French Market, New Orleans, N. Peters and Decatur streets

Stoneleigh: Readers have asked us recently for a guide to our primers, encapsulating our worldview in one place.

The first finance article I wrote online, The Resurgence of Risk, appeared at The Oil Drum:Canada in August 2007. It is by far the longest of the primers, and its purpose is to explain in some depth the nature of our credit bubble, the role of 'financial innovation', the distinction between currency inflation and credit hyper-expansion and the mechanism by which value disappears as a bubble deflates.

For further explanation of the ponzi nature of bubbles, the spectrum of ponzi dynamics underlying many economic phenomena and the implications of this for where we are headed see From the Top of the Great Pyramid. This ties in with an earlier piece, Entropy and Empire , detailing the progression of hegemonic power from empire to empire, as each rises, over-reaches, falls and passes the mantle on to its successor.

When bubbles reach their maximum extent, they invariably deflate. Our explanation as to why this is inevitable can be found in Inflation Deflated, followed by The Unbearable Mightiness of Deflation, a rebuttal to inflationist Gary North.

We dispute classical economic theory and the received wisdom as to the nature of markets. Markets are not objective, mechanical and rational as the Efficient Market Hypothesis would have you believe. Our explanation of markets as human phenomena grounded in destabilizing positive feedback can be found in Markets and the Lemming Factor.

We have a number of articles on specific aspects of our current crisis. Our view of real estate can be found in Welcome to the Gingerbread Hotel, War in the Labour Markets covers employment, The Special Relativity of Currencies addresses our view of currency inter-relationships and the value of currency relative to available goods and services, our view of the intersection between peak oil and finance can be found in Energy, Finance and Hegemonic Power , and our view of the future of power systems is explained in Renewable Power? Not in Your Lifetime .

Our predictions for the future in a nutshell are available in point form in 40 Ways to Lose Your Future , and finally our prescription for facing the future is presented in How to Build a Lifeboat . This is our attempt to convey the big picture and what we as individuals can hope to do about it for ourselves, our families and friends. We cannot avoid living through a Greater Depression, we can take action, and, being forewarned, we can avoid many pitfalls. We can avoid becoming part of the herd that is determined to throw itself off a cliff.

Job Cuts Outpace GDP Fall

The job market is doing even worse than the overall economy, prompting concern inside and outside the government that deeper-than-expected joblessness could persist once the recession ends. Breaking from historical patterns, the unemployment rate -- currently at 9.5% -- is one to 1.5 percentage points higher than would be expected under one economic rule of thumb, says Lawrence Summers, President Barack Obama's top economic adviser. Since the recession began in December 2007, the economy has lost 6.5 million jobs, 4.7% of total employment. The unemployment rate has jumped five percentage points, while the economy has contracted by roughly 2.5%.

In recent days, Mr. Summers, White House budget director Peter Orszag and Fed Chairman Ben Bernanke have all talked publicly about the unusual disconnect between growth and employment. Stubborn unemployment could be a political problem for Mr. Obama, who pushed hard for a $787 billion stimulus plan this year and has already been criticized by Republicans for failing to stem the rise in the joblessness. Though today's disparity between growth and jobs is especially stark, a jobless recovery wouldn't be new: The past two recessions were marked by firms reluctant to resume hiring right away after demand recovered.

The current disconnect could reflect an unanticipated surge in productivity -- companies finding ways to increase output with fewer workers. That could set up the economy to grow rapidly in future years. Rising productivity is the linchpin of economic growth and rising living standards. But there are darker scenarios. Struggling workers, whose wages also are being squeezed, could drag a fragile economy back into deep recession. "Final demand and production have shown tentative signs of stabilization," Mr. Bernanke told lawmakers this week as part of the Fed chairman's semiannual report to Congress. "The labor market, however, has continued to weaken."

Job insecurity could lead consumers to further pull back spending, he said, calling it "an important risk to the outlook." The latest data imply productivity is pushing higher. Macroeconomic Advisers, a St. Louis forecaster, estimates productivity grew at a rapid 5% annual rate in the second quarter. While painful for workers who lose jobs, advances in productivity could help get the economy on steadier footing. When productivity rose in the 1990s -- thanks partly to technological advances -- the economy boomed, lifting wages.

Some companies are reaping gains as they clamp down on labor costs. While corporate profits are down from a year ago, many of the biggest companies reporting income figures for the second quarter are ahead of expectations because they have cut costs so aggressively. Caterpillar Inc. this week raised its profit forecast for the year, crediting cost-cutting efforts. The company's second-quarter profits were $371 million, down from $1.106 billion a year earlier, but it said it squeezed operating costs by $4.5 billion from a year earlier. Layoffs and early retirements have reduced its work force this year by 17,100, 15% of the total, and it is instituting "rolling layoffs" in which it has been furloughing workers a few weeks at a time.

"When the economy turns around and demand picks up, we're much better suited to ramp back up because we're not looking at bringing on many new people and getting them up to speed," says Jim Dugan, a Caterpillar spokesman. Kellogg Co. said in May that net income for its first quarter rose 1.3% as cost-cutting offset falling revenue. International Business Machines Corp. said second-quarter profit rose 12% despite falling revenue. The secret: It is cutting costs by $3.5 billion this year.

For now, administration officials are taking a wait-and-see approach, and they insist they have no plans to push new measures to counteract job losses. Officials say the $787 billion economic-stimulus package will have a bigger impact over the next six months. The "two-year program that we put in place was one that had gathering and increasing force over time," Mr. Summers said in an interview. The disparity between the job market and economic growth has other important implications. For Fed officials, it implies that there will be little upward pressure on prices and wages -- in other words, little inflationary pressure -- giving officials reason to hold off on raising interest rates any time soon.

Employers' unusual behavior seems to have intensified as the economy has stabilized. When the government releases its estimate of second-quarter gross domestic product next week, economists expect it will show a contraction of less than 2% at an inflation-adjusted annual rate. During the same three months, employers cut payrolls at an annual rate of more than 4%, eliminating 1.3 million more jobs. That kind of disconnect violates an economic rule of thumb called Okun's Law, after the late economist Arthur Okun, which holds that every two-percentage-point drop in the economic-growth rate corresponds with a one-percentage-point rise in the unemployment rate.

In most downturns since World War II, businesses were slow to reduce their work forces in response to inventory buildups or slowing sales. In the recessions of the early 1990s and the early 2000s, though, businesses moved more quickly to cut early in the downturn and were slow to rehire. "You certainly have the impression that businesses in general have learned to slash payrolls and employment faster than in the past," said Paul Volcker, the former Fed chairman and an economic adviser to Mr. Obama. "There's been a steep decline in business activity without the conventional impact on profits. Somehow, companies have managed to keep productivity higher than you might have thought given economic activity."

U.S. Initial Jobless Claims Rise by 30,000 to 554,000

The number of Americans filing claims for unemployment benefits jumped last week from a six- month low as distortions caused by shifts in the timing of auto- plant shutdowns subsided. Applications rose by 30,000 to 554,000 in the week ended July 18, in line with forecasts, figures from the Labor Department showed today in Washington. Claims had fallen by 93,000 over the previous two weeks. The number of people collecting unemployment insurance decreased to the lowest level in three months, also reflecting seasonal issues surrounding closures at carmakers.

“The numbers have come down but they still have a ways to go down before the bleeding of jobs is over,” said Andrew Gretzinger, a senior economist at MFC Global Investment Management in Toronto, who had forecast 555,000 claims. “The labor market is still weak and is going to remain that for some time to come.” Federal Reserve Chairman Ben S. Bernanke this week said unemployment was the “most pressing issue” facing policy makers aiming to stem the worst recession in five decades. The loss of jobs threatens to undermine consumer spending and represents a “downside risk” to the economy, he said. An analyst at Labor said claims will probably remain volatile for another week.

Economists forecast claims would increase to 557,000 from a previously reported 522,000 for the prior week, according to the median of 44 projections in a Bloomberg News survey. Estimates ranged from 500,000 to 600,000. Stock-index futures advanced as San Jose, California-based EBay Inc. and Dearborn, Michigan-based Ford Motor Co. reported better-than-estimated results and investors speculated a report today may show home resales increased. Futures on the Standard & Poor’s 500 Index rose 0.3 percent to 952.00 at 9 a.m. in New York. The four-week moving average of jobless claims, a less- volatile measure than weekly initial claims, declined to 566,000, the lowest level since January, from 585,000.

