"Laundry day in the Quarter, New Orleans, 1133-1135 Chartres Street"

Ilargi: Just after I wrote a few days ago on the Consumer Metrics Institute's latest batch of graphs and data, I saw that Doug Short had had the same idea, and even added a number of his own great graphs using the CMI data. I decided to do a follow-up on the topic, because this may well be the most important set of economic indicators we have available to us when it comes to what's going to happen between now and 2011, as well as beyond. (Do note, once again, that CMI bases its data exclusively on the 70% of US GDP driven by consumers.)

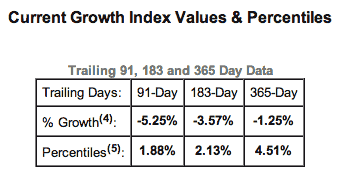

Allow me to start off with what Doug Short has to show and tell. That is, after this little detail, which Short has had no time to incorporate yet either: The CMI Current Growth Index Values table indicates a further deterioration in the 91-day Trailing Index from last Friday's -5.06%. Today it stands at -5.25%:

Take it away, Doug:

The charts below focus on the [Consumer Metrics Institute] 'Trailing Quarter' Growth Index, which is computed as a 91-day moving average for the year-over-year growth/contraction of the Weighted Composite Index, an index that tracks near real-time consumer behavior in a wide range of consumption categories. The Growth Index is a calculated metric that smooths the volatility and gives a better sense of expansions and contractions in consumption.

The 91-day period is useful for comparison with key quarterly metrics such as GDP. Since the consumer accounts for over two-thirds of the US economy, one would expect that a well-crafted index of consumer behavior would serve as a leading indicator. As the chart suggests, during the five-year history of the index, it has generally lived up to that expectation. Actually, the chart understates the degree to which the Growth Index leads GDP. Why? Because the advance estimates for GDP are released a month after the end of the quarter in question, so the Growth Index lead time has been substantial.

Has the Growth Index also served as a leading indicator of the stock market? The next chart is an overlay of the index and the S&P 500. The Growth Index clearly peaked before the market in 2007 and bottomed in late August of 2008, over six months before the market low in March 2009.

The most recent peak in the Growth Index was around the first of September, 2009, almost eight months before the interim high in the S&P 500 on April 23rd. Since its peak, the Growth Index has declined dramatically and is now deep into contraction territory.

It's important to remember that the Growth Index is a moving average of year-over-year expansion/contraction whereas the market is a continuous record of value. Even so, the pattern is remarkable. The question is whether the latest dip in the Growth Index is signaling a substantial market decline like in 2008-2009 or a buying opportunity like in June 2006.

The next chart is a three-way overlay — the 91-day Growth Index, GDP and the S&P 500. I've also highlighted the recession that officially began in December 2007 and unofficially ended last summer. As a leading indicator for GDP, the Growth Index also offers an early warning for possible recessions.

Preliminary Conclusion

The Consumer Metrics Institute's Growth Index hasn't been in operation very long, but thus far it has been an effective leading indicator of GDP. As such, the prospect of a double-dip recession, something that's happened only once since the Great Depression, remains a possibility.

Ilargi: It won't surprise you when I say that I think Doug Short's preliminary conclusion, that a double-dip recession "remains a possibility", is way too cautious, to say the least.

A society cannot buy its way out of a debt-driven depression by taking on more debt, or at least not when a number of vital necessities are entirely lacking. When there's no (rise in) productive capacity, or in consumer spending, and when exports can't go up substantially, in other words, when every penny written off has to be replaced by another penny borrowed just to stand still, it doesn't really matter what all sorts of statistics seem to indicate, that society is no better off for it, and can thus not be said to be out of its recession.

As for the choice of the words "remains a possibility", look, I know CMI hasn't been around for ages, and I know nobody can predict the future, and yes, maybe, there's a flaw somewhere in their model. But I also know that this model, as we can all see in the graphs, has been remarkably and consistently dead on when compared to both "official" GDP numbers and the S&P 500.

And with that in mind, what I see, especially in Doug Short’s last graph, the one where all three come together, is downright scary. Yes, since CMI doesn't incorporate government spending in its data (other than direct give-aways to consumers, presumably), there is a chance of the government injecting enough money to counter the downtrend.

Still, if you look closely, and you shift the CMI Growth Index forward by one quarter, and the S&P backward by the same amount, relative to GDP, so you get a more or less correct alignment of peaks and troughs, there can be only one conclusion: the 91-day Trailing Index, which is a leading indicator, foresees a huge drop in both GDP and the stock market in the months ahead.

How low can we fall in the fall?

David Rosenberg, citing Macroeconomic Advisers' U.S. real GDP series, says we're in for a -1.5% drop. He's supposed to be the doomer among "serious economists", yet he's still quite a ways away from the -5.25% that CMI data indicate. Not that a -1.5% plunge in US GDP wouldn't be sufficiently devastating all by itself, mind you.

A few more or less recent developments may shed some additional light on what lies ahead. David Streitfeld writes in the New York Times:

Housing Fades as a Means to Build Wealth[..] many real estate experts now believe that home ownership will never again yield rewards like those enjoyed in the second half of the 20th century, when houses not only provided shelter but also a plump nest egg.

The wealth generated by housing in those decades, particularly on the coasts, did more than assure the owners a comfortable retirement. It powered the economy, paying for the education of children and grandchildren, keeping the cruise ships and golf courses full and the restaurants humming. More than likely, that era is gone for good. "[..]

If the long term is grim, the short term is grimmer. Housing experts are bracing themselves for Tuesday, when the sales figures for July will be released. The data is expected to show a drop of as much as 20 percent from last year. The supply of homes sitting on the market might rise to as much as 12 months, about twice the level of a healthy market. That would push down prices as all those sellers compete to secure a buyer, adding to a slide that has already chopped off as much as 30 percent in home values. [..]

In an annual survey conducted by the economists Robert J. Shiller and Karl E. Case, hundreds of new owners in four communities — Alameda County near San Francisco, Boston, Orange County south of Los Angeles, and Milwaukee — once again said they believed prices would rise about 10 percent a year for the next decade. With minor swings in sentiment, the latest results reflect what new buyers always seem to feel. At the boom’s peak in 2005, they said prices would go up. When the market was sliding in 2008, they still said prices would go up.

Ilargi: Americans, or a large part of them, have -correctly- given up on the notion of the home as a nest egg, or even an ATM. They will increasingly be reluctant to put what's left of their wealth there. So where does their money go? Not in stocks either, say both Bernard Condon at AP :

Bond Bubble Fear Returns as Investors Flee StocksBad economic news sent investors out of stocks and into U.S. Treasurys this past week, extending a rally that has defied some of Wall Street's best minds, and, some say, logic. Treasury bonds maturing in 20 years or more have returned 21 percent so far this year. By contrast, stocks in the Dow Jones industrial average have lost 2 percent. The question now: Is it too late to jump into the great government bond bonanza?

.......... and Graham Bowley at the New York Times:

In Striking Shift, Small Investors Flee Stock MarketInvestors withdrew a staggering $33.12 billion from domestic stock market mutual funds in the first seven months of this year, according to the Investment Company Institute, the mutual fund industry trade group. Now many are choosing investments they deem safer, like bonds. If that pace continues, more money will be pulled out of these mutual funds in 2010 than in any year since the 1980s, with the exception of 2008, when the global financial crisis peaked. [..]

Charles Biderman, chief executive of TrimTabs, a funds researcher, said it was no wonder people were putting their money in bonds given the dismal performance of equities over the past decade. The Dow Jones industrial average started the decade around 11,500 but closed on Friday at 10,213. "People have lost a lot of money over the last 10 years in the stock market, while there has been a bull market in bonds," he said. "In the financial markets, there is one truism: flow follows performance."

Ilargi: In other words, as a society, Americans no longer buy homes nor stocks, or at least a whole lot less than they once did. They now think bonds are where safety lies. Which is partially true. Unfortunately, many will get into long-term bonds, which promise the highest returns. That gets them into a market place they don't know, and if they want to sell before their bonds mature, they are bound to find that other parties do know it.

