Girls outside movie house in Amite City, Louisiana

Ilargi: No, we're not getting into today’s home prices data. Well, maybe just to say that Business Week made it two days in a row with a happy note in the morning and a more realistic one in the afternoon. I guess that way they can claim to always be right. No, prices didn't rise, says BW. In fact, they went down. Just not by a lot:

.... seasonally adjusted prices fell just 0.16% from the previous month.

That's still real different from all other headlines, including their own morning line. But let's leave that stuff alone.

Today's best story for me comes from Elizabeth MacDonald at FOX, who spells out how there are hundreds of billions of dollars being drawn, quartered, drowned and smothered to death at General Electric, all of which the US taxpayer, who else, will have to cough up. The insane ways in which its "banking unit" GE Capital, an insane sort of company to begin with, was contorted in order to make sure its sticky hands and wide open beak were best positioned to gobble up public funds, is a sight to behold.

Everybody talks about Gold in Sacks these days, but GE is just as much a cornerstone in America's taxpayer subsidized corporations. Not that they're not just very happy to play under the radar for now. Count them in for a few hundred billion in losses, easily. They'll be announced when you're not counting. And be honest, who is these days?

I’ll leave you with a series of direct quotes, and don't worry, you won’t be the only one whose eyes hurt after reading through them.

• GE Capital was launched in 1932 to help finance its parent’s industrial operations.

• GE chief executive Jeffrey Immelt now sits on the Obama administration’s economic advisory board.

• Earnings at GE Capital plummeted 80% in the second quarter, triggering a 47% plunge in GE’s overall profits.

• GE now says GE Capital faces $34.4 billion in pretax losses and impairments over the next two years....

• Some $270 billion has been torched, immolated out of GE’s market capitalization since 2008....

• GE’s shares hit a 17-year low earlier this year.

• GE let its finance unit dangerously bulk up on all sorts of bad assets during the bubble years, including commercial real estate, $230 billion or so (GE is one of the world’s largest commercial lenders), as well as $183 billion in consumer finance assets (including private label credit cards), and all sort of other assets coming from distressed markets such as the UK and Eastern Europe...

• GE first shocked Wall Street in April 2008 when it missed its earnings estimates by a country mile, with the finance unit’s losses in tow. Ever since, GE has been racing to pare down GE Capital’s $635.5 billion balance sheet to $400 billion. GE chief executive Immelt has also been steadily jawboning lower the company’s profit targets, and vows to cut GE Capital’s profit share of the parent’s earnings down to 30% from 55% in 2007. The market itself is helping Immelt keep to that promise.

• GE Capital has about $81 billion in long-term debt maturing by the end of 2009, and of that, $43 billion came due June 30.

• Last fall [..] GE and its coterie of lawyers descended on Washington to get banking regulators to let GE and its sick finance unit in the door in the taxpayer bailout programs. GE did so by delivering a tortured reading of a 1991 law enacted after the S&L crisis.

The law had to do with stopping “systemic risk” and although GE does not own a bank, it instead owns two small thrifts. Though the thrifts represent just 3% of its overall assets, GE rammed itself through this giant loophole hooked wider by its lawyers.

• ... GE won access to the FDIC debt guarantee program, nearly 40%, it’s estimated, of which represent backstops for GE Capital. GE gets to insure a maximum $126 billion of its debt through this program–already GE is the single biggest corporate user of this FDIC debt insurance.

• If companies can’t take this ocean of water onto their balance sheets when this FDIC insurance expires 2012, then the FDIC, meaning, the US taxpayer must. Already, the FDIC has insured an estimated $340 billion in this program....

• GE also accesses the Federal Reserve’s commercial paper backstop, a maximum $98 billion there ...

• And its footnote disclosures show it may access the Fed’s TALF program, whereby it gets government help for its securitizations of tens of billions of dollars worth of all sorts of assets on its balance sheet, with another $55 billion or so now sitting warehoused in Enron-style off balance sheet vehicles.

• However, GE Capital is not subject to the Fed’s stress tests, nor is it subject to the Fed’s rules for limiting risk, nor is it subject to government limits on executive compensation.

• A look at its balance sheet should also trigger serious concern. GE has $572.8 billion in liabilities and $635.5 billion in assets teetering atop a razor-thin $32.9 billion in tangible common equity....

• To some analysts on Wall Street, GE Capital appears levered up like any run of the mill, overextended hedge fund.

• And here’s one of its most glaring, fire-engine red flags: GE Capital also has $203.2 billion borrowings coming due in the next four years, about two-thirds of the company’s total debt.

Tiny Home-Price Drop is Best News Yet

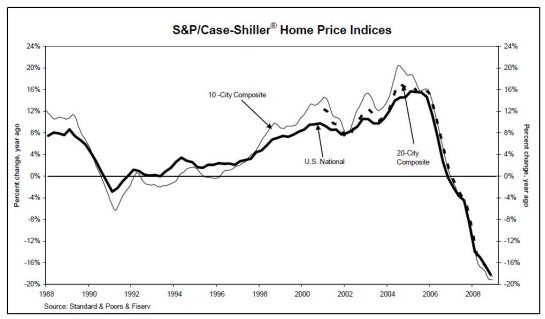

You won't find it in the July 28 press release from Standard & Poor's, or in most news reports, for that matter. But the most encouraging statistic from the Standard & Poor's Case-Shiller 20-City Composite Home Price Index report released on July 28 is that in May, seasonally adjusted prices fell just 0.16% from the previous month.

That minuscule monthly change works out to an annual rate of decline of a little under 2%. That's a huge improvement considering that from last September through March, the index was falling at an annual rate of more than 20%. S&P's press release, and most news reports, focused on the unadjusted prices, comparing them with a year earlier and noting that the rate of decline had slowed.

Even some longtime bears were impressed by the data. Economist David Rosenberg of Gluskin Sheff & Associates in Toronto wrote, "now this is a green shoot!"

To be sure, this is not definitive evidence that the housing bust is over. Prices, and sales volumes, could still take another tumble. For one thing, the $8,000 federal tax credit for first-time homebuyers expires in November. More important, the number of home foreclosures is continuing to mount, adding supply to the market at the same time that sales of new and existing homes remove supply. As long as the unemployment rate is around double digits, there will be downward pressure on the housing market.

You have to dig a little bit for the seasonally adjusted data, by the way. It's here on the S&P Web site. (S&P, like BusinessWeek, is owned by The McGraw-Hill Companies.)

The raw, unadjusted index actually showed a price increase from April to May, but that's not the right number to focus on because prices typically rise from April to May—a fact that The Wall Street Journal's Web site missed in its article headlined "Home Prices Post Monthly Increase."

"Recession's Over, Recovery Underway": What's Missing in Action

by Charles Hugh Smith

The mainstream media is gleefully hyping "the recession is over, the recovery is underway." Nice, except for everything that's missing in action.

"The recession is over, the recovery is underway." Exactly what will be driving this fabulous "recovery"? Let's check in on the usual forces which have powered previous recoveries:

1. Autos/vehicles: missing in action (MIA). Annual sales have plummeted from 17 million vehicles a year to about 9 million a year, and the U.S. probably contains about 30 million surplus/lightly used vehicles ( a number snagged from economist David Rosenberg's latest report). Modern vehicles can easily last 15-20 year, so the "need" to replace vehicles is rather low. Actual "necessary" replacement might require as few as 5 million vehiclesa year.

With unemployment at 16%, assets down by $10 trillion and the FIRE economy (finance, real estate and insurance) in disarray, where does anyone think the consumer borrowing firepower will come from to finance an extra 8 million vehicles a year?

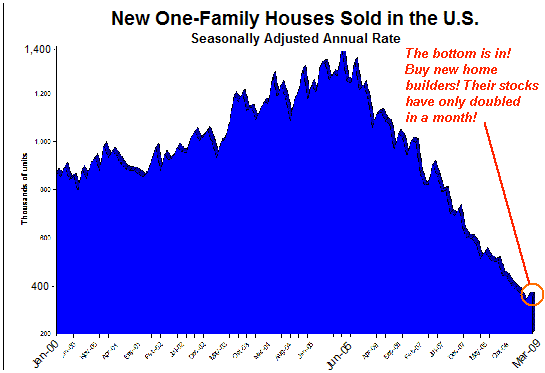

2. Housing/real estate: missing in action (MIA). Let's see: new home sales down from 1.4 million a year to 350,000 a year and the headlines are screaming "recovery in housing" even as house prices are down 50% from the bubble peak andstill declining. The Case-Shiller index just came in at a year-over-year decline of 17% and the market is cheering because it's a few tenths of a percent "better than expected."

