. The Fed limits itself to owning no more than 35 percent of any specific security it holds in its System Open Market Account, or SOMA.

“Our Treasury strategists point out it could also cause pricing distortions along the curve, if, for example, the Fed continues to target a 40 percent purchase concentration in the 6-10 year maturity bucket, as it has in its recent purchases,” analysts at JPMorgan Chase & Co., including Alex Roever, wrote in an Oct. 22 research report. The report predicts the Fed will buy about $250 billion a quarter during the easing campaign.How about $500 billion?

And, incidentally, since the "independent" Treasury will be forced to issue more debt to fill all the demand for $2 trillion over the next 12 months, as there is not enough debt in the pipeline to fill $2TN worth of demand and prevent the entire curve pancaking at zero (i.e., the 30 year yielding precisely 0.001%) it also means that the government will be forced to come up with more deficit programs, which also means that primary dealers will now also determine US fiscal policy.

Which begs the question, why is anyone pretending that the political vote on November 3 matters at all?

Below are the 18 banks that, in a completely separate vote, will henceforth rule America, regardless of what particular puppets end up in the Congress and Senate:

BNP Paribas Securities Corp.

Banc of America Securities LLC

Barclays Capital Inc.

Cantor Fitzgerald & Co.

Citigroup Global Markets Inc.

Credit Suisse Securities (USA) LLC

Daiwa Capital Markets America Inc.

Deutsche Bank Securities Inc.

Goldman, Sachs & Co.

HSBC Securities (USA) Inc.

Jefferies & Company, Inc.

J.P. Morgan Securities LLC

Mizuho Securities USA Inc.

Morgan Stanley & Co. Incorporated

Nomura Securities International, Inc.

RBC Capital Markets Corporation

RBS Securities Inc.

UBS Securities LLC.

Fed Asks Dealers to Estimate Size, Impact of Debt Purchases

by Rebecca Christie and Craig Torres - Bloomberg

The Federal Reserve asked bond dealers and investors for projections of central bank asset purchases over the next six months, along with the likely effect on yields, as it seeks to gauge the possible impact of new efforts to spur growth. The New York Fed survey, obtained by Bloomberg News, asks about expectations for the initial size of any new program of debt purchases and the time over which it would be completed. It also asks firms how often they anticipate the Fed will re- evaluate the program, and to estimate its ultimate size.

With their benchmark interest rate near zero, policy makers meet Nov. 2-3 to consider steps to boost an economy that’s growing too slowly to reduce unemployment near a 26-year high. Financial-market participants are focusing on the size, timing and maturities of likely purchases aimed at lowering long-term rates, with estimates reaching $1 trillion or more.

"If they buy too much, I think there’s a real chance that rates are going to rise because people are worried about inflation," said Stephen Stanley, chief economist at Pierpont Securities LLC in Stamford, Connecticut. "If they don’t buy much, they’re not going to have a market impact." William Dudley, president of the New York Fed and vice chairman of the Federal Open Market Committee, set expectations of about $500 billion for a new round of so-called quantitative easing, a figure he used in an Oct. 1 speech.

Investor Concern

"What the market wants to hear is that the Fed is going to buy $1 trillion" of Treasuries, said Joseph Lavorgna, chief U.S. economist at Deutsche Bank Securities Inc. in New York. "Concerns that it might be less is causing investors to worry about how deep and broad this program is going to be."

Treasuries rose for the first time in seven days today, pushing the yield on the benchmark 10-year note down two basis points, or 0.02 percentage point, to 2.698 percent as of 10:38 a.m. in London. The yield climbed to the highest in more than a month yesterday on speculation that the Fed will buy less debt than some traders had been expecting.

Europe’s Stoxx 600 Index increased 0.7 percent today and Standard & Poor’s 500 Index futures rose 0.3 percent. The New York Fed’s survey coincides with a Treasury Department questionnaire asking dealers about the outlook for bond-market liquidity. Treasury officials say any additional program of asset purchases by the Fed won’t affect borrowing plans.

Avoiding Disruption

Treasury officials say they want to avoid any disruption to the $8.5 trillion market in U.S. government debt, the world’s most liquid, as the Fed weighs restarting large-scale asset purchases. The Treasury also doesn’t want to give any impression to investors, particularly those based overseas, that it might be coordinating with the Fed to finance the national debt.

"Treasury debt-management decisions are designed to deliver the lowest cost of borrowing over time and are entirely independent from monetary-policy decisions made by the Federal Reserve," Mary Miller, assistant secretary for financial markets, said in an e-mail to Bloomberg News yesterday. Before joining the Treasury last year, Miller was head of global fixed- income portfolio management at T. Rowe Price Group Inc. in Baltimore. The Treasury is scheduled to hold its quarterly meetings with bond dealers tomorrow, ahead of the department’s Nov. 3 refunding announcement.

Treasury Yields

The New York Fed surveyed primary dealers required to bid in U.S. debt auctions. It asked dealers to estimate changes in nominal and real 10-year Treasury yields "if the purchases were announced and completed over a six-month period." The amounts dealers can choose from are zero, $250 billion, $500 billion and $1 trillion.

"Yields would have to back up" if the market is overestimating the size of Fed purchases, said Joseph Abate, money-market strategist at Barclays Capital Inc. in New York. "The dealer community is running much less leverage than they did before. The amounts of inventory they are financing is smaller. Their capacity to absorb extra supply is lower." The Treasury is watching for signs the Fed’s buying program might affect market operations. Fed purchases would take place as the Treasury reduces debt issuance, raising questions of whether the government would have to sell additional securities to avoid market disruptions.

‘Nuclear Option’

"That’s certainly kind of a nuclear option for Treasury," Stanley said. "They would always and everywhere like to avoid that." Extra debt sales have happened just twice in the past decade, with so-called snap reopenings of existing securities in the aftermath of the Sept. 11, 2001, terrorist attacks and at the height of the financial crisis, in October 2008. The Treasury acted to shore up market liquidity and prevent a trading freeze caused by shortages of highly sought securities.

The Treasury has put a premium on selling its debt in a regular and predictable fashion. Those efforts may be tested by the Fed’s purchase campaign, which would take place in the secondary market rather than at Treasury auctions. The Fed’s purchases might run as high as $100 billion a month, some analysts say -- almost equaling the entire amount the government is likely to sell.

‘Tugging’ the Wheel

"If the Fed commits itself to buying back the bulk of the Treasury’s net new issuance through open-market purchases, it will have more than one hand tugging on the wheel of federal debt management policy," said Lou Crandall, chief economist at Wrightson ICAP LLC in Jersey City, New Jersey. Crandall said the frequency of note auctions, combined with low interest rates, "sharply increases the likelihood of accidental reopenings in the next phase of the rate cycle."

The Fed is unlikely to buy up the entire supply of new securities, although it may adjust its internal guidelines of how much it can hold of any given issue. The Fed limits itself to owning no more than 35 percent of any specific security it holds in its System Open Market Account, or SOMA. "Our Treasury strategists point out it could also cause pricing distortions along the curve, if, for example, the Fed continues to target a 40 percent purchase concentration in the 6-10 year maturity bucket, as it has in its recent purchases," analysts at JPMorgan Chase & Co., including Alex Roever, wrote in an Oct. 22 research report. The report predicts the Fed will buy about $250 billion a quarter during the easing campaign.