The level of continuing claims decreased by 88,000 to 6.23 million in the week ended July 11, the lowest since April, from 6.31 million. The unemployment rate among people eligible for benefits, which tends to track the jobless rate, held at 4.7 percent in the week ended July 11. Forty-one states and territories reported an increase in new claims, while 12 reported a decrease. These data are reported with a one-week lag. Today’s figures coincide with the week the Labor Department conducts its survey for the monthly payrolls report. U.S. employers have eliminated 6.5 million positions since the recession began in December 2007, the most of any downturn since the Great Depression.

Economists surveyed by Bloomberg earlier this month project the jobless rate will exceed 10 percent by early 2010, even as the worst of the job cuts may have passed. Bernanke this week said that while the economy is showing “tentative signs of stabilization” the central bank intends to maintain a “highly accommodative” monetary policy for “an extended period.” “Job insecurity, together with declines in home values and tight credit, is likely to limit gains in consumer spending,” Bernanke said in testimony before Congress. “The possibility that the recent stabilization in household spending will prove transient is an important downside risk to the outlook.”

Air Products & Chemicals Inc., the world’s largest hydrogen producer, yesterday said it will cut more jobs and close more plants to reduce expenses. Chief Executive Officer John McGlade is eliminating an additional 1,150 jobs, or 6 percent of the workforce, as the global recession trims demand. “While we are still seeing the impact of the global recession on our volumes, we’ve seen signs of improvement during this quarter in some of our end markets, particularly in electronics and Asia,” McGlade said in a statement.

Jobless claims tend to be volatile in late June and July, when automakers typically halt production and idle workers to re-equip factories to build new models. General Motors Co. and Chrysler LLC halted production earlier than usual this year as they worked through bankruptcy proceedings. GM emerged from bankruptcy this month and Chrysler did the same in June.

Real Misery Index: Recalculating The Hard Times

The Huffington Post has developed a new feature that aims to provide a more accurate gauge of what is happening in the lives of millions of Americans as a result of the ongoing economic hard times. We're calling it the Real Misery Index The original Misery Index is a formula created by economist Arthur Okun that adds the current unemployment rate to the yearly increase in the consumer price index (a measure of inflation). It's an easily digestible number that the media loves to use to give a snapshot of how well or poorly the economy is doing.

Unfortunately, it's not a very useful statistic. For starters, the unemployment statistic traditionally used represents only a fraction of the jobless since it doesn't include part-time workers and those who have given up looking for work. Moreover, the consumer price index has been criticized for under-emphasizing essential goods such as food and gas. Also, the original Misery Index doesn't include a whole host of economic indicators that have a huge impact on the actual well-being of millions of Americans -- factors like the number of people losing their homes, losing their health care, and going bankrupt or defaulting on their credit cards. The rise in the cost of gas is important -- but what does it matter if you don't have a home to heat or a car to drive?

So, after consulting with experts who study economic trends, and receiving suggestions from many of our readers, we have created the Real Misery Index. It combines a more accurate unemployment statistic (the U6 formulation), with the inflation rate for three essentials (food and beverages, gas, medical costs), and year-over-year percent increases in credit card delinquencies, housing prices, food stamp participation, and home equity loan deficiencies. To formulate our index, we gave equal weight to the broad unemployment numbers and the combination of the other seven metrics. Thus, we added the broad unemployment U6 statistic to the average of the seven other statistics.

In the accompanying chart, we've compared the current recession to previous recessionary periods, including 1990-1991 and the 2000-2001 dot-com collapse. (Unfortunately, since some of the statistics we use for our formulation were not available at the time, we are not able to include 1980, during which the traditional misery index hit an all-time peak of 22.) The traditional Misery Index for the current recession is only 8.1, below the index for the 1991 downturn and barely higher than the 2001 dot-com collapse. But the Real Misery Index for 2009 -- at 29.9 -- is almost three times higher than the index for 2001, showing that the economy is in much worse shape.

We've also included three related charts, which provide additional snapshots of the state of the economy -- year-over-year increases in bank loan delinquencies (which includes credit cards, home equity loans, auto loans), foreclosures and auto repossessions. We've incorporated some suggestions from readers, including foreclosures and credit-card delinquencies. Other great suggestions, such as utility cut-offs and the number of homeless, are not tracked on a national level or are not accurately counted, and could not be included.

HuffPost's Real Misery Index will be updated each month, as soon as the relevant statistics become available. But this remains a work in progress so, by all means, feel free to make recommendations, suggest other statistics and point us in the direction of other useful resources. Send your suggestions to misery@huffingtonpost.com.

Accountants Gain Courage to Stand Up to Bankers

Jonathan Weil

Turns out America’s accounting poobahs have some fight in them after all. Call them crazy, or maybe just brave. The Financial Accounting Standards Board is girding for another brawl with the banking industry over mark-to-market accounting. And this time, it’s the FASB that has come out swinging. It was only last April that the FASB caved to congressional pressure by passing emergency rule changes so that banks and insurance companies could keep long-term losses from crummy debt securities off their income statements.

Now the FASB says it may expand the use of fair-market values on corporate income statements and balance sheets in ways it never has before. Even loans would have to be carried on the balance sheet at fair value, under a preliminary decision reached July 15. The board might decide whether to issue a formal proposal on the matter as soon as next month. “They know they screwed up, and they took action to correct for it,” says Adam Hurwich, a partner at New York investment manager Jupiter Advisors LLC and a member of the FASB’s Investors Technical Advisory Committee. “The more pushback there’s going to be, the more their credibility is going to be established.”

The scope of the FASB’s initiative, which has received almost no attention in the press, is massive. All financial assets would have to be recorded at fair value on the balance sheet each quarter, under the board’s tentative plan. This would mean an end to asset classifications such as held for investment, held to maturity and held for sale, along with their differing balance-sheet treatments. Most loans, for example, probably would be presented on the balance sheet at cost, with a line item below showing accumulated change in fair value, and then a net fair-value figure below that. For lenders, rule changes could mean faster recognition of loan losses, resulting in lower earnings and book values.

The board said financial instruments on the liabilities side of the balance sheet also would have to be recorded at fair-market values, though there could be exceptions for a company’s own debt or a bank’s customer deposits. The FASB’s approach is tougher on banks than the path taken by the London-based International Accounting Standards Board, which last week issued a proposal that would let companies continue carrying many financial assets at historical cost, including loans and debt securities. The two boards are scheduled to meet tomorrow in London to discuss their contrasting plans.

While balance sheets might be simplified, income statements would acquire new complexities. Some gains and losses would count in net income. These would include changes in the values of all equity securities and almost all derivatives. Interest payments, dividends and credit losses would go in net, too, as would realized gains and losses. So would fluctuations in all debt instruments with derivatives embedded in their structures. Other items, including fair-value fluctuations on certain loans and debt securities, would get steered to a section called comprehensive income, which would appear for the first time on the face of the income statement, below net income. Comprehensive income now appears on a company’s equity statement.

Another quirk is that the FASB doesn’t intend to require per-share figures for comprehensive income. Only net income would appear on a per-share basis. My guess is that means Wall Street securities analysts would be less likely to publish quarterly earnings estimates using comprehensive income. Think how the saga at CIT Group Inc. might have unfolded if loans already were being marked at market values. The commercial lender, which is struggling to stay out of bankruptcy, said in a footnote to its last annual report that its loans as of Dec. 31 were worth $8.3 billion less than its balance sheet showed. The difference was greater than CIT’s reported shareholder equity. That tells you the company probably was insolvent months ago, only its book value didn’t show it.

The debate over mark-to-market accounting is an ancient one. Many banks and insurers say market-value estimates often aren’t reliable and create misleading volatility in their numbers. Investors who prefer fair values for financial instruments say they are more useful, especially at providing early warnings of trouble in a company’s business. “It’s been a religious war,” FASB member Marc Siegel said at last week’s board meeting. “And it’s been very, very clear to me that neither side is going to give, in any way.”