Short-term Treasuries, people, are the one and only truly viable alternative to cash in your pocket. Even precious metals will prove too volatile in the next few years, though they should be fine later on. Question is: can you afford to hold on to them if the economy staggers, if you lose your home, your job, your health insurance?

The mass move into bonds leads Ambrose Evans-Pritchard to make the following somewhat ironic observation:

America no longer needs Chinese money, for now[China] is building strategic reserves of oil and coal, and probably industrial metals. State entities are buying up natural gas reserves in Africa and Central Asia, or oil sands in Canada, or timber in Guyana. Where this expansion runs into political barriers, they are funding projects – such as a $10bn loan to Petrobras for the deepwater oil off Brazil. Where all else fails, they are buying equities. All of this recyles China's reserve surplus away from US debt.

So it is a good thing that US citizens have stepped into the breach, investing a record $185bn into bonds funds this year (ICI data). JP Morgan describes this as "extraordinary prejudice", evidence of irrational fear. Or perhaps JP Morgan has an extraordinary prejudice against bonds, arguably the shrewdest asset in a world where fiscal stimulus is being withdrawn before the rest of the economy has reached "escape velocity". The inventory cycle is ebbing, manufacturing has tipped over, the workforce is still shrinking, and the economy is sliding into a deflationary rut.

As Moody's said this week, the Great Recession has made sovereign debt suspect. "The burden of proof now falls on governments". Events have "fast-forwarded history", ripping away the 20-year cushion we counted on before the "adverse debt dynamics" of our aging crisis hits home.

Two epochal forces are colliding in the global bond market: core deflation is gathering force but the West is losing sovereign credibility just as fast. Arch-bear Albert Edwards at Société Générale advises clients to prepare for a violent policy swing from one extreme to the other. First we deflate into the abyss: then we inflate hard rates to get out again. At some point the "euthanasia of the rentier" will wear off. Misjudge the sequence at your peril.

Ilargi: However this may be, I urge you to take another look at the Consumer Metrics Institute data. Realize that their Growth Index is a leading indicator, and thus both the S&P 500 and the US GDP numbers, if we take the last five years as a measuring stick, will, over the next quarter, follow the Growth Index down. Way down.

As per this morning, the discrepancy between US GDP (official estimate still +2.45%) and CMI Growth Index (-5.25%) is a staggering 7.7%!. And then look at how closely the two are correlated in the graphs. They’re almost perfect twins. Until now?!

Something evidently has to give here, and it won't be the American consumer, that much we have seen, (s)he ain't giving much, if anything, of what (s)he’s got left. And both the government and the Fed, try as they might, and they certainly will try, have very limited influence on that American consumer, the protagonist in 70% of GDP, and her/his faith in the future. Once that faith begins to wane, and there can be little doubt that it is, it will start feeding on itself on the way down.

If we get anywhere near what the CMI data (seem to) foresee, we’ll have drama, tragedy, mayhem and panic all wrapped in one neat package. The US economy cannott withstand anything even near that sort of fall and pretend the world is still the same.

A few more -inevitable- broken promises and false green shoots and Americans will end up putting their money, if they have any left at all, in their mattresses, not in homes, not in stocks or bonds, not even in banks. Which in turn will cause GDP to fall further. Finish the story at home and color the pictures.

The Never Ending Recession

by The Pragmatic Capitalist

I have long believed that the rally in stocks was largely based on a mean reverting move that was based almost entirely on government intervention and stimulus (see here & here). But few people have remained more steadfast in their bearishness than David Rosenberg. And unfortunately for the market David Rosenberg has been redeemed. His macro outlook is becoming confirmed with every day – deflation, stimulus based recovery, continuing recession. If his outlook continues to be right then Mr. Rosenberg believes we could see a negative GDP print THIS quarter. And if he’s right that means analysts are far too optimistic about the upcoming quarter:"Our suspicions have been confirmed — the recession never ended. Macroeconomic Advisers produces a monthly U.S. real GDP series and it shows that the peak was in April, as we expected, with both May and June down 0.4% in the worst back-to-back performance since the economy was crying Uncle! back in the depths of despair in September-October 2008. The quarterly data show that Q2 stands at a +1.1% annual rate (so look for a steep downward revision for last quarter) and the "build in" for Q3 is -1.5% at an annual rate.

Depending on the data flow through the July-September period, it looks like we could see a -0.5% to -1% annualized pace for the current quarter. Most economists have cut their forecasts but are still in a +2.5% to +3.5% range. What is truly amazing is that despite all the fiscal, monetary, and bailout stimulus, the level of real economy activity, as per the M.A. monthly data, is still 2.5% below the prior peak.

To put this fact into context, the entire peak to trough contraction in the 2001 recession was 1.3%! That is incredible. Interestingly, and dovetailing nicely with our deflation theme, nominal GDP fell 0.3% in May and by 0.4% in June. This is a key reason why Treasury yields are melting."

Analysts at 2.5%-3.5% while Rosenberg is at -1.5%. Wow. If their expectations for equities this year were any indication (see here) then this it might be safe to say that Mr. Rosenberg is the ultimate contrarian Wall Street analyst – and one of the few worth listening to.

Housing Slide in U.S. Threatens to Drag Economy Into Recession

by John Gittelsohn and Bob Willis - Bloomberg

Housing led the U.S. out of seven of the last eight recessions. This time, it may kill the recovery. Home sales collapsed after a federal tax credit for buyers expired in April. Since then, the manufacturing-led expansion, which began in the second half of 2009, has been waning, with jobless claims rising and factory orders falling. "If foreclosures continue to mount and depress home prices, that could send the economy back into a recession," said Celia Chen, an economist who tracks the industry for Moody’s Analytics Inc. "The housing market and the broader economy are closely intertwined."

Spending on home construction and items such as furniture and stoves accounted for about 15 percent of gross domestic product in the second quarter, according to West Chester, Pennsylvania-based Moody’s Analytics. Real estate also can influence consumer spending indirectly. When values soared in the mid-2000s, people used the boost in equity to pay for cars and vacations. After prices fell, homeowners lost that cushion and curbed spending.

A report tomorrow by the Chicago-based National Association of Realtors will show July sales of existing homes plummeted 12.9 percent from June, the biggest monthly loss of 2010, according to the median estimate of economists surveyed by Bloomberg. New-home sales, which account for less than a 10th of housing transactions, stayed at the second-lowest level on record last month, economists predict Commerce Department data will show on Aug. 25.

Housing in ‘Doldrums’

"Housing continues to be stuck in the doldrums," said Jeffrey Frankel, a member of the business-cycle dating committee at the National Bureau of Economic Research, the arbiter of when U.S. recessions begin and end, and a professor at Harvard University in Cambridge, Massachusetts. With 14.6 million Americans out of work, homeowners are struggling to hold onto their properties. One in seven mortgages were delinquent or in foreclosure during the first quarter, the highest in records dating to 1979, according to the Washington- based Mortgage Bankers Association.

Foreclosures probably will top 1 million this year, said RealtyTrac Inc., an Irvine, California-based data company. Federal efforts to help have had little success. Of 1.31 million loan modifications started under the Obama administration’s Home Affordable Modification Program, 48 percent were canceled by the end of July, the Treasury Department said Aug. 20. More than half of all modifications defaulted again within 12 months, the Office of the Comptroller of the Currency said June 23.

Sidelined Buyers

Shadow inventory, or the number of homes repossessed or in default that eventually will be offered for sale, stood at 7.3 million in the first quarter, according to Laurie Goodman, an analyst in New York at mortgage-bond broker Amherst Securities Group LP. As those properties hit the market, prices will come under pressure and buyers will wait for better deals.