The U.S. has 18.7 million vacant homes and even if you bulldoze a couple million in shrinking rust-belt cities we still have 16.7 million vacant dwellings, plus thousands more foolishly being constructed every year.

Furniture sales and auctions of old furniture are in the ditch; ditto draperies, carpeting, hardwood flooring, etc. etc., much of which is still manufactured in the U.S. No wonder the manufacturing sector is still contracting as well.

The bubble in commercial real estate has yet to pop but the needle is currently being inserted into the balloon. Too many malls, too many strip malls, too many office towers, too many CRE buildings everywhere.

3. FIRE economy: missing in action (MIA). Finance, real estate and insurance were the boomtown industries in the housing bubble. They're diminished and will never come back; the consumer must save now to avoid a retirement in a cardboard box, flipping houses for profits is history and people are paying off debt, not churning new loans.

4. Healthcare: missing in action (MIA). Everybody and their brother has been touting healthcare as the "growth industry" but since it already consumes 17% of the entire U.S. GDP, there's very little oxygen left. The ever-expanding entitlements of Medicare and Medicaid are actually being trimmed, and those 15 million people who have lost their jobs and/or benefits can't go to the doctor and have their insurance carrier billed $10,000 any more. Healthcare has peaked and a growing shareof the government's revenues will be going to pay interest on the ballooning national debt, not expanding healthcare. Any other view is fantasy; the interest on the debt is already $400 billion a year and interest rates haven't even started rising.

5. Education: missing in action (MIA).This is the other highly touted "always expanding" jobs factory. Tell that to the thousands of teachers, janitors, and administrators being laid off as local government tax revenues crater. And people are finally waking up to the unfortunate fact that private diploma mills are not actually offering much of an edge in the real world; in fact, neither are pricey private universities.

When it comes time to create your own job, nobody cares about your diploma--they only want value and results. The current crop of graduates may be in some sort of elevated state of denial--i.e. believing the job drought will end next year--but the old ploy ofgoing back to graduate school to wait out the recession may not work unless you're getting a graduate degree in stem cell research or network security. In any event, education is no longer the "guaranteed job factory" because funding for all local government functions is being slashed.

6. Local government: missing in action (MIA). The same can be said for government itself, which continued to add tens of thousands of jobs even as the recession began slashing and burning the private sector economy. The reductions in local government headcount have yet to really kick in, as Federal stimulus funding is staving off cuts that would have resulted from plummeting tax revenues. All the stimulus has done is push the job cuts in state, county and city governments forward into 2010.

All three of these sectors--government, education and healthcare--expanded dramatically because tax revenues skyrocketed as a result of the bubble. For example, look at this chart of the total assessed value of Florida real estate 1990 to 2005: it tripled. Now think of all those luscious property taxes which gushed into local government coffers:

All those expecting unlimited growth in government, education and healthcare seem to forget that all these expanded as a result of the bubble in tax revenues derived from the bubble in credit, stock and bond markets and real estate.

7. Small business: missing in action (MIA).Small businesses are the real job engine of the economy, but unfortunately very few small businesses are expanding and anxious to hire more employees. The vast majority are still trying to stave off insolvency and are looking to cut more hours and staff positions. There simply is no alternative as the State (all levels of government) increases the tax load on small business even as they claim to "care about small business." True, in one way: they care the way parasites care about not killing the host outright but merely bleeding it to the point of near-death.

Unfortunately, the parasites misjudged and their host is expiring.

8. Domestic manufacturing: missing in action (MIA). While the manufacturing sector is still formidable in many areas, as we all know much has been shipped overseas for the basic, classic capitalist reason that the move increased profits stupendously. Now, however, a "recovery" or "export boom" in manufacturing cannot pull the entire economy any longer because the manufacturing sector has shrunk to such a small percentage of the overall economy.

9. Structural reform: missing in action (MIA).Instead of cleaning out the embezzlement, fraud, gaming, leverage, exploitation, obfuscation, etc. at the heart of the U.S. financial sector, the guilty have been rewarded with gargantuan bailouts and the innocent (taxpayers) punished. The public pension systems which boosted retirement benefits in the bubble years are heading for insolvency but rather than reform them the unions and political lackeys are shoving this reality under the rug lest various interest groups get angered.

Healthcare, a.k.a. sick-care, is in desperate need of deep structural reform but instead we are treated to a Kafka-esque nightmare charade in which another trillion dollars will be squandered "to save money later." The special interests have this "industry" in a chokehold and will only release their grip when the poor old system expires, as it most certainly will, and soon.

10. Strong dollar: missing in action (MIA). If the dollar loses half its current exchange value (as measured by the DXY Dollar Index) as many expect then the cost of all imports such as oil magically double. Thus we could see $130/barrel oil even as the price in gold or other currencies didn't move at all or actually became cheaper.

11. Collateral/borrowing power: missing in action (MIA). You've probably seen this chart or one like it recently:

With $10 trillion of assets down the drain and the entire economy maxed out on credit, where do economists expect new credit growth to come from? Martians with good credit landing and hurrying into Bank of America for loans?

12. Leadership: missing in action (MIA). We have few leaders in any sector, public or private; we have panderers to various special interests and voting blocs, similar to any run-of-the-mill Third World kleptocracy. To my knowledge only Ron Paul speaks to fundamental issues such as getting rid of the Federal Reserve and the failure of the entire Keynsian "intervention/manipulation of free markets to save them"project. Few speak to the end-state of all government dependent on credit bubbles for its growth and policy: insolvency.

Bashing Goldman Sachs Is Simply a Game for Fools

by Michael Lewis

From the moment I left Yale and started working for Goldman Sachs, I’ve felt uneasy interacting with those who don’t. It’s not that I think less of Goldman outsiders than I did while I remained among you. It’s just that I feel your envy, and know that nothing I can do or say will ever persuade you that I am no more than human. Thus, like many of my colleagues, I have adopted a strategy of never leaving Goldman Sachs, apart from a few brief, spasmodic attempts to make what you outsiders call “love” or “the beast with two backs.” Goldman recognizes how important it is for its people to replicate themselves. We bill no performance fees for the service.

Today, the sheer volume of irresponsible media commentary has forced us to reconsider our public-relations strategy. With every uptick in our share price it’s grown clearer that we who are inside Goldman Sachs must open a dialogue with you who are not. Not for our benefit, but for yours. America stands at a crossroads, and Goldman Sachs now owns both of them. In choosing which road to take, ordinary Americans must not be distracted by unproductive resentment toward the toll-takers. To that end we at Goldman Sachs would like to dispel several false and insidious rumors.

Rumor No. 1: “Goldman Sachs controls the U.S. government.”

Every time we hear the phrase “the United States of Goldman Sachs” we shake our heads in wonder. Every ninth-grader knows that the U.S. government consists of three branches. Goldman owns just one of these outright; the second we simply rent, and the third we have no interest in at all. (Note there isn’t a single former Goldman employee on the Supreme Court.) What small interest we maintain in the U.S. government is, we feel, in the public interest. Our current financial crisis has its roots in a single easily identifiable source: the envy others felt toward Goldman Sachs.

The bozos at Merrill Lynch, the dimwits at Citigroup, the nimrods at Lehman Brothers, the louts at Bear Stearns, even that momentarily useful lunatic Joe Cassano at AIG -- all of these people took risks that no non-Goldman person should ever take, in a pathetic attempt to replicate Goldman’s financial returns. For too long we have allowed others to emulate us. Now we are working productively with Treasury Secretary Tim Geithner and the Congress to ensure that we alone are allowed to take the sort of risks that might destroy the financial system.

Rumor No. 2: “When the U.S. government bailed out AIG, and paid off its gambling debts, it saved not AIG but Goldman Sachs.”

The charge isn’t merely insulting but ignorant. Less responsible journalists continue to bring up the $12.9 billion we received from AIG, as if that was some kind of big deal to us. But as our CFO David Viniar explained back in March, we were hedged. Our profits from AIG “rounded to zero.” People who don’t work at Goldman Sachs, of course, find this implausible: How could $12.9 billion round to zero? Easy, but you just need to understand the mathematics.

Let’s assume AIG transferred $12,880,560,250.34 of taxpayer money to Goldman Sachs. A Goldman outsider, asked to round this number, might call it $12,880,560,250.00. That’s not how we look at it; at Goldman we always round to the nearest $50 billion, so anything less than $25 billion rounds to zero. Think of it that way and you can see that $12,880,560,250.34 isn’t even close to not rounding to zero.