The central bank makes the securities in its portfolio available to dealers through its daily securities lending operation, making it unlikely that Fed purchases alone would lead to an acute shortage of a given issue. For now, the Treasury is doing everything it can to show borrowing independence. The department is extending the average maturity of its debt and ramping up sales of 10-year and 30-year securities while cutting issuance of the medium-term securities the Fed is more likely to buy.

Fed Gears Up for 'Gradual' Stimulus,

by Jon Hilsenrath and Jonathan Cheng - Wall Street Journal

The Federal Reserve is close to embarking on another round of monetary stimulus next week, against the backdrop of a weak economy and low inflation—and despite doubts about the wisdom and efficacy of the policy among economists and some of the Fed's own decision makers. The central bank is likely to unveil a program of U.S. Treasury bond purchases worth a few hundred billion dollars over several months, a measured approach in contrast to purchases of nearly $2 trillion it unveiled during the financial crisis. The announcement is expected to be made at the conclusion of a two-day meeting of its policy-making committee next Wednesday.

The Fed's aim is to drive up the prices of long-term bonds, which in turn would push down long-term interest rates. It hopes that would spur more investment and spending and liven up the recovery. But officials want to avoid the "shock and awe" style used during the crisis in favor of an approach that allows them to adjust their policy, and possibly add to their purchases, over time as the recovery unfolds. Fed Chairman Ben Bernanke's push to restart the bond-buying program—a form of monetary stimulus known as quantitative easing—has been greeted with deep skepticism among some of his colleagues.

In some of his strongest words yet, Thomas Hoenig, president of the Federal Reserve Bank of Kansas City, said Monday that more expansive monetary policy was a "bargain with the devil." In the next few months, internal opposition to Mr. Bernanke's approach could intensify as presidents of three regional Fed banks who have expressed skepticism about the plan—Narayana Kocherlakota of Minneapolis, Richard Fisher of Dallas and Charles Plosser of Philadelphia—take voting positions on the Fed's policy-making body. There are 12 regional Fed banks, and five voting seats on the Federal Open Market Committee rotate among them every year, with New York always keeping one.

Investors already expect Fed action. Stock prices have rallied since Mr. Bernanke broached the idea of bond buying in late August. But investors and analysts are divided on whether the gambit will work. In normal times, the Fed reduces short-term interest rates when it wants to spur growth. But the central bank already cut short-term rates to near zero in 2008, so it is turning to an unconventional measure.

Some Fed officials argue the economy is going through long-term changes that the central bank can't rush, and worry a large bond-buying program might only stoke future inflation or a new asset bubble. But the view likely to prevail at the Nov. 2-3 meeting is that the economy is falling short on two fronts: Unemployment, at 9.6%, means the Fed is falling short of its legal mandate to maximize employment. Inflation, which is running a bit above 1% so far this year, is below the Fed's informal objective of about 2%, and runs the risk of falling even lower. With so much unused capacity and spare labor, many officials contend, the Fed is unlikely to stoke a worrisome amount of inflation.

Though details remain to be being sorted out internally, the broad outlines have taken shape. Unlike in March 2009, when the Fed laid out a program to buy $1.75 trillion worth of Treasury and mortgage bonds over six to nine months, officials this time want flexibility as they assess if the program is working. Mr. Bernanke has used the analogy of a golfer with a new putter: Unsure how it will work, he finds best strategy is to tap lightly at first and keep tapping until the golfer figures out how best to use the putter.

The Fed could leave open the possibility of more purchases in the future, particularly if inflation is projected to remain below 2% and the unemployment outlook remains high, which is currently the expectation of many officials. Or it could halt the program if the economy or inflation surprisingly take off, officials have said. Fed officials will update their forecasts for growth, unemployment and inflation through 2013 at the upcoming meeting.

Some investors are on edge about how the Fed will proceed. On the one hand, the Dow Jones Industrial Average has risen 12% since Mr. Bernanke began hinting about buying more bonds two months ago, a welcome rise inside the Fed. But commodities prices are also soaring, with copper, gold and oil prices rising 16%, 8.1% and 13% respectively. That could portend more inflation than the Fed wants. At the same time, the dollar has slid nearly 10% against the euro; that could help U.S. exports, but it creates tensions with trading partners. A sharp drop in the dollar could give Fed officials pause.

The main aim of a bond buying program would be to drive down long-term interest rates by pushing up the price of Treasury bonds and thus driving down their yields. From nearly 4% in April, the yield on the 10-year Treasury note has already tumbled to about 2.6%, in part because investors expect the Fed to be in the market buying bonds. Mortgage rates, closely tied to the 10-year note yield, have fallen to their lowest levels in more than four decades.

Some investors say the Fed doesn't have much margin for error next week. Too modest a move could disappoint those who say the economy needs aggressive Fed action, but an overly muscular approach could prompt concerns the Fed is overreacting. "There is room on either side for a negative surprise," said Mike Ryan, chief investment officer for UBS Wealth Management Americas.

A Wall Street Journal survey of private sector economists in early October found that the Fed is expected to purchase about $250 billion of Treasury bonds per quarter and continue until mid-2011, amounting to about $750 billion in all. New York Fed president William Dudley put forward one key benchmark in a speech earlier this month. He noted that $500 billion worth of purchases had the same impact on the economy as a reduction of the federal funds rate by one-half to three-quarters of a percentage point.

In speeches this week, Mr. Dudley repeated he found the economy's weak state "unacceptable" and said "further Fed action was likely to be warranted." The bond-buying program is likely to focus on Treasury bonds with maturities mostly between 2-years and 10-years, according to interviews with some officials. The Fed could buy even longer-term bonds, though some officials are reluctant to do that aggressively because it could expose them to long-term losses without much added benefit.

‘Savage’ Austerity Is in U.S.’s Future, Buiter Says

by Daniel Kruger and Tom Keene - Bloomberg

Fiscal austerity measures detailed [last week] by the U.K. government will soon be needed in the U.S., according to Willem Buiter, Citigroup Inc.’s chief economist. Britain’s deepest budget cuts ever, outlined by Chancellor of the Exchequer George Osborne, will eliminate almost 500,000 public-sector jobs and impose a levy on banks. The moves are part of a plan to reduce the 156 billion-pound ($245 billion) deficit, which is forecast to be 10.1 percent of gross domestic product this year, to 2.1 percent in the 2014-15 fiscal year.

"The only question was really the timing and the composition," given the finite willingness of financial markets to endure budget shortfalls, New York-based Buiter said in a roundtable interview on "Bloomberg Surveillance Midday" with Tom Keene. "This is very savage, but no more savage than what the U.S. will have to endure when it gets going."

Stimulus spending to revive the economy and the lingering effects of the recession on tax revenue pushed the U.S. budget deficit for fiscal year 2010 to $1.29 trillion, the second- largest on record, the Treasury Department reported on Oct. 15. The gap was surpassed only by last year’s $1.42 trillion shortfall. The U.S. will still be able to borrow for a while at "risk-free rates" because its markets remain bolstered by the dollar’s role as the world’s reserve currency, Buiter said. "It won’t last forever, that buffer of protection," Buiter said. "Market discipline is being eroded by the burden of unsustainable deficits."