Those sidelined house hunters include Marion and Jim Lasswell, who said they spend most weekends looking at homes for sale near Raleigh, North Carolina. His engineering job at iRobot Corp. is secure, the couple’s credit is good and they have saved enough for a 20 percent down payment, Marion Lasswell said. The problem: they don’t think the market has hit bottom. "We’re still watching prices drop," Lasswell, 38, a registered nurse, said in a telephone interview. She said they won’t buy "until there’s an awesome deal."

GDP Weakens

Home prices tumbled 33 percent from their July 2006 peak to the low in April 2009, according to the S&P/Case-Shiller 20-city index. They may drop another 20 percent by 2012 if the economy slips back into a recession, according to Chen, the Moody’s Analytics economist. Gross domestic product increased less than 1.5 percent in the second quarter, the slowest rate since the recovery began, according to the median forecast by economists in a Bloomberg survey. That’s down from the 2.4 percent rate initially reported by the Commerce Department last month. Growth may ease to 1.3 percent by the first quarter of next year, according to the New York-based Conference Board.

Consumer spending rose 1.6 percent in the second quarter, down from 1.9 percent in the previous three months. Purchases of home furnishings and appliances fell 1.7 percent to an annual pace of $256.5 billion in June from a 2010 high in April, according to the Bureau of Economic Analysis. "There is an epidemic of thrift," said Nariman Behravesh, chief economist at IHS Inc. in Lexington, Massachusetts. "Households and businesses are super-cautious right now. Sometime in the next 6 to 12 months, we’ll start to see more movement on home and car purchases and greater willingness on the part of businesses to hire."

Federal Reserve policy makers on Aug. 10 made their first attempt to shore up the recovery by pledging to keep their holdings of securities and prevent money from draining out of the banking system. They said the economic expansion probably will be "more modest" than earlier anticipated. The Fed has held the target for its benchmark lending rate near zero since December 2008 and purchased $1.43 trillion worth of debt to keep rates low and bolster housing. "Household spending is increasing gradually, but remains constrained by high unemployment, modest income growth, lower housing wealth and tight credit," the Fed said in a statement.

Buying Plans

The average U.S. rate for a 30-year fixed mortgage dropped to 4.44 percent in the second week of August, the lowest recorded by McLean, Virginia-based Freddie Mac, the second- largest mortgage buyer. A July survey by the Conference Board found 1.9 percent of the respondents planned to buy a home in the next six months, near December’s 27-year low of 1.7 percent. A sustained economic recovery depends on the job growth required to boost consumer spending, said Behravesh of IHS. The unemployment rate may average 9.6 percent this year, based on the median estimate of economists in a Bloomberg survey. That would be the highest annual rate since 1983.

Home construction and property sales led the way out of the previous seven recessions going back to 1960, according to PMI Group Inc., a mortgage insurer in Walnut Creek, California. New- home sales improved an average of eight months before the beginning of economic growth, and single-family housing starts improved seven months before recovery. That didn’t happen in the last recession. Sales of new houses fell in five of the eight months before economic expansion began in 2009’s second half. Housing starts fell in two of seven months. While the Lasswells in North Carolina said they’ll keep spending their weekends looking at homes, they aren’t in a hurry to buy. "I don’t see things getting better," Marion Lasswell said. "I expect prices to be flat for a long time."

Housing Fades as a Means to Build Wealth

by David Streitfeld - New York Times

Housing will eventually recover from its great swoon. But many real estate experts now believe that home ownership will never again yield rewards like those enjoyed in the second half of the 20th century, when houses not only provided shelter but also a plump nest egg.

The wealth generated by housing in those decades, particularly on the coasts, did more than assure the owners a comfortable retirement. It powered the economy, paying for the education of children and grandchildren, keeping the cruise ships and golf courses full and the restaurants humming. More than likely, that era is gone for good. "There is no iron law that real estate must appreciate," said Stan Humphries, chief economist for the real estate site Zillow. "All those theories advanced during the boom about why housing is special — that more people are choosing to spend more on housing, that more people are moving to the coasts, that we were running out of usable land — didn’t hold up."

Instead, Mr. Humphries and other economists say, housing values will only keep up with inflation. A home will return the money an owner puts in each month, but will not multiply the investment. Dean Baker, co-director of the Center for Economic and Policy Research, estimates that it will take 20 years to recoup the $6 trillion of housing wealth that has been lost since 2005. After adjusting for inflation, values will never catch up. "People shouldn’t look at a home as a way to make money because it won’t," Mr. Baker said.

If the long term is grim, the short term is grimmer. Housing experts are bracing themselves for Tuesday, when the sales figures for July will be released. The data is expected to show a drop of as much as 20 percent from last year. The supply of homes sitting on the market might rise to as much as 12 months, about twice the level of a healthy market. That would push down prices as all those sellers compete to secure a buyer, adding to a slide that has already chopped off as much as 30 percent in home values.

Set against this dismal present and a bleak future, buying a home is a willful act of optimism. That explains why Adam and Allison Lyons are waiting to close on a $417,500 house in Deerfield, Ill. "We’re trying not to think too far ahead," said Ms. Lyons, 35, an information technology manager. The couple’s first venture into real estate came in 2003 when they bought a condo in a 17-unit building under construction in Chicago. By the time they moved in two years later, it was already worth $50,000 more than they had paid. "We were thinking, great!" said Mr. Lyons, 34.

That quick appreciation started them on the same track as their parents, who watched the value of their houses ascend for decades. The real estate crash interrupted that pleasant dream. The couple cannot sell their condo. Unwillingly, they are becoming landlords. "I don’t think we’re ever going to see the prosperity our parents did, but I don’t think it’s all doom and gloom either," said Mr. Lyons, a manager at I.B.M. "At some point, you just have to say what the heck and go for it."

Other buyers have grand and even grander expectations. In an annual survey conducted by the economists Robert J. Shiller and Karl E. Case, hundreds of new owners in four communities — Alameda County near San Francisco, Boston, Orange County south of Los Angeles, and Milwaukee — once again said they believed prices would rise about 10 percent a year for the next decade. With minor swings in sentiment, the latest results reflect what new buyers always seem to feel. At the boom’s peak in 2005, they said prices would go up. When the market was sliding in 2008, they still said prices would go up. "People think it’s a law of nature," said Mr. Shiller, who teaches at Yale.

For the first half of the 20th century, he said, expectations followed the opposite path. Houses were seen the way cars are now: as a consumer durable that the buyer eventually used up. The notion of housing as an investment first began to blossom after World War II, when the nesting urges of returning soldiers created a construction boom. Demand was stoked as their bumper crop of children grew up and bought places of their own. The inflation of the 1970s, which increased the value of hard assets, and liberal tax policies both helped make housing a good bet. So did the long decline in mortgage rates from the early 1980s.

Despite all these tailwinds, prices rose modestly for much of the period. Real home prices increased 1.1 percent a year after inflation, according to Mr. Shiller’s research. By the late 1990s, however, the rate was 4 percent a year. Happy homeowners were taking about $100 billion a year out of their houses, which paid for a lot of good times. "The experience we had from the late 1970s to the late 1990s was an aberration," said Barry Ritholtz of the equity research firm Fusion IQ. "People shouldn’t be holding their breath waiting for it to happen again."

Not everyone views the notion of real appreciation in real estate as a lost cause. Bob Walters, chief economist of the online mortgage firm Quicken, acknowledges that the recent collapse will create a "mind scar" just as the Great Depression did. But he argues that housing remains unique. "You have to live somewhere," he said. "In three or four years, people will resume a normal course, and home values will continue to increase."

All homes are different, and some neighborhoods and regions will rebound more quickly. On the other hand, areas where there was intense overbuilding, like Arizona, will be extremely slow to show any sign of renewal. "It’s entirely likely that markets like Arizona will not recover even in the 15- to 20-year time frame," said Mr. Humphries of Zillow. "The demand doesn’t exist." Owners in those foreclosure-plagued areas consider themselves lucky if they are still solvent. But that does not prevent the occasional regret that a life-changing sum of money was so briefly within their grasp.