So, the board devised a way to let readers of a company’s balance sheet see alternative values for loans and various other financial instruments -- at cost, or fair value -- without having to search through footnotes. At last week’s meeting, FASB member Tom Linsmeier called this a “very useful approach that addresses both sets of those constituents’ concerns.” This will not satisfy the banking lobby, which doesn’t want any significant expansion of fair-value accounting. “I guess the nicest thing I can say is it’s difficult to find the good in this,” Donna Fisher, the American Bankers Association’s tax and accounting director in Washington, told me. If the bankers don’t like it, that’s probably a good sign the FASB is doing something right.

Ignoring Watchdog Report, Treasury Gives Three Major Banks Sweetheart Deals

Four major banks have repurchased warrants from the Treasury Department since a congressional watchdog reported that the backroom deals where the prices were negotiated were ripping off the taxpayer.

In three of the subsequent four transactions, the deals have only gotten worse. The Congressional Oversight Panel report was based on 11 transactions with small banks and concluded that taxpayers walked away with about 66 percent of what they could have gotten. At a hearing on the warrant repurchase program in the House on Wednesday, Herbert Allison Jr., a senior Treasury official, insisted that the sweet deals the banks got were needed to aid the liquidity of the smaller institutions.

The four transactions since then have all been with major institutions. Three of them returned between 54 and 65 percent of what the taxpayer could have gotten on the open market. On June 17th, BB&T agreed to buy back its warrants for $67 million. The bank reported the transaction in a July 17th press release. On July 8th, the Treasury sold warrants back to State Street Corporation for $60 million. On July 15th, Treasury gave up warrants to U.S. Bancorp for $139 million. The latter two transactions are listed by the Treasury in its transactions report for the period ending July 17th.

"We are very pleased to have completed the repurchase of the warrant, effectively concluding U.S. Bancorp's participation in the Capital Purchase Program," said Richard K. Davis, chairman, president and chief executive officer of U.S. Bancorp, when announcing the deal. As well they should be. The warrants that USB bought from the taxpayer for $139 million had a fair market value of $260 million, says an academic who has closely tracked the bailout and the warrant repurchase program.

Linus Wilson is an assistant professor of finance at the University of Louisiana at Lafayette's B. I. Moody III College of Business and he uses essentially the same methodology to calculate fair market value that the Congressional Oversight Panel used -- the Black-Scholes and Merton option pricing models. That methodology is signed off on in the report by Nobel-Prize-winning economist Robert Merton himself. According to Wilson's calculations, the State Street warrants, which paid the taxpayer $60 million, should have brought in $92 million at fair market value. And the value of BB&T's warrants was $114 million, meaning the Treasury left $47 million on the table.

Yet one bank did give the taxpayer a fair shake: Goldman Sachs. Yes, the Goldman Sachs that Rolling Stone reporter Matt Taibbi recently described as "a great vampire squid wrapped around the face of humanity, relentlessly jamming its blood funnel into anything that smells like money." Wilson speculated that Goldman Sachs decided to pay fair price to avoid more of the bad press that's been coming its way the last several months. The bank paid $1.1 billion for its warrants, which Wilson estimates have a fair market value of $1.12 billion based on Tuesday's closing price on shares of Goldman Sachs. Goldman could afford to pay it out, too, considering that it pulled down a $3.4 billion profit in the last quarter and the taxpayer gave it billions by funneling money through AIG to Goldman.

But if the only way the public has of getting full price is to put the history of the bank on the cover of a magazine, then most banks are likely to get better deals. A Treasury official said in a statement to the Huffington Post that the process it uses to determine the price of the warrants is fair: "The warrants for common stock held by Treasury do not trade on any market and therefore do not have observable market prices. Their values can only be estimated. Treasury follows a comprehensive approach to estimating these values, which involves using a variety of inputs including a set of well-known financial models.

These models will include, but will not be limited to, binomial and Black-Scholes option-pricing models, and are widely used in financial markets to value options and warrants. Treasury also relies on indications from market participants as to what they would be willing to pay for the warrants. We obtain quotes from three separate market participants who regularly invest in or trade similar securities. We also retain outside managers to provide full, independent valuations. Together, these various methods constitute a robust process for estimating value and protecting the taxpayers' interests."

The Treasury Department refuses to comment on negotiations until two days after they are completed, giving the public and outside investors no say in the process. Recently, a group of House Democrats began an effort to end the practice and introduced legislation to require the Treasury to hold public auctions. The specific flaw in the Treasury methodology, Wilson told the Huffington Post, is that it doesn't give enough weight to the bank's stock price in its calculation. "Treasury starts out with a very low price [that it offers in negotiations. Banks come back with an even lower price. Banks get a very good deal," said Wilson. "Taxpayers would be better served if the Treasury took an optimistic view of the warrants' value and moved most of them to auction."

But the more general flaw with the Treasury process is a simple lack of transparency. A public auction would "avoid congressional scrutiny and immunize banks and Treasury from any accusations of there being some sort of sweetheart deal," said Wilson. In several instances the banks have been more transparent about the transactions than the Treasury Department. The BB&T transaction has yet to appear on the Treasury report even though the deal was struck on July 17th, as the bank announced. The bank hasn't yet paid for the warrants, so Treasury won't comment on it. JPMorgan Chase & Co. has reportedly asked the Treasury to hold a public auction, unhappy with Treasury's offer. We know that because JPMorgan said so publicly, but a Treasury spokeswoman wouldn't confirm it, saying the department doesn't comment until two days after the transaction is complete.

The JPMorgan case is telling. Since Treasury has so far set the bar so low for the warrant repurchases, banks that are just now entering negotiations don't want to pay more than the nice deal the last guy got. Selling the warrants at auction would put an end to the game. There's still time, noted the oversight panel, chaired by Harvard Prof. Elizabeth Warren, stating that "the process is still at an early enough stage that the maximum benefit for the taxpayer could be realized if the open market process is enacted now." But the longer they wait, the more taxpayer money is left on the table. Treasury shows no signs of changing on its own. Rep. Mary Jo Kilroy (D-Ohio) hopes she can force it to with her House bill. "Other investors would want to get a return on their investment," she said. "There's no reason taxpayers shouldn't."

WATCH Kilroy challenge Treasury on the warrant deals:

Home Resales in U.S. Increased More Than Forecast

Home resales in the U.S. rose in June for a third consecutive month, spurred by tax incentives, lower borrowing costs and foreclosure-driven declines in prices. Purchases climbed 3.6 percent to an annual rate of 4.89 million, stronger than forecast and the highest level since October, the National Association of Realtors said today in Washington. Median prices fell 15 percent. The gain in sales confirms Federal Reserve Chairman Ben S. Bernanke’s remarks this week that the worst housing slump in eight decades appears to be moderating. A record drop in household wealth, due in part to the plunge in property values, and mounting unemployment are among the reasons rebounds in housing and the economy are likely to be drawn out.

“We have finally bottomed out,” said Stuart Hoffman, chief economist at PNC Financial Services Group in Pittsburgh. Improved affordability “is stalemating the drag from higher unemployment.” Hoffman forecast sales would rise to a 4.9 million pace. Economists forecast existing sales would rise to a 4.84 million rate from a previously reported 4.77 million for May, according to the median of 68 projections in a Bloomberg News survey. Estimates ranged from 4.7 million to 5 million.

The Labor Department earlier today reported that first-time applications for jobless benefits climbed by 30,000 to 554,000 in the week ended July 18. The number of workers filing claims had dropped by 93,000 over the previous two weeks, reflecting changes in the timing of mid-year auto shutdowns to retool for the new-model year. Stocks gained and Treasury securities fell after the report. The Standard & Poor’s 500 index rose 1.4 percent to 967.67 at 10:21 a.m. in New York.

June traditionally is one of the top sales months of the year as families prepare to move before the start of the next school term, according to the NAR. The group adjusts the figures for these seasonal variations in order to facilitate month-to- month comparisons. Sales were down 0.2 percent compared with a year earlier. The gain last month was based by a 14 percent jump in purchases of condominiums. Sales of single-family houses increased 2.4 percent and were up 0.2 percent from June 2008, the first year-over-year gain since September.