Rumor No. 3: “As the U.S. government will eat the losses if Goldman Sachs goes bust, Goldman Sachs shouldn’t be allowed to keep making these massive financial bets. At the very least the $11.4 billion Goldman Sachs already has set aside for employees in 2009 -- $386,429 a head, just for the first six months -- is unfair, as the U.S. taxpayer has borne so much of the risk of the wagers that generated the profits.”

Really, we don’t know where to begin with this one. It is wrong-headed in so many different ways! Let’s begin with the idea that the taxpayer is running a bigger risk than we are. The billions he stands to lose are trivial; after all, they round to zero. The real risk, when you think about it even for a minute, is the risk we take ourselves: that Goldman will cease to exist and we will cease to be Goldman employees. To flirt with such tragedy we obviously need to be paid.

Rumor No. 4: “Goldman employees all look alike.”

Several recent newspaper photos have revealed that a surprising number of Goldman Sachs workers are white, male and bald. That non-Goldman people glance at such photos and think “Holy crap, they even look alike!” just shows how deeply anti- Goldman bigotry runs in American life. We at Goldman represent unique clusters of DNA; if we bear some faint surface resemblance to one another, and to creatures from the 24th century, it is only because our superior powers of reasoning lead us to hold in our minds exactly the same thoughts, at exactly the same time.

A shared disinterest in growing hair, for instance, isn’t a coincidence of nature but an expression of healthy like- mindedness. “The world is a pool table,” our naked-headed CEO likes to tell us. “And all the people in it are either stripes or solids. You alone are the cue balls.”

Rumor No. 5: Goldman Sachs is “a great vampire squid wrapped around the face of humanity, relentlessly jamming its blood funnel into anything that smells like money.”

Those words are of course taken from a recent issue of Rolling Stone magazine and they are transparently false. For starters, the vampire squid doesn’t feed on human flesh. Ergo, no vampire squid would ever wrap itself around the face of humanity, except by accident. And nothing that happens at Goldman Sachs -- nothing that Goldman Sachs thinks, nothing that Goldman Sachs feels, nothing that Goldman Sachs does --ever happens by accident.

The Shadow Banking Pyramid

by Max Keiser

The current spate of fraud on Wall St., and specifically the front-running and market manipulation scams being committed by Wall St. banks on the floor of the NYSE and other market making venues, is finally getting some coverage This would be good news if it weren't meaningless.

Some background: I first started reporting on the rigged markets scandal in the U.S. and the U.K. five years ago in the pages of The Ecologist magazine in the U.K. I predicted that the unraveling of FannieMae and FreddieMac was all but certain due to obvious accounting fraud. I was one of many pointing out the blindingly obvious, but this information was kept out of view from the main stream America for fear it would frighten the sheep into cutting back on their leveraged speculation and consumption; using their homes like ATM machines.

In an economy dictated to by the unholy triangle of GE, CNBC, and Wall St., weapons, propaganda and lottery tickets, delusions (and fiat currencies) must be preserved. Talking about crooks on Wall St. has been a staple while co-hosting my radio show in London with Stacy Herbert on ResonanceFM 104.4, "The Truth About Markets." Week after week we forensically describe the workings of Wall St. frauds -- drawing on my experience as a former Wall St. trader and inventor of patented financial engineering technologies used on Wall St. today -- to explain how the scams are done in full view of the SEC and CFTC.

ResonanceFM is a musicians cooperative listened to primarily by bong smoking squatters in Shordditch who, by virtue of the fact that mainstream American and British media chose not to cover these crimes left open a niche for us to cover, have become preternaturally knowledgeable about fraudulent Collaterized Debt Obligations, Special Purpose Entity Accounts and High Frequency Trading Arbitrage. Many of these pot heads thank me today because many of them put their meager savings into gold bullion as we have been suggesting since 2002 -- which shot up 40% against the British Pound last year.

In 2006 I started making documentaries for Al Jazeera English. Death of the Dollar, Rigged Markets and Money Geyser explained, respectively, the structural weakness of the dollar, the structural weakness of the New York Stock Exchange, and the structural weakness of the global currency grid and in particular the currency and economy of Iceland. A year later, the Icelandic krona and the economy evaporated in a cloud of currency 'carry trade' ice and dust exactly as we predicted it would. In 2007 the sup-prime scandal and the controlled demolition of Bear Stearns and Lehman Brothers got under way thanks to the Washington-Wall St. revolving door that gave us the Goldman Sachs-Oval Office axis of insider trading, the S&L crash, the 1987 crash, the Long Term Capital Management (LTCM) crash, the crash of Drexal Burnham, Enron, WorldCom and the dot-com crash.

America has become the most corrupt empire in history and since the debts that caused each of these catastrophes was never paid off, but simply put off the balance sheet and traded in what Prime Minister Gordon Brown calls the 'Shadow Banking System' or to be more precise the Shadow Banking Pyramid, Americans can expect to live in the shadow of debt in perpetuity. America's debts are bigger than the entire GDP of the world, so unless the whole world decides to bail out America by gifting America 100 percent of their wages and profits for a year or more America can forget about ever digging its way out of the debt tomb.

In 2008 I produced and presented a series for BBC World News, The Oracle. For ten weeks I hammered away reporting on the rot that was threatening to take down America; the duplicitous spewings of Hank Paulson, Ben Bernanke, and Tim Geithner, as well as the parasitical machinations of the Fed, but I wasn't surprised when Congress appeased financial terrorists on Wall St. and coughed up 700 billion dollars in ransom at the end of last year to ensure payment of Goldman Sachs' bonus pool for 2008 and 2009.

This is why I do not believe that the main stream media's belated reporting on Wall St. scandals is meaningful. It's too late. Like the New York Times sitting on the Bush wire tap story until after the election of 2004, the story of banking buccaneers and vipers in the New York Times reads more like a requiem than a news story. The Egyptians had the great pyramids in the Valley of the Kings we have the great pyramids of debt created in the canyons of Wall St. These are now permanent features on the American and British financial landscape that have effectively turned Americans and Brits into debt slaves.

Wall Street on Speed

The New York Times recently reported that the latest scheme--or scam--on Wall Street is something called High Frequency Trading. Very sophisticated financial firms, such as Goldman Sachs, are tipped off by the New York Stock Exchange's own computers to pending buy and sell orders. Armed with ultra sophisticated computer algorithms, the insiders anticipate the direction of the market based on what they learn about supply and demand for a given security. They can make an extra penny here and an extra penny there at the expense of us suckers, adding up to billions.

"Nearly everyone on Wall Street is wondering how hedge funds and large banks like Goldman Sachs are making so much money so soon after the financial system nearly collapsed," wrote the Times' Charles Duhigg in a front page piece that was the talk of New York and Washington. "High-frequency trading is one answer." As debates in the blogosphere in the last couple of days have made clear, there are a couple of possibilities of what is at work here. One is that Goldman and others are literally using privileged information to make trades ahead of markets, in which case they are committing a felony.

Specifically, the abuse is known as "front-running," or trading ahead of customers, and it is an explicitly illegal form of market manipulation. Front running is epidemic on Wall Street--the whole point of an investment bank trading for its own account is to take advantage of its specialized knowledge of markets--and the SEC or the Justice Department shuts down front-running when it becomes too blatant to ignore. The other possibility is that the Goldmans of the world have found themselves a nice loophole. Tapping into the Stock Exchange's own computers and other sources of trading activity is something that anyone in theory could do, but only a few privileged insiders have the sophistication to exploit what they find. Often orders are placed, only to be cancelled. Their purpose is to figure out what the market is willing to pay, and then get in ahead of it.

But suppose that High Frequency Trading doesn't violate any law. It still is the essence of what's wrong with the recent metastasis of money markets into private game preserves for insider-traders. Consider for a moment some first principles. The legitimate and efficient function of financial markets is to connect investors to entrepreneurs, and depositors to borrowers. There is no legitimate reason whatever for this to be done by the millisecond. At bottom, the process is pretty simple. The intermediary--the bank, savings institution, or investment bank makes its fees for making a judgment about risk and reward. How likely is the loan to be paid back? How high an interest rate should it charge? How should a new issue of securities be priced? The investor decides whether to indulge a taste for risk or for prudence.