Robert Austin, a Phoenix lawyer, paid $200,000 for his home in 2000. Five years later, his neighbors listed a similar home for $500,000. Freedom beckoned. "I thought, when my daughter gets out of school, I can sell the house and buy a boat and sail around the world," said Mr. Austin, 56. His home is now worth about what he paid for it. As for that cruise, "it may be a while," Mr. Austin said. Showing the hopefulness that is apparently innate to homeowners, he added: "But I won’t rule it out forever."

Will Growing Rental Trends Undermine U.S. Home Sales?

by Keith Jurow - Real Estate Channel

There is a far-reaching change occurring now which threatens housing markets around the country. A survey conducted by Harris Interactive for the National Apartment Association in May 2010 found that 76% of those surveyed now believe that renting is a better option than buying in the current real estate market, up from 71% in 2008. Especially sobering was the fact that 78% of those surveyed were homeowners.

David Neithercut, CEO of Equity Residential, the nation's largest multi-family landlord, believes that there is a "psychology change" in the mind of consumers. In a June address to an industry conference, he declared that there is "a change in one's thought process about the benefits or wisdom of owning a single-family home."

Given this introduction, let's take an in-depth look at whether there is a movement away from the idea of homeownership as a worthwhile goal and toward the benefit of renting.

End of the Housing Bubble Led to a Surge in Houses Available to Rent

As early as the summer of 2005, the slowdown in speculative buying in the hottest metros caused a flood of investor-owned homes to hit the rental market. In August 2005, an article in the Wall Street Journal entitled "Speculators Push Rents Down" pointed out that the supply of rental homes in the Phoenix area almost doubled from a year earlier. Average rents for these houses dropped by nearly 10%. Similar situations were found in markets as diverse as Fairfield County in Connecticut, Kansas City, Las Vegas, San Diego and Palm Coast, Florida.

Even more ominous was the fact that 1.34 million single-family home rentals stood vacant. This had risen from only 900,000 in 2003 according to Harvard University's Joint Center for Housing Studies. Many of these homes became rentals because the investor was unable to flip the property. By the end of 2006, the number of vacant homes for sale had skyrocketed to 2.1 million according to the Census Bureau.

As I pointed out in a previous REAL ESTATE CHANNEL article, the glut of rental homes in bubble markets such as Phoenix had caused rents to plunge to half the cost of owning that same home by the beginning of 2008. The press began to notice that the soaring number of homes and condos for rent was providing an attractive alternative to buying.

A June 2008 Associated Press article posted in the Los Angeles Times emphasized that these rental properties were attracting "displaced homeowners" who preferred them to an apartment. As foreclosures soared, these displaced homeowners continued to opt for rental homes. A January 2010 article about the Denver rental market posted by Inside Real Estate News pointed out that "if a family loses their home in a foreclosure, instead of leasing an apartment in a building they will rent another home." What happens after a single-family foreclosure is that "the family moves into a rental house down the street." The author noted the irony in the fact that the home they are moving into may also be a foreclosure that had been bought by an investor.

2010 - Homes for Rent Continue to Increase and Rents Continue to Weaken

With the collapse in Florida home prices over the past three years, you would think that house rents might have begun to firm. No way. An article published in January 2010 in the online Herald Tribune painted a dismal picture of the rental market. One landlord who owns more than 150 single-family homes lamented that "There isn't the demand that there was a few years ago because we've lost our construction workers ... We certainly have a lot of empty units."

Another owner of ten rental homes stated that she and other landlords had had to reduce rents by "at least a third." A house that commanded a rent of $900 a few years ago gets only $500 now. There are simply not enough potential renters who can afford even these slashed rents. Because many of these smaller professional landlords are also faced with rising vacancies, a growing number of them are seeing their properties fall into foreclosure.

A month later, an article appeared on iMarketNews.com which reviewed the house rental market around the country. The picture was nearly as grim. In Brooklyn, New York, whose market has held up better than most, rents have slipped by roughly 20% since early 2009. A similar percentage drop was seen in the California communities of Venice and Santa Monica.

The owner of a property management firm in St. George, Utah stated that home rental vacancies were the highest he had seen in the last thirty years. Another property management owner in Portland, Oregon bemoaned the fact that frustrated sellers have been throwing their properties onto the rental market, adding to the glut. The same thing was happening in the California Inland Empire city of Temecula. One close observer of that market noted that the asking rent for single-family homes had slipped below apartment rents which was almost unthinkable only a year or two earlier.

More recently, the May 2010 Las Vegas Rental Home Market Report stated that median house rents were down nearly 10% from a year earlier even though leasing volume was up by 20%.

Those Who Can Afford to Buy Are Extremely Reluctant to Do So

While surveys and statistics can be very revealing about the housing market, you cannot really get a good sense of the changing mindset of Americans from them. To do that, you need to spend time reading comments written on some of the housing blogs and in response to online articles.

Let's start with a blog called Metropolis which covers the Philadelphia region. A mid-July posting by the roughly 30 year old editor discussed the question faced by her and her husband since they moved from Boston. Clearly, they had the combined income to afford to purchase in the pricy Center City.

Yet they decided to rent even though rents were high. As she explained the decision, "Part of the appeal of being young, urban and childless is the freedom to travel frequently, relocate on a whim, and throw all of our disposable income at shiny new consumables." She went on to ask, "Do I want the responsibility of owning a home? Not in the slightest." Though she admitted that she and her husband might purchase a property, she ended the article by declaring that "Until then, I'll be proudly writing my monthly rent checks."

One of the commenters on the article advised the author that there were plenty of affordable nice rentals with great amenities outside of Center City. Another commenter with a new baby felt the pressure from everyone to buy a property in the suburbs. But that was not what they wanted. As she put it: "We're moving this fall from one rental to another, and I like the feeling of having something new. With a pool I don't pay for, a gym that's open 24 hours a day, and emergency plumbers on staff at 2 a.m., I have enough responsibility in my life that I don't need a home." She closed by declaring that "my rent payment gets me ... the amenities I've grown accustomed to ... and the peace of mind that someone else is responsible for maintenance."

Another blog raised the question of whether it made more sense to rent or buy. A Chicago commenter said unequivocally that "I think we might be renters forever. My husband and I love sitting ... in the park reading the Sunday New York Times while our landlord is stuck fixing the garbage disposal. Time is priceless. And we are nowhere nearly as freaked out about finances as our friends are."

Another commenter explained unequivocally that "Renting is a service I gladly pay for. We spend about $40 a day for use of a nice three-bedroom townhouse on a quiet street, with a private yard, a larger park for kids in the complex ... I like having money set aside for a surprise like a weekend trip to Manhattan or a night at the Opera instead of a blown water heater or a leaky roof."

Finally, an article on the online Wall Street Journal in early August discussed the glut of homes for sale. One commenter proudly boasted that "I sold my home four years ago in south Orange County [CA] and have been biding my time as the market props run their course."

Another commenter declared that "[I] have close to 200k household income, 100k down payment waiting in the bank, but any home I'm interested in is close to a million or more. Sure, I could afford a condo or home in less desirable areas, but I prefer to live near my socio-economic peers. I don't understand how families can afford to buy 700-800k homes on 70k household incomes. Until things make sense, I'm not buying. I'm happy to continue renting in a nice neighborhood close to work, and use the left over cash to feed my nest egg."

The Caretaker Alternative

For those of you who may be reluctant to buy but are hesitant to sign a lease of one year or longer, an alternative known as a caretaker could be worth looking into. To deal with the growing number of vacant, habitable homes which the owner would eventually like to sell, an industry known as home tending has blossomed in the last fifteen years.

The concept is a simple one. Vacant homes often attract vandals, thieves, drug dealers and even squatters. Home tending companies provide clients such as individual owners, real estate agents, builders with vacant homes built on spec, remodelers fixing up a property to flip, and occasionally banks with a carefully screened live-in caretaker.

The home tender firm does not charge the client anything. How do they make money? Caretakers gladly pay a reasonable fee to live in a very nice home with their own furniture. According to one home tending company owner in San Antonio, the caretaker may pay about $750 a month to occupy and care for a house worth $400,000.