‘Overhang’ on Economy

Governments now face the question of when to begin addressing budget imbalances, said Howard Davies, chairman of the London School of Economics, in the interview. "Our government has made a big throw of the dice today and said we’ve got to get on with it because the existence of this large deficit is an overhang on the economy preventing people from regaining confidence and investing," Davies said. "They know that at some point they’re going to have to pay increased taxes or public spending’s going to be cut."

The cuts are the right thing to do, Davies said. It’s an open question whether Osborne has focused "too much on spending and not enough on taxing," Davies said. "I hope he’s willing to be a bit flexible."

Fiscal disaster set to explode

by Justin Rohrlich - MarketWatch

American states face a perpetual Sophie’s Choice of sorts. When times are good, and you own a business, the last thing you want to do is give up more of your profit. When times are bad, the last thing you want to do is give up more of your diminished receipts.

But many U.S. states are now in a vicious cycle that will be exploding in December. As businesses lay off workers, fewer payroll tax dollars go into each state’s unemployment insurance trust fund. Simultaneously, as businesses lay off workers, more dollars are coming out of those states’ trust funds to pay unemployment benefits.

Since March of 2009, 31 states have borrowed billions from the federal government to continue paying out unemployment benefits while keeping their UI trust funds from insolvency. The federal stimulus provided for a moratorium on interest payments until Dec. 2010. And, as you likely know, that’s a month from now.

Take a look at California. The Golden State is on the hook for $11 billion in unemployment benefits this year but only taking in $4.6 billion. According to the Pew Center for the States, California would have to at least double its business tax to make up for the lost $6 billion.

Pew quotes Rick McHugh of the National Employment Law Project, who says it’s "important to pay attention to the… states in good shape. Washington State hasn’t had to borrow from the federal unemployment fund since the 1980s and — if things continue looking the way they are — it won’t have to anytime soon. Over the past decade, the state’s legislature and business community agreed to a set of taxes that kept the unemployment trust fund well funded throughout the current recession."

Companies headquartered in Washington like Starbucks Corp., Amazon.com Inc., and Costco Wholesale Corp., pay comparatively higher payroll taxes than do Texas-based companies like Dell Inc. and Whole Foods Market Inc.. But, while nowhere close to Michigan’s $382.57 per capita borrowing, now Texas’s unemployment insurance borrowing stands at $1.4 billion, which works out to $57.19 per person, still quite a bit higher than Arizona’s $6.50. It’s important to note that Texas also created half of all new net jobs in the country last year.

Even though state trust funds have now borrowed more, adjusted for inflation, than they did during 1981 and 1982, independent trader Jeff Macke doesn’t believe state governments’ UI trust funds will be driven to insolvency in December.

"It helps to think of this as you would a parent loaning his kids money," he told Minyanville. "Dad may really want to get paid back. He may impose all sorts of penalties on his non-paying children. But it would be stupid for Dad to drive his deadbeat children into destitution for missing a payment. Ruining the kid results in dad never getting paid back and likely incurring further expense when Junior inevitably gets into real trouble."

Zombie America vs. China’s Zombie-Eaters 2020

by Paul B. Farrell - MarketWatch

"Zombie Economics: How Dead Ideas Still Walk Among Us," could easily have been entitled "Zombie Capitalism." Why? The book is all about undead Reaganomics zombie-isms like "trickle-down" that nearly destroyed the American economy in 2008.

Now that same Zombie Capitalism is being resurrected by the Goldman Conspiracy of Wall Street Banksters and their new partner, the GOP Tea Party of No-No. Yes, folks, America’s self-destructive Zombie Capitalism has once again returned from the mausoleum of toxic undead ideas.

But this was so predictable. As Naomi Klein, author of "Shock Doctrine: The Rise of Disaster Capitalism," warned: "Free-market ideology will come roaring back when the bailouts are done, and the massive debts the public is accumulating to bail out the speculators will then become part of a global budget crisis."

Get it? The Zombie Capitalism of Reaganomics couldn’t kill us during the dot-com crash or subprime credit collapse, but now Zombie Wall Street is shooting for the "Third Meltdown of the 21st Century."

Wait, an even better title would be, "Zombie America." Why? America is not only enjoying Halloween, the great celebration of the undead, but in our election madness we also created a historic trick-or-treat, with invisible monster billionaire backers, ghoulish politicians and blood-sucking vampires emerging from graves in foreign sovereign nations to poison our souls from within.

But the scariest monsters this Halloween are the China Zombie Eaters who are devouring the dying jobs of Zombie Americans. China’s Zombie Eaters are infinitely more dangerous than all the spooky foreign nations funneling megabucks into the Chamber of Commerce’s Supreme Court-sanctioned lobby.

Here are 8 demonic reasons why China’s aggressive "economic warfare" is also a secret long-term defensive military strategy:

1. Zombie-eating China has a long-range plan to conquer America

Listen closely, because the nuttiest theories are so often revealed later as hidden truths. Remember Delaware Tea Party Senate candidate "I’m no witch" Christine O’Donnell. You may question her credibility about secret classified documents revealing that China has a "carefully thought out and strategic plan to take over America."

But still, the facts are that the China Zombie Eaters are destroying and devouring millions of American jobs.

We also know China is stealing U.S. state secrets, stealing proprietary patents, stealing our technology. We know China is hacking away, aggressively engaged in a not-so-secret cyber war against America. We also know China has forged alliances with America’s enemies, including Iran, Venezuela and North Korea.

So while you’ll chuckle at a non-witch’s "classified" plans, the fact is China Zombie Eaters are our worst nightmare, aggressively engaged in wars against America on multiple fronts.

As Ross Terrill, a China expert at Harvard, put it in the Wilson Quarterly: "The Chinese Communists are very aware of this contest with the United States, though Americans (beyond the Pentagon) are not."

Yes, Zombie America is clueless about the threat. And, Terrill warns, our lack of awareness will destroy us: "By being a shrinking violet, the United States would simply hand over the future to China."

2. Zombie-eating China ‘buys’ Australia with surplus U.S. dollars

Want more proof? Read Malcolm Knox’s recent piece in Bloomberg-BusinessWeek: "The Deal is Simple. Australia Gets Money. China Gets Australia." Wake up Americans. While our Zombie Politicians are fighting selfish turf wars this election cycle, China is using its foreign currency reserves (U.S. dollars) to buy rights to Australia’s commodities and natural resources, giving China Zombie Eaters long-term access to natural gas, minerals, iron ore and more.

A lot of those resources are found in Queensland, Australia, the home of John Quiggin, the economics professor who wrote the book "Zombie Economics." Quiggin also summarizes the five main undead ideas of "Zombie Capitalism" in Foreign Policy magazine.

3. China Zombie Eaters easily bully Japan into submission

In a recent New York Times column Nobel Economist Paul Krugman warned: "Last month a Chinese trawler operating in Japanese-controlled waters collided with two vessels of Japan’s Coast Guard. Japan detained the trawler’s captain; China responded by cutting off Japan’s access to crucial raw materials."