But the hyperactive trading markets and creations of recent decades such as credit default swaps and high speed trading algorithms add nothing to the efficiency of financial markets. They add only two things--risk to the system, and the opportunity for insiders to reap windfall profits. Therefore, whether or not Goldman's lawyers have figured out how it can engage in High Frequency Trading and stay within the law, there is a strong case that this entire brand of financial engineering should be prohibited. The whole game should be slowed down. Bona fide investors should get in line under the rule of first come, first served. Anything else should be considered illegal market manipulation. No dummy transactions. There is absolutely no gain to economic efficiency from having prices of securities change in milliseconds, and much gain to the opportunities for manipulation.

The need to restrain traders from exploiting their privileged knowledge is an old fight. During the New Deal, for example, many reformers proposed that floor specialists for investment bankers and brokerage houses simply be prohibited from trading for their own accounts. They should be there simply to execute buy and sell orders for customers. Otherwise, the conflict of interest would be overwhelming--and this was before computers. These reformers were overruled, but insider trading was explicitly prohibited (and good luck catching it.)

Now, as then, it is a mark of Wall Street's stranglehold on politics that the most sensible of remedies seem impossibly radical. One very good way to damp down the dictatorship of the traders, and raise some needed revenue along the way, would be through a punitively high transactions tax on very short term trades. Genuine investors should get favored fax treatment. Pure traders should be taxed, and very short term manipulation taxed into oblivion. If the financial crisis has proven anything, it is that capital markets have become an insiders' game in which trading profits crowd out the legitimate business of investment. The whole business-models of the most lucrative firms on Wall Street are a menace to the rest of the economy. Until the Obama administration recognizes this most basic abuse and shuts it down, it will be more enabler than reformer.

GE Capital Needs More Funds

by Elizabeth MacDonald

For the second time this year, GE has laid bare GE Capital’s books to assuage Wall Street’s concerns about the finance unit’s stability, and the results are of deep concern.While the company works hard to calm investor nerves at yet another Wall Street meeting, there are a number of danger zones on GE Capital’s balance sheet that GE is scrambling to fix.

GE has been the worst performer in the Dow Jones Industrial Average this year, due to its finance unit’s serious problems. The industrial conglomerate now says it may need to inject $2 billion to $7 billion into GE Capital in 2011 to bolster its finances.

GE Stuns Wall Street–Again

Last week, GE shocked Wall Street once again with a nasty second quarter profit report. Earnings at GE Capital plummeted 80% in the second quarter, triggering a 47% plunge in GE’s overall profits. GE now says GE Capital faces $34.4 billion in pretax losses and impairments over the next two years under the worst case scenarios under the government’s stress tests.

If GE spins off GE Capital (which it vows it won’t), without the benefit of a deep-pocketed industrial parent and the extraordinary generosity of the US taxpayer, there are deep concerns that GE Capital might go under, analysts on Wall Street fear.

GE’s Non-bank Bank

Which is why GE has successfully pressured the government to let it use all sorts of taxpayer bailout programs, even though GE Capital is ostensibly not a bank, and is instead a charter member of the shadow banking system, where it sells bank products unregulated by the government.

If it were a bank, GE Capital would be the seventh largest in the country in terms of assets, just behind Morgan Stanley. A member of the Dow since 1896, GE Capital was launched in 1932 to help finance its parent’s industrial operations. GE chief executive Jeffrey Immelt now sits on the Obama administration’s economic advisory board.

While the US government has helped GE, it has refused to come to the help of GE Capital’s competitor CIT Group, leaving this small business finance company to scramble to get private funding to shore up its severely damaged balance sheet.

Earlier this year, the Obama administration said it would seek to do away with a notably weak bank regulator, the Office of Thrift Supervision, which also fell down on the job overseeing the troubled insurer AIG (AIG owns thrifts as well, putting it in the OTS’s purview). That raises the question whether GE Capital might be subject to more intense reviews by another government body–the Federal Reserve, since GE Capital uses Fed bailout programs.

Administration Growing Uneasy

The thinking behind the abolishment of the OTS was, the Administration was growing increasingly uneasy with non-banks like GE using a backdoor into taxpayer bailout programs since companies have purchased what are called ‘industrial loan companies,’ usually based in Utah, which do loan and credit card processing as well as other backroom banking operations. The Administration, the thinking is, instead wanted to force these companies to either focus on commerce or banking, but not both, triggering speculation GE would have to spin off GE Capital.

Immelt Sticks to His Guns

GE chief executive Immelt has said GE has no intention of doing that, and today the company is sticking to that party line.

“GE is and will remain committed to GE Capital, and we like our strategy,” Immelt has already said in a memo to staffers. The company again has reiterated that GE Capital would be profitable this year, with an estimated $5 billion in earnings, down from $7.1 billion last year and half the $10.3 billion it posted in 2007.

Some $270 billion has been torched, immolated out of GE’s market capitalization since 2008, and GE’s shares hit a 17-year low earlier this year.

Short-term Obsession = Long-Term Problems

Obsessed with short-term profit goals, GE let its finance unit dangerously bulk up on all sorts of bad assets during the bubble years, including commercial real estate, $230 billion or so (GE is one of the world’s largest commercial lenders), as well as $183 billion in consumer finance assets (including private label credit cards), and all sort of other assets coming from distressed markets such as the UK and Eastern Europe, assets which now sit like anvils on GE Capital’s balance sheet.

GE Struggles to Downsize GE Capital

GE first shocked Wall Street in April 2008 when it missed its earnings estimates by a country mile, with the finance unit’s losses in tow. Ever since, GE has been racing to pare down GE Capital’s $635.5 billion balance sheet to $400 billion. GE chief executive Immelt has also been steadily jawboning lower the company’s profit targets, and vows to cut GE Capital’s profit share of the parent’s earnings down to 30% from 55% in 2007.

The market itself is helping Immelt keep to that promise.

GE Capital Not Earning Its Keep

GE Capital earns its keep by exploiting the spread between the cost of debt it issues and the loans and finance contracts it writes, making it highly vulnerable to a credit market meltdown.

In other words, GE Capital relies on short-term borrowings for its funding needs, so when the credit markets collapsed last fall, GE was staring into the abyss. GE Capital has about $81 billion in long-term debt maturing by the end of 2009, and of that, $43 billion came due June 30.

How GE Maneuvered–Fast

Last fall, after AIG, Lehman Bros., Wachovia and Washington Mutual collapsed, after Freddie Mac and Fannie Mae were taken into government conservatorship, GE and its coterie of lawyers descended on Washington to get banking regulators to let GE and its sick finance unit in the door in the taxpayer bailout programs. GE did so by delivering a tortured reading of a 1991 law enacted after the S&L crisis.

The law had to do with stopping “systemic risk” and although GE does not own a bank, it instead owns two small thrifts. Though the thrifts represent just 3% of its overall assets, GE rammed itself through this giant loophole hooked wider by its lawyers.

Things got even worse earlier this year when GE lost its coveted Triple-A rating, which lets it borrow dirt cheap in the credit markets. It also slashed its dividend for the first time since 1938, a dividend tantamount to an annuity, analysts have noted. GE then raced to use taxpayer bailout programs.

GE’s Government Loopholes

So GE won access to the FDIC debt guarantee program, nearly 40%, it’s estimated, of which represent backstops for GE Capital. GE gets to insure a maximum $126 billion of its debt through this program–already GE is the single biggest corporate user of this FDIC debt insurance. The program lets GE borrow dirt-cheap in the credit markets to fund its operations. GE vows it will soon exit this program.

If companies can’t take this ocean of water onto their balance sheets when this FDIC insurance expires 2012, then the FDIC, meaning, the US taxpayer must. Already, the FDIC has insured an estimated $340 billion in this program, which it plans to end by October.

GE also accesses the Federal Reserve’s commercial paper backstop, a maximum $98 billion there. And its footnote disclosures show it may access the Fed’s TALF program, whereby it gets government help for its securitizations of tens of billions of dollars worth of all sorts of assets on its balance sheet, with another $55 billion or so now sitting warehoused in Enron-style off balance sheet vehicles.

However, GE Capital is not subject to the Fed’s stress tests, nor is it subject to the Fed’s rules for limiting risk, nor is it subject to government limits on executive compensation.

Ugly Profit Forecast

And while it says it will be profitable this year, GE Capital though has stress tested its balance sheet, and the results were ugly. As noted, it said it faces $34.4 billion in pretax losses and impairments over the next two years, using the worst case scenarios in the government’s stress tests.

