Donnie Cole. 'Our baby doffer,' they called him. This is one of the machines he has been working at for some months at the Avondale Mills, Birmingham, Alabama. Said, after hesitation, 'I'm 12,' and another small boy added, 'He can't work unless he's twelve.' Child labor regulations conspicuously posted in the mill

Ilargi: I see all sorts of people claim that Germany, France and Japan are now no longer in a recession. This is an idea based on a set of numbers that cover one single quarter. While there may well be some technical interpretation that says that a recession is over as soon as one quarter, month, or week, looks positive, I don't see it contributing much to anyone's credibility. That is, if numbers for this month or quarter, or subsequent ones later in the year, turn negative again, what will be the party line then? That a second recession has started hot on the heels of the first one?

Moreover, even if Germany and France could find a way to make these 2nd quarter claims stick, they are, as I mentioned a few days ago, surrounded by neighbors that are mired deep in their respective doghouses, and if they remain there, they’ll draw the two right back in with them. As for Japan, that country has lived through such a long time of such profound economic trouble that only caution vis-à-vis one-off numbers would seem to constitute an appropriate approach.

And then there's the rest of the world, starting with the US and UK, which have spent obscene amounts of yet-to-be-earned revenues, but are still hovering below the zero line, despite using the most creative accountancy money can buy. All in all, "the end of the recession" sounds like a call that's ridiculously premature, if not simply ridiculous, period. The desire for this thing to be over gets the better of objective reasoning every single time a number is discovered that's not painted in thick red strokes. And whereas optimism may be a noble trait, realism can't be all that far behind. If this recession lasts until 2012, and turns into a depression on its way there, the sunny calls will look preposterous. But for some reason the rose-colored pundits don't seem to mind looking foolish. Perhaps it's a group thing; they sure don't risk standing out from the crowd.

That's a long detour to get where I wanted to be: the -mental- visualization of the present financial (as well as economic and political) crisis in all its aspects. If the picture of a recession that you have in your head is one of a stone being thrown out of the window of a high-rise, you will automatically assume it will have to keep on falling all the way down, and if and when it stops doing that, however briefly, the picture doesn't fit the assumptions anymore. Hence, you will conclude that the recession must be over.

You are using the wrong image. The picture that best describes the way in which recessions and depressions behave is that of a boulder rolling down the side of a mountain. It doesn't go straight down, it follows the shape of the slope, and it will hit all sorts of objects along the way that will interrupt its fall, and perhaps even cause it to bounce upward for a few seconds. But it's certain to resume its way down and keep on going, for reasons Isaac Newton very eloquently explained, unless and until it finds a new equilibrium, which will most likely happen at the foot of the slope.

To complete the metaphor, you could add that only at the moment the new equilibrium has been reached, the millions of little human ants can once again go about their daily grind of dragging the boulder back up the mountain. A nice little last visual detail for your viewing pleasure: the angle of the slope is determined by the amount of debt that exists right before the moment the boulder is pushed off the top of the mountain.

Quote of the day:

....... the banking industry is an integral part of the UK economy and as such is more powerful as a sector than the UK government and the UK regulators put together.

U.S. housing starts, producer prices fall in July

Ground breaking for new U.S. homes fell unexpectedly in July, but a rise in single-family home construction for a fifth straight month kept hopes alive the economy was poised to recover from recession. The Commerce Department on Tuesday said housing starts fell 1 percent to a seasonally adjusted annual rate of 581,000 units, well below market expectations for 600,000 units.

June's housing starts were revised up to 587,000 units from the previously reported 582,000 units. Groundbreaking for single family homes, the worst-hit part of the housing market, rose 1.7 percent to an annual rate of 490,000 units -- the highest since October. "The single-family sector continued to edge higher and that was the silver lining of the report," said Michelle Meyer, an economist at Barclays Capital in New York. U.S. stock index futures pared gains, while U.S. government debt prices trimmed losses after the weak housing and prices data.

While data has pointed to the likely end of the recession, analysts have warned of a weak recovery as rising unemployment crimps consumer spending. A higher-than-expected quarterly profit reported by Home Depot Inc on Tuesday helped ease investor fears as the world's largest home-improvement chain partly offset weak sales with cost cutting. No. 2 U.S. discount retailer Target Corp also reported better than expected results.

Compared to July last year, housing starts dropped 37.7 percent. New building permits , which give a sense of future home construction, fell 1.8 percent to 560,000 units in July, and were down 39.4 percent from a year ago . The inventory of total houses under construction fell to record low 609,000 in July, the department said, while the total number of permits authorized but not yet started also hit a record low at 102,300.

A separate report from the Labor Department showed U.S. producer prices fell 0.9 percent versus a 1.8 percent gain in June. Compared with the same period last year, producer prices were a record 6.8 percent lower in July. Core producer prices, which exclude food and energy costs, edged 0.1 percent lower in July compared with a forecast for a 0.1 percent rise, and after a 0.5 percent increase in June. The core producer price index stood 2.6 percent higher measured on a year-on-year basis, versus a forecast for a 2.8 percent advance.

US Wholesale Prices Fell In July, Showed Biggest Drop In 60 Years Over Last Year

Wholesale prices dropped sharply in July, and over the past 12 months fell by the largest amount in more than six decades of record-keeping. The Labor Department said Tuesday that wholesale prices dropped 0.9 percent last month. That's triple the decline economists had expected and was driven by big decreases in both energy and food costs. Over the past 12 months, the prices of goods before they reach store shelves fell 6.8 percent.

Core inflation, which excludes energy and food, also was well-behaved. It dropped 0.1 percent in July, better than 0.1 percent gain economists expected.

With inflation under control, some may worry about a dangerous bout of falling prices that can also drive wages down, but most economists said deflation remains a remote threat. The last period of deflation in the U.S. occurred in the 1930s during the Great Depression. "Deflation-worriers will find some cause for concern in the general picture, though the broad pattern remains one of gently oscillating monthly price changes, rather than sustained tip into decline," Pierre Ellis, senior economist at Decision Economics, wrote in a note to clients.

Meanwhile, housing starts and applications for future projects both dipped unexpectedly last month, a sign that the building industry's recovery from the prolonged housing slump is likely to be bumpy and gradual. The Commerce Department said new construction fell 1 percent in July to a seasonally adjusted annual rate of 581,000 units. Economists expected a pace of 600,000 units. Applications for building permits, an indicator of future activity, fell 1.8 percent to an annual rate of 560,000 units, also below economists' estimates of 580,000 units. The declines in the Producer Price Index showed wholesale inflation pressures were even more subdued than prices at the consumer level. The government last week reported that the Consumer Price Index was unchanged in July and over the past 12 months fell 2.1 percent, the biggest decline in nearly 60 years.

For July, wholesale energy prices fell 2.4 percent after having surged 6.6 percent in June. Gasoline dropped 10.2 percent and home heating oil plunged 11.9 percent. Food prices at the wholesale level fell 1.5 percent last month, reversing a 1.1 percent rise in June. A big drop in vegetable prices led the overall decline, but beef and egg prices also fell. The 6.8 percent decline in wholesale prices over the past year was the biggest since the government began keeping such records in 1947. It surpassed the 5.2 percent drop in the period ending in August 1949. The 0.1 percent drop in core inflation left those prices rising 2.6 percent over the past 12 months. In July, prices for passenger cars fell 1.7 percent, the biggest decline in nearly three years.

On Wall Street, stocks rose a bit in morning trading following gains in overseas markets driven by upbeat economic news from Germany, Europe's largest economy. The Dow Jones industrial average added about 60 points and broader indices also rose. The 1.8 percent gain in wholesale prices in June was the biggest one-month increase since November 2007. But economists said it represented a temporary burst and was not the beginning of a dangerous bout of spiraling prices. Economists believe energy prices, which had propelled much of the gain, will level out and that the weak economy will keep the lid on overall inflation. Crude oil prices topped $72 a barrel in June but were trading below $67 per barrel Tuesday.