Bad news: Like a wounded tiger, China’s Zombie Eaters will turn against anyone. China controls 97% of "the world’s supply of rare earths, minerals that play an essential role in many high-technology products, including military equipment. Sure enough, Japan soon let the captain go."

4. China Zombie Eaters are aware of Pentagon war strategies

That trawler incident got me thinking of the Pentagon study from Fortune back during the Bush/Cheney years: "By 2020 there is little doubt something drastic is happening." The Pentagon warned that "as the planet’s carrying capacity shrinks, an ancient pattern of desperate, all-out wars over food, water, and energy supplies would emerge ... warfare is defining human life." You can bet China’s generals have the same strategic playbook.

Krugman fears the Zombie Eaters long-range plans: "I don’t know about you, but I find this story deeply disturbing, both for what it says about China and what it says about us. On one side, the affair highlights the fecklessness of U.S. policy makers, who did nothing while an unreliable regime acquired a stranglehold on key materials. On the other side, the incident shows a Chinese government that is dangerously trigger-happy, willing to wage economic warfare on the slightest provocation." Maybe even military action?

5. Zombie-eating China way ahead of Pentagon’s war planners

Krugman calls this "economic warfare." But the Marine Corps veteran in me sees a long-range strategy of out-flanking a complacent Zombie America.

It’s well-known the China Zombie Eaters are making deals all over the world — in Africa, South America, Russia and Asia — tying up long-term natural resources, using their surplus credits of U.S. dollar reserves to lock up essential global commodity futures. Meanwhile America’s Zombie Politicians waste time in myopic election turf wars for personal gain, failing to see that America’s consumers and taxpayers are financing China’s war plans. Wake up. Admit it.

So to echo Krugman: I don’t know about you, but on so many fronts China’s behavior smells like their leaders are doing lots more than expanding China’s economy (the Foreign Policy Journal predicts China will explode from 11% to 40% of the global GDP by 2040, creating a $123 trillion economy that will dwarf America’s GDP).

But even more deeply disturbing, China’s behavior tells us they are obviously engaged in long-term defensive military strategies as well as economic planning, and that in the future, another trawler incident may well provoke dangerously trigger-happy Chinese leaders into escalating from defensive military strategies to a preemptive strike protecting China’s economic power.

6. Zombie-eating China aided by the Goldman Conspiracy vampires

The Wall Street Journal reports that Goldman Sachs CEO Lloyd Blankfein (obviously supported by the ghost of former CEO Hank Paulson who left the American Treasury buried in a graveyard of trillions of debt) "is trying to rehabilitate its public reputation with an ad campaign." Yes, that undead Wall Street zombie will try "to show how it helps create jobs, is planning to make changes in the way it reports its finances and how it relates to clients, investors and analysts."

Warning: Goldman’s no passive zombie. They’ll always be the textbook bloodsucking Wall Street vampire for all future Halloweens, what Rolling Stone’s Matt Taibbi called a "giant vampire squid wrapped around the face of humanity, relentlessly jamming its blood funnel into anything that smells like money."

That image forever defines Goldman as an enemy of America, especially now for using its conspiracy of anti-capitalists to aid and abet China Zombie Eaters in their economic war to bury America for all eternity.

7. Zombie AARP retirees vs. American under-40 taxpayers

Unfortunately the coming domestic class war will further drain America’s global power. Soon America will resemble France. Total chaos today. President Sarkozy’s under siege for raising the retirement age from 60 to 62.

French bankers are still getting rich, like Wall Street. But they control government, budget cuts, austerity. Result? Class wars: Students stormed the French Senate. Trade unions blocked airports. Oil refineries forced closure of 3,000 French gas stations. Cost: $100 million a day.

French voters are not zombies, they’re role models. Soon Zombie Americans will revolt, arising as the undead. France has 62 million, America’s five times bigger. Imagine an American class war when Zombie AARP’s 40 million members react after our Zombie Congress raises the Social Security retirement age (or cuts benefits, or raises taxes).

Bet on a nationwide revolution of young voters, unions, unemployed and poor, as in France.

8. Warning: Zombies can’t vote … but zombies will revolt!

Remember "The Night of the Living Dead?" Their time is on the horizon. In the full moon, cemeteries will empty of the undead. Revolting, they will fulfill their destiny. They will take back America from the eternally greedy Zombie Bankers and feckless Zombie Politicians.

Happy Halloween all you zombies, ghouls, vampires, witches and devilish monsters sucking the blood out of America’s soul … your time is coming soon, the end of your evil ways, when a new "night of the living dead" revives our great nation.

Pimco likens US to 'Ponzi' scheme

by Philip Aldrick - Telegraph

US authorities are operating a "brazen" Ponzi scheme in government debt by buying trillions of dollars of bonds to stimulate the economy, according to Bill Gross, managing director of Pimco, the world's biggest bond house.

In a bid to restart the stalling recovery, the US Federal Reserve is next week expected to unveil a second round of quantitative easing (QE) of as much as $500bn, on top of the $1.2 trillion already completed. In typically robust comments, Mr Gross said the Fed had run out of other options but warned that more QE would in the long-term mean "picking the creditor's pocket via inflation and negative real interest rates".

"[Cheque] writing in the trillions is not a bondholder's friend; it is in fact inflationary, and, if truth be told, somewhat of a Ponzi scheme," he wrote on his investment outlook, arguing that creditors have always expected to be paid out of future growth. "Now, with growth in doubt, it seems the Fed has taken Ponzi one step further," he said. "The Fed has joined the party itself. Has there ever been a Ponzi scheme so brazen? There has not."

More QE is a huge gamble, he said, but necessary because the US is "in a 'liquidity trap', where interest rates or QE may not stimulate borrowing or lending because consumer demand is just not there." Mr Gross is best-known in the UK for saying gilts were "resting on a bed of nitroglycerine" as a result of the nation's high debt levels. Pimco has since reversed its position on the UK and advised clients to gamble on a British recovery.

Current Contraction Surpasses "Great Recession"

by Rick Davis - Consumer Metrics Institute

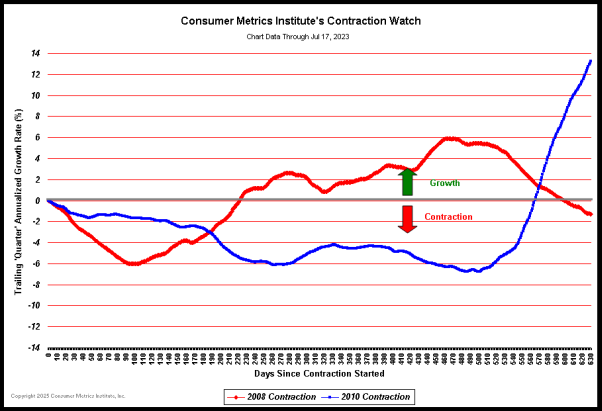

On October 20, 2010 the aggregate severity of the 2010 contraction in consumer demand surpassed the similar measure of economic pain experienced during the "Great Recession." And a glance at our "Contraction Watch" tells us that the pain is not about to end anytime soon:

(Click on chart for fuller resolution)

In the above chart, the day-by-day courses of the 2008 and 2010 contractions are plotted in a superimposed manner, with the plots aligned on the left margin at the first day during each event that our Daily Growth Index went negative. The plots then progress day-by-day to the right, tracing out the changes in the daily rate of contraction in consumer demand for the two events.

