Last run of Barney, Gene, and Tom, District Fire Department horses, Washington, D.C.

For more, See July 18 2009 Washington Post story

Ilargi: I've been thinking a lot about Fannie and Freddie, and I haven't figured out what is going to happen, or how. Whatever it is, it will be shocking, there’s no escaping that.

A bad bank "solution" for Fannie and Freddie is what I see contemplated. With half of the $12 trillion US mortgage market soundly underwater by 2011, and 9 out of 10 Alt-A's and OptionARM’s in that sort of trouble, I am trying to wrap my mind around the sort of bad bank that will have to be, and what it will mean for the people in the street. And I'm sure the loans are not the worst kind of paper in the books, it's got to be the securities. China owns so much of that, it's scary, and that's reason enough to transfer the losses to unsuspecting Americans. And just take a look at this:

In 1999, when [Larry Summers] was Treasury Secretary, he warned lawmakers that Fannie Mae and Freddie Mac had grown so large that if they stumbled, the damage to the U.S. economy could be staggering.

Ten years ago, before the start of the housing bubble that would never have existed if Fannie and Freddie hadn't been there to facilitate it by buying up all the loans from the big lenders, Larry Summers of all people predicted they could bring the entire house down then. So this line should hold no surprises:

The revamping of the firms was almost included in the administration's June white paper that proposed an overhaul to the federal regulation of the financial system. But after determining that they had to craft a careful exit of the government's aid for those companies, Summers and Geithner decided to put the issue off.

A bad bank would serve to:

- Absorb the losses the Chinese et al will suffer when half of the US will be underwater

- Absorb the losses of the lenders who originated the loans and traded the securities

- Allow the game to continue and/or start afresh

Fannie and Freddie have $5-6 trillion in loans on their books. If half go toxic, that's a $2-3 trillion loss right there. Securities written on the loans have undoubtedly been hugely leveraged, and moreover the losses on them are incurred much faster, so we could be easily be looking at $20-30 trillion that is being considered for a transfer to the books of the nation's people.

It’s no wonder that there are such desperate attempts ongoing to make you believe we’re climbing out of the hole. The boys have seen how deep the hole is, and they don't want you to get a look at it. At least, not until all you have left is their losses.

It's nice and all to find out the the Fed is buying more and more Treasuries, in order to keep up appearances of actual sales. But what else did you think would be happening in the face of sales four times bigger than ever before?

I say, watch the Fannie and Freddie drama unfold. If real estate prices in 2011 are where Deutsche Bank yesterday said they will be, the amount of taxpayer money involved and consequently lost in the insane game of having the taxpayer prop up home prices, will be, to use Summers' word, staggering. Just with an extra 10 years of stagger added. When Summers issued his warning, the market was maybe $5-6 trillion. It's $12 trillion today.

If you want to be politically involved in America, here's what I suggest. Contact your representative(s), and demand they publicly reveal the total dollar amount in securities and, more broadly, derivatives, that are outstanding anywhere in the vicinity of Fannie and Freddie. Here's betting that you won't get nowhere. Nobody wants to be seen touching those kinds of amounts. That's no way to build a political career. They'd much rather see them quietly transferred to your accounts and keep their seats. But give it go: forget about auditing the Fed, it's waste of time, there's no authority for that. Push for an audit of Fannie and Freddie instead.

This is not about real estate, it's not even about the economy. It's about politics.

Fannie Mae to Tap $10.7 Billion in Treasury Capital

Fannie Mae, the mortgage-finance company taken over by the government, asked the U.S. Treasury for a $10.7 billion capital investment as an eighth straight quarterly loss drove its net worth below zero once again. A second-quarter net loss of $14.8 billion, or $2.67 a share, pushed the company to request money for the third time from a $200 billion government lifeline, Washington-based Fannie Mae said in a filing today with the Securities and Exchange Commission. Today’s results bring the company’s cumulative losses over the last two years to $101.6 billion and will bring its total draw on the Treasury to $44.9 billion since April.

The credit quality of loans and mortgage bonds that Fannie Mae owns or guarantees have deteriorated as a recession that began in December 2007 pushed more homeowners into foreclosure. A record 1.5 million U.S. properties received a default or auction notice or were seized in the first half of this year, 15 percent more than a year earlier, as employers cut jobs and temporary programs to assist homeowners came to an end, RealtyTrac Inc. said July 16.

Fannie Mae said it expects the quality of its assets to worsen further and to continue accumulating losses as it executes President Barack Obama’s efforts to modify or refinance loans for as many as nine million homeowners. "We do not expect to operate profitably in the foreseeable future," the company said in its filing. "We expect that we will experience adverse financial effects as we seek to fulfill our mission by concentrating our efforts on keeping people in their homes and preventing foreclosures."

Fannie Mae and smaller competitor Freddie Mac, which own or guarantee almost half of U.S. residential mortgage debt, are integral to Obama’s plan to help homeowners. In February, the government doubled its emergency capital commitment for each company from $100 billion, which the Treasury makes through preferred stock purchases. McLean, Virginia-based Freddie Mac has tapped $50.7 billion in aid in since November as the value of its assets dropped below the amount it owed on obligations. The companies’ regulator, James Lockhart, said yesterday that he is stepping down to pursue opportunities in business. His departure comes as debate grows over the future of the mortgage-finance companies once they emerge from the housing crisis.

Fannie Mae’s net worth, or the difference between assets and liabilities, was negative $10.6 billion as of March 31, compared with negative $18.9 billion on March 31 and negative $15.2 billion on Dec. 31, according to company statements. Fannie Mae and Freddie Mac are the largest U.S. mortgage- finance companies, owning or guaranteeing about $5.4 trillion of the $12 trillion residential mortgage debt. The Federal Housing Finance Agency put the companies under its control Sept. 6 and forced out management after examiners said the two might be at risk of failing amid the worst housing slump since the Great Depression.

The company increased reserves for future credit losses to $55.1 billion last quarter from $41.7 billion in the previous quarter. The amount of nonperforming loans that Fannie Mae guarantees for other investors rose to $144.2 billion from $121.4 billion in the first quarter, according to the filing. Fannie Mae also owned $26.3 billion in non-performing loans as of June 30, up from $23.2 billion in the first quarter. The fair value of Fannie Mae’s assets was negative $102 billion last quarter, compared with $110.3 billion at the end of March.

Fannie Mae and Freddie Mac shares, which were above $30 in March of last year, have been trading at less than $1 since December, except for one day in March when Freddie closed at $1.01. Fannie Mae closed at 79 cents today on the New York Stock Exchange, and Freddie Mac finished the day at 84 cents.