After hitting a record at $147 per barrel in July 2008, oil prices slid for most of the rest of 2008, a decline that trimmed earnings at oil companies. Many major oil companies, including Exxon Mobil Corp., Chevron Corp., Royal Dutch Shell and French petroleum giant Total SA, recently reported second-quarter profit declines of more than 50 percent. The Federal Reserve believes inflation will remain subdued for some time as the country struggles to emerge from the worst recession since World War II. The Fed last week they planned to keep a key bank lending rate at a record low near zero for an "extended period," despite seeing signs that the economic downturn was "leveling out."

US Mortgage Deliquency Rate Hits All-Time High In 2nd Quarter

The delinquency rate on U.S. mortgage loans hit an all-time high in the second quarter, but the pace of growth for the rate slowed, a possible sign the mortgage crisis may be beginning to turn the corner. Data provided by credit reporting agency TransUnion shows the ratio of mortgage holders who are 60 days or more behind on their payments increased for the 10th straight quarter, to 5.81 percent nationwide for the three months ended June 30. That's up 65 percent, from 3.53 percent, in the 2008 second quarter.

Deliquency of 60 days is considered a precursor to foreclosure, because of the difficulty homeowners would have coming up with two back payments to bring themselves current. While the deliquency rate hit a new high, however, the increase from the first quarter to the second was 11.3 percent. In the two prior quarters, the rate jumped nearly 16 percent. That slowdown may be a good sign, said FJ Guarrera, vice president of TransUnion's financial services division. "We have reason to be cautiously optimistic," he said.

While there's no way to know exactly why the pace of growth is slowing, Guarrera said, it appears that programs aimed at helping distressed homeowners from both the government and mortgage lenders are beginning to help. In addition, he said, consumers are being more careful with their spending. For the second quarter, Nevada, Florida, Arizona and California remained the four states with the highest deliquency rates, mirroring the locations where foreclosures are the highest. Nevada's deliquency rate spiked to 13.8 percent, from 11.6 percent in the first quarter and 6.63 percent in the 2008 second quarter.

In Florida, the delinquency rate rose to 12.3 percent, from 11 percent in the first quarter, and 6.47 percent in the 2008 second quarter. TransUnion culls its database of 27 million consumer records to produce the statistics. North Dakota and South Dakota remained the states with the lowest deliquency rates. North Dakota's rate actually edged down a hundreth of a percent, to 1.5 percent. Ohio, Idaho and Connecticut also saw decreases from the first quarter to the second. Guarrera saw particular importance in the statistics for Ohio, where deliquency edged down to 4.57 percent from 4.58 percent in the first quarter.

The Ohio rate remains up substantially from the 2008 second quarter, when it stood at 3.77 percent, but the quarter-over-quarter decline, while small, was significant, he said. "I believe this is a precursor to recovery," Guarrera stated, noting that the recession was felt first in the Rust Belt and Sun Belt states. "We see this as a really good sign." Not all of the news was positive, Wyoming and Utah, two states that have been far from the center of the foreclosure crisis, saw their deliquency rates jump the most, to 2.85 percent and 4.68 percent, respectively. Guarrera noted both states has a small populations, so results can be skewed by small changes.

TransUnion still expects the mortgage deliquency rate to keep rising, but now expects the national rate to top out just under 7 percent around the end of the year. That's a slight revision from earlier in the year, when the company predicted the rate would go past that mark. Nevertheless, it's going to take about a year before the rates start to fall across most of the country, Guarrera said, and it will be quite some time before the national rate returns to its historic norm between 1.5 percent and 2 percent. "Forecasts are telling us that the recovery will be slow," he said.

Tax Bills Put Pressure on Struggling Homeowners

Hard times are causing more homeowners to fall behind on their property taxes. But in thousands of cases, they are not responsible to their local governments, but to private companies that charge double-digit interest and thousands of dollars in service fees. This is because in recent years struggling cities and counties have sold their delinquent tax bills to the highest bidder. It seemed a painless way to turn old debts into cash to finance schools or public services.

But housing advocates say the private companies may be exacerbating the foreclosure crisis, pushing out homeowners faster than would governments, which are increasingly concerned about neighborhoods becoming wastelands of abandoned properties. "In the beginning, you’re getting this immediate windfall of cash," said Anita Lopez, the auditor of Lucas County, Ohio, which sold off more than 3,000 tax liens for $14.7 million. The county includes Toledo. "But when you think about abandoned properties, foreclosed properties — the cost to the community is far more expensive than the short-term benefits."

Investors say the arrangement actually benefits everyone. School districts, fire departments and public parks get an infusion of cash. The investors take on a risky but potentially high-yielding investment. And taxpayers do not have to pick up the slack from scofflaw landlords or tax evaders. Governments, of course, can charge interest and penalties too, and they foreclose on properties for back taxes. But governments charge interest rates that are half what private investors charge — often offering no-interest payment plans — and are also more likely to be concerned about the long-term prospects of neighborhoods.

In Toledo, one of the areas hardest hit by the downturn and by private lenders holding tax liens, homeowners like Richard Fix are facing foreclosure for a few thousand dollars in overdue taxes.

Mr. Fix said he lost his job with Chrysler in January 2008 and took a lower-paying job. As he and his family struggled to pay their mortgage, credit cards and other bills, he said they fell behind on $5,900 in taxes. "I’m in a no-win situation at this point," he said.

With the economy faltering and property values plunging, homeowners and landlords are falling behind on their bills or abandoning their property, just as governments are facing huge budget shortfalls. Private investors step in and buy tax liens, paying governments upfront all or part of the value of the taxes. The investors then get the right to foreclose on the properties, taking priority over mortgage lenders, and to charge interest rates as high as 18 percent on the unpaid taxes. "It beats the heck out of any certificate of deposit," said Howard Liggett, executive director of the National Tax Lien Association.

Because the sales occur in a patchwork of cities and counties across more than two dozen states, there are no figures tracking the number of tax-lien sales nationwide. The liens that are sold come from cases in which homeowners pay taxes to the local government, not through their lenders. But Mr. Liggett, whose group represents tax-lien investors, said they generated about $10 billion every year. In 2006, Lucas County began selling off its overdue tax certificates to a New Jersey company named Plymouth Park Tax Services, a subsidiary of JPMorgan Chase. It also operates under the name Xspand.

The company, once run by the former governor of New Jersey, James J. Florio, was sold to Bear Stearns and then absorbed into JPMorgan after Bear’s collapse last year. Today, Plymouth Park is one of the largest players in the tax-lien business. Plymouth Park has filed more than 1,000 foreclosure actions against delinquent taxpayers, more than any single mortgage lender in the county. But it says that it has only foreclosed on 56 of those filings. Plymouth Park has bought $2 billion in tax liens across the country since 2008, and says the number of foreclosures around Toledo is an aberration.

All told, foreclosures in Lucas County rose to 4,093 in 2008 from 3,486 in 2007, and they are on track to be 7 percent higher this year than 2008, according to county figures. Plymouth Park’s president, John Garzone, said the company tried to set up payment plans with homeowners and foreclosed only as a last resort. The company said that the government would most likely have initiated many of those foreclosures on its own. "Less than 1 percent of our overall investment actually becomes a foreclosed-on property," Mr. Garzone said. "Our main interest is to try and get the properties back onto the tax rolls."

But now, many are in danger of falling off them. Christopher Clark, 57, lives in the Toledo home where he spent his teenage years and where he cared for his mother before she died. He said he scrapes by on $674 in monthly disability payments and assistance from friends and by selling old books and a pipe collection on eBay. He amassed $6,450 in delinquent taxes over the years, a debt that was sold to Plymouth Park in 2007 and 2008. The company added $1,853 in interest charges to the original bill, and various fees, according to Mr. Clark’s lawyer, Deborah Tassie, and filed for foreclosure. "I’m still in denial," Mr. Clark said. "I’ve been here through good times and bad, lousy neighbors and good neighbors. What I’m going to do, I have no idea."