GE Capital’s Perilous Balance Sheet

A look at its balance sheet should also trigger serious concern. GE has $572.8 billion in liabilities and $635.5 billion in assets teetering atop a razor-thin $32.9 billion in tangible common equity, its net worth on a hard assets basis, after you strip out ephemera like goodwill (the payment made above book value in acquisitions) or intangibles, like, say, the value of the brains of its spreadsheet jockeys.

To some analysts on Wall Street, GE Capital appears levered up like any run of the mill, overextended hedge fund.

Paying the Piper

And here’s one of its most glaring, fire-engine red flags: GE Capital also has $203.2 billion borrowings coming due in the next four years, about two-thirds of the company’s total debt.

Can GE refinance that debt without the taxpayers’ help?

Politicians Accused of Meddling in Bank Rules

Accounting rules did not cause the financial crisis, and they still allow banks to overstate the value of their assets, an international group composed of current and former regulators and corporate officials said in a report to be released Tuesday. The report, from the Financial Crisis Advisory Group, also deplored successful efforts by politicians to force changes in accounting rules and said that accounting standards should be kept separate from regulatory standards, contrary to the desire of large banks.

“The message to political bodies of ‘Don’t threaten, Don’t coerce’ flies in the face of some of what has been coming from the European Commission and from members of Congress,” said Harvey Goldschmid, a co-chairman of the group and a former member of the Securities and Exchange Commission. The report itself, written by a group that included Tommaso Padoa-Schioppa, a former Italian finance minister; Lucas Papademos, a vice president for the European Central Bank, and Michel Prada, a former head of the French stock market regulator, used considerably more diplomatic language.

“We have become increasingly concerned about the excessive pressure placed on the two boards to make rapid, piecemeal, uncoordinated and prescribed changes to standards, outside of their normal due process procedures,” the group wrote in its report, which was commissioned by the Financial Accounting Standards Board of the United States and the International Accounting Standards Board. “While it is appropriate for public authorities to voice their concerns and give input to standard setters, in doing so they should not seek to prescribe specific standard-setting outcomes,” the report added.

Earlier this year both boards, under pressure from banks and politicians, made rapid changes to allow banks more leeway in valuing assets and thus reduce the losses they would otherwise have to report. The group, whose other co-chairman is Hans Hoogervorst, the chairman of the Netherlands Authority for the Financial Markets, said that despite arguments that the financial crisis was worsened by forcing banks to write down their assets to market value, the overall effect had been the opposite.

Pointing to rules that delayed the write-down of bad loans and allowed banks to hide risks off their balance sheets, the group said the net impact of accounting rules “has probably been to understate the losses that were embedded in the system.” Banking regulators have been looking for ways to make the regulatory system less “pro-cyclical,” perhaps by allowing banks to postpone recognition of profits in good times so that losses would not be as large in bad times.

The group cautioned that there could be conflicts between the aim of accounting rule makers to accurately reflect a company’s financial position and the goals of banking regulators. “For example,” the group wrote, “transparency may not always be the best way to prevent a run on the bank.” When those differences arise, it said, it may make sense for regulators to measure bank capital differently than accounting rules would call for, but “the effects of those differences should be disclosed in a manner that does not compromise the transparency and integrity of financial reporting.”

Despite the apparent conflict with both bankers and bank regulators, the Financial Crisis Advisory Group included a number of people with experience in those fields. Among them were Gerry Corrigan, a former president of the Federal Reserve Bank of New York and now an official with Goldman Sachs; Nobuo Inaba, a former executive director of the Bank of Japan; Gene Ludwig, a former comptroller of the currency; and Klaus-Peter Müller, the chairman of the supervisory board of Commerzbank in Germany. The group also warned against changing rules in ways that would make it easier for banks to manage earnings.

At the center of the arguments are fundamental differences in the purpose of financial statements. In one comment letter submitted to the Financial Crisis Advisory Group, the French Banking Federation argued that only assets that banks intend to trade should have to be shown at fair value, with most others valued at the original cost unless the bank had determined that losses were likely. Using market value for such assets, the bankers said, has unreasonably damaged bank capital levels.

“In the current financial crisis, financial statements could be hardly used as a tool to evaluate the economic performance of entities from a financial stability perspective as they have more reflected the collapse of financial markets,” the bankers wrote. A competing view was voiced by Edward Trott, a former member of FASB and former partner in KPMG, a large accounting firm, who said that the banks imposed different standards on their customers than they wished to have imposed on them.

“The area for bank regulators to be involved with accounting standards setting is to help identify the financial information the banks need from others to make appropriate lending and investing decisions,” Mr. Trott wrote. “In my experience, banks want current fair value information about assets that serve as collateral for loans. They do not want information about what assets cost two or three years ago.”

China warns banks over asset bubbles

Chinese regulators on Monday ordered banks to ensure unprecedented volumes of new loans are channelled into the real economy and not diverted into equity or real estate markets where officials say fresh asset bubbles are forming. The new policy requires banks to monitor how their loans are spent and comes amid warnings that banks ignored basic lending standards in the first half of this year as they rushed to extend Rmb7,370bn in new loans, more than twice the amount lent in the same period a year earlier.

Beijing’s concerns are echoed in other countries across the region, most notably South Korea, where the government says it is taking steps to cool a real estate bubble, and Vietnam, where the government has ordered state banks to cap new lending to head off inflation. The situation in much of Asia is very different from most Western economies, where governments have flooded the financial system with liquidity to encourage unwilling banks to lend more. In China, regulators are now concerned that too much money is being lent by the state-controlled banks and the country’s tentative economic rebound could come at the cost of a stable financial system.

In statements published last week, Wu Xiaoling, who recently retired as deputy governor of the central bank, warned new lending this year would probably reach as high as Rmb12,000bn, a staggering increase of 40 per cent of the entire stock of outstanding loans in just one year. She called this sort of growth excessive and said it would lead to bubbles in the property and stock markets. The flood of new lending also has implications for the quality of bank loans and the country’s overall growth.

“China's economic recovery is being constructed on the back of a savaged banking system,” said Derek Scissors, a research fellow at the Heritage Foundation in Washington. “Tens of billions – and perhaps hundreds of billions – of dollars of loans will not be repaid.” He points out that in recent years total loan growth of around 15 per cent has supported gross domestic product growth of higher than 10 per cent but in the first half of this year total loan growth of around 33 per cent supported GDP expansion of only 7 per cent.

“China's economic policies have shifted from being unsustainable over the very long term to being unsustainable for any more than one year,” Mr Scissors said. China’s benchmark stock index has already more than doubled from the low it reached last November and property prices have also rebounded strongly with state media reporting long queues and scuffles at sales promotions for some new real estate projects.

Ms Wu hinted Beijing may soon raise the amount of money banks must hold on deposit with the central bank, marking a change of policy from last year when it aggressively slashed the reserve requirement ratio and interest rates. The central bank has also ordered 10 banks, including Bank of China, to buy Rmb100bn worth of central bank notes with a maturity of one year and a return of just 1.5 per cent, according to Chinese media reports. This move is interpreted as a warning to banks that have been the most active lenders that they should now start to rein in their excessive behaviour.

Concern spreads

Worries about rapid credit growth have spread beyond China, write Tim Johnson in Bangkok and Christian Oliver in Seoul. Prakriti Sofat, a regional economist with HSBC in Singapore, has calculated outstanding loans in Vietnam have risen 17 per cent this year. Credit has been boosted a government move to subsidise 4 percentage points of interest on corporate loans to help sustain jobs. The ready availability of relatively cheap credit has coincided with a revival in the fortunes of the stock market, which is up more than 90 per cent from its low in February.

The central bank recently instructed banks to limit credit growth this year to 25 per cent. South Korean regulators have had their eyes on surging mortgage activity and property prices. Mortgage lending is running at the highest levels in two and half years. Bank lending to Korean households rose Won4,000bn last month, compared to Won2,800bn in May. To restrain mortgage growth, homebuyers are now limited to borrowing half the purchase price, down from 60 per cent. “We have seen some specific areas of Seoul where there appears to be some speculative activity so we are taking pre-emptive action,” said Rhee Chang-yong, vice chairman of Korea’s financial services commission.

Bank of China to Continue Lending Expansion Unless Government Clamps Down

Bank of China Ltd., which doled out the most loans among Chinese banks in the first half, plans to keep expanding credit unless the government clamps down on the nation’s record lending boom.

The nation’s third-largest bank will maintain its original target of generating about 10 percent of China’s new loans in 2009, Beijing-based spokesman Wang Zhaowen said by telephone yesterday. Bank of China may “fine tune” its strategy in line with any government policy changes, he said.