The number of houses on the market fell 0.7 percent to 3.82 million in June, NAR said. At the current sales pace, it would take 9.4 months to sell those homes, compared with 9.8 months in May. A 7 months supply is usually consistent with stabilization in prices, NAR chief economist Lawrence Yun, said in a press conference. It may take until the end of this year or early 2010 before property values steady, he said. The median price of an existing home fell to $181,800 from $215,000 a year earlier, the NAR said.

Existing sales reached a 4.49 million pace in January, their lowest level since comparable records began in 1999. The median price reached a six-year low the same month, extending the decline from July 2006’s record to 28 percent. Mounting foreclosures have accelerated the drop in prices. More than 1.5 million homeowners had their homes seized by banks or received default or auction notices in the first half of the year, a 15 percent increase from a year earlier and a record, Irvine, California-based RealtyTrac Inc. said July 16.

The share of homes sold as foreclosures or otherwise distressed properties fell to 31 percent last month, Yun said. The share is “declining measurably” from the 45 percent to 50 percent level seen earlier this year, he said. Falling property values have both helped and hurt demand. Some Americans who owe more on their mortgages than their homes are worth can’t sell their properties to trade up or to move to areas of the country where more jobs are available.

Seeking to stem the slump in sales and lower borrowing costs, Fed policy makers committed to a $1.25 trillion program to purchase securities backed by home loans. Those purchases, as well as direct government purchases of Treasuries, drove rates on 30-year mortgages to a record low 4.78 percent in April, according to figures from Freddie Mac. Rates have since gravitated above 5 percent. In addition, the Obama administration’s stimulus plan provided an $8,000 tax credit for first-time home buyers for purchases completed before Dec. 1.

Growing joblessness may be diluting the effectiveness of these government efforts. With unemployment at a quarter-century high of 9.5 percent and forecast to rise further, more Americans may not be willing to make big-ticket purchases. Banks have also made it harder to obtain loans for those without good credit. Wells Fargo & Co., the biggest U.S. home lender, yesterday said bad loans jumped in the second quarter as the recession made it harder for borrowers to keep up with payments. Assets no longer collecting interest climbed 45 percent as of June 30 from the first quarter, the San Francisco-based bank said. Chief Financial Officer Howard Atkins said in an interview nonaccrual loans from its acquisition of Wachovia Corp. will moderate in the coming quarters.

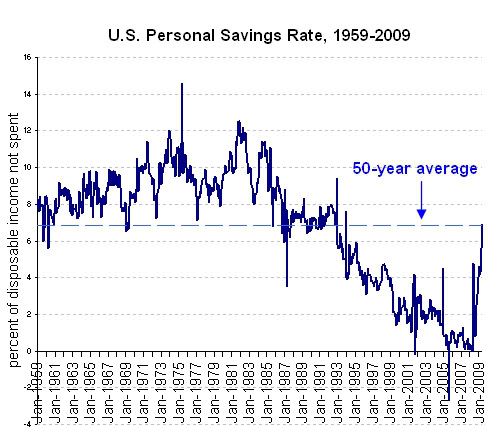

Americans not making money, much less saving it

The news out today told a story of Americans going back to their puritan fiscal roots.Americans Pay Back Debts Most Since ‘52 as Jobless Spur Savings(Bloomberg) -- For the first time since Harry S. Truman was in the White House, Americans are paying back their debts, a phenomenon that just might help keep interest rates low as the Treasury sells a record $2 trillion of bonds and rising unemployment increases U.S. savings.

The stable rock of the American citizen, repairing his balance sheet so that the Great American Economy can recharge with a clean slate, healthy and ready to take on the world. American Capitalism in action, continuing to work in the same way it has worked for hundreds of years.

At least that is what the first paragraph implies. Once you scratch the surface the story isn't nearly so pretty.

For instance, let's look at the second paragraph of this story.

While the proportion of consumers without jobs rose to 9.5 percent last month, household borrowing fell to 128 percent of the average family’s after-tax income in the first quarter from a record 133 percent in the same period a year earlier, according to data compiled by Bloomberg. The total debt of individuals, nonfinancial companies and federal, state and local governments grew at a 4.3 percent pace at the start of the year, down from a peak of 9.9 percent in the fourth quarter of 2005, Goldman Sachs Group Inc. estimated.Uh, if total debt is increasing then how is the country supposedly paying down its debts?

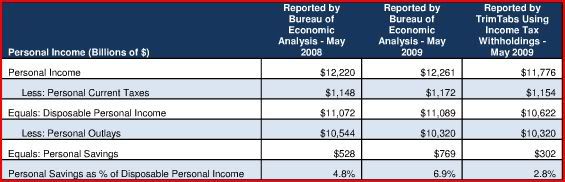

Let's ignore that question for now, and look deeper at the Commerce Department numbers. Their claim is that the savings rate is 6.9% in May, the highest since 1993.

It sounds impressive until you put it into perspective, by looking at where we are coming from. For instance, in 2007 Americans saved $57.4 Billion. At the same time they gambled away $92.3 Billion. That's a far cry from our puritan roots.

Americans are being forced to save now because their net worth has taken a brutal double-punch from the housing bubble bust and stock market crash.

But have Americans really started saving at a 6.9% rate? Let's look at how the Commerce Department puts together their numbers.The Commerce Department measures total personal income, then deducts personal spending to arrive at what was saved.

...

That's what happened in May: One-time federal stimulus payments of $250 each to retirees and others receiving government aid -- so-called transfer income -- drove total personal income up 1.4% from April, while spending rose a modest 0.3%.That boosted what the government calculates was left in people's pockets. Savings as a percentage of total disposable income jumped to 6.9% from 5.6% in April.

That one-time event merely moved private debt to public debt. The debt didn't actually get paid off.

Of course that isn't the only way that the numbers are skewed.

Trimtabs broke the numbers down to more basic elements.Our analysis based on real-time income tax deposits indicates the real savings rate is a paltry 0.9%. Consumers are in much worse shape than government statistics suggest and have little money left over to repair their tattered balance sheets.Trimtabs attacks the Commerce Department's most basic assumptions about wages and salaries.

the BEA is overstating income from wages and salaries and income from non-wage sources, which inflates the savings rate. Income tax deposits to the U.S. Treasury, which are reported in the Daily Treasury Statement (DTS), show the economy is contracting much faster than the BEA is reporting. Using this real-time data, we estimate the savings rate was only 2.8% in May.Trimtabs also subtracts both the short-term "Make Work Pay" tax credit, and the $250 one-time stimulus payment earlier this year, thus we arrive at a 0.9% savings rate.

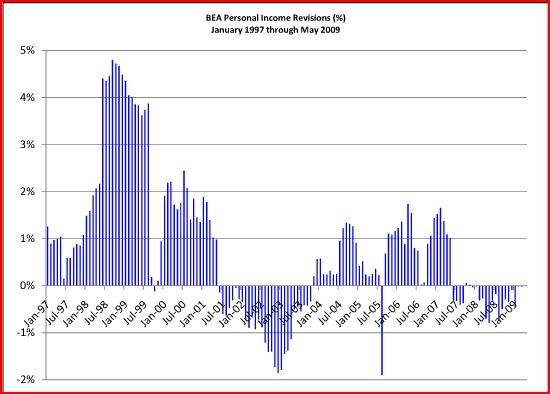

Trimtabs criticizes the BEA for using the Quarterly Census of Employment and Wages (QCEW), which is based on quarterly tax reports. The problem being that many employers pay unemployment taxes on only a small portion of their workers' salaries, and many of these payments are made at the beginning of the year.

Using the DTS instead of the QCEW, personal income would have fallen 3.6% y-o-y in May, rather than the 0.3% that the BEA reported.That's not to say that the BEA doesn't go back and revise their reports so they are more accurate. They just do after the numbers no longer have much meaning.

Once you look at real-time data, rather than BEA projections based on past quarterly data, the Green Shoots numbers wither and die.

Forecasts of positive economic growth by Q4 2009 are wishful thinking. Our real-time indicators show declines in wages and salaries are accelerating. Adjusting for the “Making Work Pay” tax credit, wages plunged 6.2% y-o-y in the past four weeks, worse than the 4.8% y-o-y decline in May and the 5.8% y-o-y decline in June.