Plymouth Park said that it charged fees related to its legal costs only, and did not charge homeowners for its own administrative costs. The county treasurer who arranged the tax sales, Wade Kapszukiewicz, said they were aimed at "out-of-town land speculators" and the most chronic tax delinquents, and were intended to avoid the elderly and disabled. "What is the alternative?" he said. "The alternative is to let people not pay taxes and do nothing about it." But housing advocates in Lucas County said homeowners were overwhelmed by the fees and interest rates. Debts of $3,300 grew to $6,800. And while Plymouth Park offered a payment plan, lawyers said that many homeowners did not have enough money to make upfront payments of a $1,000 or more.

Danyell Copeland, 36, is in court over a tax bill of less than $2,000, her lawyer said. Ms. Copeland, who works as a cook at the University of Toledo, said she had been fallen behind on her bills after her hours and overtime were cut. She chose to not pay her taxes so she could make her mortgage payments, she said. Now she worries about losing the two-bedroom house where she grows tomatoes and peppers in the garden, and where her niece and nephew spend the summer. "This is not just a house," she said. "This is a home."

Unemployment Spike Compounds Foreclosure Crisis

The country's growing unemployment is overtaking subprime mortgages as the main driver of foreclosures, according to bankers and economists, threatening to send even higher the number of borrowers who will lose their homes and making the foreclosure crisis far more complicated to unwind. Economists estimate that 1.8 million borrowers will lose their homes this year, up from 1.4 million last year, according to Moody's Economy.com. And the government, which has already committed billions of dollars to foreclosure-prevention efforts, has found it far more difficult to help people who have lost their paychecks than those whose mortgage payments became unaffordable because of an interest-rate increase.

"It's a much harder nut to crack, unemployment," said Mark A. Calabria, director of financial regulation studies at the Cato Institute. "It's much easier to bash lenders than to create jobs." During the first three months of this year, the largest share of foreclosures shifted from subprime loans to prime loans, according to the Mortgage Bankers Association. The change to prime loans -- traditionally considered safer -- reflects the growing numbers of unemployed who are being caught up in the foreclosure process, economists say.

Rep. Barney Frank (D-Mass.), chairman of the House Financial Services Committee, has proposed using $2 billion in government rescue funding to provide emergency loans to these borrowers. "We are going to be seeing more foreclosures because of prolonged unemployment," he said. "These are people who weren't in trouble and wouldn't be in trouble if they hadn't lost their job."

Unlike the borrowers with subprime mortgages who helped ignite the housing downturn more than two years ago, Deepak Malla, 42, fell behind on his payments when his information technology job was shipped overseas late last year. He does not have a subprime loan, and he made a 20 percent down payment when he bought his five-bedroom house in Ashburn in 2005. The payments were affordable -- until he lost his job. Last year, about 40 percent of borrowers who sought help at NeighborWorks, a large housing counseling group, cited unemployment or a pay cut as a primary reason for their delinquency. Now it is about 65 percent. The number citing a subprime loan fell significantly.

"Rising unemployment, for the sake of this downturn, has magnified things considerably," said John Snyder, manager of foreclosure programs for NeighborWorks. "It's less about the payment adjustment." When a subprime borrower becomes delinquent because of a hefty payment increase, the fix often involves lowering the interest rate to its original level. Unemployment poses a more difficult challenge, industry officials and consumer advocates said. During extended periods of joblessness, the borrower accrues large late fees that drive up monthly payments. And a new job often comes with lower pay, making it more difficult to catch up.

When Malla landed another job earlier this year, he took a pay cut of more than 25 percent. He launched a six-month campaign to get Wells Fargo to lower his mortgage payments from $3,500 to reflect his new financial reality, but he was rebuffed repeatedly. "I wanted to work out with them based on my current scenario," Malla said. He considered refinancing his mortgage, which had a 5.8 percent interest rate, but his home's value had fallen significantly since the market peak, making that impossible. Instead, the lender recommended that he sell the house in a short sale. That would mean selling for less than he owed and walking away with nothing.

"They didn't say why -- just that [a loan modification] is outside the investor guidelines," Malla said. "I was very, very frustrated." (After being contacted by The Washington Post, a Wells Fargo spokesman said Malla does qualify for a loan modification after all.) Banks and government regulators are studying how to address the shifting nature of the crisis, which has been exacerbated by falling home prices. When the housing crisis began in 2007, the unemployment rate was about 4.6 percent. It hit 9.4 percent last month, and many economists expect it to reach 10 percent by the end of the year.

Hope Now, a government-backed group of mortgage lenders, has established a task force to look at how to best help unemployed borrowers; one strategy involves creating new types of loan modifications. The Obama administration is also studying the issue as it considers how to make its foreclosure prevention program, known as Making Home Affordable, more effective. Many housing experts say it will take more than the $75 billion the administration has already said will be spent on foreclosure prevention.

Several economists at the Federal Reserve Bank of Boston have proposed creating a government lending or grant program for unemployed borrowers, lowering their payments for up to two years while they look for work. Such a program could cost $25 billion annually and help 3 million homeowners, lowering their payments by 50 percent on average, according to the economists' proposal. Currently, unemployed borrowers have few options to save their homes. Banks often will allow two or three missed payments, known as forbearance, to give borrowers time to find a job. Others offer to temporarily lower their payments by 50 percent. But both of these options are not permanent and are ill-suited to the current crisis, consumer advocates and industry officials say.

Part of the problem is that it is taking longer for borrowers to find new employment -- a three-month suspension of payments often is not enough. The number of unemployed people who have been looking for a job for more than 26 weeks rose more than 500,000 last month. And under the current system, once borrowers resume payments, their monthly balances rise to make up for overdue amounts. "Who knows what's going to happen at the end of the [forbearance], even if they can get it?" said Paul S. Willen, senior economist for the Federal Reserve Bank of Boston.

Citigroup established a test program for unemployed workers in March, offering to lower their payments to $500 a month for three months. But few of the 600 or so borrowers who have qualified for the plan have reported that they were able to find new jobs, and Citigroup is considering lengthening the period, company officials said. The test has shown that borrowers are at their most motivated shortly after losing their job, so the company may also lift a requirement that homeowners miss at least two payments to qualify for assistance. No decision on the changes has been made, company officials said.

The program has reinforced Citigroup's conclusion that "unemployment is in fact the root cause of many of the delinquencies," said Sanjiv Das, chief executive of CitiMortgage. The trick, he said, is to give borrowers enough assistance to keep them motivated to find a job quickly so they can resume making full mortgage payments. Under the federal foreclosure prevention program, unemployment insurance can be counted as income when a borrower applies for a modification. But the borrower must show eligibility for at least nine months of unemployment checks.

Bill Kachur of Jacksonville, Fla., lost his job as an online training instructor for a large government contractor in January and began scrambling to protect his four-bedroom home, purchased in 2000, from foreclosure. He has been able to scrape together enough to keep up his $850 monthly mortgage payments by liquidating his retirement and investment accounts to supplement his unemployment benefits of $1,200 a month. "I had to do it," said Kachur, 47. "If you have bad credit, you can't get another job."

Kachur estimates that he has enough for only a few more months of payments, but because he is eligible for more unemployment benefits, he is lobbying his lender, Bank of America, for help. A modification under the federal plan would cut his payments nearly in half, he said. He said his requests have been denied so far. Bank of America said it could not comment on Kachur's specific case. The company complies with the federal foreclosure-prevention plan, including considering unemployment benefits when appropriate, spokesman Rick Simon said. But a workout faces other tests, including whether a loan modification or foreclosure is better for the investor, he said. "It has to meet all the other guidelines as well," Simon said.