Fannie Mae was created in the 1930s under President Franklin D. Roosevelt’s "New Deal" plan to revive the economy. Freddie Mac was started in 1970. The companies were designed primarily to lower the cost of home ownership by buying mortgages from lenders, freeing up cash at banks to make more loans. They make money by financing mortgage-asset purchases with low-cost debt and on guarantees of home-loan securities they create out of loans from lenders.

U.S. Considers Bad Bank Option for Fannie Mae, Freddie Mac

The Obama administration is considering an overhaul of Fannie Mae and Freddie Mac that would strip the mortgage finance giants of hundreds of billions of dollars in troubled loans and create a new structure to support the home-loan market, government officials said. The bad debts the firms own would be placed in new government-backed financial institutions -- so-called bad banks -- that would take responsibility for collecting as much of the outstanding balance as possible. What would be left would be two healthy financial companies with a clean slate.

The moves would represent one of the most dramatic reorderings of the badly shattered housing finance system since District-based Fannie Mae was created by Congress to support mortgage lending during the Great Depression. Both Fannie Mae and Freddie Mac, based in McLean, have government charters to buy home loans from banks, which they then repackage and sell to investors. The banks can then use the proceeds to offer more loans to home buyers.

The leviathans became emblematic of the financial crisis when they were effectively nationalized in September amid a market meltdown that revealed much of their holdings to be troubled. The government has since pledged more than $1.5 trillion, including $85 billion in direct aid, to keep the mortgage market working through Fannie Mae and Freddie Mac. The proposal, which is preliminary and one of several under discussion, is scheduled to be taken up by the White House's National Economic Council on Thursday.

"

It should come as no surprise that the administration is thinking through" wholesale changes to these companies, said Andrew Williams, a Treasury Department spokesman. "We are in the preliminary stage of the process, the systematic development of options has not taken place, and no decisions have been made." Internal discussions over the future of the companies began earlier this year during the regulatory reform planning process and now are entering a more serious phase. National Economic Council Director Lawrence H. Summers has long wanted to overhaul the companies. The government's efforts so far "have taken the risk out of those two firms," Treasury Secretary Timothy F. Geithner said in a recent interview. "The only question that remains is what form, what structure they ultimately will take."

In an interview Wednesday announcing that he would step down later this month, James B. Lockhart III, the chief regulator of Fannie Mae and Freddie Mac, said there needs to be a "good bank, bad bank" structure. The "bad bank" would be a depository for Fannie Mae's and Freddie Mac's toxic assets. Then, the government could create new companies, if it chose to do so, that would attract private investment in support of mortgage finance. Options for the "good banks" include consolidating the firms into one government agency, leaving mortgage finance to private banks or maintaining a hybrid model.

The National Economic Council has looked at the "bad bank" option, among many others, in several internal policy papers. Any final decision would come after talks involving the White House, the Treasury, the Department of Housing and Urban Development and the Federal Housing Finance Agency. A major problem is that the firms own and insure trillions of dollars of existing mortgages. With the economy still in a deep recession, joblessness rising and defaults on home loans expected to continue to go up, there is great uncertainty over the size of future losses at Fannie Mae and Freddie Mac. That, in turn, is likely to drive investors from committing money to the companies.

Fannie Mae and Freddie Mac existed for years as odd hybrids, created by government to support housing but owned by private shareholders. (They are now majority-owned by the government.) Over the years, the unusual status has fed concerns that the firms exploited their quasi-governmental role to borrow money at very low rates and therefore grow far larger than was sustainable. At the same time, they had a duty to shareholders to maximize profits, leading them to take on bigger risks.

Until the future of the firms is worked out, the Obama administration has been using them to carry out its housing recovery program, including restructuring mortgages to avoid foreclosures. In addition, the Federal Reserve has bought well over $1 trillion worth of mortgage-related securities and debt from Fannie Mae and Freddie Mac. That further helped to lower interest rates on home loans. The government also has pledged up to $400 billion in direct investments in the firms.

Summers has long thought that the old structure of the companies posed a danger to the financial system. In 1999, when he was Treasury secretary, he warned lawmakers that Fannie Mae and Freddie Mac had grown so large that if they stumbled, the damage to the U.S. economy could be staggering. Few heeded him. Now, once again a leading voice on economic policy, Summers has the platform to restructure the mortgage giants. The revamping of the firms was almost included in the administration's June white paper that proposed an overhaul to the federal regulation of the financial system. But after determining that they had to craft a careful exit of the government's aid for those companies, Summers and Geithner decided to put the issue off.

Fannie, Freddie Debate Not Hurting Mortgage Rates

The increasingly public debate over what the government will eventually do with mortgage giants Fannie Mae and Freddie Mac, taken over last fall, leaves the mortgage market still waiting for a decided resolution, analyst said Thursday. The Obama administration is considering a variety of options to overhaul mortgage giants Fannie Mae and Freddie Mac, including folding the companies into a new federal government entity, the Washington Post reported Wednesday.

One option is to split the companies and putting their troubled assets in a new federally backed corporation, and possibly let to more viable portion of the company resume being shareholder-owned. The important but unclear aspect is whether the entities, in any form, continue to carry the government's implicit support of their debt to keep their borrowing costs low. The so-called government sponsored entities sell their own debt to finance purchases of mortgage-backed securities, which are bundles of individual mortgages. Their ability to finance those purchases at a low cost enable them to accept mortgages with lower rates, which helps homeowners.

"As long as the government guarantees are there, the products will trade as they do," at rates far below what fully private companies have to pay, said Kevin Giddis, managing director of fixed income for Morgan Keegan & Co. "Any change would more than likely have a negative impact on the housing market." Mortgage rates have risen over recent months as the economy appears to be improving, pushing up yields on Treasurys, which are the benchmark for a broad array of securities including mortgage debt. The rate on a 30-year fixed rate mortgage rose to 5.65% in the latest week, according to Bankrate.com. They fell to a low around 4.85% in the April. More likely than such a "good bank/bad bank" arrangement for Fannie and Freddie, the firms may be structured like a public utility, said bond strategists at RBC Capital markets.

"The firms would be even more highly regulated than they are today, with products and pricing approved by a government board, commission or agency," said Ira Jersey, head of U.S. interest-rate strategy at RBC. "Assuming adequate capital ratios were kept, the GSEs would be allowed to pay out a significant amount of profits as common share dividends." But in any case, the amount of debt held by the entities is also likely to be "dramatically" smaller, he said. The entities have been instructed to reduce the amount of debt they hold - currently near half of all outstanding home loans.

In all likelihood, the agencies will probably look rather different than they were, said Matthew Mac Donald, a bond portfolio manager at DWS Investments. The firms, one which grew out of the Great Depression, will go back to their more traditional role of facilitating a basic social goal: extending mortgages so more Americans can own homes. Their basic role was standardizing underwriting rules and pooling loans and relieving some of the credit risk for investors interested in owning mortgages.