The true severity of any contraction event is the area between the "zero" axis in the above chart and the line being traced out by the daily contraction values. By that measure the "Great Recession of 2008" had a total of 793 percentage-days of contraction over the course of 221 days, whereas the current 2010 contraction has reached 820 percentage-days over the course of 282 days -- without yet clearly forming a bottom. The damage to the economy is already 3% worse than in 2008, and the 2010 contraction has lasted 28% longer than the entire 2008 event without yet starting to recover.

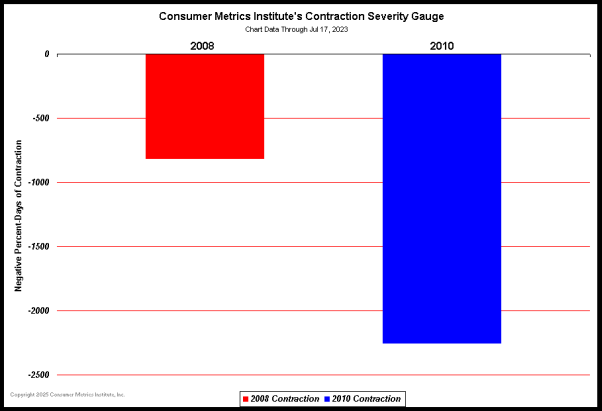

We have constructed a new chart to assist in the visualization of the "percentage-days" severity of the two contraction events:

(Click on chart for fuller resolution)

In the above chart the red vertical bar represents the -793 percentage-days of contraction in consumer demand that we measured in 2008. The blue vertical bar represents the same measure (to date) for the 2010 event. But since the 2010 event is not yet over, we have projected the eventual full extent of the 2010 event with the purple vertical bar. That projection is an average of several recovery scenarios, all of which conservatively assume that the bottom has already been reached.

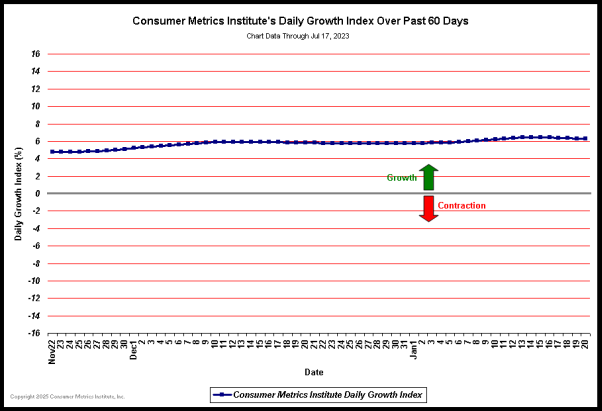

Meanwhile, we are left to wonder if a bottom as been forming in the current contraction. A detailed view of our Daily Growth Index over the past 60 days could be viewed as either encouraging or simply "more of the same," depending on your state of mind:

(Click on chart for fuller resolution)

It is important to remember that our Daily Growth Index is a moving 91-day "trailing quarter" average for our Weighted Composite Index (converted from a nominal base-100 index into a year-over-year percentage change). As such it responds to the values of both the newest day's Weighted Composite Index (just entering the 91-day average for the first time) and the 92nd day back -- which has just fallen out of the average. The current values of the Weighted Composite Index are in the -5% to -7% range, whereas the oldest days falling out of the average reflect a weaker period in late July when the Weighted Composite Index was in the -6% to -9% range. Even if current consumer demand remains relatively constant we should expect the trailing 91-day "trailing quarter" to improve slightly from recent record lows over the next 30 days. But we are unlikely to see significant improvements until the current values of the Weighted Composite Index move substantially above the zone between 94 and 96 -- which we consider unlikely until after the mid-term elections (see our comments on the impact of Political "FUD" for why we consider that unlikely).

From time to time we have been asked whether we consider the current contraction in consumer demand to be the second "dip" in a "double dip" recession. From a qualitative perspective, we believe that the "Great Recession" is not so much a "double-dip" as a single "big-scoop" that changed character somewhere in the middle. We understand that the NBER says that the recession ended in June 2009. However quantitatively/technically correct that may be by NBER standards, by "Main Street" gut-feeling standards the NBER assertion is somewhere between questionable and ludicrous, depending on the personal circumstances of the observer.

Our data indicates that the consumer portion of the "Great Recession" unfolded (and is still unfolding) along these lines:

► The recession most likely started with a drop in consumer confidence, triggered by bad financial news (Bear Stearns, Lehman Brothers, etc.) and media coverage of the "Housing Crisis"/sub-prime loans.

► The initial recessionary downturn was accelerated by political uncertainties in 2008 and rising energy prices.

► An organic recovery started late in 2008 when energy prices collapsed, lasting well into 2009 with help from short term stimuli ("Cash for Clunkers" and the Federal New Home Tax Credit).

► During 2009 (and now deeply into 2010) a ruthless corporate obsession with short term earnings exacerbated the already weak employment picture, even as equity markets recovered.

► By late summer 2009 consumers realized that this was not a "garden variety" recession, as unemployment persisted and fixed incomes plummeted.

► By early 2010 demographically appropriate "frugal" consumer habits had emerged, reducing discretionary spending in favor of increased personal savings (or the paying down of debt).

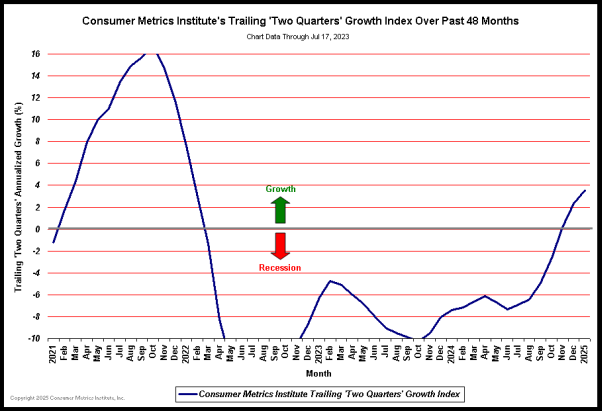

The two reversals described above can be clearly seen in a chart of our trailing 183-day "two consecutive quarters" index -- which is designed to closely follow the "two consecutive quarters" definition of a recession -- for the past 48 months:

(Click on chart for fuller resolution)

Credit the growth spurt in the middle of the above chart to a combination of dropping energy prices, consumer shopping reverting to form after a brief hiatus, positive psyches as a result of a honeymoon with the new administration, and the consumer oriented parts of the stimulus packages. All that changed when consumers realized (in late 2009) that things were not actually getting any better.

But missing from the above narrative is the potential permanence of the damage inflicted on certain consumers. Those consumers living through foreclosures will have suffered lifestyle and financial reversals that may require a decade or longer to rehabilitate. And even those fortunate enough to stay current with their mortgages may have had their dreams of upward mobility (or mobility of any sort) crushed. In both of these cases the damage will have caused changes in habits (the "new frugality") that could last decades, if not the rest of their lives. The "Great Depression" of the 1930's changed an entire generation's attitudes about banks and spending permanently. While this economic strife may not be as severe, the emotional scars may persist longer than policy makers might wish.