...

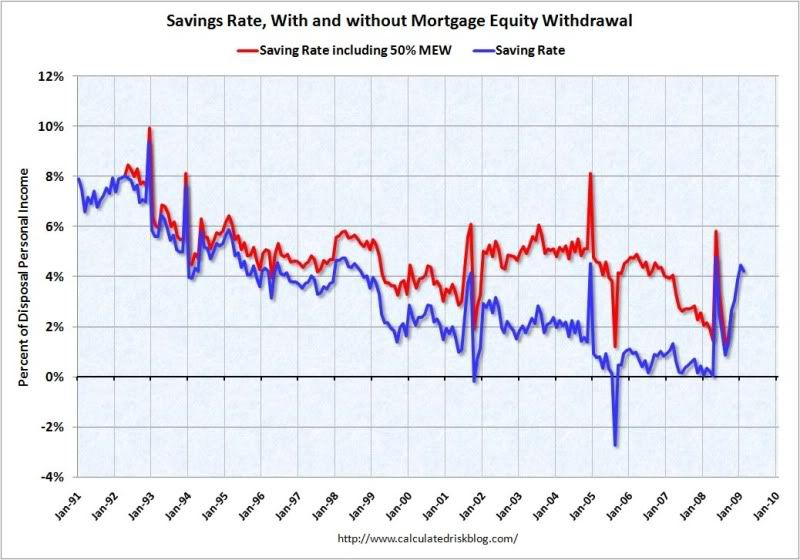

July 4 was on Saturday this year and on Friday last year. Even with the boost from this additional withholding day, withholdings fell an adjusted 6.2% y-o-y in the past four weeks. “Other” taxes plunged 32.7% y-o-y in the past four weeks after falling 35.6% y-o-y in Q2 2009. Corporate income taxes fell 32.2% y-o-y in the past four weeks after dropping 36.7% y-o-y in Q2 2009. Incomes are dropping much faster than government statistics are measuring.So why do BEA numbers showing a phantom, rising savings rate? The reason is largely due to the bursting of the housing bubble, which has cut off home equity withdraws.

$150 Billion of Assets May Return to BofA’s Balance Sheet in 2010

Bank of America may soon bring some $150bn of off-balance-sheet assets back onto its balance in Q110 with the implementation of a new accounting rule, FAS 167, potentially pressuring its capital reserves.

Of the assets the bank says it may bring to its balance sheet, home equity conduits account for an estimated $12bn, while card securitizations account for $85bn, and other variable interest entities make up the remaining $53bn, according to an equity research note by Keefe, Bruyette & Woods‘ (KBW) Jefferson Harralson.

“BAC will need to reserve for the lion’s share of these loans, but according to BAC, the accounting standards dictate that the reserving will come in the form of a capital adjustment rather than through the P/L (profit and loss),” Harralson noted in the research piece. Based on an estimated 11% annualized loss rate on the card book and 4% for the remaining loans coming onto the balance sheet, KBW estimates a capital adjustment of $7.9bn, or $0.91 per share, is needed. The firm said this estimate could be conservative if the Financial Accounting Standards Board (FASB) phases in the reserve requirements over time with the implementation of FAS 167 and if the reserve methodologies use less-than-peak expected loss rates.

Financial Accounting Standards (FAS) Statement 167 pertains to securitizations and special purpose entities, according to FASB. “Statement 167 will require a company to provide additional disclosures about its involvement with variable interest entities and any significant changes in risk exposure due to that involvement,” the Board said in a recent statement. “A company will be required to disclose how its involvement with a variable interest entity affects the company’s financial statements.”

Existing-Home Sales Rise; Prices Fall

Existing-home sales rose again in June from the previous month, but prices are still down sharply compared with last year. Home resales rose more than expected, by 3.6%, to a 4.89 million annual rate from a revised 4.72 million in May, the National Association of Realtors said Thursday. The NAR originally reported May sales up 2.4% to 4.77 million. Wall Street expected a sales rate of 4.85 million sales rate for previously owned homes.

Foreclosures and short sales reflect 31% of sales in June. Distressed property sales have pushed prices lower, year over year. The median price for an existing home last month was $181,800, a 15.4% decrease from June 2008. The average 30-year mortgage rate rose to 5.42% in June from 4.86% in May, Freddie Mac data show. Tighter credit and rising unemployment are also reducing sales. Previously owned home sales, year-over-year, were down 0.2% from the pace in June 2008, Thursday report said.

Weak demand has kept inventories of unsold homes high. Inventories of previously owned homes fell 0.7% at the end of June to 3.82 million available for sale. That represented a 9.4-month supply at the current sales pace, compared to 9.8 in May. Excess supply is depressing prices. Regionally, sales in June compared to May grew 2.5% in the Northeast, 4.0% in the South, 6.4% in the West, and 0.9% in the Midwest. Separately, the number of U.S. workers filing new claims for state jobless benefits began climbing back up last week, confirming that the dramatic declines reported earlier this month weren't necessarily signs of an economic revival.

Initial claims for jobless benefits rose by 30,000 to 554,000 on a seasonally adjusted basis in the week ended July 18, the Labor Department said Thursday. The four-week average of new claims, which aims to smooth volatility in the data, fell by 19,000 to 566,000, the lowest level since Jan. 24. The tally of continuing claims -- those drawn by workers for more than one week -- fell by 88,000 during the week ended July 11 to 6,225,000, the lowest level since April 11..

Real Estate: Commercial and Residential Prices

Here is a comparison of the Moody's / Real Capital Analytics CRE price index and the Case-Shiller composite 20 index.

Notes: Beware of the "Real" in the title - this index is not inflation adjusted - that is the name of the company (an unfortunate choice for a price index). Moody's CRE price index is a repeat sales index like Case-Shiller.Click on graph for larger image in new window.

CRE prices only go back to December 2000.

The Case-Shiller Composite 20 residential index is in blue (with Dec 2000 set to 1.0 to line up the indexes).

This shows residential leading CRE (although we usually talk about residential investment leading CRE investment, but in this case also for prices), and this also shows that prices tend to fall faster for CRE than for residential.

There has been some discussion recently of the “de-stickification” of house prices in areas of heavy foreclosure activity. Price behavior for foreclosure resales is probably similar to CRE because there is no emotional attachment to the property. But prices in bubble areas like coastal California, with little foreclosure activity, will probably exhibit more stickiness and decline, in real terms, over a longer period than the high foreclosure areas.

Jon Stewart Is America's Most Trusted Newsman

Well, in a result that he will probably accept as downright apocalyptic for America, The Daily Show's Jon Stewart has been selected, in an online poll conducted by Time Magazine, as America's Most Trusted Newscaster, post-Cronkite. Matched up against Brian Williams, Katie Couric and Charlie Gibson, Stewart prevailed with 44 percent of the vote. Now, if we're being honest, he probably managed to prevail as the winner precisely because he was the odd man out in a field of network news anchors. Nevertheless, I think Jim Cramer should feel free to SNACK ON THAT.

Brian Williams drew the second largest percentage of votes, with 29 percent. Gibson and Couric finished third and fourth, respectively, with 19 and 7 percent of the vote. Time has helpfully broken out the results, state-by-state, so if you want to muse on some anomalous results, feel free. Brian Williams won Arizona, Wyoming, Nebraska, North Dakota, Florida, South Carolina, Indiana, Delaware and Vermont, and tied in Kentucky and Alaska. Charlie Gibson was big in Tennessee and Montana. Katie Couric pulled off the Mondalian feat of winning one state: Iowa. Stewart finished no lower than second place in all states, except, curiously, Vermont.Click here for interactive chart

Take the red pill, Mr. President

"If there's a blue pill and a red pill, and the blue pill is half the price of the red pill and works just as well, why not pay half price for the thing that's going to make you well?" -- President Obama

In last night's press conference, President Obama seemed to be reliving that famous scene from The Matrix. The main character is offered a choice between a red pill that makes him see reality for what it is, and a blue pill that allows him to continue living in a pleasant world of illusions. Last night, President Obama appeared to have taken the blue pill before his press conference.