"The uncertainly isn't rattling the market at all," he said. "It's a healthy discussion as long as the government doesn't indicate it may pull support for existing programs and securities." Fannie and Freddie have long been strange hybrids of government and private institutions and may, at least initially, end up closer to the government end of that spectrum because of lack of confidence in ratings for securitizations, MacDonald said.

Of all the possible outcomes, if they government chooses to make the entities fully private, "surely rates would increase," said Jeana Curro, a mortgage strategist at UBS Securities. "If they lose their implicit government guarantee, investors would need increased compensation." Investors in mortgage-backed debt currently demand yields about 0.90 percentage points above Treasurys to compensate for the different credit structure, analysts said. Spreads between corporate bonds and Treasurys are almost three times that.

New Jobless Claims Drop By 38,000, Beating Estimates

The number of newly-laid off workers seeking unemployment insurance fell last week, the government said Thursday, fresh evidence that layoffs are easing. The Labor Department said that initial claims for jobless benefits dropped to a seasonally adjusted 550,000 for the week ending Aug. 1, down from an upwardly revised figure of 588,000 in the previous week. That's much lower than analysts' estimates of 580,000, according to a survey by Thomson Reuters. The four-week average of claims, which smooths out fluctuations, dropped to 555,250, its lowest level since late January.

The tally of people continuing to claim benefits rose, however, by 69,000 to 6.3 million, the department said, after dropping for three straight weeks. The continuing claims data lags initial claims by a week. Many economists expect initial claims to continue to decline this year. "Claims should fall over the next few months, as the economy appears more or less to have stabilized," Ian Shepherdson, chief U.S. economist at High Frequency Economics, said in a note to clients before the department's report.

When emergency extensions of unemployment are included, the total rolls climbed to a record 9.35 million for the week ending July 18, the most recent data available. Congress has added up to 53 extra weeks of benefits on top of the 26 typically provided by the states. The increase in the number of people continuing to claim benefits is a sign that jobs remain scarce and the unemployed are having difficulty finding new work.

Despite the improvement, weekly jobless claims remain far above the 300,000 to 350,000 that analysts say is consistent with a healthy economy. New claims last fell below 300,000 in early 2007.

The recession, which began in December 2007 and is the longest since World War II, has eliminated a net total of 6.5 million jobs. The unemployment rate is expected to rise to 9.6 percent when the July figure is reported Friday. The jobless rate of 9.5 percent in June marked a 26-year high. More job cuts were announced this week. The publisher of the Milwaukee Journal Sentinel said it would slash 92 jobs as the current advertising slump continues to ravage the newspaper business.

Elsewhere, about 6,000 General Motors Co. blue-collar workers have taken the latest round of early retirement and buyout offers. But GM wants to cut about 13,500 workers, setting the stage for more layoffs. Among the states, Ohio had the biggest increase in claims, with 891, followed by Oklahoma, Mississippi, Louisiana and Alaska. State data lags behind initial claims data by one week. North Carolina had the largest drop in claims, with 9,809, which it said was due to fewer layoffs in the textile, furniture, rubber and plastics, and industrial machinery industries. Michigan, Florida, Georgia and Alabama had the next largest declines.

US food stamp list tops 34 million for first time

For the first time, more than 34 miilion Americans received food stamps, which help poor people buy groceries, government figures said on Thursday, a sign of the longest and one of the deepest recessions since the Great Depression Enrollment surged by 2 percent to reach a record 34.4 million people, or one in nine Americans, in May, the latest month for which figures are available.

It was the sixth month in a row that enrollment set a record. Every state recorded a gain in participation from April. Florida had the largest increase at 4.2 percent. Food stamp enrollment is highest during times of economic stress. The U.S. unemployment rate of 9.5 percent is the highest in 26 years. Average benefit was $133.65 in May per person. The economic stimulus package enacted earlier this year included a temporary increase in food stamp benefits of $80 a month for a family of four.

The Fed's UST-POMO Pyramid Scheme Exposed

In a brilliant piece of investigative reporting, Chris Martenson (original article here) has uncovered that the Fed, merely a week after issuing $28 billion in 7 year bonds (which Zero Hedge discussed previously) via its puppet, the US Treasury, of which $10 billion ended up being purchased by primary dealers, has turned and bought 47% of the primary allocated bonds in Open Market Purchases. This is undisputed monetization removed simply via one primary dealer and less than 5 days of temporal separation in order to leave no easy trace. As Martenson points out:"A more honest and open approach would have been for the Fed to simply buy them outright at the auction but this way, using "primary dealers" and "POMOs" and all these other extra steps the basic fact that the Fed is openly monetizing US government debt is effectively hidden from a not-too-terribly inquisitive US press and public."

The question is did the Fed implicitly tell the primary dealers they are merely holding the treasuries for a flip, and that it would acquire them immediately. Absent this $4.8 billion in effectively monetized bonds, what would the Bid To Cover have been for the primaries? Would this have been the second practically failed auction for USTs after the deplorable 5 year auction results a day prior? One wonders if there would have been 62% indirect interest in these bonds (which the day before had a measly 32.5% indirect bid) if the purchasers were aware of the Fed's immediate prompt monetization of a large part of the directs' balance.

It is truly a sad state of affairs when the Fed has to manipulate public and media perception in this way, and has to cover up for the complete lack of interest in US Treasuries.

Here is the evidence Martenson dug up:

Martenson's conclusion needs no elaboration:

"The speed of the shell game is accelerating.

This immediate repurchase of newly auction bonds by the Fed tells us that demand for these bonds is not nearly as high as advertised, and that things are not quite as strong as represented.

And oh, by the way, don't expect any stock market weakness while so many billions are being shoveled out the Fed and into the pockets of the primary dealers. They'll have to do something with all that freshly minted cash....."

Zero Hedge salutes CM for this brilliant piece of sleuthing: now if only the MSM would have the guts to demonstrate the pyramid scheme that the US Bond and Equity markets have become.

Why a major revision is coming for the nation's employment numbers

Tyler Durden: Why is it that people who base their opinions on facts come off significantly less amusing than the clownshoes who predict a future based on hope and personal conflict of interest bias. Watching a boring TrimTabs' Biderman debate with some guy named John Herrmann (not to mention some other "portfolio manager" named Ron Insana) who sounds like he just came out of accounting one oh one in Rose-Colored Glasses community college is simply deliciously hilarious. Also, listen to Biderman for some objective truths about the economy and labor statistics.

PS My system doesn’t like the CNBC video format. If you have the same experience, here's the Youtube version of the same video, which isn’t great either: it's out of sync.

< American Incomes Head Down, Threatening Recovery in Spending

Household income in the U.S. is weakening as the influence of the government’s stimulus plan wanes, prompting economists, Federal Reserve officials and a Nobel laureate to warn that consumer spending may struggle. "Consumers have started to change their behavior and they are going to save more," said Richard Berner, co-head of global economics at Morgan Stanley in New York and a former researcher at the Fed. "You have pressure on wages, you have employment still declining."