Also absent from the above narrative is the impact of the Federal Reserve's extended "zero rate" policy on those attempting to live on a lifetime's modest accumulation of wealth. On Wall Street and inside the Beltway there are no perceived victims of low interest rates, because low rates result in obscene spreads between the real cost of institutional borrowing (essentially zero) and the real rate of consumer lending (18% to 24% on real-world short term loans). Meanwhile every barrier possible has been raised to prevent those lower rates from propagating to those most in need of longer term relief.

Lost on the policy makers is the fact that what's good for banks is not necessarily good for their depositors. Simply stated, it has become impossible to live on the earnings generated by a lifetime of middle class savings. In June 2007 an accumulation of $2,000,000 in an IRA or 401K would translate into $100,000 in annual income when invested in 1 year T-Bills, an annual income higher than the per capita income in any of the richest nations on earth. That was certainly a reasonable target for a middle class household, and one that would allow a comfortable retirement without significant changes in lifestyle.

Today the same $2,000,000 (if it was somehow preserved throughout the "Great Recession") would earn $4,200 per annum if invested similarly -- or roughly the per capita income in the Republic of the Congo. No wonder that many "Baby Boomers" are increasing savings and postponing retirement to the chagrin of younger people desperately looking for jobs; the alternative is a third-world lifestyle.

Wall Street Proprietary Trading Goes Under Cover

by Michael Lewis - Bloomberg

A few weeks ago we asked a simple question: Why are the same Wall Street banks that lobbied so hard to dilute the passages in the Dodd-Frank financial overhaul bill banning proprietary trading now jettisoning their proprietary trading groups, without so much as a whimper? The law directs regulators to study the prop trading ban for another 15 months before deciding how to enforce it: why is Wall Street caving now?

The many answers offered by Wall Street insiders in response boil down to a simple sentence: The banks have no intention of ceasing their prop trading. They are merely disguising the activity, by giving it some other name. A former employee of JPMorgan, for instance, wrote to say that the unit he recently worked for, called the Chief Investment Office, advertised itself largely as a hedging operation but was in fact making massive bets with JPMorgan’s capital. And it would of course continue to do so.

The fullest explanation came from a former Lehman Brothers corporate bond salesman named Robert Wosnitzer, who is now at New York University, writing a dissertation on the history of proprietary trading. He’s been interviewing Wall Street bond traders, he said, and they have been surprisingly open about their intentions to exploit one obvious loophole in the new law.

The innocent eye might have trouble spotting this loophole. The Dodd-Frank bill bans proprietary trading (Page 245: "Unless otherwise provided in this section, a banking entity shall not engage in proprietary trading") and then appears to make it clear what that means (Page 565: "The term ‘proprietary trading’ means the act of a (big Wall Street bank) investing as a principal in securities, commodities, derivatives, hedge funds, private equity firms, or such other financial products or entities as the comptroller general may determine").

Invitation for Abuse

The big invitation for abuse, Wosnitzer says, lies in the phrase "as a principal." It falls to the comptroller general - - or, more specifically, the General Accountability Office, which is overseen by the comptroller general -- to determine precisely what the phrase means. And, at the moment, the GAO pretty clearly hasn’t the first clue. ("We’re really too early in the process to speak to how we might define it," said spokeswoman Orice Williams Brown.) Never mind: Wall Street is busily defining the term for itself.

Make an Argument

"One trader I interviewed," Wosnitzer says, "said that from here on out, if he wants to take a proprietary position in a credit, he will argue that he bought the position because a customer wanted to sell the position, and he was providing liquidity; and in order to keep the trade on, he would merely offer the bonds 10 basis points higher than the offered side, so that he will in effect never get lifted out of the position, while being able to say that he is offering the bonds for sale to clients, but no one wants ‘em. When the trade finally gets to where he wants it -- i.e., either realizing full profit, or slaughtered by losses -- he will then sell it on the bid side, and move on.

Of course, there is all sorts of flawed logic here, but the point is that...there are a hundred different ways to claim to be acting as an agent or for a customer.’’ This ambiguity is no doubt one reason the financial reform bill passed in the first place. Even its clearest prohibitions are couched in language inviting Wall Street to evade them. But the new game of cat and mouse raises a simple, even naive question: Why do these giant Wall Street firms want so badly to make huge bets with their shareholders’ capital?

Save Us

After all, the point of the ban on proprietary trading is as much to save the banks from themselves as to save us from them. We have just come through a period where putatively shrewd individual bond traders lost not millions but billions of dollars for their firms, by making really stupid bets. Even before the crisis there was never any reason to think that traders at big Wall Street firms had any special ability to gamble in the financial markets. Anyone with a talent for investing is unlikely to waste it on Morgan Stanley or Bank of America; he’ll use it for himself, or for some hedge fund, which allows him to keep more of his returns.

And if this were true before the financial crisis it is even more true after it, when trading inside a big Wall Street bank will be less pleasant and more fraught with politics. Yet Wall Street’s biggest firms apparently still badly want their traders to be allowed to roll the bones. Why?

What They Do

One answer -- which Wosnitzer points to -- is that this is what Wall Street firms now mainly do. Beginning in the mid- 1980s, the Wall Street investment bank, seeing less and less profit in the mere servicing of customers, ceased to organize itself around its customers’ needs, and began to build itself around its own big and often abstruse gambles.

The outsized gains (and losses), the huge individual paychecks, the growing ability of traders to bounce from firm to firm from one year to the next, the tolerance for complexity that doubles as opacity: all of the signature traits of modern Wall Street follows from the willingness of the big firms to allow small groups of traders to make giant bets with shareholders’ capital, which the shareholders themselves don’t and can’t understand.

The new way of life began at Salomon Brothers in the early 1980s, right after it turned itself from a partnership into a publicly traded corporation; but it soon spread to the others. ‘‘That was the particular moment when a new culture of finance crystallizes," Wosnitzer says. "And it restructures all of finance. All of a sudden it’s ‘I made X, pay me X minus Y or, screw you, I’m leaving.’"

Keep It Simple

There’s a simple, straightforward way for the GAO to construe the Dodd-Frank language, and it would reform Wall Street in a single stroke: to ban any sort of position-taking at the giant publicly owned banks. To say, simply: You are no longer allowed to make bets in the same stocks and bonds that you are selling to investors.

If that means that Goldman Sachs is no longer allowed to make markets in corporate bonds, so be it. You can be Charles Schwab, and advise investors; or you can be Citadel, and run trading positions. But if you are Citadel you will be privately owned. And if you blow up your firm, you will blow up yourself in the bargain.

Insider Selling Volume at Highest Level Ever Tracked: 3,177 to 1

by John Melloy - CNBC

The overwhelming volume of sell transactions relative to buy transactions by company insiders over the last six months in key leading sectors of the market is the worst Alan Newman, editor of the Crosscurrents newsletter, has ever seen since he began tracking the data. The strategist looked at insider trading activity amongst the top ten companies that make up the Nasdaq such as Apple, Google and Amazon.