Bank of China advanced a record 902 billion yuan ($132 billion) of loans in the first half, leading a credit explosion that drove stocks and property prices higher and helped spur an economic recovery. The lending spree, encouraged by the government, has fanned concerns that asset bubbles will form and bad loans will rise, and the bank regulator yesterday called on lenders to control the flow of credit. “Banks are willing to sacrifice their long-term health for short-term gains in profit, and more importantly, to please the government,” said Wen Chunling, a Beijing-based analyst at Fitch Ratings. “A significant part of the loans extended in the first half may become non-performing over the next five to 10 years.”

Capital adequacy ratios at China’s banks have dropped as a result of a surge in lending in the first half of the year, the central bank said in a report on its Web site today. “The rapid decline in capital adequacy ratios and strengthened risk management may constrain the banking industry’s ability to sustain rapid growth in credit,” it said. The China Banking Regulatory Commission has indicated in past weeks it’s concerned about excessive credit creation. Yesterday, the watchdog told banks to ensure loans intended for investment in fixed assets go to projects that support the real economy. That push is colliding with the government’s attempts to ensure an economic recovery.

Premier Wen Jiabao last week pledged to maintain a “moderately loose” monetary policy, suggesting the government is more concerned with keeping the economy growing than with preventing a rebound in bad debts. “Banks have every incentive to dole out more loans,” said Yang Qingli, a Beijing-based analyst at BOCOM International Ltd. “When the government is driving in the fast lane, you can’t just stop immediately.” New loans in the nation may surge to a record 11 trillion yuan this year as the government is still concerned about “a possible second dip in the recovery path,” BNP Paribas SA said last week. China’s economic growth accelerated to 7.9 percent in the second quarter.

“We will continue to expand lending and other business to implement the government’s fiscal and monetary policy and help economic growth,” Bank of China’s Wang said. “The key strategy won’t change.” The bank, 67.5 percent government-owned, accounted for 12.2 percent of new loans in China in the first half. Non-performing loans at China’s 17 biggest lenders, almost all of which are state-controlled, fell by 43 billion yuan from the start of the year to 444 billion yuan as of June 30. Foreign lenders, which hold less than 3 percent of China’s banking assets, reported an 11 percent increase in soured debts in the period, according to the banking regulator.

Chinese banks extended a record 7.37 trillion yuan of new loans in the first half, triple the amount offered in the same period a year earlier and 47 percent more than the government’s full-year target, after lending restrictions were eased in November to stem an economic slowdown. “I would say Chinese banks failed the test in dealing with this economic crisis,” said Wen of Fitch Ratings.

Standard & Poor’s said July 10 that credit risks are “mounting” at domestic banks and asset quality is likely to deteriorate this year and in 2010. The weakening of asset quality remains “manageable,” the ratings company said. Bank of China will continue to lend to 10 key industries with government policy support, including steel, shipbuilding and automobile, Wang said. About 30 percent of its loans went to those industries in the first half.

China May Press Geithner on Dollar, Economy in Washington Talks

The dollar may be the focus of Chinese-U.S. talks starting in Washington today as China presses the Obama administration on how it will tame the fiscal deficit and protect the U.S. currency’s value, Morgan Stanley said. Treasury Secretary Timothy Geithner and Secretary of State Hillary Clinton will host two days of meetings spanning topics from the economic crisis to North Korea. The Strategic and Economic Dialogue is the Obama administration’s first with China.

“If the key issue in the past was the renminbi’s exchange rate, now it’s the U.S. dollar,” said Wang Qing, an economist at Morgan Stanley in Hong Kong. The yuan is a denomination of the renminbi. “What China cares about the most is the stability of the dollar and the stability of U.S. policy.” The global slump has highlighted the common interests of the economies, ranked first and third largest in the world, as Vice Premier Wang Qishan seeks to preserve the value of the world’s biggest Treasury holdings and the U.S. pushes China to rely more on domestic demand and not exports for growth.

“Raising personal incomes and strengthening the social safety net to address the reasons why Chinese feel compelled to save so much would provide a powerful boost to Chinese domestic demand and global growth,” Geithner and Clinton wrote in a joint article published in today’s Wall Street Journal. The talks this week will move beyond economic matters for the first time.

Few global problems “can be solved without the U.S. and China together,” Geithner and Clinton wrote. “The strength of the global economy, the health of the global environment, the stability of fragile states and the solution to nonproliferation challenges turn in large measure on cooperation between the U.S. and China.” The two sides will probably discuss ways to revive the dormant six-party negotiations aimed at persuading North Korea to give up its nuclear program, a U.S. official said last week.

“From the provocative actions of North Korea, to stability in Afghanistan and Pakistan, to the economic possibilities in Africa, the U.S. and China must work together to reach solutions to these urgent challenges,” Geithner and Clinton wrote. China’s exchange-rate policy will be discussed, an Obama administration official said at a press briefing last week. The U.S. wants a more flexible yuan, though Geithner has avoided a showdown on the issue, declining to repeat comments he made in written remarks to lawmakers after his Senate confirmation hearing in January that China was “manipulating” its currency.

“This was a most unfortunate thing to say publicly,” said Donald Straszheim, managing principal of Straszheim Global Advisors in Los Angeles. “They think the playing field is basically tilted by China managing its currency.”

Both nations are pumping cash into their economies to revive growth in the face of the worst financial crisis since the Great Depression. Though Premier Wen Jiabao said in March he was worried about the safety of the nation’s U.S. assets, China bought $38 billion of U.S. notes and bonds in May, taking its holdings to $801.5 billion. The U.S. deficit may reach a record $1.85 trillion for the fiscal year ending Sept. 30, almost four times the previous fiscal year’s $455 billion shortfall, according to the Congressional Budget Office.

Federal Reserve Chairman Ben S. Bernanke will brief Chinese officials about how the U.S. plans to keep inflation in check over the next few years, people advised of the plan said this month. In June, Geithner told China that the U.S. wants to shrink its budget gap as soon as an economic recovery takes hold. “Both nations must avoid the temptation to close off our respective markets to trade and investment,” Geithner and Clinton wrote. “Both must work hard to create new opportunities for our workers and our firms to compete equally, so that the people of each country see the benefit from the rapidly expanding U.S.-China economic relationship.”

Housing Recovery: Sell Now Or Your Capital Will Be Trapped

by Charles Hugh Smith

As news reports of housing's "recovery" fill the mainstream media, the devastating effects of rising interest rates are never mentioned: every house with equity becomes a capital trap.

Here's the "housing is recovering" story graphically depicted:

Anecdotally, breathless stories of the return of multiple bids are filtering into a Mainstream Media anxious to report "proof" of a "recovery in housing."

Just for context, let's take a quick look at the Case-Shiller Index:

This translates into a 50% decline in bubblicious areas of the nation: Dr. Housing Bubble: Calif. Housing drops 50% from peak.

As noted in the above article, fully 58% of all California home sales are foreclosure resales. In other words, "the bottom is in, now is the time to snap up bargains."

Not so fast. Let's focus on the key feature of buying a house as opposed to, say, a TV: very, very few people buy a house with cash. The vast majority of real estate purchases are financed with mortgages--debt.

And credit is lent at a rate of interest. As a result, the relationship between interest rates and the value of real estate is a see-saw. Buyers can only afford X per month in mortgage payments. If interest rates double, they can only afford to buy a house at a much lower valuation. Here are graphic depictions of the relationship:

In other words, when interest rates double, house prices will drop in half, regardless of any other conditions.The newly risk-averse lenders will only originate mortgages which amount to roughly a third of the borrower/buyer's monthly income, and so this is the metric which controls the price of housing.

The price can be set to whatever level the seller desires, but it will eventually settle to the price the buyers can actually afford.

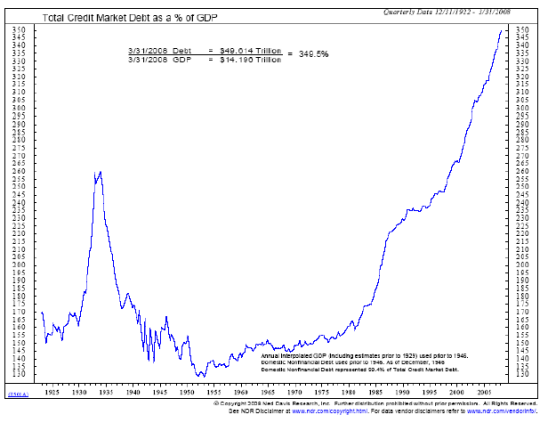

So why am I suggesting interest rates could double from 4.5% to 9% in the near future? Please consider this chart of total U.S. debt, 1929-2008:

The above debt expansion might remind you of the curveset to the right: exponential (and thus unsustainable).