Wages and salaries, which drive recoveries in spending, fell 4.7 percent in the 12 months through June, the biggest drop since records began in 1960, according to Commerce Department figures released yesterday. The Obama administration’s tax cuts, extended jobless benefits and a one-time Social Security bonus have helped mask the damage done by the worst employment slump since the Great Depression. Personal incomes, which include interest income, dividends, rents and other payments as well as wages, tumbled 1.3 percent in June, more than forecast and the biggest drop in four years, yesterday’s Commerce report showed.

Excluding the effects of the stimulus plan, June incomes would have dropped 0.1 percent after no change in May, according to the report. In May, one-time additional payments to Social Security recipients boosted incomes 1.3 percent. One of every 10 American workers will be without a job by early 2010, economists project, shaking the confidence of those still on payrolls and discouraging spending. It may take as long as 15 years for consumers to fully repair finances battered by the decline in home values, stocks and employment, said Edmund Phelps, winner of the Nobel prize in economics in 2006.

Decreasing pay is not the only hurdle for consumers. Plunging home prices and stocks reduced household net worth by a record $13.9 trillion from the third quarter of 2007 through this year’s first quarter, according to figures from the Fed. "Households are going to have to do an awful lot of rebuilding of their wealth," Phelps, a professor at Columbia University in New York, said this week in an interview on Bloomberg Television. "Even if that rebuilding goes on at a pretty good clip, it will take 12 or 15 years for households to get to the wealth level that they had several years ago. Consumer demand is going to take a long time to rebuild to normal levels."

In the second half, incomes and spending will be hurt by the loss of transitory factors such as lower fuel prices, decreased tax rates and the one-time payment to retirees, William Dudley, president of the Fed Bank of New York, said in a speech last week. "Consumer spending is unlikely to rise much faster than income" because of the need to boost savings, he said. "Weak income growth will be an effective constraint on the pace of consumer spending." Companies continue to trim expenses, threatening further cuts in pay and benefits. Tenneco Inc., the world’s largest maker of vehicle-exhaust systems, temporarily lowered pay and hours worked to reduce labor costs by 10 percent. Earlier this year, the Lake Forest, Illinois-based company suspended contributions to employees’ 401(k) retirement accounts and cut pay for the top 50 executives.

Government assistance such as the "cash-for-clunkers" program will help postpone the inevitable increase in savings and slowdown in spending as more baby boomers approach retirement, said David Rosenberg, chief economist at Gluskin Sheff & Associates Inc. in Toronto. "Spending is in desperate need of gimmicks like cash-for- clunkers in order to grow on a short-term basis," he said. The program, which offers as much as $4,500 for trading in older, less fuel-efficient cars, ran through its $1 billion fund in about a week, and Congress is considering adding $2 billion. Auto industry data this week showed sales jumped to an 11.3 million annual pace last month, the highest level since September.

Mounting joblessness is among reasons that economists such as Rosenberg say will prompt Americans to save more. Unemployment, already at a 26-year high of 9.5 percent in June, may top 10 percent by early next year, according to the median estimate of economists surveyed by Bloomberg last month. Economists estimate that a Labor Department report at the end of the week will show employers cut an additional 328,000 workers from payrolls in July. That would bring the total loss of jobs since the recession began in December 2007 to 6.8 million.

The savings rate in June fell to 4.6 percent as incomes dropped, yesterday’s Commerce Department report showed. The rate, which reached a 14-year high of 6.2 percent the previous month, is likely to keep climbing, Rosenberg said. A rate as high as 15 percent can’t be ruled out, he said. "This is a different consumer than we had in the past 20 years," Rosenberg said. "People are going to increasingly be putting more money into cookie jars, rather than into buying more cookie jars."

It's All About Jobs!

What brings together the President of the United Steelworkers from Pittsburgh, a Corporate CEO now living in New York, and the former senior U.S. Senator from Michigan? It's all about jobs -- and the urgent need for millions of new ones. While President Obama has spoken forcefully about laying a new foundation for the economy, one that creates good jobs and rising incomes and that moves us from an era of borrow-and-spend to one where we save and invest and are able to produce more at home than we consume, we believe that the Administration still needs to address two glaring shortcomings in its economic program.

First is the failure, aside from the emergency restructurings of Chrysler and GM, to enact an all-of-government national manufacturing and industrial policy designed to simultaneously ensure the competitiveness of US-based businesses and grow high-value jobs in America. And second is the need to begin the promised reform of our trade policies with those economies, particularly China's, that do not play by the same rules we do and occasionally even cheat.

It is also by now very clear that the economic stimulus plan passed by Congress in February will not move us toward anything approaching full employment, since by the Administration's own estimate, the plan will "save or create" (but mostly just save) only 3.5 million jobs over two years, which are just a quarter of the 13.3 million jobs effectively lost since this recession began in December 2007 and just 12% of the workers already effectively unemployed.

Even in past recessions, the number of unemployed workers not included in the official Bureau of Labor Statistics monthly figure -- that is, workers who are either part-time of necessity, marginally attached, or have quit the labor force out of frustration -- has almost never exceeded a third or so of that official number. Now, however, there are nearly a million more uncounted unemployed than counted ones, making the total number an unprecedented 30.2 million workers, instead of the official 14.7 million, and the effective unemployment rate is a staggering 18.7%, instead of 9.5%.

When, 19 months after this recession began, nearly 19% of the nation's workers are still effectively unemployed and when even the nation's current full-time employees are working only an average of 33.1 hours a week, which are the fewest hours on record since the BLS began counting in 1964, it is clear that we are already deep into a jobless recovery. And by now it is just as clear that this jobless recovery will be particularly susceptible to a new downturn, because of the way it is already feeding back on itself, and that there will be little relief for the 47 out of 50 states, whose budgets have been absolutely blasted by falling tax revenues.

Significant and timely job retention and creation overall must be an urgent priority, certainly on a par with health care reform, but these dismal macro unemployment numbers tell only the big picture part of the jobs deficit story.

Importantly, we need to be just as worried about the fact that our economy has mostly hemorrhaged jobs in the very sector -- manufacturing -- that must grow in order for us to move permanently away from debt-financed consumption as the principal engine of economic growth.

And it is the current and now decades-long persistent manufacturing jobs collapse that unites the three of us as friends and as colleagues, despite coming from very different backgrounds. Just since this recession began, manufacturing has lost 13% of its workforce; manufacturing industries now represent a meager 11.7% of GDP; people working in manufacturing now account for only 8.7% of the jobs in the country; a quarter of the nation's 282,000 remaining manufacturing companies -- 90,000 in all -- are now deemed severely "at risk"; and we have run an average annual trade deficit in manufactured goods of more than $500 billion over the past five years.