Then he analyzed the biggest members of the Retail HOLDRs ETF like Gap, Target and Costco, as well as the top insiders in the semiconductor industry at companies such as Altera, Broadcom and Sandisk. The largest companies in three of the most important leading sectors of the market have seen their executives classified as insiders sell more than 120 million shares of stock over the last six months. Top executives at these very same companies bought just 38,000 shares over that same time period, making for an eye-popping sell to buy ratio of 3,177 to one.

The grand total for the three sectors are "as awful as we have ever seen since we began doing this exercise years ago," said Newman, who was ahead on such trends as the dangers of high-frequency trading and ETFs before the ‘Flash Crash’. "Clearly, insiders are seeing great value only in cash. Their actions speak volumes for the veracity for the current rally."

But the overall market doesn’t seem to care. The S&P 500 is up 16 percent since its 2010 low hit on July 2nd on the back of strong earnings driven by cost-cutting and the hopes for even more quantitative easing from the Federal Reserve. The insider data "is good reason for considerable caution once the price action fades," said Simon Baker, CEO of Baker Asset Management. Still "insiders normally buy early and sell early too. Longer term -- 12 months out -- it is more of a red flag."

Newman isn’t alone in warning about insider selling. The latest report from Vickers Weekly Insider, a publication that makes investments based upon these transactions, shows that total insider sell transactions relative to purchases on the New York Stock Exchange are running at a ratio of more than four to one over the last eight weeks. The normal reading, because of options selling and other factors, is about 2 sales for every buy, according to Vickers.

To be sure, many investors feel the heavy insider selling is just an anomaly based on other reasons. "These are folks that have had to dip into their stocks for the first time in years, as their salaries have been cut and their bonuses, outside Wall Street, have been significantly curtailed," said J.J. Kinahan, chief derivatives strategist for TD Ameritrade. " This may speak more to a cash flow problem, then a market belief."

Still Newman, who is also a favorite commentator of Barron’s columnist Alan Abelson, sees the insider selling as just the latest reason, along with the mortgage foreclosure mess and fully invested mutual fund managers with no fresh powder to put to work, to be cautious on the market. "At the risk of sounding like a broken record, we expect a significant correction," said the newsletter editor.

U.S. Seeks to Shield Goldman Secrets

by Scott Patterson - Wall Street Journal

Goldman Sachs Group Inc. has always closely guarded the secrets of its lucrative high-speed trading system. Now the securities firm is getting a help from an unusual source: federal prosecutors. Federal prosecutors in Manhattan this week asked a federal district judge to seal the courtroom at the forthcoming trial of a former Goldman computer programmer accused of stealing the firm's computer code. The move was a formal request to empty the courtroom of the general public when details of Goldman's trade secrets are being discussed. The trial is set to start to late November.

Prosecutors also asked that any documents related to Goldman's trading strategies remain under seal. Such requests are common when proprietary corporate information could be exposed in a trial, lawyers say. This case is unusual in that it involves secrets about a potentially lucrative trading system, rather than, say, ingredients in a soda formula. Sergey Aleynikov, 40 years old, was arrested by Federal Bureau of Investigation agents in Newark Liberty International Airport on July 3, 2009, and charged with the theft of computer code behind Goldman's high-frequency trading platform. The programmer was indicted in February and has pleaded not guilty.

Motions filed this week by the government and the defense offer a window into arguments that will decide Mr. Aleynikov's fate. Prosecutors are expected to argue that his actions could have harmed Goldman Sachs. A spokesman for the bank declined to comment. Lawyers for Mr. Aleynikov, whom the indictment alleges uploaded Goldman code to a server in Germany and then downloaded it to his home computers, are expected to contend that the code he took only represented a fraction of the broader strategy and couldn't be used to hurt Goldman's business, court documents suggest.

Earlier this year, Mr. Aleynikov's defense team sought details from the government and Goldman Sachs regarding the bank's high-frequency computer systems. The court denied those requests. Lead defense attorney Kevin Marino, of the Chatham, N.J., law firm Marino, Tortorella & Boyle, argued in his motion this week that the defense requires access to information about Goldman's trading system to prove Mr. Aleynikov "could not have intended to injure Goldman" by taking the firm's trading code.

The bar for clearing a courtroom can be high, said Sandra McCallion, a lawyer specializing in trade-secret cases for the New York law firm Cohen & Gresser LLP. The government has to show that "this is something that is so secret that it will cause harm to [Goldman] if it were made public," she said. The arrest of the Goldman programmer helped put high-frequency trading into the spotlight last year. The strategy, in which powerful computers buy and sell securities at ultrafast speeds, has proved lucrative for many traders. The indictment said Goldman's high-frequency trading operation generated "many millions of dollars in profits per year."

The strategy also has come under heightened scrutiny amid concerns that some high-frequency traders were gaining unfair advantages in the market. The Securities and Exchange Commission has launched an in-depth study of issues surrounding high-speed trading and is considering several proposals to monitor it. This year, regulators have focused on the role high-frequency traders played in the May 6 "flash crash," when some of the fast-moving firms stepped away from the market during the height of the turmoil.

Court documents filed by the government in July 2009, soon after Mr. Aleynikov's arrest, state that Goldman's strategies involve "sophisticated, high-speed and high-volume trades on various stock and commodities markets." Prosecutors allege that Mr. Aleynikov transferred a substantial portion of that code to a computer server in Germany. He then downloaded the code to his personal laptop, which he allegedly brought to Chicago, where he had a meeting a firm that had hired him, start-up trading shop Teza Technologies LLC.

Teza became embroiled in its own legal battle following Mr. Aleynikov's arrest. Founder Mikhail "Misha" Malyshev and Teza employees were sued by their former employer, Chicago hedge fund Citadel LLC, for violating agreements not to work for a competitive firm. In mid-October 2009, a Chicago court granted sanctions against Teza. The Teza case showed how details surrounding a trading strategy can emerge during the course of a trial, including disclosures that the Citadel high-frequency unit pulled in about $1 billion in 2008.

US Mortgages to Drop Below $1 Trillion to Low Since 1996

by Jody Shenn - Bloomberg

Home lending in the U.S. will fall below $1 trillion next year to the lowest level since 1996, according to the Mortgage Bankers Association. Originations will decline to $996 billion in 2011, from a projected total of $1.4 trillion this year, the trade group said today in a statement released during its annual conference in Atlanta. Lending reached a record $3.8 trillion in 2003 as refinancing soared, with new loans remaining elevated over the next few years as home prices and sales boomed.

Rates that are unlikely to go lower even if the Federal Reserve buys more U.S. debt will cause refinancing to dissipate by the second half of next year, Jay Brinkmann, the mortgage group’s chief economist, said. A rush by U.S. homeowners to refinance at near record-low interest rates has marked a rare bright spot for the mortgage industry, under attack for choking the economy with shoddy loans and botched foreclosures.

"With these interest rates, you cannot be having a bad year in 2010," Dan Arrigoni, chief executive officer of Minneapolis-based U.S. Bancorp’s mortgage unit, the sixth- largest U.S. home lender, said yesterday during a panel at the conference. "It will probably go down as ranking number one or two for us, both in terms of production and profits."