How else could he convince himself, the Congressional Budget Office's numbers notwithstanding, that his health care reform bill will not increase both health care costs and the federal deficit? How else can he continue to make the argument that a massive expansion of government spending on health care will solve rather than exacerbate the current problems? How can he repeatedly express such absolute certainty that such a measure will easily pay for itself several times over in the long run? Why can he not at least acknowledge the possibility that it will become a costly and useless trillion-dollar boondoggle that follows in the footsteps of his stimulus package?

With his example of the red and blue pills, and another about whether a child's hypothetical tonsils should be removed, President Obama unwittingly presents the real problem with his plan for reform. Here is a well-meaning government official who so fails to grasp the problem in health care that he can present such absurd oversimplifications and suggest that this sort of thing is the real problem -- doctors simply lack the common sense to make obvious medical decisions.

President Obama wants us to solve this problem by putting himself and other government officials in charge of rescuing medicine from the medical profession. If medical doctors with a decade of schooling cannot distinguish between good cures and ineffective ones that must be discontinued, then by gosh, we're lucky that the good folks from the government can. President Obama thus frames the issue as a false choice between doing nothing at all and handing over to Washington complicated, case-by-case medical decisions that cannot possibly be legislated or dictated by government.

This transfer of medical authority to the bureaucracy is intended to curb costs. Unfortunately, there is exactly one thing that government can do to control costs in health care: it can insist on paying below cost. This shifts the cost burden to private insurance companies, which in turn pass along higher premiums to their patients. This is what government-run Medicare does today for many treatments, including cancer. Government will do more of this kind of "saving" when it assumes greater responsibility for funding citizens' health care, particularly if a government-option health care plan is established.

The Mayo Clinic which President Obama praised in his speech last night is the same Mayo Clinic whose president signed onto a letter to Congress yesterday, expressing fears that a government-option health care plan Obama wants to establish will do more of this cost-shifting. The letter states:Under the current Medicare system, a majority of doctors and hospitals that care for Medicare patients are paid substantially less than it costs to treat them. Many providers are therefore already approaching a point where they can not afford to see Medicare patients. Expansion of a Medicare-type plan without a method to define, measure, and pay for healthy outcomes for patients will move many doctors and hospitals across this threshold, and ultimately hurt the patients who seek our care. We should not put more Americans into the current unsustainable system.

President Obama brushed off this concern last night near the end of his press conference, citing a hopeful but very vague blog post on Mayo's website that went up a day before the letter was sent. In addition to ignoring budgetary and medical concerns, he repeated his dubious promise that his plan will not force millions of Americans out of health insurance plans they already have and like. He had no comforting words to convince anyone of the wisdom of creating two new taxes on employers -- one of them a tax that punishes small businesses with a higher tax rate if they create more jobs -- in the middle of a recession.

The one thing President Obama did not do last night was address directly any of the concerns that Americans have about his pending reform proposals. With this sort of rhetorical detachment from reality, it is not surprising that public support for his vision of health care reform is gradually eroding. President Obama needs to take the red pill, even if it does cost twice as much.

Recession over, recovery ‘nascent,' Canada's central bank says

Canada's recession is over, and the country is beginning what will be a long reconstruction of the wealth destroyed by the financial crisis, the central bank said Thursday. Gross Domestic Product will expand at an annual rate of 1.3 per cent this quarter, compared with an earlier forecast for a contraction of 1 per cent between July and September, the Bank of Canada said in its latest monetary policy report. The dramatic shift is the result of stronger financial conditions, surprisingly high consumer and business confidence and a first-half contraction that was less severe than the economic catastrophe the central bank was bracing for when it last published its views on the economy in April.

If the Bank of Canada's new forecast proves correct, Canada's first recession since the early 1990's lasted three quarters, making it one of the shortest downturns on record. Short, but severe. Canada's economy was operating about 3.5 per cent below its production capacity, a hole that will take well into 2011 to fill, the central bank said. The automotive and forestry industries are restructuring, business investment is weak and unemployment continues to rise. All that will make the recovery fragile, and explains why the central bank recommitted Tuesday to keep the benchmark lending rate at a record low of 0.25 per cent until the middle of next year.

“The recovery is nascent,” the Bank of Canada said. “Effective and resolute policy implementation remains critical to sustained global growth.” The Bank of Canada's revisions are based on a domestic economy that has weathered the global recession better than policy makers expected and confidence that the rebounds in the United States and China are about to give a lift to exporters and commodity prices. In April, the central bank predicted the economy would collapse by 7.3 per cent in the first quarter, a reading that instead came in as a 5.4 per cent contraction. The former would have been the worst on record; the later is the biggest decline since the recession of the early 1990s.

“With the reiteration of the conditional commitment to keep rates unchanged, it seems like the compass continues to point to a slow, but eventual recovery,” said TD senior economics strategist Charmaine Buskas. The central bank left its second-quarter outlook unchanged, predicting GDP shrank 3.5 per cent between April and June. Consumer spending likely increased in the period, bringing forward purchases that policy makers originally assumed would occur later this year or even next, the report said. Household credit has remained surprisingly high, reflecting the central bank's efforts to lower borrowing costs to encourage purchases of houses and other big ticket items.

Over the months ahead, the Bank of Canada is counting on exporters to take over for consumers. The U.S. economy is “at its trough,” and Canadian exporters will benefit disproportionately from the rebound because of their tight trade links with the world's largest economy, the Bank of Canada said. China's growth also is remarkably strong, which will provide a boost to commodity prices, the report said. Still, risks remain. The biggest threat to the Bank of Canada's outlook is the dollar, which has surged more than 5 per cent this month, jumping over 90 U.S. cents.

Policy makers worry about persistent strength in the currency because it makes Canadian exports less competitive abroad. The central bank's forecast for economic growth of 3 per cent in 2010 and 3.5 per cent in 2011 is based on an assumption that the loonie's value will average 87 cents over that period. “A stronger and more volatile Canadian dollar could act as a significant drag on growth and put additional downward pressure on inflation,” the report said.

The central bank is mandated by law to keep inflation advancing at a pace of about 2 per cent a year. The Bank of Canada's inflation outlook remains largely unchanged from April. Policy makers predict the consumer price index declined in the second quarter, will drop 0.7 per cent this quarter and eventually reach 2 per cent in the second quarter of 2011. Financial conditions also could take longer to return to normal, since unexpected losses at financial institutions could trigger another crisis of confidence in credit markets or bond traders could demand higher yields because of concern over rising budget deficits, the report said. “Fragility in the global economy persists,” the central bank said. “Financial deleveraging by banks, households and firms is continuing, mirrored by ongoing adjustments on the real side of the economy.”

Bruce Power pulls plug on two planned nuclear stations

Bruce Power has pulled the plug on its ambitious plans to construct two new nuclear stations in Ontario. The company says the stations, which it had hoped to build at Nanticoke on Lake Erie and at its existing nuclear complex near Port Elgin on Lake Huron, are no longer needed because of plunging electricity demand in the province. The cancellations follow a similar decision late last month by the Ontario government to shelve a plan to build a new nuclear plant. The province cited the high costs of constructing the station as part of the reason for its decision.

Bruce Power currently operates two nuclear stations it is leasing from the Ontario government at the Port Elgin site. In a statement, the company said it will focus on refurbishing reactors at these stations rather than embarking on new construction. The decision will have no impact on the company's interest in building new atomic stations in Alberta or Saskatchewan. Both provinces are expected to issue policy statements on nuclear power later this year, according to the company.

“These are business decisions unique to Ontario and reflect the current realities of the market,” said Duncan Hawthorne, Bruce Power's president. “For more than five years, we've examined our options and refurbishing our existing units has emerged as the most economical.” Bruce Power says it has notified the Canadian Nuclear Safety Commission and the Canadian Environmental Assessment Agency that it will withdraw its site license applications and suspend its environmental assessments in Bruce County and Nanticoke.

Mr. Hawthorne said its research indicated both sites “held great promise for new build if the market conditions were more favourable” but the company has to take actions that were “ best for us, for Ontario and its ratepayers.” There have been hopes among nuclear energy proponents that interest in atomic power was about to undergo a revival, after worries over the Three Mile and Chernobyl accidents caused construction of new plants to cease in North America for the past two decades.