Congress and the Administration, working together, need to immediately enact a robust industrial policy that puts American workers first and is comparable to the policies of our major trading partners. And then we need to integrate this policy with efforts to be the world's dominant manufacturer of green technologies and components, which offer us such enormous opportunities.

Perhaps the biggest example today, in dollar terms, of what the failure to have our own manufacturing and industrial policy has wrought is California, which has just confronted the largest annual budget deficit in the history of the Union. California would have had a dramatically smaller deficit, or maybe even none at all, if in the state manufacturing workers today simply represented the same share of total workers as they did in the year 2000, which was 12.8%. Instead, California lost, over this period, more than 400,000 manufacturing jobs which, after considering multiplier effects, would have benefited its budget on the order of $300 billion of cumulative income taxable wages.

The need for an elaborate American industrial policy was first widely observed as far back as the early 1980s, and by 1993 some in the Clinton Administration and especially some enlightened members of Congress tried to enact such a policy. Regrettably, against great opposition from the country's major multinational companies and the "free traders," they failed, and now 16 years later, we still don't have one.

Even if some in our political leadership today still don't understand and accept this basic imperative, America's main trade competitors sure do. Each of the other members of the G-20 has such a policy, and together they are using them now to great effect to resuscitate their broken economies and further weaken ours. Germany, Japan and South Korea are doing everything possible to preserve their significant manufacturing bases, while China, which consistently accounts for 60% of the US trade deficit in manufactured goods, is particularly accelerating its efforts to grow its manufacturing sector. We believe that two things are currently holding us back from having our own manufacturing and industrial policy -- and both need to be quickly disabused.

First, some in the Obama Administration, along with others of influence, wrong-headedly believe that one job is as good as another, whether it is in manufacturing or service. This is simply not true, and even the simplest comparison of the two sectors shows that:

- Compensation in manufacturing jobs is 20% greater than in non-manufacturing jobs;

- Service jobs do very little to help America's balance of trade, and mostly just move incomes around the country; and

- Manufacturing has by far the largest multiplier effect of all job sectors, creating 1.40 of additional economic activity for each 1.00 of direct spending, 2.5 other jobs on average for each job in it, and, at the upper end, 16 associated jobs for each high-tech manufacturing job.

Second, these same individuals assume, again with no supporting evidence, that new jobs associated with exported services will make up for past and future manufacturing job losses. One Administration official even said recently that America's export future resides in exporting "consulting and legal services, software, movies and medicine," which is simply impossible in dollar terms. In fact, in the future, high-quality service jobs are at least as much at risk of being offshored as are manufacturing jobs, as India and China are especially keen on seeing such jobs domiciled on their own shores.

In addition to throwing its full weight behind an all-of-government manufacturing & industrial policy, the Administration must also be willing to:

- "Pick winners" from Main Street and then support them, because all other developed nations and China do so every day, to great competitive effect. (Right now, the only "winners" being picked and seriously supported seem to be those residing on Wall Street, which is sadly ironic since it was largely these very same financial institution that just brought our economy to its knees.) The Administration has moved modestly in this direction with proposals to encourage private investment in wind and solar energy and by making certain modest targeted federal investments. However, it needs to do much more if we are to create new comparative advantages in these and other industries.

- Fund a 10-year (not the current two-year) program of significant public investment to upgrade and rebuild our nation's infrastructure, which will provide the much-needed foundation for higher-value added production and advanced business services.

- Adopt "Buy American" requirements related to all federal procurement, which now makes up about 20% of the US economy. America appears to be the only nation among the major developed nations and China without a significant "buy domestic" procurement program, and we need one desperately for our own economic recovery and global competitiveness.

- Enact major corporate tax reform to incent corporations to create jobs here and to eliminate the current incentives for them to relocate manufacturing and service jobs abroad. This reform should include reducing the corporate income tax and payroll tax and moving to a value-added-tax or VAT to replace that lost revenue.

- Make loans and credit facilities readily available to the nation's small and medium size businesses and manufacturers, which desperately need them while the likes of Goldman Sachs and the major banks are succoring off of US Government guarantees and TARP monies but not lending to these smaller companies. (How foolish indeed was it to let CIT, which every day loans money to 950,000 small and medium size businesses, essentially fail for lack of an "angel" in the Treasury Department, while Treasury continues to resuscitate but barely reform the errant Wall Street banks that precipitated this financial crisis.)

However, not even a broad new national industrial policy can right our economic ship without there also being complementary trade policies that prevent other economies from gaining unfair competitive advantages. The Administration and Congress also need to immediately move away from our past decades of misguided trade policies and demand trade agreements that have meaningful labor and environmental standards and forbid illegal subsidies and currency manipulation. At the same time, we need to dispense with "one size fits all" trade agreements that ignore significant differences in levels of development, forms of government, and reciprocity.

But most immediate and most important, we still need the fundamental reworking of our trade relationship with China that was promised during the Campaign, which despite two major Administration encounters already with them has yet to occur. China's massive trade surplus with the United States -- a staggering $277 billion of manufactured goods just in 2008 -- is mostly the result of its severely undervalued currency, massive legal and sometimes illegal subsidies to its own manufacturers, and very aggressive policies to induce foreign corporations to shift their production facilities and technology to it. These policies have already cost us millions of jobs, and they will keep costing us jobs until they are fixed.

Challenging China over its unfair trade practices is not just necessary for the future of US manufacturing jobs -- it is also critical for the world economy. The global economy simply can't function if the third-largest individual economy runs current account surpluses on the order of 8 to 10% of GDP, as China has done consistently for the past few years. These are truly unprecedented times, and thus looking at past business cycles and responses for the answers is likely to be of only very limited relevance and utility, as too many in the Administration and Congress seem to do by ideological reflex.

Instead, we need, as soon as possible, an Emergency National Summit on Manufacturing, to be attended by relevant Cabinet officers, the bipartisan leadership of both Houses of Congress, and a small number of the top corporate and labor leaders on this issue. We also need an activist executive branch and Congress willing both to turn around the excessive laissez faire and deregulatory approaches of the last eight and, in some cases, the last thirty years, and to enact that national manufacturing & industrial policy we are calling for.

Our national goals, in the medium term, must be to near fully employ those 30 million currently unemployed American workers, and in the process to more than double the number of Americans working in manufacturing, which is the least amount needed to get our economy back on track sustainably. It's all about jobs -- whatever it takes!

The Beginning of the End for Treasury Bonds

On Tuesday, Treasury suffered its worst five-year auction in history. Yet that news barely made a headline. It’s not the first time Treasury has struggled to sell its paper...and they're certainly not alone. The Germans – among several other Euro-zone credits – have struggled to auction their debt since last October with four failed or reduced bond auctions (even the Chinese endured a failed bond auction this July).