Deflation Coming In From Abroad

The deflation story [begins] to pick up steam. [Yesterday's] trading consisted of falling stocks, falling commodities, falling gold and a stronger dollar -- a classic deflationary combo. And new data from the Bureau of Labor Statistics shows that after several months of rising prices, imports are starting to drop again... watch out.

Time To Switch to Cash: Elliott Wave's Robert Prechter

In late February, we had long-time bear Robert Prechter, Founder & CEO of Elliott Wave International on the "Closing Bell," where he predicted a sharp rally. Prechter has been studying the charts for the past 30-years. That's a pretty bullish call for the perma-bear! Since March 9th, the S&P 500 has seen one of the fastest upside moves ever. According to Prechter's latest Elliott Wave Theorist, that 50% gain in five months carried the index to the lower end of his target zone of 1,000-1,100.

Now, he's turning bearish again. His biggest call: the dollar is forming a major bottom and starting a multi-year advance. Prechter also says that the potential for the dollar's bottom is an important thesis for deflation. Another bold prediction: Prechter is calling for the next wave of deflation! All of this just another bearish signal for stocks and he's recommending investors switch to cash.

German investor optimism at 3-year high

Germany’s economic rebound has gained momentum with a closely watched survey showing investor confidence surging to the highest level in more than three years. The Mannheim-based ZEW institute said its "economic sentiment" indicator, which gauges expectations about economic trends over the next six months, had jumped by 16.6 points to 56.1 points in August, the highest since April 2006. The latest data followed last week’s news that Germany and France had beaten the US and UK in escaping recession. Both countries reported a 0.3 per cent rise in gross domestic product in the second quarter.

Germany’s export-led economy – the largest in Europe – appears to be benefiting from revival in global prospects as well as fiscal stimulus measures, which have boosted car sales. With the ZEW index regarded as offering a guide to likely trends in economic activity in coming months, the latest reading has boosted expectations that the third quarter will see an even stronger German performance. The index was based on a poll of more than 300 analysts and institutional investors.

"The good second quarter was probably just the beginning of a mid-summer sprint," said Carsten Brzeski, European economist at ING in Brussels. Manufacturing orders data have also pointed to a revival in growth. Germany’s economy had been expected to contract by as much as 6 per cent this year but Axel Weber, Bundesbank president, told a German newspaper earlier this week that such forecasts would probably have to be revised upwards. He cautioned, however, against "calling too early the end of the financial crisis".

The ZEW index fell sharply after the collapse of Lehman Brothers, the US investment bank, last year. It has since recovered steadily, although it dipped temporarily in July, and is now well above its historical average of 26.5 points.

Wolfgang Franz, ZEW’s president, said that last week’s GDP data showed that financial market experts’ expectations about a recovery "have come true". But he also warned that there was "no reason for euphoria". German prospects depended on a global upturn and would "recover only gradually", he said. Economists think that rising unemployment and continuing worries about Germany’s banking sector will act as drags on growth. The effects of emergency measures by governments and central banks to boost growth may also prove short-lived.

Germany and France Really Out of Recession?

Aug. 14. MIG Investments Chief Market Analyst Paul Day on his skepticism of France and Germany's recovery from recession.

Waiting for Something to Prick China's Bubble

Why do I feel like the macro data reported by China Monday night made both China-bears and bulls smack their lips?Well, as a China-bear myself right now, I wanted to interpret the data as the first signals of a slowdown, something that could be devastating given [among other things] the leveraged asset growth that's occurred over the last few quarters. My bullish adversaries will plug the data into their analyses to reconfirm that the Chinese government is wary of burgeoning bubbles and is taking measures to not overheat their economy.

Getting technical, FXP: Slow Stochastic set new ST highs on 7/31 & 8/7, which action was confirmed by the stock's price performance= BULLISH. Couple that with a MACD cross on 8/5, where the curve is sloping up and divergence is increasing= BULLISH.I didn't get the definitive fundamental "go" I was looking for from July's data. Rather, I translate the data from an annual perspective, interpreting it in the context of the government's FY09 targets: yes, China reported some unexpected m/m and y/y drops, but those numbers seem to have the re-aligned the economy on a track to hit its year end goals. In that context, July's data showed a gravitational pull to the mean.

Although I'm net short China right now (long FXP and short the front 13 calls) in my own portfolio, I've kept my clients on the sidelines until I get more definitive fundamental sell signals. I can day-trade technicals in my own account, but I'm cautious not to let clients' capital stagnate while shorting a consolidating Chinese market for 2 quarters.That being said, some problems still remain. While China's economic targets seem appropriate, its means to that end weren't. We're all aware of the forced lending that occurred 2q09. Credit was easy, collateral requirements were lax, and credit investment was ill-advised.

Truth be told, July's data brought some pretty volatile performance to the table, like the m/m drop in bank lending. As I said, that's fine if China's trying to cool down after an unprecedented run, but all these loans and all this investment has been channeled into assets and markets. From Ambrose Prichard:

Beijing is walking a tightrope by trying to offset the collapse in exports – almost 40pc of GDP – with an investment blitz in roads, railways, and industry through state-owned companies.

The real economy cannot absorb the money, so it is leaking into asset speculation. The central bank estimates that 20pc of fresh credit has ended up in equity markets. The Shanghai Index is up 80pc this year, though profits have fallen by almost a third. The pattern echoes the final phase of Japan's Nikkei bubble in 1989.

There's a growth requirement necessary to keep loans and investments performing, to thereby substantiate these piles of leveraged capital. While the Shanghai has rallied, credit extension swelled mostly at the end of that market run, at which time the small-money decided to jump into the swimming pool.

With China diversifying away from an Export-driven model toward a more domestic, consumer-based model, the effect of a weak USD is taking a different role. The Yuan was kept artificially low for years to lure the US to Chinese exports. Now, facing an inevitably weaker USD and a more protectionist "Buy America" M.O., China changed its strategy by divesting dollar denominated assets and stockpiling hard assets (i.e. commodities).

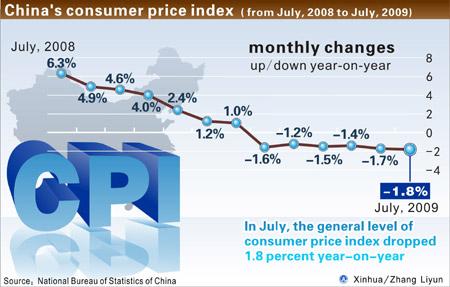

A 23% y/y drop in exports, a 1.8% y/y drop in CPI! It's taking some serious stimulus to displace the export evaporation with domestic consumption.

From Andy Xie:

…China’s average [property] price per square meter nationwide is quite close to the average in the US. The US’s per capita income is seven times China’s urban per capita income. The nationwide average price is about three months of salary per square meter, probably the highest in the world. As far as I can tell, a lot of properties can’t be rented out at all. Those that can bring in 3% yield, barely compensating for depreciation. The average rental yield, if one including those that can’t be rented out, is probably negligible. China’s property price doesn’t make sense from affordability or yield perspective.

So what are the definitive signals I'm looking for to prick China's asset bubble? I'm watching CPI for deflation, but more importantly, I'm watching the Dollar Index, which sits around 77 today. A secular bear market for the Dollar redirected liquidity into China, that's the executive summary of what's happened here. With the Chinese government already stimulating the economy, they could be caught with their pants down when the dollar strengthens.

Kind of a contingency of the dollar's performance, I'm also watching commodity prices. Although Chinese GDP has a heavy allocation toward net exports, commodity price performance resonates top to bottom, government to consumer, because of the leveraged buying spree we've seen. Dollar strength will support higher net exports, but the damage resulting from commodity price destruction will be a negative multiple of whatever net benefits may arise.