But recently, some of that optimism has faded. Besides the cancellations in Ontario, major utilities in the U.S., including Entergy Corp. and Exelon Corp., have temporarily suspended some of their plans for new nuclear power plants. And last month, Moody's Investors Service, a credit rating firm, warned that it was considering taking a more negative view on utilities considering new nuclear stations. Shawn-Patrick Stensil, a spokesman for Greenpeace, said the rapidly escalating price tag on new nuclear plants is undermining investor confidence in the technology. He contend that cost worries prompted Bruce Power to cancel its Ontario projects because it often takes 10 years or more to build a new plant and utilities normally don't cancel plans because a recession temporarily cuts electricity use.

“I think they're using that as an excuse,” Mr. Stensil said, who said he doubts that Bruce would “would be able to convince private investors to take on that kind of risk” that comes from building two new plants. But Murray Elston, Bruce Power's vice-president corporate affairs, rejected the claim, saying that “it really is the fact that right now the capacity of our system to generate is well beyond what our demand is.” He said the company had not yet sought pricing details for the two new plants.

The real estate roots of the crisis in the US

by Elena Panaritis

Two years after it began, there is now a coalescing of opinion about the causes of the U.S. financial crisis and what should be done to resolve it, yet there is a serious element missing both in the causation analysis as well as in the prescriptive solution. This crisis, which has infected the global economy so severely, is very much a non-traditional one that calls for a non-traditional solution.

The impact in the United States so far has been worse than anything since the Great Depression: unemployment reached 9.5 percent in June, up from 7.8 percent in January, home prices were down 27% at the end of the first quarter from their 2006 peak, and 1.5 million homes were in foreclosure. After jumping by 30 percent in February, home foreclosure rates tapered off but are again on the rise. According to the New York Times, the loss in property value could total $500 billion.

There is general agreement that the financial crisis results from a variety of factors: an extremely low household saving rate in the United States; excessive public and private liquidity creation and a wave of cheap and easy credit which was directed into real estate speculation; proliferation of “subprime” mortgage loans to high-risk borrowers, interest rates kept too low for too long that further increased incentives to over-borrow; the failure of financial supervision and regulation.

However, there is a much less obvious element that everybody is missing, that of a poorly defined and weak underlying asset namely real estate/property. Indeed, it is at the heart of the crisis. A chain is only as strong as its weakest link and the weak link here is the system used to define the asset of real estate/property in terms of use and cash flow, its supply, and pricing. In this crisis, real estate assets were badly defined for the most part, making them less securely bankable and more susceptible to price manipulation and destabilizing speculation. That’s still true, yet no one is raising the issue.

Usually, economic crises result from bad regulation and over-liquidity in the financial markets (the first four of the five factors mentioned above). Economists usually address the demand side of the assets (i.e. how an asset is financed and the credit markets around it) (as opposed to the actual regulatory infrastructure that defines and creates assets to become securely tradable with reduced risk, that is, the supply side. In this crisis, the asset (real estate) was/is for the most part badly defined - and it is this side of the equation that needs to be examined rather than taken for granted.

The current economic crisis stems from the fact that the underpinnings of the market are either broken or rotted, and in some cases there are no underpinnings. That makes it a non-traditional crisis; what we are confronting is the direct result of inadequacies in upstream property rights. This crisis combines the original sin of badly valued properties with a financial system based on harmful, unproductive gambling and incentives to continue gambling. As a result, investors in mortgage-backed securities did not have enough, reliable information on the mortgage itself. They only had information on ratings of the derivative, but not of the actual underlying asset.

We cannot achieve secure derivative trading if the information on the underpinning asset is not standardized but oblique and difficult to find - because markets run on information. In the same way we understand the need to standardize derivatives, we must understand the need to do the same for the underlying real estate assets. While we have national and international trading in asset-based securities, the information on the assets themselves is localized, and the way it is collected and reported varies from county to county and state to state.

What, then, should be done? We need to treat this crisis as an opportunity not only to install a more rigorous regulatory regime for the financial sector, but also to listen to the non-traditional economists - that is practitioners of institutional economics. They will tell us that we need to overhaul the way property rights and property values are established in this country. We need a structural reform that establishes standards for how property is evaluated and how it is offered to the market.

We need a standardized repository of information about the asset of property, so that no one has to search multiple places to make sure a title is good and that there are no outstanding liens dating back decades. We need to ensure that all buyers can access information about the pricing of property. Let’s start with a consolidation of information county by county, and use the best standardized information we can find - typically from registries of deeds and from title insurance companies - to get things going.

The U.S. property rights system is severely broken. The incorrect valuation of land, properties, and thus mortgages is at the center of our current crisis, and if we don’t fix things so that mortgages are valued correctly we will not have addressed the root cause of why things are the way they are today. Traditionally, economists are trained to assume that pricing in general is a point of equilibrium defined by almost perfect market forces, where the demand and supply meet and neither the buyer or seller has a huge informational advantage. The traditional model also assumes that markets are frictionless and transaction costs are near zero especially when we deal with the supply side.

From that they continue to assume that systems (rules, regulations, norms) that define the tradability of assets are given and near perfect. But this is rarely the case. In reality the systems that define supply of land and real estate tend to be full of transactions costs and information leakages, and that makes it really difficult to follow the old maxim that a price or value based on how much one is willing to pay is necessarily the right price.

These are the same economists who, faced with a crisis, would concentrate on the downstream usage of an asset - that is, the asset’s treatment in the financial markets. They would typically pay little or no attention to the upstream definition of the asset - that is, the actual system that structures the supply of the asset - the pool of all assets ready to be traded in the market - before it enters the market.

Their solutions would be all the traditional ones, that is, solutions that touch on the impacts of distorted financial markets, that is, markets for ‘downstream’ financial assets: macroeconomic stability, regulation of the financial sector, even labor regulations, and by taking these steps, they would consider transactions costs to be close to zero, and disregard societal and market wrinkles.

What about practitioners of institutional economics? They would emphasize how the underlying asset is defined, whether all the characteristics that help determine its market price are clear, and how the original creation of the asset takes place. And so, to whom do the powers-that-be turn for solutions in this non-traditional crisis? They are following the lead of the traditional economists and the conventional path of economic analysis.

The Obama administration’s economics team came in determined to get a handle on this crisis. There has been a concerted effort to lift the fog and manage as much as possible the systemic risk that has been created by panic over a suddenly uncertain future. The team has focused on policies to reduce uncertainty about the derivatives markets and restore confidence, to return banks to healthy levels of capital and bring tighter oversight to the derivatives markets.

These steps are needed, but they are not enough. Everyone has pointed to the greed of the financial sector, the manic behavior of banks and new lending institutions that continued to leverage up to take advantage of the spreads between their securitized assets and their ever-shorter funding maturities, the lax regulation of the derivatives markets, and the fact that almost anything could be bundled with anything else, no matter how heterogeneous - one security could include consumer debt, credit cards and home mortgages. Also there is a wide acknowledgment that when banks stop lending it both brings about a cyclical contraction and fuels a weakening of long-term productivity in any economy.

But is it enough simply to reduce uncertainty regarding the capitalization of banks? Does lifting the fog of uncertainty about the complex derivatives also cure the core problem? No one is touching the roots of the crisis. When Timothy Geithner, US Treasury Secretary, is asked about the signs of improvement, he points to impacts of the systemic crisis, such as unemployment, lending rates, and so on. He has yet to point to a single indicator that goes to the roots.

Where is his explanation of what is being done to address the bad rules and regulations governing how property rights in real estate are established in the United States, which is the primary reason that all the systemic problems could bring us down the path to negative-equity mortgage loans? What does he have to say about long-term miscalculations of the value of mortgages on an asset - real property - that ought to be unambiguous and transparent in our market economy? What is going to be done to ensure that land valuations are not driven by guesswork?

Until the United States accepts that it has a badly flawed approach to establishing and verifying real estate property rights and to determining the valuation of property, until it puts in place a system that homogenizes and standardizes the underlying securitized assets of real estate and housing - the same way securities are required to be homogeneous prior to being traded in bundles - these underlying real estate assets will continue to be toxic. They may be less toxic, or more toxic, as the crisis ebbs and flows, but they will be toxic nonetheless - and they will be on the balance sheets of banks.