That’s almost mind-boggling...especially since I’d consider the Germans the best government credit in the world, possibly along with the Swiss and Norwegians. The United States, like several other European governments, is struggling to sell a truckload of Treasury’s this year. Investors are advised that this slow bleed can easily magnify into a full-blown crisis over the next few years if the global economy fails to recover. But government debt has enjoyed a great run for the last thirty years...

From 1981-82 until December 2008 Treasury bonds enjoyed a secular bull market as interest rates collapsed from a Volcker Fed peak of 20% in 1981 to 2.25% in December of last year. Zero-coupon bonds – long-term bonds on steroids – have earned big double-digit gains over the last 28 years as rates tumbled, handily outpacing most global stock markets. But the big bond bull market is over.

Faced with an unprecedented funding gap thanks to the worst credit collapse since the 1930s and plunging tax revenues, the United States is now issuing more debt than ever to finance its expenditures. About $2 trillion dollars is estimated to be auctioned this fiscal year. And what it can’t finance, Treasury simply monetizes vis-à-vis the Federal Reserve, as we all already know, through the process of "quantitative easing." Several other central banks are doing the same thing this year, including the Swiss National Bank and The Bank of England.

Yet nobody has a debt the size of America’s. Deficits are clearly out of control with no political resolve to reduce spending. At some point, a major lenders’ strike looms as foreigners balk at financing this paper. If that happens, the United States could be forced to impose a deficit-financing tax or a VAT consumption tax to finance its explosive debt and the interest required to service outstanding Treasury bonds. The Chinese are stuck with about 40% of this paper, the Japanese about 25% and the British about 10%. Rightfully concerned, the biggest holders of U.S. Treasury debt outside of Japan and England have increased their rhetoric lately, as they grow nervous about their declining dollars. The Chinese and the Russians are the most vocal, fed-up with dollar depreciation.

Last week, Treasury was successful in selling its tranche of seven-year Treasury bonds. But for the second time in a week, Treasury attracted poor demand for the sale of five-year and two-year notes. That raises the cost for Treasury as it relies on the Fed to absorb unwanted notes.

Five Reasons the Market Could Crash This Fall

With all this blather about “green shoots” and economic “recovery” and new “bull market,” I thought I’d inject a little reality into the collective financial dialogue. The following are ALL true, all valid, and all horrifying…Enjoy.

1) High Frequency Trading Programs account for 70% of market volume

High Frequency Trading Programs (HFTP) collect a ¼ of a penny rebate for every transaction they make. They’re not interested in making a gains from a trade, just collecting the rebate.

Let’s say an institutional investor has put in an order to buy 15,000 shares of XYZ company between $10.00 and $10.07. The institution’s buy program is designed to make this order without pushing up the stock price, so it buys the shares in chunks of 100 or so (often it also advertises to the index how many shares are left in the order).

First it buys 100 shares at $10.00. That order clears, so the program buys another 200 shares at $10.01. That clears, so the program buys another 500 shares at $10.03. At this point an HFTP will have recognized that an institutional investor is putting in a large staggered order.

The HFTP then begins front-running the institutional investor. So the HFTP puts in an order for 100 shares at $10.04. The broker who was selling shares to the institutional investor would obviously rather sell at a higher price (even if it’s just a penny). So the broker sells his shares to the HFTP at $10.04. The HFTP then turns around and sells its shares to the institutional investor for $10.04 (which was the institution’s next price anyway).

In this way, the trading program makes ½ a penny (one ¼ for buying from the broker and another ¼ for selling to the institution) AND makes the institutional trader pay a penny more on the shares.

And this kind of nonsense now comprises 70% OF ALL MARKET TRANSACTIONS. Put another way, the market is now no longer moving based on REAL orders, it’s moving based on a bunch of HFTPs gaming each other and REAL orders to earn fractions of a penny.

Currently, roughly five billion shares trade per day. Take away HFTP’s transactions (70%) and you’ve got daily volume of 1.5 billion. That’s roughly the same amount of transactions that occur during Christmas (see the HUGE drop in late December), a time when almost every institution and investor is on vacation.

HFTPs were introduced under the auspices of providing liquidity. But the liquidity they provide isn’t REAL. It’s largely microsecond trades between computer programs, not REAL buy/sell orders from someone who has any interest in owning stocks.

In fact, HFTPs are not REQUIRED to trade. They’re entirely “for profit” enterprises. And the profits are obscene: $21 billion spread out amongst the 100 or so firms who engage in this (Goldman Sachs (GS) is the undisputed king controlling an estimated 21% of all High Frequency Trading).

So IF the market collapses (as it well could when the summer ends and institutional participation returns to the market in full force). HFTPs can simply stop trading, evaporating 70% of the market’s trading volume overnight. Indeed, one could very easily consider HFTPs to be the ULTIMATE market prop as you will soon see.

TAKE AWAY 70% of MARKET VOLUME AND YOU HAVE FINANCIAL ARMAGEDDON.

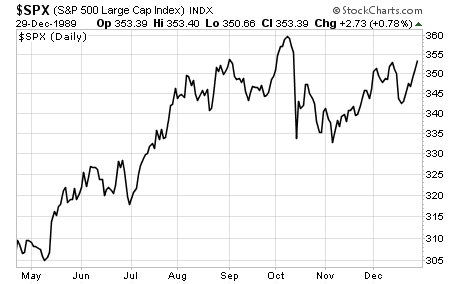

2) Even counting HFTP volume, market volume has contracted the most since 1989

Indeed, volume hasn’t contracted like this since the summer of 1989. For those of you who aren’t history buffs, the S&P 500’s performance in 1989 offers some clues as what to expect this coming fall. In 1989, the S&P 500 staged a huge rally in March, followed by an even stronger rally in July. Throughout this time, volume dried up to a small trickle.

What followed wasn’t pretty.

Anytime stocks explode higher on next to no volume and crap fundamentals you run the risk of a real collapse. I am officially going on record now and stating that IF the S&P 500 hits 1,000, we will see a full-blown Crash like last year.

3) This Latest Market Rally is a Short-Squeeze and Nothing More

To date, the stock market is up 48% since its March lows. This is truly incredible when you consider the underlying economic picture: normally when the market rallies 40%+ from a bear market low, the economy is already nine months into recovery mode. Indeed, assuming the market is trading based on earnings, the S&P 500 is currently discounting earnings growth of 40-50% for 2010. The odds of that happening are about one in one million.

A closer examination of this rally reveals the degree to which “junk” has triumphed over value. Since July 10th:

- The 50 smallest stocks have outperformed the largest 50 stocks by 7.5%.

- The 50 most shorted stocks have beaten the 50 least shorted stocks by 8.8%.