We've all read about the $2 trillion Federal deficit for this fiscal year; but let's not forget that corporations, local governments and agencies and real estate buyers also want to borrow money. Bottom line: the demand for surplus capital far exceeds the supply of surplus capital globally.

Every other government on the planet (yes, even the Chinese government) is also anxious to borrow huge sums of money from someone to fund their exploding deficit spending. Courtesy of frequent contributor U. Doran, here is a report from Sprott Asset Management on how dependent the U.S. ison non-U.S. capital: The Solution...Is the Problem.

The excellent John Mauldin recently issued a report on how governments want to borrow $5 trillion but there is no more than $3 trillion available to borrow: Buddy, Can You Spare $5 Trillion?

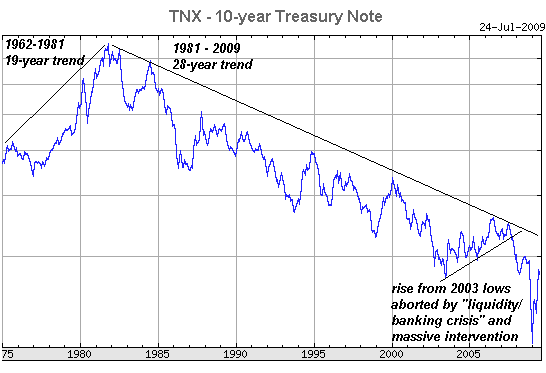

This is the classic "unstoppable force hitting the immovable object"--oh, but wait: interest rates are set by the market and are thus quite movable.Consider this chart of the 10-year U.S. Treasury bill yield:

Note that the rise from 2003 lows was aborted by a global "flight to safety" and a massive intervention in the capital markets by the Federal Reserve and U.S. Treasury which caused interest rates to plummet to unprecedented lows.

But longer term, this cycle of declining interest rates is already extremely long in tooth at 28 years and counting. the average interest rates cycle has historically measured about 20 years in length, suggesting this cycle is due for a turn and the start of a 20+-year cycle of rising interest rates:

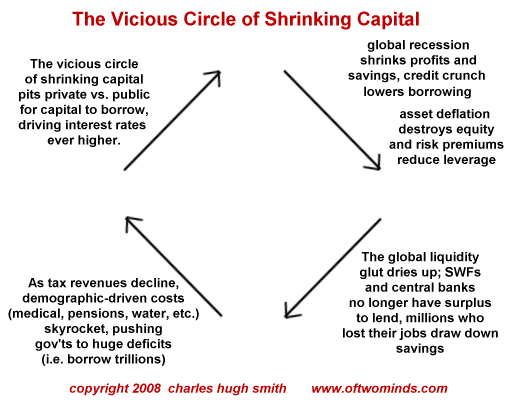

But wait: it gets worse. Surplus money looking for a home is drying up even as the demand for surplus capital skyrockets. This vicious circle can bedisplayed thusly:

The net result is interest rates will have to rise--and soon. While it is impossible to predict exact dates, simple laws of supply and demand dictate that rates will soon rise and will rise steeply as the shortfall between what governments want to borrow and what's available to borrow becomes visible (not to mention private demand for capital).

As interest rates rise, then the Capital Trap shuts on all equity locked in real estate.I covered this subject last year: The Housing Capital Trap Snaps Shut(May 28, 2008)

The mechanism can best be illustrated with an example. Let's say a homeowner who bought long ago has a $100,000 mortgage on a home which was once worth $450,00 at the bubble peak. Now the property has sunk to a value of $250,000. The owner still has $150,000 in equity: quite a substantial sum.

But if interest rates double, then the house would have to fall roughly in half to be affordable to buyers. Equity would shrink to a mere $25,000. Or alternatively, if the owner insisted the "true value" was still $250,000 based on other metrics, then the capital is trapped as the house cannot be sold in the marketplace.

Thus it can be argued that to the degree a house is an investment and the basis of household wealth, the owner would be wise to sell the house now in this brief "housing recovery" while rates are still low, pocket the $150,000 equity (For simplicity's sake, I leave out commissions, property taxes, etc.) and rent an equivalent home.

As interest rates rise, that equity will begin earning a decent return in a simple savings account.

I know this concept--that savings will accrue more wealth than equity in a house--is so alien as to be absurd. We have been conditioned by the past three decades of explosive rises in real estate valuations and declining interest rates to believe "real estate always rises" and cash is essentially trash. But the 28-year long orgy of ever-lower rates is ending, and may end abruptly, and soon, as the U.S. Treasury seeks not just to borrow trillions more but also roll over expiring bonds.

The key concept here is that a house is only worth what someone can afford to pay for it. Thus we must be wary of divining "the bottom" based on metrics which don't take rising interest rates into account.

Why can't the Fed just print the $2 trillion the government wants to borrow? Wouldn't that solve the problem? In theory, perhaps, but in practice, when the Fed did exactly that, announcing it was printing $300 billion to buy Treasuries, the bond market reacted violently by pushing rates up dramatically.

Printing trillons of dollars is seen as inflationary by the bond market, and if inflation is being ramped up to 4%, why buy a bond that pays 2%? To keep buying bonds which are guaranteed to lose money is simply unwise. The net result is the Fed cannot just print $3 trillion (don't forget all the bonds which have to be rolled over) and buy Treasuries--the bond market would instantly demand much higher rates to compensate for the additional risks of inflation.

Real estate industry cheerleaders counter by sayinghousing "always rises in inflationary eras." By that theyrefer to the 70s, when real estate shot up alongside rising inflation. But what they forget is that housing was rising from extreme levels of affordability, and that the Baby Boom was entering its prime homebuying decade in the 70s.

Now we have 18.7 million vacant homes, a high level of unaffordability and rising interest rates.

There are many psychological reasons to own property: the sense of security, that you can do what you want with the home and yard, and so on. These are very real and valuable. But as an investment, rising interest rates will trap whatever capital is sunk in the house. To the degree a house is not just shelter and psychological security but an investment, that matters.

Ilargi: I've long said that I sort of expect perhaps some country somewhere to blow open the derivatives bubble. But Italy, of all places?

JPMorgan, UBS, Deutsche Bank May Face Indictment in Milan Derivatives Case

The Italian prosecutor probing alleged fraud on derivatives contracts with the City of Milan will seek indictments against four banks after completing his investigation, two people familiar with the case said. Milan Prosecutor Alfredo Robledo will seek fraud charges against UBS AG, Deutsche Bank AG, JPMorgan Chase & Co. and Depfa Bank Plc, said the people, who asked not to be identified because the decision hasn’t been publicly announced. Robledo also is requesting that 14 individuals stand trial on fraud charges, one of the people said.

Robledo is trying to prove that the London units of the banks made about 101 million euros ($143 million) in so-called illicit profits by arranging contracts that adjusted payments on Milan’s 1.7 billion euros of bonds. The four banks defrauded Milan by misleading the borrower on the economic advantage of the financing and hid their commissions on the derivatives, Robledo has alleged. “We are confident that the strength of our legal position will ultimately be demonstrated through the judicial process,” JPMorgan said in an e-mailed statement today. “The JPMorgan employees involved in the transactions acted with the highest degree of professionalism and entirely appropriately.”

Zurich-based UBS, Frankfurt-based Deutsche Bank and Depfa Bank got back 164 million euros of assets seized by the authorities after prosecutors accepted a cash guarantee, three people familiar with the case said July 1. The banks deposited a total of 56 million euros in exchange for the assets that were seized on April 27, said the people. JPMorgan, which wasn’t part of that agreement, reached an accord in the past week to reduce the 92.3 million euros of its assets seized to 44.9 million euros, one of the people said. The City of Milan is separately suing the four banks after it lost money on derivatives it bought from the lenders in 2005.

Loss provisions spook Deutsche investors

Deutsche Bank on Tuesday confirmed the rebound in its investment banking operations, but increased its provisions substantially in the second quarter in a sign of the difficult economic climate that is set to delay the banking sector’s return to full health. Germany’s largest bank reported net income of €1.1bn ($1.57bn) in the second quarter, driven by investment banking in what Josef Ackermann, chief executive, said in a statement were “satisfactory” results.