Loan rates are influencing refinancing levels even more than during the last explosion in mortgages because tighter lending standards and an almost 30 percent drop in U.S. property prices since their 2006 peak are limiting consumers’ use of cash-out refinancings to tap home equity, said Brinkmann of the Washington-based Mortgage Bankers Association.

Refinancing to Drop

As new-mortgage volumes decline, lenders will need to trim their operations and face greater competition for loans that reduces lending margins, Brinkmann said.

Total home lending will drop next year because refinancing will fall "as mortgage rates increase and the pool of eligible borrowers shrinks," the group said in the statement. More loans for home purchases will offset some of that decline, as "existing home sales recover and home prices stabilize."

This year’s estimated $480 billion of home-purchase mortgages would be the lowest total since 1993, Brinkmann said. Next year, such lending may rise to $626 billion, as refinancing falls to $370 billion from $921 billion, his projections show. Home-loan executives including Arrigoni and Todd Chamberlain, who oversees mortgage lending at Birmingham, Alabama-based Regions Financial Corp., said at the conference that they will be able to respond to lower originations because they expanded this year by adding temporary workers and authorizing overtime for existing employees.

Home-Purchase Lending

Ron J. McCord, chairman of Oklahoma City-based First Mortgage Co., which makes about $1 billion in loans a year, said that he "brought back retirees" who can be let go. His company has been focusing on strengthening its home- purchase lending, including by building relationships with real- estate agents and training staff on government mortgage programs for American Indians, because "we all thought the refis could die this year," he added.

Increases in the value of mortgage-servicing contracts as interest rates rise, extending their projected lives by reducing estimated refinancing, will help some lenders offset lower origination profits, Arrigoni and McCord said. The average rate on a 30-year, fixed-rate mortgage fell to a record low 4.19 percent earlier this month, down from this year’s high of 5.21 percent in April, according to McLean, Virginia-based Freddie Mac.

Compared with a year earlier, existing home sales were down 19 percent in September, the National Association of Realtors said yesterday. Sales fell to a 4.53 million annual rate, exceeding the 4.3 million pace that economists forecast, according to the median projection in a Bloomberg News survey. The Mortgage Bankers’ estimates for total lending have declined from its forecast last month for $1.45 trillion of originations in 2010 and $1.06 trillion in 2011.

Mortgage Investors of the World, Unite!

by Shira Ovide - Wall Street Journal

CNBC has more news today about a pow-wow held by institutional investors to discuss mortgage issuers’ potential liability over problems with home loans. Deal Journal colleague Ruth Simon reported the New York meeting — called "Robosigners and Other Servicing Failures" — came amid increased interest among investors to pursue claims against mortgage-loan servicers and originators for packaging bad mortgages into investment securities.

As the FauxClosure Crisis spreads further, last week a group of institutional investors, including Freddie Mac, Fannie Mae, BlackRock and Pimco sent a letter to Bank of America, seeking to recoup mortgage-related losses. Analysts’ estimates of industry-wide mortgage hits to banks have gone as high as $130 billion

Fed Won’t Join Bank High Court Appeal on Crisis Loans

by Bob Ivry and Greg Stohr - Bloomberg

The Federal Reserve won’t join a group of the largest commercial banks in asking the U.S. Supreme Court to let the government withhold details of emergency loans made to financial firms in 2008. The central bank’s decision not to appeal makes it less likely the high court will hear the case, said Tom Goldstein, a Washington lawyer who has argued 22 cases before the high court since 1999 and whose Scotusblog Website tracks the panel.

The Clearing House Association LLC, a group of the biggest commercial banks, filed the appeal today. Under federal rules for appeals, a lower court’s order requiring disclosure remains on hold until the Supreme Court acts. "We will await a determination from the courts and will comply fully with any final order," said David Skidmore, a spokesman for the central bank. "The Federal Reserve remains committed to timely and responsible transparency of its operations."

The bank group is appealing a federal judge’s August 2009 ruling requiring the Fed to disclose records of its emergency lending. Bloomberg LP, the parent company of Bloomberg News, sued for the release of the documents under the Freedom of Information Act. The central bank has never disclosed the identities of borrowers since the creation in 1914 of its Discount Window lending program, which provides short-term funding to financial institutions, the Clearing House said in its petition.

‘Threatens to Harm’

"Disclosure of this information threatens to harm the borrowing banks by allowing the public to observe their borrowing patterns during the recent financial crisis and draw inferences -- whether justified or not -- about their current financial conditions," the group said in its appeal. The Fed’s emergency programs, which were "essential responses to the recent financial crisis," would be harmed if the central bank is forced to disclose lending records, the group said in a statement today. "Unless the ruling is overturned by the U.S. Supreme Court, businesses and individuals may decline to participate in these programs, possibly impairing the federal government’s ability to act effectively in times of crisis."

"Greater transparency results in more accountability, and the banks’ resistance continues to engender suspicion among taxpayers about the bailouts," said Matthew Winkler, Bloomberg News editor-in-chief. "The banks’ move to appeal will deepen the public’s skepticism and defend a position that every other court has disagreed with. The public has the right to know." Under the Supreme Court’s normal procedures, the justices may say as early as mid-December whether they will take up the case. If so, they would hear arguments next year and likely rule by July.

The central bank’s decision not to file its own appeal undermines a central argument against disclosure, said Simon Johnson, a finance professor at the Massachusetts Institute of Technology and a former chief economist at the International Monetary Fund. "The banks are on their own -- their appeal without the Fed makes it clear that system stability issues are not at stake," Johnson, a Bloomberg contributor, said in an e-mail. The Fed and the U.S. solicitor general, who serves as the government’s top Supreme Court lawyer, will probably file a brief in response to the Clearing House petition, said Goldstein, of Scotusblog. He’s a lawyer at Akin Gump Strauss Hauer & Feld LLP.

Possible Argument

One possibility is that the government will argue that the case isn’t worthy of Supreme Court review, even though it will say lower courts reached the wrong conclusion, Goldstein said. The fact that the banks appealed while the Fed did not "demonstrates the desperation of the banks to hide their true condition during the crisis," said Joshua Rosner, managing director of Graham Fisher & Co., an investment advisory firm in New York. "Political realities made it harder for the Fed to do the banks’ dirty work," he said.

The Fed is facing unprecedented oversight by Congress. The Wall Street Reform and Consumer Protection Act, known as Dodd- Frank, mandates a one-time audit of the Fed as well as the release of details on borrowers from Fed emergency programs. Discount Window loans made after July 21, 2010, would have to be released following a two-year lag. The Bloomberg lawsuit asks for information on that facility and others.

At issue in the litigation are 231 "remaining term reports," originally requested by the late Bloomberg News reporter Mark Pittman, documenting loans to financial firms in April and May 2008, including the borrowers’ names and the amounts borrowed. Pittman asked for details of four lending programs, the Discount Window, the Primary Dealer Credit Facility, the Term Securities Lending Facility and the Term Auction Facility. After averaging $257 million a week in the five years before March 2008, Discount Window borrowing jumped to a peak of $111 billion on Oct. 29, 2008. It was $20 million last week. The other three programs accounted for more than $800 billion in lending at their peak, according to Fed data.