China bank lending fell almost 77% in July

Lending by Chinese banks slowed in July, softening the pace of growth in the nation's broad money supply, following record loan issuance in the first half. Data released Tuesday by the People's Bank of China showed new loans for July totaled 355.9 billion yuan ($52 billion), down almost 77% from June's 1.53 trillion yuan. The latest figures brought total lending growth this year to 7.7 trillion yuan, a more than doubling from the first seven months of last year. Of July's loan figure, 236.5 billion yuan went to households while 119 billion yuan went to corporations, the smallest such issuance since November 2007.

"After the blowout in June (when 1.228 trillion of net loans were extended to corporations), a sharp slowdown was always going to happen, but this may still unnerve the market and is another signal that the momentum has dissipated," wrote Standard Chartered analysts in a note Tuesday. July's loan issuance was weaker than many expected, with consensus estimates pegging the figure at 500 billion yuan. Standard Chartered said loans in the second half will likely amount to 2.5 trillion yuan, bringing total loan growth for the year to 10 trillion yuan.

The bank said the weaker-than-expected loan figure would add to the argument that it was too early to tighten. It noted that the figures would have been seen by Premier Wen Jiabao ahead of his weekend speech, which called for continuation of a proactive fiscal policy and a moderately loose monetary policy. Merrill Lynch described the July loan figure "a decent amount" but said indications were that "overall monetary and credit policy will continue to be relatively loose before spring 2010." Meanwhile, China's money supply, as measured by M2, expanded 28.4% in July from the same month a year earlier, easing slightly from June's growth of 28.5%.

"China's banking regulator has advised banks to avoid sudden surges in lending and to ensure that loans are channeled into the real economy," said J.P. Morgan's head of China equities, Jing Ulrich. Chinese banks had issued 7.4 trillion in loans in the first half, about three times the year-earlier level. Other data released Tuesday showed household savings fell 19.2 billion yuan as households shifted funds out of savings accounts to mutual funds or accounts held with securities companies.

Expansive China faces grass-roots resentment

Algerian shopkeeper Abdelkrim Salouda has witnessed China's global economic expansion first-hand and he does not like it, especially since he was in a mass brawl this month with Chinese migrant workers. "They have offended us with their bad behavior," said Salouda, a devout Muslim who lives in a suburb of the Algerian capital. "In the evening ... they drink beer, and play cards and they wear shorts in front of the residents."

From Africa to Europe, the Middle East and the United States, China's drive to project its economic might abroad can sometimes breed fear and resentment. The risks are likely to grow as Beijing channels more of its foreign exchange reserves, which stood at $2.13 trillion at the end of June, into foreign investments. From having a handful of tiny investments abroad less than two decades ago, China has grown to the world's sixth-biggest foreign investor and overtook the United States as Africa's top trading partner last year. That breath-taking rise has brought problems: allegations from emerging countries that China is stripping them of resources and suspicions in the developed world that obscure state interests lurk behind Chinese investments.

Where governments welcome Chinese investments for the boost they bring to their economies, a widely perceived Chinese tendency for Chinese firms to import their own workers has created tensions with job-seekers. "It's very new, it's very big, it's full of potential hazards, it's also full of potential benefits," said Kerry Brown, Senior Fellow at Britain's Chatham House think tank.

The challenge of how to deal with such tensions will only be magnified as the global slowdown prompts Beijing to pump even more of its foreign exchange reserves overseas. China used to be content to keep its surplus dollars in the bank or in U.S. government debt. But the financial crisis and subsequent downturn have, in some quarters, shaken faith in the strength of the dollar and U.S. Treasuries. With China still needing to secure access to global resources, some Chinese policy-makers are talking about redirecting billions of dollars into overseas investment instead.

The resentment felt by the Algerian shopkeeper toward his new Chinese neighbors is not universal: people in many places welcome the benefits from Chinese investment. Those can include aid with few strings attached, capital for infrastructure that Western donors will not fund and competition that drives down prices. Despite the clashes in Algeria's capital this month, its government welcomes Chinese investment. A $9 billion minerals-for-infrastructure deal is presented by Congolese President Joseph Kabila as a cornerstone of his plan to rebuild the Democratic Republic of Congo after years of war.

China will build roads, schools and hospitals in exchange for mining rights. In Guinea's capital, Conakry, the Chinese government is building a 50,000-seat sports stadium as a gift. "We are very satisfied with our cooperation with China," said Denis Sassou-Nguesso, the president of Congo Republic on a visit to a hydro-electric dam being built by Chinese contractors. "Contrary to certain assertions, it's not just Chinese on the various construction sites, there are also numerous Congolese workers," he said.

But in some countries, it is the sheer size of the Chinese presence that causes tension. Russian officials estimated that last year there were 350,000 Chinese migrants living in the country's far eastern regions, many illegally. The native population, in an area almost 10 times the size of France, is just over 7 million. Asked if the numbers of Chinese migrants jeopardized Moscow's control there, a senior Russian migration official said: "There is a threat. It should not be overstated but there is a threat," said the official, who did not want to be identified because of the sensitivity of the subject.

Elsewhere, the fact that the lion's share of Chinese investments are from the state itself or state-controlled companies, is the source of friction. One of the best-known cases of thwarted Chinese expansion was when U.S. lawmakers blocked the sale of oil company Unocal to China's CNOOC Ltd. in 2005. One senator said the deal would effectively give the Chinese Communist Party control over a strategic U.S. resource. In Sudan, rebels accuse Beijing of supporting Khartoum in the six-year-old conflict in Darfur -- and they see Chinese companies as the embodiment of that policy.

"Their only interest in Sudan is their own economic benefit," said Al-Tahir al-Feki, a spokesman for Sudan's rebel Justice and Equality Movement. "As soon as that benefit is gone they will disappear, leaving so many things destroyed behind them."

Another accusation leveled at Chinese investors is that they cut corners. Five Zambians were shot and wounded in 2005 in a riot over pay and safety standards at a Chinese-owned mine, and a year later 52 Zambians were killed in an explosion at a Chinese firm manufacturing explosives for mining. In January, Chinese traders in Guinea closed their shops for several days for fear of reprisals after the authorities found Chinese-made fake medicines. "A part of the population attacked the Chinese expatriates, whom they associated with the offenders. We ... had to intervene to calm the situation," said a military source who was speaking on condition of anonymity because he was not authorized to speak to the media.

China says its investors are forced to go into "frontier markets" because developed countries lock them out of more stable economies. As a result, they say, the risks they face are higher. There is some truth in that argument, said Brown from the Chatham House think tank, a former British diplomat in Beijing and the author of "The Rise of the Dragon," a book on Chinese investment. "The underlying pattern we find is that in countries where governance is decent like Botswana or South Africa, where there's reasonable rule of law and some kinds of infrastructure to control ... Chinese investment, then it's not too problematic," he said.

"However, in countries where there are problems of governance, problems of environmental impact, problems of labor rights, unfortunately Chinese investment performs very poorly indeed." China has started to address the damage to its reputation as an overseas investor. Big firms have hired Western consultancy firms to give advice. Many are now seeking local partners, or favoring less high-profile indirect investments. There are signs too that the Chinese government is doing more to win over the trust of local communities.

In Algeria, the Chinese embassy said it had advised its nationals to respect the country's traditions. In Zambia, poor communities have received Chinese donations that include footballs and boreholes for drinking water. But much of the responsibility will still rest with investment recipients to set out clear rules on how they manage the growing flows of cash. "My hunch is that foreign governments have got to make decisions about where they want the money to go and where they say no," said Kerry.

Digg Dialogg: Timothy Geithner

Digg has partnered with The Wall Street Journal for an exclusive interview with U.S. Secretary of Treasury Timothy Geithner. Alan Murray, Deputy Managing Editor of The Wall Street Journal, will be asking him the most popular questions as submitted and voted upon by you. From now until Thursday, August 20th at 12 Noon PT, you can submit and Digg up questions to decide which will be asked.