The monthly payment is not rent according to a company owner in the Phoenix area. As she explains it, the caretaker is a subcontractor of her firm who understands that there is no fixed time commitment for staying in the house.

The caretaker is responsible for keeping the house clean and maintained and the yard mowed and manicured so it can be shown to a prospective buyer at a moment's notice. The Phoenix firm does a background check and requires caretakers to complete their training program. The caretaker must also carry a minimum of $300,000 in liability insurance and $25,000 personal property insurance.

When the house is sold, the caretaker is usually given 10-14 days to vacate. One of the largest firms, located in Utah, will sometimes shift a caretaker to another property when the one they have been occupying is sold.

Who are these caretakers? Many of them are professionals who are relocating and either need a temporary place to reside or want to learn more about an area before deciding where to live more permanently. They also include former homeowners who have lost their property to foreclosure and need a place to live until they can get back on their feet. Some are divorced men or women in transition and looking to start a new phase in their lives. Others are renters trying to save enough money for a down payment on a house they hope to buy in the future.

Why Renting Will Be a Popular Alternative to Buying for Years

Some housing analysts argue that the American dream of home ownership is still alive and well and will reassert itself when the economy and housing markets recover. This is little more than wishful thinking.

The housing bubble of 2004-2006 was the climax of a powerful belief which had formed over decades that residential property prices always go up. The collapse in home prices around the country since late 2006 has shattered this assumption. Zillow's latest Homeowner Confidence Survey for this year's second quarter reported that one-third of all homeowners do not believe that home prices have reached a bottom.

The change in attitude toward owning a home cited in the beginning of this article has now reached the blogosphere. A Google search I ran on renting vs. buying found a website which posted links to 48 blogs that touted renting as the preferable option. How many of them were there during the peak bubble years?

The attraction of renting now is boosted by the growing vacancy rate for both houses and apartments. The following chart posted recently by the Calculated Risk blog shows the long-term upward trend.

With nationwide vacancy rates now well over 10%, it is extremely difficult for a landlord to even consider raising rents. Since roughly 25% of all home sales are currently going to investors paying cash, large numbers of homes will continue to be thrown onto the rental market.

The one major market where there is apparently a shortage of nice 3-4 bedroom rental homes is Phoenix according to the Cromford Report. If this claim is accurate, it is due to thousands of former homeowners who have lost their house to either foreclosure or a short sale and are looking for an attractive home to rent. The supply is down because, as I have reported in a previous article, banks are withholding most repossessed homes from the market.

For all the reasons discussed in this article, the attractiveness of renting will be a serious impediment to the return of potential buyers to the housing market. The change in consumer attitude is well summed up in this March 2010 post on a Zillow advice thread:

"We cannot wait to rent and walk away from this upside down/underwater bad investment. And while we go through the process (foreclosure) 6 to 8 months, we will be socking away the $2600+ mortgage payments preparing for our rental. Even $1500.00 for the rental of a home as nice or even nicer is $1100.00 per month ahead. Just think, no property taxes, no HOA dues and when something goes wrong, call the landlord. We can handle the credit hit. Currently we have about 840 FICO. The way things are going we will be able to save enough cash to just buy a house in a few years."

Post-Mortgage Meltdown, Where Do We Go Now?

by NPR

For more than 20 years, the mantra in Washington has been "more, not less" when it comes to Fannie Mae, Freddie Mac and the expansion of homeownership. But in light of the financial crisis and Fannie and Freddie's near-collapse, policy leaders are also rethinking the government's role — and many Americans are starting to question whether homeownership is the only path to the American Dream.

Fannie and Freddie function by buying, bundling and then stamping a government guarantee on mortgages. Then they sell them to investors. It keeps the banks happy because it keeps capital flowing, and it keeps consumers happy because it makes low, fixed-rate mortgages possible. At least that how things were supposed to unfold. But the two mortgage finance giants "made astonishing mistakes," Raj Date, executive director of a financial policy think-tank called the Cambridge Winter Center, told NPR's Audie Cornish.

'It Has All Come Back To Haunt Them'

"As normal people everywhere in the country realized that housing prices seemed to be growing straight into the stratosphere, instead of becoming more conservative about lending against those ridiculously high values, Fannie and Freddie just continued to make the same kind of loans and indeed made more aggressive loans during that period of 2005, 2006, 2007," Date said. "And it has all come back to haunt them."

So instead of rationally-priced credit, he said, the country wound up with a $6 or $7 trillion bubble in housing values. And all of Wall Street and most of the country's banks made the same sort of mistakes, Date said. Policy makers are at a bit of a crossroads, said Date, who was among a number of industry leaders who huddled with Treasury Secretary Timothy Geithner this week to figure out a new way forward on housing.

Fannie and Freddie have dramatically scaled back their level of aggressiveness in underwriting credit, Date said. But, he added, "the fact of the matter is that on average and over time, Fannie and Freddie represent an economic subsidy from the public at large to middle and upper middle-income homeowners." Despite talk on Capitol Hill of dismantling the two organizations, it might be tough to get rid of them. That's because Fannie and Freddie, along with the Federal Housing Administration, are responsible for some 95 percent of the mortgages in the country today, Date said.

"If you think that the fall of 2008 was calamitous, believe me, you haven't seen anything yet if you were just somehow to turn off the lights on Fannie and Freddie today," he warned. "That said, I think the policy makers are trying to be thoughtful about the right long-term answer is for housing finance more broadly, and that involves revisiting some issues that have been treated as sort of untouchable for quite some time." Ultimately, Date said it might be time to rethink homeownership as an American ideal.

The White Picket Fence Reconsidered

"The world we live in today is not quite the world that existed in 1950," he noted. "The nature of households and the rate at which they dissolve and reform, the nature of work and its transient nature across geographies are all things that suggest that maybe, just possibly, a middle-class American shouldn't stake themselves to an illiquid, very large, concentrated, leveraged asset —- that is to say, a house."

Alyssa Katz, author of Our Lot: How Real Estate Came To Own Us, also thinks America needs to reconsider the American Dream. "Homeowenership has gone from being pretty much an unmitigated good — something that would provide stability — and instead has thrown a huge cloud of doubt over the value of homeownership for a lot of people." Even so, there also are downsides to renting, she said.

"Some of the common beliefs about renting are absolutely true," Katz said. "Being a renter has very little security. They don't have any promise they'll be able to live in the apartment or home for more than a year or two. Renting is also perceived as something that really divides Americans by class. So I think for a lot of potential renters, or people who own and are thinking of making that transition to renting, they have to overcome this sense that they are giving up a sense of status."

That's a tough thing to shake for many Americans, she said. If more people rent, the benefits of homeownership will only increase for those who own homes because the pool will shrink, Katz said. "Those who have access to homeownership and the benefits that it brings, as a result of policy, will be even more privileged than they are now."

$4.4 Trillion

by WSJ Editorial

That's how much the US spending baseline has increased in 31 months.

Speaking last Wednesday in Columbus, Ohio, President Obama asked, "How do we, over the long term, get control of our deficit?" Good question. Here's the answer suggested by last Thursday's semi-annual budget summary from the Congressional Budget Office: Stop spending so much. CBO's mid-year review largely reinforces the bad news we already knew—to wit, that spending has exploded since Democrats took over Congress in 2007, first with the acquiescence of George W. Bush and then into hyperdrive after Mr. Obama entered the White House.To appreciate the magnitude of this spending blowout, compare CBO's budget "baseline" estimate in January 2008 with the baseline it released Thursday. The baseline predicts future spending based on the law at the time. As the nearby chart shows, in a mere 31 months Congress has added more than $4.4 trillion to the 10-year spending baseline. The 2008 and 2009 numbers are actual spending, the others are estimates. As recently as 2005, total federal spending was only $2.47 trillion.