Let the traditional economists work on the things they understand. Meanwhile, let’s combine basic institutional economics with some practical reality and fix the broken system. It will take political will, strong leadership from a new and popular president, and a direct confrontation with the special interests that would like to maintain the status quo while continuing to get bailouts.

Hypo May Be Liable for Late Disclosure, Judge Says

Hypo Real Estate Holding AG may have informed the markets too late about the risks its subprime holdings presented and may be liable for compensating shareholders, a German judge said. Hypo, which disclosed 390 million euros ($554.5 million) in writedowns on the group’s collateralized-debt obligations on Jan. 15, 2008, needs to explain why it didn’t inform the markets earlier, Presiding Judge Matthias Ruderisch said at a Munich court hearing today. Shareholders have sued the lender and are seeking about 3.6 million euros in damages.

“It’s a fact that Hypo had 1.5 billion euros in CDOs, it’s a fact that in the second half of 2007 there was no market for these papers and it’s a fact that internal calculations found impairments of 13 million euros already in November 2007,” Ruderisch said. “We can’t believe the bank had reliable data for a disclosure only in January 2008.” Hypo Real Estate almost collapsed in September after its Irish Depfa unit failed to get short-term funding amid the credit crunch. Munich-based Hypo has since received a total of 102 billion euros in debt guarantees and credit lines. A parliamentary committee is examining whether Chancellor Angela Merkel’s government could have done more to prevent the bailout and Munich prosecutors are investigating former Hypo managers.

Hypo’s stock fell 38 percent on Jan. 15, 2008, on the disclosure. In a separate shareholder suit, the court in June ordered Hypo to pay a shareholder 4,000 euros in compensation. Lawyers for Hypo appealed that ruling and asked the court to also throw out today’s suits. Hypo had said in two press releases in 2007 that it hadn’t been hurt by the U.S. subprime turmoil. “We think the suits are unfounded,” Hypo spokesman Oliver Gruss said in an e-mail. “We still think we complied with the disclosure requirements.”

Ruderisch said the court’s assessment is preliminary. Only shareholders who bought the stock from November 26, 2007 through Jan. 15, 2008, could claim damages, he said. The judge asked Hypo’s lawyers to provide written documentation on how and when the lenders calculated the impairments and how the company leadership was informed. An Oct. 29 ruling is scheduled. mThe shareholders’ second claim -- that Hypo should have warned about the risks of Depfa’s business model in 2007 -- is likely to be dismissed, Ruderisch said. Depfa refinanced long- term government financing with short-term credit and failed to obtain funding when inter-banking lending dried up after Lehman Brothers Holdings Inc.’s bankruptcy in September.

“We don’t think the market didn’t know Depfa’s strategy in 2007 or that it would have seen that as a problem back then,” said Ruderisch. “The market only saw that as a risk much later when the interest rates structures changed dramatically.” In a separate suit that also targets former Hypo executives Georg Funke and Bo Heide-Ottosen, the court today said it’s unlikely that shareholders can claim damages from both men because it can’t be shown that they intended to harm investors. Lawyers for the pair asked the court to throw out the cases. Today’s suits are among several dozen cases pending in Munich against Hypo

Germany must waste no time in reforming its banks

Back in November 2008, Rahm Emanuel, then the White House chief of staff-designate, laid down a useful measuring rod for what lay ahead: "Never allow a crisis to go to waste." In the wake of the financial crisis, that dictum has direct application not just for the US, but the entire world. Alas, in the middle of 2009, it is not just American policymakers who are letting a great crisis go to waste. Things are not much better in Germany, where this crisis ought to have led to the long-overdue reform of the banking sector - the consolidation of the Landesbanken.

Germany has seven independent state banks, or Landesbanken, which are jointly owned by the state governments and the savings banks. Established to provide state guarantees for regional business development, this practice was essentially outlawed by the European Commission back in 2002. Since then, Landesbanken have faced corporate governance problems. For example, the advisory boards of Landesbanken are supposed to control the top management but professional expertise plays no role in the allocation of seats. In some Landesbanken, neither the management nor the board had reliable information about their holdings of subprime mortgage products when the crisis hit.

Worse, the already doubtful sustainability of their business model - international wholesale banking - has been shattered by the financial crisis. To compensate for their low rates of return compared with private banks of equal size, many Landesbanken before the crisis created structures to hold assets outside their balance sheets. Protected by state guarantees, they borrowed large sums of money in capital markets, which they invested in supposedly high-yielding subprime products with good credit ratings. When theproducts were subsequently downgraded, two state banks were forced to merge immediately. Four of the remaining seven state banks lost much of their equity and had to be bailed out by various state governments with tens of billions of euros.

This situation could get much worse: if the Landesbanken fail to clean up their balance sheets, the next decline in equity capital could prove lethal. To avert such an outcome, it is imperative to establish a "bad bank" to receive their toxic assets - and then continue the clean-up by reducing the number of Landesbanken through mergers.The total assets of Germany's state banks exceed €1,900bn ($2,695bn, £1,640bn). All Landesbanken rank among the 15 biggest German banks - with four of them in the top 10. These four account for about 23 per cent of total assets of the top 10.They are so big and interconnected with the entire banking sector that bankruptcy is not an option.

Due to the unsolved problem of toxic assets and the shortage of equity capital, Standard and Poor's recently downgraded most of the Landesbanken to a rather mediocre level of around BBB+. This has turned the crisis in German banking to a large extent into a crisis specific to the Landesbanken. Against this backdrop, the federal government and the savings banks, as the biggest shareholders, have called for the Landesbanken to merge, to a maximum of three. State governmentsoppose this strategy because the continued existence of the Landesbanken makes it easier for them to manage their cash flow and to implement industrial policy decisions without much publicity.

One way for the federal government to restructure the system would be to take the toxic assets at zero value from the four ailing Landesbanken and transfer them into the bad bank, with the losses covered by the shareholders - state governments and savings banks. The federal government could then recapitalise the good state banks, possibly in co-operation with the savings banks. Pressured by the new shareholders - federal government and savings banks - the remaining Landesbanken could hardly resist merging into a single good bank.

Reform is both needed and possible. While this process will evolve in stages, one can envision a world in which even the two state banks that are considered relatively stable - Helaba and Nord LB - would be privatised. That would be the logical conclusion of a process that has seen the idea of an explicit public purpose of the Landesbanken fall by the wayside.

The authors are president and research director of Financial Markets at DIW Berlin, the German Institute for Economic Research

Pubs closing at rate of 52 a week as hard-up drinkers shun their local

The rate of pub closures is accelerating, with 52 going out of business every week at a cost of 24,000 jobs over the past year, figures show. Almost 2,400 pubs and bars have vanished from villages and towns in the past 12 months, according to research for the British Beer & Pub Association (BBPA). Local pubs serving small communities have been the worst hit, the association said. The number of closures represents the steepest rate of decline since records began in 1990 and has risen by a third compared with the same period last year, when 36 pubs were closing every week.

A preference for drinking more cheaply at home, rather than going out, is thought to have contributed to closures. A BBPA spokesman said: “The biggest impact is the recession. There are fewer people out and fewer people spending money in pubs and bars. Pubs are diversifying but, unfortunately, if you are a community pub you can’t transform yourself into a trendy town centre bar.” The BBPA said that the total number of pubs and bars has fallen from a steady 60,000 “for years” to the 53,466 still trading. It added that of the 52 premises closing each week, 40 are local pubs and nine are high street bars. The recession is claiming about 461 bar jobs a week, according to the figures, compiled by CGA Strategy, the market information group.

The BBPA said that establishments that serve foods, such as gastropubs, were more resilient, closing at a rate of only one a week. By contrast, branded pubs and café-style bars are faring relatively well and are opening at a rate of two every seven days. The fall in spending in pubs and bars is the latest in a string of setbacks for publicans in recent years. Inflationary pressures cut drinkers’ spending power in 2007, resulting in a drop in revenue. The smoking ban in 2007 and changes to the licensing laws have dealt further blows. The BBPA said that higher taxes on beer imposed in the past two Budgets had contributed to the industry’s woes, adding about £600 million to the pub industry’s tax bill.