- Why has the federal reserve bank never been audited?

- You failed to pay some of your federal taxes in 2001. And in 2002. And in 2003. And in 2004. Please explain.

- What is your position on Ron Paul’s House Resolution 1207? (Which as of the writing of this question has 282 cosponsors.) http://www.auditthefed.com/

- Last week you requested that Congress raise the $12.1 trillion statutory debt limit, saying that it could be breached as early as mid-October. This is in addition to the increase already approved in February this year to accommodate the added debt from the $787 Billion stimulus plan. How is this anything other than runaway government spending? What will it take for us to see US debt go the other direction?

- How do you feel about the revolving door between high job positions in the treasury and Goldman Sachs?

- You were a member of the Federal Reserve, a group that so thoroughly mismanaged our monetary policy that they helped create a massive housing bubble because of foolish loans and speculation enabled by low interest rates, and then you were involved in a horribly mismanaged bailout that hasn’t freed up credit markets and can’t even account for all the money it spent. Why are you running the Treasury Department?

- What is one mistake you’ll admit to making since taking over as Treasury Secretary? What do you wish you’d done differently?

Why the 'Carry Trade' Is Back

As central bankers keep pumping huge sums into the global financial system, they are also pumping up one of the riskier investment strategies in the currency market. Known as the "carry trade," the strategy involves borrowing money in countries such as Japan where interest rates are low, then investing it where rates are higher and pocketing the difference. After flourishing during the boom years, the trade all but disappeared as big currency swings led to heavy losses amid the financial crisis. Now, though, as markets calm down and as some central banks signal interest-rate increases while others hold rates near zero, hedge funds and other investors are wading back in.

"It's starting to come back," says Stephen Jen, a managing director at BlueGold Capital Management LLP in London. "Investors are starting to think about rate hikes, which makes such trades more relevant and attractive." If the trade keeps growing, it is likely to have an effect on currencies, weighing on the ones in which traders borrow and pushing up those in which they choose to invest. It also can have the opposite effect at times when investors become more risk-averse, as they did Monday, pushing the yen up sharply against other currencies.

The Japanese yen remains a popular borrowing currency, given the central bank's adherence to an interest-rate target near zero. But other regions are attractive, such as Europe, where the key rate is 1%, or the U.S., where interest rates are close to zero and the Federal Reserve has pumped more than $1 trillion into the economy this year. While precise indicators on the carry trade are hard to come by, analysts at Deutsche Bank say they see money moving back into the Brazilian real, a bellwether for the carry trade given Brazil's history of high interest rates. As of mid-August, investors had a net $4 billion in bearish bets on the currency, down from $12 billion in early March. Meanwhile, the real has risen 28% against the U.S. dollar since the end of February.

Many of the carry trades are part of broader bets on a global economic recovery, analysts and investors say. Some investors are putting their borrowed yen and dollars into assets in Australia, a large commodity producer that stands to benefit from an economic rebound in one of its key customers, China. Since the end of February, the Australian dollar has risen 29% against the U.S. currency.

To be sure, the carry trade can entail big risks, particularly with differences among interest rates still thin compared with the boom years. A mere 1.5% fall in the Norwegian krone, a popular carry-trade play, against the dollar would wipe out the potential gains for a hedge fund doing the $10 million dollar-krone trade. Carry traders take comfort in the relative calm in stock and currency markets, as compared with the darkest days of the crisis. "Carry trades are for smooth rides," says Drausio Giacomelli, head of emerging-markets strategy at Deutsche Bank in New York.

Shame gene has disappeared from financial system

When Lazard Brothers, the London arm of the Lazard banking empire, was brought to its knees by a rogue trader in 1931, the miscreant made a confession and shot himself. Nowadays it is only a mild exaggeration to say that European rogue traders serve relatively short jail sentences before taking to the lecture circuit to explain that the damage they wrought was largely the fault of stupid directors. That, and the return of a "business as usual" ethos in relation to bank bonuses, suggests that the shame gene has gone missing in the financial system. Bankers’ lack of sensitivity to the wider concerns of society is also symptomatic of a culture that has become heavily transactional to the point of being blinkered.

The recent results of the big banks have shown once again that bank profits are increasingly driven by proprietary trading. And ethical niceties rarely rank high on the traders’ agenda. As Roger Bootle of Capital Economics points out, a curious and possibly unique feature of the financial business is that traders are often applauded by bosses and colleagues for eviscerating their clients. A similar ethical deficit has been evident in the subprime mortgage market where big bonuses were earned for extending loans to people with no prospect of being able to service or repay the debt.

In such markets trust is in short supply. Much has been written about how perverse incentives have encouraged bankers to put the whole system at risk. Less often observed is that when incentives are pushing people in a direction that is at odds with ethical behaviour, customers will be ripped off and conflicts of interest abused. In a financial world where trust is lacking, the only way to prevent bad behaviour is tough regulation. The scale of the financial debacle is such that it would be natural to expect a hefty regulatory response on these behavioural issues as well as on systemic risk. Yet the current controversy about bonuses on both sides of the Atlantic raises questions as to whether regulators have the stomach for the fight.

In the UK, government ministers clearly feel that the Financial Services Authority is pussy-footing on bankers’ pay for fear of encouraging senior bankers to stage a great British evacuation to more lenient jurisdictions. That underlines one of the more unfortunate consequences of the financial bust. On the one hand, we have deglobalisation, as supply chains are shortened and cross-border banking is threatened with tougher capital requirements. On the other, we have a potential acceleration in what might be dubbed malign globalisation. The labour market for top bankers is internationally flexible and could become more so if there are big differences between countries on the regulation of pay and incentives. And regulatory arbitrage will almost certainly increase as a result of the lawmakers’ response to the crisis.

Yet the politicians are not on the side of the angels in all this. They would like the banks to lend more and the bankers to be paid less. But the Anglophone world badly needs to deleverage. And because both the household and corporate sectors are indeed paying down debt, demand for credit is anyway weak. Meantime the central bankers’ remedy for cranking up credit, quantitative easing, merely pumps up asset prices as central bank purchases of bonds put money into the hands of institutional investors.

In the UK, ministers have also been seduced by the argument that Britain’s competitive advantage in financial services must not be jeopardised by an over-draconian regulatory response to the crisis. They are therefore relaxed about keeping a universal banking model that permits big risk-taking with complex financial instruments. They are also relaxed about moral hazard and reluctant to shrink banks that are too big to fail. None of this bodes well for our ability to avoid further bubbles and busts. Nor does it reflect well on those central bankers who argued that because it was too hard to identify bubbles and too dangerous anyway to prick them, the right policy was simply to clear up afterwards.

The mess is too great. And the clean-up seems unlikely to address adequately such problems as excessive and morally hazardous concentration in banking and a reward system that generously remunerates successful punting but imposes no penalty for loss-making bets. Some central bankers, like rogue traders, lack a shame gene.

US credit card rates rise in 1st half of '09

The nation's banks raised credit card rates and increased their profit from lending to consumers in the first half of 2009, according to a consumer advocacy group. The Pew Safe Credit Cards Project said Monday the median lowest advertised credit card rate rose to 11.99% in July from 9.99% in December. At the same time, the group said, the profit banks made on credit card debt rose 46%. The group, which says on its Web site that it seeks to "protect customers from unfair credit card practices," said its figures are based on a survey of nearly 400 credit card issuers. The full results of the survey are scheduled to be published next month.

The study said the rate banks charge on credit card loans on top of what it costs to borrow from the Federal Reserve rose to 8.74% in July from 5.99% in December. That came as banks' borrowing costs were cut in the wake of the Fed slashing its benchmark interest rate to a range near zero percent. A spokesman for the financial services industry said the ongoing financial crisis made raising money difficult and expensive, with the costs passed on to consumers in the form of higher rates.