Keep that $4.4 trillion in mind the next time you hear Mr. Obama or Speaker Nancy Pelosi say they "inherited" this budget mess. Let's assume the recession that Mr. Obama inherited—Mrs. Pelosi was already in power—was responsible for causing $1 trillion or so in deficit spending. That still doesn't explain why the annual deficit of roughly $1.4 trillion will be nearly as high in fiscal 2010, after a year of economic growth, as it was in 2009. Or why CBO says the deficit will still be nearly $1.1 trillion in 2011 even if all of the Bush-era tax cuts are repealed.

The deficit is barely declining because of the lackluster economic recovery, which continues to yield too little revenue, and especially because of the record levels of spending passed by the Democratic Congress and eagerly signed by Mr. Obama. To pick one illustration: The annual average increase in domestic, nondefense discretionary spending—on the likes of education, food stamps, and things other than Medicaid, Medicare and Social Security—was 6.4% from 1999-2008. Yet in 2009, nondefense discretionary spending rose by 11.2%, and in 2010 it will grow by another 14.7%.

Much of this increase has been added directly to the CBO baseline, compounding future spending levels as far as the green-eyeshade can see. After all of this, CBO nonetheless predicts that nondefense discretionary spending will grow by only 2.3% in 2011. If you believe that, you probably believe that someone other than Mrs. Pelosi will be Speaker of the House.

Bond Bubble Fear Returns as Investors Flee Stocks

by Bernard Condon - AP

Maybe bonds aren't so dull after all. Bad economic news sent investors out of stocks and into U.S. Treasurys this past week, extending a rally that has defied some of Wall Street's best minds, and, some say, logic. Treasury bonds maturing in 20 years or more have returned 21 percent so far this year. By contrast, stocks in the Dow Jones industrial average have lost 2 percent. The question now: Is it too late to jump into the great government bond bonanza?To bulls, the rally is still in its early stages. They say the weak economy will cause stocks to keep falling and people to seek the safety of U.S. government debt. Reports this past week of unexpectedly high unemployment claims and a manufacturing slowdown in the mid-Atlantic region helped bolster their case. But others say Treasury prices have risen too high, perhaps even to bubble proportions. The thinking goes that investors could dump Treasurys as quickly as they bought them on even a whiff of inflation. Inflation is bad for bonds because it eats into principal.

Bonds are generally regarded as safer than stocks because you get your money back when they mature. But that's only true if you pay face value. If you buy when prices are higher, say $101 for a $100 bond, you'll get $1 less than you put in. In purchasing power, you get back even less thanks to inflation. But bonds, of course, also pay interest, and this can more than make up the difference. The problem is, bond bears argue, the interest isn't compensating you much now. The yield on 10-year Treasurys, which moves opposite its price, stands at 2.61 percent, a low not seen since early 2009 during the depths of the credit crisis. At that rate, it would take you 27 years to double your money.

"In the long run we don't think you'll make a good return" in government bonds, says Mark Phelps, CEO of money manager W.P. Stewart & Co., citing the low yields. Phelps suggests that investors worried about a stalled recovery should stick to stocks of big, conservative companies with little debt and fat dividends. Though you can still get hurt if their stocks fall, at least the dividends will help compensate. An added appeal: The dividends offered by such blue chips are higher than current 10-year Treasury yields.

PepsiCo Inc., for instance, will pay you $3 annually now for every $100 you invest: nearly 50 cents more than Washington pays for holding your money for 10 years. What's more, the stock is trading at 14.5 times estimated annual earnings. The median, or midpoint, over the past 20 years is 23 times estimated earnings, meaning the stock is cheap, at least by this one measure. Phelps also likes Procter & Gamble Co. stock. It pays you even more than Pepsi: $3.20 a year for every $100 invested. The maker of Pampers diapers and Pringles chips trades at 14.8 times estimated earnings, a discount to its 19 median. "To put all in Treasurys, looks like a mistake to us," says Phelps, whose firm manages $1.5 billion. But he adds, "I would have said that at the beginning of the year, and I would have been wrong."

He's got good company. For years, famed investors and economists have been warning that the price of Treasurys had risen too high. Bill Gross of giant bond firm Pimco said that Treasurys had some "bubble characteristics" in December 2008 when 10-year yields neared 2 percent. Nouriel Roubini, who gained near celebrity status after calling the crash, warned of a bubble about the same time. In a letter to his Berkshire Hathaway shareholders last year, Warren Buffett compared the "U.S. Treasury bond bubble of late 2008" to the Internet and housing bubbles.

However, as fears of an economic collapse receded last year, investors rushed into stocks and out of Treasurys, sending prices down and yields up. Now, as yields slip closer to their late 2008 lows, bubble talk has returned. On Wednesday The Wall Street Journal published a letter from Wharton professor Jeremy Siegel and Jeremy Schwartz, director of research at Wisdom Tree Investments Inc., that likened Treasurys to dot-com stocks of the late '90s before they crashed. The headline: "The Great American Bond Bubble." They noted that yields on some bonds are the lowest in 55 years. Their advice to investors will sound familiar: Buy blue chips with fat dividends.

Avi Tiomkin, chief investment officer of Tigris Financial Group and a Treasury bull for years, disagrees. "Dividends are great as long as a company can make money," he says. "But if the economy sinks, they'll stop paying." Tiomkin says he's sticking with Washington IOUs. A year ago he correctly predicted the 10-year yield would fall from 3.75 percent to around 2.50 percent by mid-2010. Now he foresees deflation, or a consistent and widespread fall in prices for goods and services similar to what afflicted Japan during the '90s. And that will drive more people into Treasurys, lifting prices and pushing 10-year yields to below 2 percent, possibly all the way to 1 percent, within a year.

Van Hoisington, president of an eponymous investment firm in Austin, Texas, who also foresaw the Treasury rally, is not buying all the bubble talk either. In his latest newsletter, he writes that "The risk, if not the probability, is that deflation lies ahead." He recommends buying Treasury bonds, as he has done for years now. He has returned 11 percent over three years. Jack Ablin, chief investment officer at Harris Private Bank, prefers stocks. But even he's worried.

Ablin notes that Federal Reserve interest rate cuts intended to spur borrowing and spending don't have much of an impact if people are swimming in debt and can't or won't borrow. If prices of consumer goods fall, he says, that will make matters worse as people defer purchases in hopes they can buy cheaper later. "There is little (the Fed) can do but stand on sidelines with pom poms and cheer people on," he says.

In Striking Shift, Small Investors Flee Stock Market

by Graham Bowley - New York Times

Renewed economic uncertainty is testing Americans’ generation-long love affair with the stock market. Investors withdrew a staggering $33.12 billion from domestic stock market mutual funds in the first seven months of this year, according to the Investment Company Institute, the mutual fund industry trade group. Now many are choosing investments they deem safer, like bonds. If that pace continues, more money will be pulled out of these mutual funds in 2010 than in any year since the 1980s, with the exception of 2008, when the global financial crisis peaked.

Small investors are "losing their appetite for risk," a Credit Suisse analyst, Doug Cliggott, said in a report to investors on Friday. One of the phenomena of the last several decades has been the rise of the individual investor. As Americans have become more responsible for their own retirement, they have poured money into stocks with such faith that half of the country’s households now own shares directly or through mutual funds, which are by far the most popular way Americans invest in stocks. So the turnabout is striking.

So is the timing. After past recessions, ordinary investors have typically regained their enthusiasm for stocks, hoping to profit as the economy recovered. This time, even as corporate earnings have improved, Americans have become more guarded with their investments. "At this stage in the economic cycle, $10 to $20 billion would normally be flowing into domestic equity funds" rather than the billions that are flowing out, said Brian K. Reid, chief economist of the investment institute. He added, "This is very unusual." The notion that stocks tend to be safe and profitable investments over time seems to have been dented in much the same way that a decline in home values and in job stability the last few years has altered Americans’ sense of financial security.