The results exceeded a consensus estimate by analysts of about €1bn but were slightly below those of the first quarter. Shares in Deutsche Bank were 11 per cent lower at €46.28 in afternoon Frankfurt trading. Provisions against credit losses rose to €1bn, double the amount in the preceding three months and about the same as Deutsche Bank ’s total provisions during 2008. The sum included €433m related to two counterparties – unnamed by the bank – as well as a rise of more than 50 per cent in provisions against lending to private and business clients, driven in particular by the continued deterioration of lending in Spain.

In total Deutsche Bank took €1.4bn in one-off charges during the quarter. The bank declined any firm forecasts for 2009, with Mr Ackermann saying the outlook for would be strongly influenced by progress in the global economy. “We have witnessed stabilisation of the world’s banking industry and financial markets. Increased liquidity and lower volatility in financial markets are both supportive for our business,” he said. Revenues of €7.9bn were higher than in the first quarter but net interest income was significantly below analysts’ estimates

Deutsche Bank ’s core investment banking business more than doubled its revenues compared with the second quarter of 2008, with the bank pointing to “one of the best quarters ever” for interest rate trading. Foreign exchange trading and money markets were at a slightly lower level than in the first quarter, but revenues from equity sales and trading were the highest in 18 months. Investment banking produced pre-tax income of €828m compared with a €311m loss in the same quarter last year.

However, profits in Deutsche Bank’s other three banking divisions fell compared with a year ago. Wealth management remained troubled, with a 36 per cent fall in revenues and a pre-tax loss of €85m. The bank took a €110m charge on property held by Rreef, its alternative asset management business. Pre-tax profits in private and business banking fell from €328m a year ago to €55m, partly reflecting €150m in redundancy costs.

Reflecting Deutsche Bank’s attempts to shrink its balance sheet and reduce leverage, total assets fell by about 18 per cent to €1,730bn during the quarter, the lowest level since the financial crisis began in 2007. Using an alternative calculation under US accounting rules, Deutsche said it had cut its balance sheet by 31 per cent during the past 12 months. The bank’s tier one capital ratio rose to 11 per cent – its highest level since the crisis began – while the core tier one ratio, excluding so-called “hybrid” capital, was 7.8 per cent compared with 7.1 per cent at the end of March.

Investing rules for the End of Civilization

In his 2008 bestseller, "Wealth, War and Wisdom," hedge fund manager Barton Biggs warns that investors must "assume the possibility of a breakdown of the civilized infrastructure." And to prepare for a breakdown of civilization, "your safe haven must be self-sufficient and capable of growing some kind of food ... It should be well-stocked with seed, fertilizer, canned food, wine, medicine, clothes, etc." Bloomberg Markets suggested that by "etc." he meant guns, as Biggs added "a few rounds over the approaching brigands' heads would probably be a compelling persuader that there are easier farms to pillage."

That warning's not from a hippie radical. Biggs was a respected Wall Street guru at Morgan Stanley for 30 years. As the chief global strategist Institutional Investor magazine put him on its "All-America Research Team" 10 times. Smart Money said: "Biggs is without question the premier prognosticator on the international scene and a mover of markets from Argentina to Hong Kong." Biggs is advising America's wealthy elite. But what about Main Street Americans? Investors often ask me where to invest today, even Bogleheads and investors committed to the Lazy Portfolio strategy. They see the Goldman Conspiracy manipulating this rally. That worries many.

What do you believe? What value do you give to "the future." First, answer these three questions: What's your investment strategy if you know you might die on Dec. 21, 2012, or possibly this year after getting a negative diagnosis from an oncologist or maybe not till 2050 when the United Nations says global population will be 50% higher (from 6 billion now to 9 billion), while demand for energy, oil, gas and coal doubles and the global supply of those commodities remains relatively constant.

Disaster films, terminal illnesses, 2050 and 'The End'

Behavioral economists have answers. But your gut's also good at predicting. So here's what you'll likely do:

- You'll go see the new disaster film, "2012" about the end of the Mayan calendar. After all, it's by the same director who "destroyed" the earth in "The Day After Tomorrow," "Independence Day" and "Godzilla." No new investment strategies, but a must-see film, a great catharsis and distraction.

- If you had a terminal illness, the future is here, now. There's no tomorrow. You're concerned about protecting loved ones and future generations with what you have, and enjoying time with them.

- But how to invest for the "End of Civilization" coming around 2050? The next 40 years will be confusing: Accelerating struggles between aging populations and disenchanted youth, soaring commodity prices, global warming, peak oil, food shortages, famine, blackouts, rationing, civil disorder, increasing crime, worldwide jihads, riots, anarchy and other dark scenarios of a tomorrow with "warfare defining human life."

Yes, that's how doomsayers label the worst-case scenario. It also must be what Ultra-Conservative-Guru Biggs worries about in his darker moments. So back to the question: What will Main Street investors do? Here again, even with the planet's survival threatened, they'll go watch "2012," be entertained, experience a catharsis, feel relieved, and afterwards, have dinner, slip back into denial. And later, they'll vote against anything that offers solutions to future problems, especially if it raises taxes.

Why? Very simple: Our "Brains Aren't Wired to Fear the Future," writes New York Times columnist Nicholas Kristof. We're wired to respond to crises, while pushing off the real big problems (health care, Social Security, etc.) That's basic behavioral economics: Over tens of thousands of years, evolution has programmed our brains so that collectively we will behave counter-productive with the future, making an "End of Civilization" scenario inevitable, a foregone conclusion, a self-fulfilling prophecy. Why? Because our brains are handicapped, we are literally incapable of acting soon enough to solve the problem.

Six simple rules

But there must be a very small percentage of you out there with a desire to make your remaining days on Earth as pleasant as possible for you and your loved ones. So here are "Six New Rules till the End of Civilization 2050." If they don't scare you, hopefully they'll amuse you. Or better yet, wake you up, maybe get you into action ... before it's too late ... before your grandkids are fighting over what little is left:

1. Greed is really good

Yes, if you are going to follow the same advice as the rich, you and your family always come first. Grab more than your share, many times what's fair. No remorse, because 2050 is coming sooner than you think. Create a protective wall of money and resources that will make whatever time's left as comfortable as possible.

2. Invest in Goldman Sachs and its Wall Street co-conspirators

Seriously, these guys are the poster boys for the word "greed." The Goldman Gang, Goldman Conspiracy, whatever you call them, these guys just took control of Washington and the Treasury; their rapid recovery is proof that "greed is great." Do what they do. Amass as much capital and goods as possible, ignoring the rest of us, then cruise to the finish line.

3. Frugality, stockpiling, hoarding

"The Millionaire Next Door" says it's very simple: "Frugal Frugal Frugal! ... Millionaires live well below their means ... Being frugal is the cornerstone of wealth-building." That way you can stash away lots more for later when the going gets rough, when others attack to get what you've stockpiled.

4. Return to your roots

Remember Biggs' advice about subsistence farming. Survival instincts and personal ingenuity will be your best investment. Your family could be without electricity, water, gasoline in the final days, so keep "well-stocked with seed, fertilizer, canned food, wine, medicine, clothes, etc. Think Swiss Family Robinson."

5. Global warfare, plus ammo and guns

Five years ago Fortune did report on the "Pentagon's Weather Nightmare." Yes, the military warned of "the mother of all national security issues" as "the planet's carrying capacity shrinks, an ancient pattern reemerges: the eruption of desperate all-out wars over food, water, and energy supplies." So invest in the defense industries America needs as the rest of the world reacts more to our greed.

6. Accept death

Back in 1973, my first year at Morgan Stanley, I read Ernest Becker's brilliant Pulitzer Prize winner, "The Denial of Death." Today his message is even more powerful: Yes we will all die, tomorrow. But to enjoy the days left, you must accept death today ... accept even now as behavioral economists warn us that our brains are our own worst enemy, as well as the planet's, for we are on a self-destruct path of no return.

Parable at the Pearly Gates

Too macabre for you? So you don't miss the satire, here is a final message, in the spirit of Milton Berle's classic movie, "Always Leave Them Laughing." It's from USA Today, told by that great comedian Carol Leifer:"Mother Teresa died and went to heaven. God greeted her at the Pearly Gates. 'Be thou hungry, Mother Teresa?' asked God. 'I could eat,' Mother Teresa replied. So God opened a can of tuna and reached for a chunk of rye bread, and they began to share it. While eating this humble meal, Mother Teresa looked down into hell and saw the inhabitants devouring huge steaks, lobsters and pastries. Curious but deeply trusting, she remained quiet.