"A key thing to recognize is that about half of the funding for credit card loans comes from securitization" through private investors, said Peter Garuccio, a spokesman for the American Bankers Association. "We all know what happened in the secondary (credit) market last fall, and it's still very dry, which has made it more difficult and more expensive to fund credit cards."

The initial findings from the study came days before the first provisions of the Obama administration's credit card reform act go into effect. Beginning Thursday, cardholders will be able to reject rate increases imposed by banks and will have up to five years to pay off their credit card balance at the current rate. The new provisions also prevent credit card issuers from more than doubling a borrowers' minimum payment and raised the minimum number of days that banks need to give before making significant changes to a contract to 45 from 30. The act, which President Obama signed into law in May, will not be fully implemented until February. Eleni Constantine, director of Pew's financial security portfolio. said the final version of the act will ban retroactive rate increases and prohibit "hair trigger" penalties for errors such as late payments.

Banks Keep Tightening Loan Standards

Banks continued to tighten lending standards to businesses and households, but there are hints that the credit crisis is beginning to ease, according to the Federal Reserve's periodic survey of banks released Monday. Meanwhile, the Fed said it would extend a program aimed at bolstering consumer-loan and commercial-real-estate markets into 2010, even as it allows other recovery programs to expire. The Fed's Term Asset Backed Securities Loan Facility, or TALF, was set to expire at the end of the year. But Fed and Treasury officials said in a statement that consumer- and business-loan and commercial-real-estate markets were still "impaired" and were likely to remain so for some time. The program will be extended to March 31; some facets will run until the end of June.

Under TALF, the Fed makes low-interest loans to investors and offers them protection against losses. The investors in turn use the cash to buy securities backed by a wide range of assets -- from credit-card debt to auto loans. The aim of the program is to get credit to consumers, businesses and commercial-real-estate borrowers. The Treasury provides financial support to the Fed for any losses on the loans. "A lot of repair has been done, but the market is still not 100% operational," said Derrick Wulf, senior portfolio manager at Dwight Asset Management. "The Fed is being careful not to derail the frail recovery."

Indeed, about a third of banks surveyed said, on net, that they tightened lending to businesses in the three months ended in July, down from roughly 40% in April's survey. The percentage of banks that tightened standards on commercial-real-estate loans dropped 20 percentage points, to 45%. For residential real estate, the percentage fell to 20% from a peak of about 75% a year ago. Caution was evident in the Fed report as demand for loans weakened in every sector except for residential mortgages. The drop in demand was the top reason banks cited for the overall decrease in business lending. They also cited fewer borrowers with good credit as a factor for the drop in lending.

"Most banks reported that they expected their lending standards across all loan categories would remain tighter than their average levels over the past decade until at least the second half of 2010," the Fed report said. A separate report released by the Treasury said total average loan balances at the 22 largest recipients of government bailout dollars fell 1.1% to $4.3 trillion in June. Meanwhile, loan originations rose 12.7% to $312.1 billion, buoyed by strong growth in originations by Goldman Sachs Group Inc. and American Express Co. as well as seasonal factors and new-home purchases.

American Express saw a 41% increase in originations in its credit-card business. Goldman, which repaid in mid-June the money it had received through the Troubled Asset Relief Program, posted 131% growth in originations on new commitments for commercial and industrial loans.

S.E.C. Floats a Short-Selling Proposal

The Securities and Exchange Commission, after months of considering what to do about short-selling, came up with a new idea on Monday that could make it virtually impossible to place an order to sell stock short and be sure it would be executed quickly. The commission asked for additional comments on that idea, delaying for at least a month the possibility of commission action.

The proposal would require that short sales be made only at a price higher than the current best price being offered by would-be buyers of the stock. It is similar to the so-called tick-test, which was effective on many stock markets before 2007, but would be more restrictive and could be easier to apply given the current structure of markets. There is now no limit on short-selling, so long as the seller can locate shares to borrow.

Short-sellers trade borrowed shares of a stock, hoping to buy them back later at a lower price and pocket the difference. The latest proposal is not a completely new idea; the S.E.C. suggested it deep in its earlier proposal, but did not request detailed comment on it. That it is now seeking comment could indicate that at least some members of the commission think the approach could be a good one. Pressure on the S.E.C. to do something about short-selling grew last year when the stock market nearly collapsed in the wake of the failure of Lehman Brothers. The commission banned short-selling in some financial stocks for a time, and some investors, supported by members of Congress, demanded permanent changes in the rules.

Much of Wall Street has argued that there is no evidence that short-selling caused the plunge last year, and the academic studies available do not support the idea. But the pressure on the commission to do something has been intense. Several stock exchanges suggested a proposal similar to the new one, if the commission felt it had to do something. The commission asked for comment on whether the latest proposal should become effective for all stocks at all times, or should take effect only after a "circuit breaker" was tripped. Such a circuit breaker could be activated if the stock in question declined by a certain amount — say 10 percent — or for all stocks if a major market average fell by a similarly large percentage. The exchanges said a circuit breaker would be needed.

The old tick-test depended on whether the short sale was executed at a price that was higher than the last different price. Such a rule was relatively easy to impose when virtually all trading in stocks listed on the New York Stock Exchange was done on the exchange. Now, however, such trades are executed in dozens of locations, and markets can delay reporting trades for up to 90 seconds. As a result, brokerage firms argued, it is virtually impossible to know with certainty what the last trade was, and therefore something based on the old tick-test would be impossible to administer.

The "alternative uptick rule" that the S.E.C. suggested on Monday would be based solely on the current best bid price for a stock — a figure that is kept up to date and is readily accessible. If the best bid for a stock was $20 a share, a short-seller could put in a sell order at $20.01. If someone agreed to buy at that price, the trade could be completed. But no short sale could be executed immediately, at least until all the buy orders at the best bid price had been filled. The commission said that could "potentially lessen some of the benefits of legitimate short-selling, including market liquidity and pricing efficiency," and asked for comment on whether that was likely.

The commission asked for comment on whether such a rule would help to prevent "potentially abusive or manipulative short-selling" from driving the market down, and whether adopting such a rule would improve investor confidence. Even if the commission were to settle on the new approach, it would have to decide what circuit breakers, if any, would be needed. And the commission would have to decide what exemptions, if any, were appropriate. Much of Wall Street wants to exempt market makers and traders who follow certain market-neutral strategies, warning that without them, those traders would be subject to unnecessary risks of having to maintain positions overnight.

The old tick rule was dropped in 2004, after an experiment in which the commission found that eliminating it for some stocks had no apparent effect on trading. There was virtually no public controversy at the time, but that changed after the 2008 market plunge; the S.E.C. could face a hostile reaction from some members of Congress if it does not act. For some, the issue of short-selling has been tied up with the issue of "naked short-selling," a practice that involves selling stocks short without borrowing them. It appears that other S.E.C. rules have virtually eliminated such selling, particularly for stocks listed on Nasdaq or major stock exchanges. But it remains an emotional issue, and some believe naked short-selling is still a major problem.

America’s Japanese banks

A banking system loaded down with hundreds of billions of dollars worth of unrecognized bad debt — Japan in the 1990s? No, it’s the United States today. And where are American banks hiding their losses? Among other places, in their loan portfolios.

Banks have written down billions in toxic securities, but many toxic loans are still carried at close to full value. According to data published by the Federal Reserve late last year, banks are carrying $3 trillion of residential real estate loans and $1.7 trillion of commercial real estate loans on their books for a total of $4.7 trillion. Dan Alpert at Westwood Capital thinks as much as a fifth of that total could be uncollectable. "We know lots of mortgage loans are underwater," he says, describing the situation where the value of collateral has fallen below the principal balance of a loan. "A majority of the loans banks are holding were originated at the height of the bubble, when securitization broke down."