It may take many years before it is clear whether this becomes a long-term shift in psychology. After technology and dot-com shares crashed in the early 2000s, for example, investors were quick to re-enter the stock market. Yet bigger economic calamities like the Great Depression affected people’s attitudes toward money for decades. For now, though, mixed economic data is presenting a picture of an economy that is recovering feebly from recession. "For a lot of ordinary people, the economic recovery does not feel real," said Loren Fox, a senior analyst at Strategic Insight, a New York research and data firm. "People are not going to rush toward the stock market on a sustained basis until they feel more confident of employment growth and the sustainability of the economic recovery."

One investor who has restructured his portfolio is Gary Olsen, 51, from Dallas. Over the past four years, he has adjusted the proportion of his investments from 65 percent equities and 35 percent bonds so that the $1.1 million he has invested is now evenly balanced. He had worked as a portfolio liquidity manager for the local Federal Home Loan Bank and retired four years ago. "Like everyone, I lost" during the recent market declines, he said. "I needed to have a more conservative allocation." To be sure, a lot of money is still flowing into the stock market from small investors, pension funds and other big institutional investors. But ordinary investors are reallocating their 401(k) retirement plans, according to Hewitt Associates, a consulting firm that tracks pension plans.

Until two years ago, 70 percent of the money in 401(k) accounts it tracks was invested in stock funds; that proportion fell to 49 percent by the start of 2009 as people rebalanced their portfolios toward bond investments following the financial crisis in the fall of 2008. It is now back at 57 percent, but almost all of that can be attributed to the rising price of stocks in recent years. People are still staying with bonds.

Another force at work is the aging of the baby-boomer generation. As they approach retirement, Americans are shifting some of their investments away from stocks to provide regular guaranteed income for the years when they are no longer working. And the flight from stocks may also be driven by households that are no longer able to tap into home equity for cash and may simply need the money to pay for ordinary expenses.

On Friday, Fidelity Investments reported that a record number of people took so-called hardship withdrawals from their retirement accounts in the second quarter. These are early withdrawals intended to pay for needs like medical expenses. According to the Investment Company Institute, which surveys 4,000 households annually, the appetite for stock market risk among American investors of all ages has been declining steadily since it peaked around 2001, and the change is most pronounced in the under-35 age group.

For a few months at the start of this year, things were looking up for stock market investing. Optimistic about growth, investors were again putting their money into stocks. In March and April, when the stock market rose 8 percent, $8.1 billion flowed into domestic stock mutual funds. But then came a grim reassessment of America’s economic prospects as unemployment remained stubbornly high and private sector job growth refused to take off.

Investors’ nerves were also frayed by the "flash crash" on May 6, when the Dow Jones industrial index fell 600 points in a matter of minutes. The authorities still do not know why. Investors pulled $19.1 billion from domestic equity funds in May, the largest outflow since the height of the financial crisis in October 2008. Over all, investors pulled $151.4 billion out of stock market mutual funds in 2008. But at that time the market was tanking in shocking fashion. The surprise this time around is that Americans are withdrawing money even when share prices are rallying.

The stock market rose 7 percent last month as corporate profits began rebounding, but even that increase was not enough to tempt ordinary investors. Instead, they withdrew $14.67 billion from domestic stock market mutual funds in July, according to the investment institute’s estimates, the third straight month of withdrawals. A big beneficiary has been bond funds, which offer regular fixed interest payments. As investors pulled billions out of stocks, they plowed $185.31 billion into bond mutual funds in the first seven months of this year, and total bond fund investments for the year are on track to approach the record set in 2009.

Charles Biderman, chief executive of TrimTabs, a funds researcher, said it was no wonder people were putting their money in bonds given the dismal performance of equities over the past decade. The Dow Jones industrial average started the decade around 11,500 but closed on Friday at 10,213. "People have lost a lot of money over the last 10 years in the stock market, while there has been a bull market in bonds," he said. "In the financial markets, there is one truism: flow follows performance."

Ross Williams, 59, a community consultant from Grand Rapids, Minn., began to take profits from his stock funds when the market started to recover last year and invested the money in short-term bonds, afraid that stocks would again drop. "We have a very volatile market, so we should be in bonds in case it goes down again," he said. "If the market is moving up, I realized we should be taking this money and putting it into something more safe rather than leaving it at risk."

America no longer needs Chinese money, for now

by Ambrose Evans-Pritchard - Telegraph

As the Sino-American showdown in the South China and Yellow Seas escalates into the gravest superpower clash since the Cold War, the United States cannot wisely rely on China to help fund its budget deficit for any longer.

The cacophony of voices in Beijing questioning or mocking the credit-worthiness of the US is now deafening, from premier Wen Jiabao on down. The results are in any case manifest: US Treasury data show that China has cut its holdings of Treasury debt by roughly $100bn (£65bn) over the past year to $844bn. ZeroHedge reports that net purchases by the big three of China, Japan, and the UK (Mid-East petro-dollars) have been sliding for two years. In August they bought the least amount of US debt this year.

China is finding other ways to recycle its trade surplus and hold down its currency, buying record amounts of Japanese, Korean, Thai, and no doubt Latin American bonds. "Diversification should be the basic principle," said Yu Yongding, an ex-adviser to the Chinese central bank. Beijing is buying gold on the dips, or doing so quietly through purchases of scrap ores, or by deals with miners such as Coeur d'Alene in Alaska.

It is building strategic reserves of oil and coal, and probably industrial metals. State entities are buying up natural gas reserves in Africa and Central Asia, or oil sands in Canada, or timber in Guyana. Where this expansion runs into political barriers, they are funding projects – such as a $10bn loan to Petrobras for the deepwater oil off Brazil. Where all else fails, they are buying equities. All of this recyles China's reserve surplus away from US debt.

So it is a good thing that US citizens have stepped into the breach, investing a record $185bn into bonds funds this year (ICI data). JP Morgan describes this as "extraordinary prejudice", evidence of irrational fear. Or perhaps JP Morgan has an extraordinary prejudice against bonds, arguably the shrewdest asset in a world where fiscal stimulus is being withdrawn before the rest of the economy has reached "escape velocity". The inventory cycle is ebbing, manufacturing has tipped over, the workforce is still shrinking, and the economy is sliding into a deflationary rut.

Above all, bond appetite reflects what David Rosenberg at Gluskin Sheff calls the new frugality. Americans are saving again. Surplus nations are in for a nasty shock if they hope to feed off US demand as if nothing had changed. Yet bond yields have fallen to nose-bleed levels. Ten-year rates are at an all-time low of 2.27 in Germany, and back to 0.92pc in Japan's deflation laboratory. They have slid to 2.6pc in the US.

When yields plumbed these depths over the winter of 2008-2009, latecomers burned their fingers badly. 10-year Treasury yields doubled in five months as the effects of zero Fed rates, quantitative easing, and $2 trillion of fiscal stimulus worldwide halted the downward spiral. This time yields may stay low for longer. Fiscal and interest rate ammo has been exhausted, though not QE. I have little doubt that central banks can lift the West out of debt-deflation if needed with genuine QE – not Ben Bernanke's Black Box "creditism", or Japan's fringe dabbling. Whether they have the nerve or the ideological willingness to do so is another matter.

Does that mean bond yields must keep falling to unimaginable lows, as they have in Japan for twenty years? Perhaps, but Japan is sui generis (captive bond market, vast foreign assets, demographic atrophy), and the world has moved on. As Moody's said this week, the Great Recession has made sovereign debt suspect. "The burden of proof now falls on governments". Events have "fast-forwarded history", ripping away the 20-year cushion we counted on before the "adverse debt dynamics" of our aging crisis hits home.

Two epochal forces are colliding in the global bond market: core deflation is gathering force but the West is losing sovereign credibility just as fast. Arch-bear Albert Edwards at Société Générale advises clients to prepare for a violent policy swing from one extreme to the other. First we deflate into the abyss: then we inflate hard rates to get out again. At some point the "euthanasia of the rentier" will wear off. Misjudge the sequence at your peril.