Why is this?

Because this rally has largely been a short squeeze.

Consider that the short interest has plunged 72% in the last two months. Those industries that should be falling the most right now due to the world’s economic contraction (energy, materials, etc.) have seen the largest drop in short interest: Energy -90%, Materials -94%, Financials -86%.

In simple terms, this rally was the MOTHER of all short squeezes. The fact that it occurred on next to no volume and crummy fundamentals sets the stage for a VERY ugly correction.

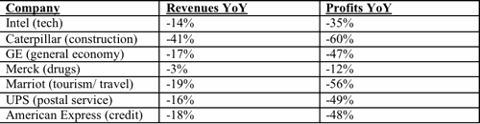

4) 13 Million Americans Exhaust Unemployment by 12/09

A lot of the bull-tards in the media have been going wild that unemployment claims are falling. It strikes me as surprising that this would be true given the fact that virtually every company that posted the alleged “awesome” earnings in 2Q09 did so by laying off thousands of employees:

- Yahoo! (YHOO) will cut 675 jobs.

- Verizon (VZ) just laid off 9,000 employees.

- Motorola (MOT) plans to lay off 7,000 folks this year.

- Shell (RDS.A) has laid off 150 management positions (20% of management).

- Microsoft (MSFT) plans to lay off 5,000 people this year.

So unemployment claims are falling, that means people are finding jobs right? Wrong. It means that people are exhausting their unemployment benefits. When you consider that there are 30 million people on food stamps in the US (out of the 200 million that are of working age: 15-64) it’s clear REAL unemployment must be closer to 16%.

And they’re slowly running out of their government lifelines.

The three million people who lost their jobs in the second half of 2008 will exhaust their benefits by October 2009. When you add in dependents, this means that around 10 million folks will have no income and virtually no savings come Halloween.

Throw in the other four million who lost their jobs in the first half of 2009 and you’ve got 13 million people (counting families) who will be essentially destitute by year-end.

How does this affect the stock market?

The US consumer is 70% of our GDP. People without jobs don’t spend money. People who are having to work part-time instead of full-time (another nine million) spend less money than full time employees. And people who are forced to work shorter work weeks (current average is 33, an ALL TIME LOW), have less money to spend.

Wall Street makes a big deal about earnings (earnings estimates, earnings forecast, etc), but when it comes to economic growth, sales are the more critical metric. Companies can increase profits by reducing costs temporarily, but unless actual top lines increase, there is NO growth to be seen. No revenue growth means no hiring, which means no uptick in employment, which means greater housing and credit card defaults, greater Federal welfare (unemployment, food stamps, etc), etc.

So how will corporate profits perform as more and more consumers become part-time, unemployed, or destitute? Well, so far profits have been awful. And that’s BEFORE we start seeing millions of Americans losing their unemployment benefits.

click to enlarge

With the S&P rallying on these already crap results… what do you think will happen when reality sets in during 3Q09?

5) The $1 QUADRILLION Derivatives Time Bomb

Few commentators care to mention that the total notional value of derivatives in the financial system is over $1.0 QUADRILLION (that’s 1,000 TRILLIONS).

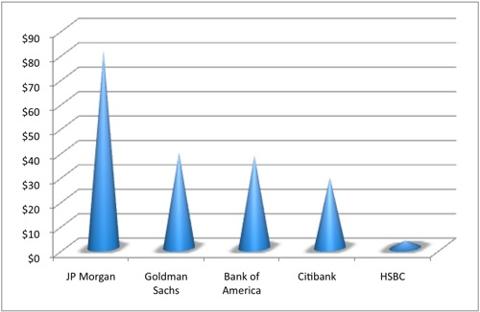

US Commercial banks alone own an unbelievable $202 trillion in derivatives. The top five of them hold 96% of this.

By the way, the chart is in TRILLIONS of dollars:

As you can see, Goldman Sachs alone has $39 trillion in derivatives outstanding. That’s an amount equal to more than three times total US GDP. Amazing, but nothing compared to JP Morgan (JPM), which has a whopping $80 TRILLION in derivatives on its balance sheet.

Bear in mind, these are “notional” values of derivatives, not the amount of money “at risk” here. However, if even 1% of the $1 Quadrillion is actually at risk, you’re talking about $10 trillion in “at risk.”

What are the odds that Wall Street, when allowed to trade without any regulation, oversight, or audits, put a lot of money at risk? I mean… Wall Street’s track record regarding financial instruments that were ACTUALLY analyzed and rated by credit ratings agencies has so far been stellar.

After all, mortgage backed securities, credit default swaps, collateralized debt obligations… those vehicles all turned out great what with the ratings agencies, banks risk management systems, and various other oversight committees reviewing them.

I’m sure that derivatives which have absolutely NO oversight, no auditing, no regulation, will ALL be fine. There’s NO WAY that the very same financial institutions that used 30-to-1 leverage or more on regulated balance sheet investments would put $50+ trillion “at risk” (only 5% of the $1 quadrillion notional) when they were trading derivatives.

If Wall Street did put $50 trillion at risk… and 10% of that money goes bad (quite a low estimate given defaults on regulated securities) that means $5 trillion in losses: an amount equal to HALF of the total US stock market.

This of course assumes that Wall Street only put 5% of its notional value of derivatives at risk… and only 10% of the derivatives “at risk” go bad.

Do you think those assumptions are a bit… low?

Bank of England warns recession is 'deeper than previously thought' as it extends 'printing money' scheme by £50 billion

Hopes for a quick economic rebound crumbled today after the Bank of England dramatically expanded its controversial money-printing operation. In a move that stunned the City, the Bank voted to pump an extra £50 billion into the markets over three months - a rate of over half a billion pounds a day. The official interest rate was also pegged at an all-time low of 0.5 per cent, as the Bank warned the recession was proving ‘deeper than previously thought.’ Today’s decision blindsided many City analysts and traders, because recent figures on housing and business activity pointed to a tentative recovery.

Sterling slid as much as 1 per cent to $1.6826 against the dollar, while the FTSE 100 index leaped as much as 1.6 per cent before later losing some ground. But while the Bank acknowledged there are signs that a ‘trough in output is close at hand,’ there are no signs Governor Mervyn King is letting up in his efforts to battle the recession. A statement pointed the finger squarely at Britain’s banks, saying they are continuing to reduce the supply of credit to hard-pressed businesses. This will suppress the economy’s potential to grow, the Bank argued. Financial conditions remain ‘fragile,’ it added, and interest rates on loans remain ‘elevated’.

‘The need for banks to continue repairing their balance sheets is likely to restrict the availability of credit, and past falls in asset prices and high levels of debt may weigh on spending,’ the statement said. Economist Danny Gabay of Fathom Financial Consulting said: ‘This is not a positive sign about the economy. It is rather an honest reflection of how parlous a state the UK is in at the moment.’ While the City welcomed the additional cash, the Bank’s so-called Quantitative Easing (QE) programme is hugely controversial.