When securitization markets were fully functional, banks had been able to package and sell their loans to investors. When those markets buckled, banks were forced to eat their own cooking — much of it rancid. Banks argue that loans should not be marked down if they’re still "performing." As long as borrowers are meeting their contractual obligations, there’s no reason to take a writedown. The problem is, this gives banks an excuse to extend, amend and pretend. They can make concessions on loan terms or delay foreclosure notices, if only to maintain the fiction that borrowers will make good.

With real estate prices likely to fall, and stay, 40 percent below the peak, borrowers have a big incentive to renege on their side of the bargain. This is how we become Japan. Emergency bailout facilities allow banks that otherwise would have failed under the weight of bad loans to hold those loans to maturity — pretending the bad ones will be paid off in full over time. In reality, many loans will default and banks will bleed capital for years. Take commercial real estate. As the Congressional Oversight Panel has reported, few CRE loans that were originated at the peak will qualify for refinancing when they mature. Banks can pretend they will, carrying the loans at values far above what will ever be paid back.

FASB wants to bring some clarity to the issue. A plan under discussion would force banks to record loans at fair value on their balance sheets. But it’s not clear how much good that would do. One problem is that it’s much more difficult to determine the fair value of a loan than it is the fair value of a security, where more liquid markets with more frequent price quotes make measurement relatively easier. With loans, banks must rely on internal models. Banks are now required to report fair value estimates four times a year. But the most recent data raises just as many questions as it answers.

For instance, what estimates are banks using in their models? As Jonathan Weil of Bloomberg noted, Regions Financial carries its loans at 34 percent above fair value, Citigroup carries its loans at no premium. This could mean Regions faces bigger losses down the road, or it could mean Citi’s fair-value calculation is too charitable. More likely, it means both. Determining fair value is largely subjective. So FASB’s proposal, to make banks adjust their balance sheets accordingly, is imperfect. It could have a positive impact if regulators use the new information to force banks to raise more capital, cushioning balance sheets from the future writedowns we know are lurking.

But will banks raise enough? Probably not. Alpert is highly skeptical that banks’ fair value estimates are accurate: "Given the decline in value of collateral backing these loans, it’s very likely banks are underestimating the severity of future losses." So what do we do? We can start by eliminating government guarantees that allow banks to avoid dealing with the problem. As things stand, the biggest banks have no incentive to write down loans because the Federal Reserve, Federal Deposit Insurance Corporation and Treasury Department have, in effect, promised them unlimited financing to hold loans to maturity. As the Japanese can tell you, this is just a recipe for stagnation. Thanks to a debt bubble that authorities refused to deal with decisively, that country is now entering its third consecutive lost decade.

Disclose the fair value of complex securities

Banks and other financial institutions are lobbying against fair-value accounting for their asset holdings. They claim many of their assets are not impaired, that they intend to hold them to maturity anyway and that recent transaction prices reflect distressed sales into an illiquid market, not what the assets are actually worth. Legislatures and regulators support these arguments, preferring to conceal depressed asset prices rather than deal with the consequences of insolvent banks.

This is not the way forward. While regulators and legislators are keen to find simple solutions to complex problems, allowing financial institutions to ignore market transactions is a bad idea. A bank typically argues that a mortgage loan for which it continues to receive regular monthly payments is not impaired and does not need to be written down. A potential purchaser of the loan, however, is unlikely to value it at its origination value. The purchaser calculates a loan-to-value ratio using the current, much lower value of the house. After calculating the likelihood of default, the potential buyer works out a price balancing the risk of default and amount that might be lost – a price well below the carrying value on the bank’s books.

The bank is likely to ignore this offered price, or trades of similar assets, with the claim that unusual market conditions, not a decline in the value of the assets, causes a lack of buyers at the origination price. Its real motive, however, is to avoid recognising a loss. Yet, by keeping assets at their origination value, the bank creates the curious possibility that its traders could buy an identical loan more cheaply and so carry two identical securities in the same not-for-sale account at vastly different prices.

Financial assets, even complex pools of assets, trade continuously in markets. Markets function best when companies disclose valid information about the values of their assets and future cash flows. If companies choose not to disclose their best estimates of the fair values of their assets, market participants will make their own judgments about future cash flows and subtract a risk premium for non-disclosure. Good accounting should reduce such dead-weight losses.

This already happens in another financial sector. Mutual funds in the US now use models, rather than the last traded price, to provide estimates of the fair values of their assets that trade in overseas markets. The models forecast the prices at which these overseas assets would have traded at the close of the US market, based on the closing prices of similar assets in the US market. In this way, the funds ensure that their shareholders do not trade at biased net asset values calculated from stale prices. Banks can similarly use models to update the prices that would be paid for various assets. Trading desks in financial institutions have models that allow them to predict prices to within 5 per cent of what would be offered for even their complex asset pools.

Obtaining fair-value estimates for complex pools of asset-backed securities, of course, is not trivial. But these days it is possible for a bank’s analysts to use recent market transaction prices as reference points and then adjust for the unique characteristics of the assets they actually hold, such as the specific local housing prices underlying their mortgage assets.

For fair-value estimates made by internal bank analysts to be credible, they need to be independently validated by external auditors. Many certified auditors, however, have little training or experience in the models used to calculate fair-value estimates. In this case, auditing firms can use outside experts, much as they do today with actuaries and lawyers who provide an independent attestation to other complex estimates disclosed in a company’s financial statements. The higher cost of using independent experts is part of the price of originating and investing in complex, infrequently traded financial instruments.

Legislators and regulators fear that marking banks’ assets down to fair-value estimates will trigger automatic actions as capital ratios deteriorate. But using accounting rules to mislead regulators with inaccurate information is a poor policy. If capital calculations are based on inaccurate values of assets, the ratios are already lower than they appear. Banks should provide regulators with the best information about their assets and liabilities and, separately, allow them the flexibility and discretion to adjust capital adequacy ratios based on the economic situation. Regulators can lower capital ratios during downturns and raise them during good economic times.

No system of disclosing the fair value of complex securities is perfect. Models can be misused or misinterpreted. But reasonable and auditable methods exist today to incorporate the information in the most recent market prices. Investors, creditors, boards and regulators need not base decisions on biased values of a company’s financial assets and liabilities.

Robert Kaplan and Robert Merton, 1997 Nobel laureate in economics, are professors at Harvard Business School. Scott Richard is a professor at the Wharton School of the University of Pennsylvania

Backdating Likely More Widespread

The majority of companies that improperly backdated stock options never were caught by regulators or confessed to the practice, according to a new academic study. Researchers at the University of Houston's C.T. Bauer College of Business used a sophisticated statistical test to sift through more than 4,000 publicly traded companies for those with patterns of granting options at abnormally favorable times, often at low points for their share prices.

The study identified 141 companies with such advantageous options-granting practices that the researchers concluded they were highly likely to have been involved in backdating. Ninety-two of those companies never were publicly linked to investigations or announced earnings restatements related to backdating. The companies include advertising giant Omnicom Group Inc., retailer Dress Barn Inc., trucking firm J.B. Hunt Transport Services Inc. and equipment-rental concern United Rentals Inc. Officials at the companies, which showed some of the strongest signs of likely backdating in the study, had no comment or said they found no evidence of wrongdoing.

The unpublished study is the latest sign since the backdating scandal erupted in 2006 that the practice might have been more widespread than thought at the time. Other researchers have drawn a similar conclusion. Scott Whisenant and Rick Edelson, authors of the University of Houston study, said such abnormally favorable options-granting patterns would be expected to occur by chance in only a couple of companies that they examined. Still, the study cautioned that the findings are "purely statistical" and don't "claim to provide categorical or absolute legal proof that any specific company has engaged in backdating."