Facing Budget Gaps, Cities Sell Parking, Airports, Zoo

by Ianthe Jeanne Dugan - Wall Street Journal

Cities and states across the nation are selling and leasing everything from airports to zoos—a fire sale that could help plug budget holes now but worsen their financial woes over the long run. California is looking to shed state office buildings. Milwaukee has proposed selling its water supply; in Chicago and New Haven, Conn., it's parking meters. In Louisiana and Georgia, airports are up for grabs.

About 35 deals now are in the pipeline in the U.S., according to research by Royal Bank of Scotland's RBS Global Banking & Markets. Those assets have a market value of about $45 billion—more than ten times the $4 billion or so two years ago, estimates Dana Levenson, head of infrastructure banking at RBS. Hundreds more deals are being considered, analysts say.

The deals illustrate the increasingly tight financial squeeze gripping communities. Many are using asset sales to balance budgets ravaged by declines in tax revenues and unfunded pensions. In recent congressional testimony, billionaire investor Warren Buffett said he worried about how municipalities will pay for public workers' retirement and health benefits and suggested that the federal government may ultimately be compelled to bail out states.

"Privatization"—selling government-owned property to private corporations and other entities—has been popular for years in Europe, Canada and Australia, where government once owned big chunks of the economy. In many cases, the private takeover of government-controlled industry or services can result in more efficient and profitable operations. On a toll road, for example, a private operator may have more money to pump into repairs and would bear the brunt of losses if drivers used the road less.

While asset sales can create efficiencies, critics say the way these current sales are being handled could hurt communities over the long run. Some properties are being sold at fire-sale prices into a weak market. The deals mean cities are giving up long-term, recurring income streams in exchange for lump-sum payments to plug one-time budget gaps. The deals are threatening credit ratings in some cases and affecting the quality and cost of basic utilities such as electricity and water. Critics say many of the moves are akin to individuals using their retirement plans to pay for immediate needs, instead of planning for the future.

"The deals are part of a broader restructuring of our economy that carries big risks because of revenue losses over time," says Michael Likosky, a professor at New York University who specializes in public finance law. Municipalities argue that the money they raise could help build more long-term assets, boost efficiency and avoid raising taxes. "The City of Los Angeles shouldn't be in the parking business," says Mike Mullen, senior adviser to L.A.'s mayor. Mr. Mullen was hired from Bank of Montreal to study selling some of the city's assets, including parking spaces, which bring in about $20 million annually.

In the U.S., selling public buildings and leasing them back got some attention in the 1980s, but those deals were largely done for tax benefits and the asset generally stayed in public hands. The current deals are fundamentally different because control of the asset transfers to private hands. In such deals, "the private investor takes on operating risk," Mr. Likosky says. In New York's Nassau County, officials last week began seeking buyers for the rights to rent on a former military base called Mitchel Field. The county would still own the 200-acre site, but would get an upfront payment from an investor who would collect the rent payments for up to 30 years—estimated at about $113 million. The county hopes to raise about $20 million to help fill a budget gap.

The most popular deals in the works are metered municipal street and garage parking spaces. One of the first was in Chicago where the city received $1.16 billion in 2008 to allow a consortium led by Morgan Stanley to run more than 36,000 metered parking spaces for 75 years. The city continues to set the rules and rates for the meters and collects parking fines. But the investors keep the revenues, which this year will more than triple the $20 million the city was collecting, according to credit rating firms.

After the deal, some drivers complained about price increases as well as meter malfunctions caused by the overwhelming number of quarters that suddenly were required. Based on the new rates, the inspector general claimed the city was short-changed by about $1 billion. "The investors will make their money back in 20 years and we are stuck for 50 more years making zero dollars," says Scott Waguespack, an alderman who voted against the lease. A spokeswoman for Morgan Stanley declined to comment.

Thomas Lanctot, head of public finance at William Blair & Co., which advised the city on the leasing, says Chicago got a good price. The deal protects the city from economic risks, he said, such as drivers moving to mass transit. "This is not the crown jewels," he says. "This is asphalt." The city said it is investing $100 million of the $1.16 billion in human infrastructure programs like a low-income housing trust fund, ex-offender and other job and social programs. About $1 billion has already been spent on operational expenses such as salaries and sanitation—a fact that came into the equation when Fitch Ratings in early August downgraded Chicago's bond rating to "AA" from "AA-plus."

The downgrade, which could raise borrowing costs, was due partly to Chicago's "accelerated use of reserves to balance operations," Fitch said. Around the country, at least a dozen public parking systems are up for bid, including in San Francisco and Las Vegas. Proponents say private businesses are better at balancing parkers with spaces, advertising and matching prices with demand. Critics claim the sales are garnering too little money, are driving up parking rates and removing a valuable revenue stream. Besides, if a city wants to use a parking lot property for something else years down the road, it can't—the city is typically locked into parking for the lease's life unless it compensates the new operator for the long term revenue loss.

In Pittsburgh, the mayor is proposing to lease out the parking system for an upfront sum of about $300 million over 50 years and funnel the money into the pension system. Bill Peduto, a city councilman, is fighting the plan. The spaces generate $35 million annually, and considering that the concessionaires are proposing doubling rates, he says, the city will ultimately lose $3.5 billion over the life of the lease. "Even with the money from a sale, we'll have to put another $17 million annually into the pension fund—and we don't have that," Mr. Peduto says. He prefers raising parking rates slightly and floating a bond to stabilize the pension fund.

The privatization trend is being spurred by a cottage industry of consultants, lawyers and bankers. Allen & Overy, a New York law firm, dubs it "rescue investing" and recently provided investors a booklet on "jurisdictions of opportunity"—municipalities whose laws, budget woes and credit ratings make them most likely to make deals. "More public-private partnerships for public infrastructure in the U.S. have reached commercial and financial close than during any comparable period in U.S. history," the booklet says.

Many municipalities have long done a poor job of running their roads, parking spaces and bridges, contends David Horner, a lawyer at Allen & Overy. Maintenance contracts, for example, are highly political and with revenues shrinking, infrastructure is increasingly deteriorating. Critics say buyers are taking advantage of municipalities at a vulnerable time and lack the incentive that governments have to maintain quality. Among assets on the block all over the country are state and city office buildings. Arizona received national attention in late 2009—including a skit on the "Daily Show"—when it announced plans to raise more than $1 billion turning over control of public buildings and leasing them back. Much of the money is being used to plug the state's budget hole.

Such "one-time budget maneuvers" were cited in a Moody's Investor Services report recently to downgrade Arizona a notch. "We view these asset sales as 1-shots…that create structural budget imbalances in future years, but that may be necessary actions to bridge the time gap until revenue stabilization or growth returns," says Robert Kurtter, a managing director at Moody's. The California legislature recently released a report by its analyst's office entitled "Should the State Sell its Office Buildings?" California originally bought office buildings to save money, the report says. The cost of leasing them back "would exceed sales revenue," it said, making the sales "poor fiscal policy." But "in the current budget environment," it added, such deals are necessary to balance the budget.

Water supply also is being sold to private interests. In Milwaukee, a consumer advocate called a plan to sell the water system "mortgaging Milwaukee's future." The report, by Washington-based Food and Water Watch, says private water service in general costs 59% more as new owners seek to recoup their investment. It adds: "Water users cannot vote private managers or state-appointed regulators out of office." City Comptroller W. Martin Morics argues that the plan, which is on the back burner, could bring in more than $500 million through a lease over 75 to 99 years.

Airports also are being privatized under a limited federal program. Deals under consideration for lease include airports in New Orleans and Puerto Rico. In Lawrenceville, Ga., residents last month protested against the privatization of Gwinnett County, Ga., airport. Their main concerns were noise and pollution, as a private owner aims to expand it into a commercial airport. The county and a private operator have said that the plan would free up revenues, now reserved for airport use only, for other purposes and create jobs.

Dallas is selling prized outdoor spaces. After turning over operation of the zoo to a private firm, the city is now hawking the Farmers' Market and Fair Park. "It would be part of budget solutions and streamlining operations," says city spokesman Frank Librio, who notes that the city is doing what it can to close a budget gap and replenish reserves.

How States Hide Their Budget Deficits