Some analysts fear creating such large sums of fresh money could ultimately lead to Weimar Republic-style hyper-inflation - although the Bank today insisted the credit crunch is ‘bearing down’ on price growth. And the vast bulk of the new cash is being used to purchase government bonds, leading to accusations that the Bank of England is tacitly helping the Treasury finance its own deficit. ‘They are leaving themselves open to that charge,’ said Mr Gabay. ‘It is becoming easier and easier to lay the charge at their door that this is simply a very elaborate smokescreen.’

Conservative Treasury spokesman Philip Hammond said: ‘The decision to continue QE is an attempt to counter the contraction in the economy in the second quarter and the continuing slide in lending to businesses. But every extension of QE also adds to the longer term risk of fuelling inflation when the economy recovers.’ Before today’s decision, the majority of experts had believed the Bank’s money-creation scheme was nearly finished - or that the Bank would at least pause for a few months to survey the impact of its efforts to date. However, Alan Clarke of BNP Paribas said the Bank is now unlikely to stop at £175 billion.

He said risks of outright deflation are so dire that Mr King may ultimately have to create £300 billion of new money - equal to the entire national output of Belgium. Mr Clarke said: ‘It is the right decision to expand this scheme. There are serious downside risks for (the economy and inflation). Ultimately we may hit £200 billion or even £300 billion.’ Under the QE scheme, the Bank purchases government and corporate bonds off City firms and pays for them with newly created money. The hope is that this should boost the amount of cash flowing around the economy and bolster bank lending.

It should also suppress the interest rates on gilts - the main form of government debt - and as a consequence push down borrowing costs across the economy. Yet as the Bank’s own statement acknowledged today, the scheme has thus far failed to bring an end to the credit crunch. Indeed, there is strong evidence that banks are hoarding cash at their Bank of England current accounts rather than lending it to their consumers. The Bank’s own figures show that lending to businesses tumbled by a record £14.7 billion between April and June - the biggest fall since records began.

And earnings figures from Lloyds Banking Group on Wednesday showed the firm is continuing to reduce the quantity of credit it has offered to businesses. With firms and families also trying to borrowing, and with joblessness rising quickly, the economic outlook remains bleak , experts said. ‘Households remain under severe stress,’ said James Knightley of ING bank said. ‘The pick-up in activity will be more muted than previous recovery periods - especially with credit being so heavily restricted.’

Despite Bailouts, Business as Usual at Goldman

Lloyd C. Blankfein has a story about the cataclysm that nearly brought down all of Wall Street. It goes something like this: One by one, lesser banks were swept away by the financial storm of 2008. And as the floodwaters rose, no one, not even Goldman Sachs, seemed safe. The question, in Mr. Blankfein’s eyes, was how high the water would rise. But Washington stepped in with all those bailouts before the surge reached Goldman.

The story, which was recounted by several friends and colleagues, represents a sobering private admission from Mr. Blankfein, Goldman’s chief executive. Publicly, it is a different story. Now that Goldman is minting money again, the bank insists that it was never in any real danger. Mr. Blankfein, in an e-mail message this week, disputed his private account, saying Goldman’s survival was never in doubt. Other Goldman executives reject the notion that the bank was rescued at all.

"We did not have a near-death experience," said Gary D. Cohn, Goldman’s president. The government saved the financial industry as a whole, but it did not save Goldman Sachs, he said. Rarely has the view from inside a company been so at odds with the view outside it. Could Goldman Sachs have lived if all those other giant banks had failed? Could it alone survive financial Armageddon?

Goldman executives are dismissive, even defiant, when critics argue that the bank is playing a heads-we-win, tails-you-lose game with American taxpayers. And yet the questions keep coming. Last month the story of Goldman’s postcrisis success — and conspiracy theories surrounding it — leapt from the business pages to the cover of Rolling Stone. The idea that nothing has changed for Goldman Sachs strikes many outsiders as absurd. In this era of mega-bailouts, Goldman is widely perceived, on Wall Street and in Washington, as too big and important to fail. If its bets pay off, Goldman profits and its employees get rich. If its bets go bad, ultimately taxpayers will have to pick up the bill.

"Many observers on the market believe that Goldman and others of its size now have a free insurance policy," said Elizabeth Warren, the chairwoman of the Congressional oversight panel for the $700 billion bailout fund. "Whether they do or not is less important than the fact that many in the market believe they do. That means at some level Goldman is playing with the American taxpayers’ future." Is Goldman gambling at America’s expense? Of course not, Mr. Cohn said. Should it change its business strategy in the wake of the gravest financial crisis since the Depression? No. Is Goldman taking big risks to make big profits? Courting more outrage over Wall Street pay with its plans to pay lavish bonuses? Throwing its weight around in Washington? No, no, no.

Goldman executives dispute suggestions that high-stakes market gambles are behind its big profits — $3.4 billion in the second quarter. And they are dumbfounded when people like Ms. Warren suggest companies like Goldman, which paid back its bailout money last month, now operate with an implicit taxpayer guarantee. After so many wrenching changes on Wall Street and in the economy, it might come as a surprise that the post-bailout Goldman is virtually indistinguishable from the pre-bailout one.

The bank has strengthened its capital base and reduced its use of leverage — the borrowed money that turbo-charges profits on the way up and can prove devastating on the way down. But Goldman sees little reason to change the way it does business. In fact, its executives are surprised that anyone would suggest it should. Even Goldman’s conversion to a traditional banking company at the height of the crisis — a step many predicted would clip Goldman’s gilded wings — has been deftly sidestepped.

It is, in other words, business as usual at Goldman — and what a business it is. Quarter after quarter, Wall Street executives scour Goldman’s results hoping to figure out how the bank makes so much money. Mr. Cohn and other executives, in recent interviews, sketched the broad outlines of an answer. Mr. Blankfein declined to be interviewed for this article. During the second quarter, Goldman bet, correctly, that the financial markets would calm down. It wagered that market volatility would decline and that certain securities tied to the troubled home mortgage market would revive. Its securities underwriting business bounced back too.

A vast majority of profits came from trading on behalf of clients like big mutual funds, pension funds and endowments, rather than from staking Goldman’s own money in the markets, Mr. Cohn said. Proprietary trading now accounts for about 10 percent of profits, down from 20 percent in 2005. Goldman dominated institutional trades linked to changes in a closely watched stock market index, the Russell 2000, and is benefiting because old competitors like Bear Stearns and Lehman Brothers are no longer around. "We don’t have to outsmart the market today," said Mr. Cohn. "We just have to do what our clients want us to do."

But unlike some of its rivals, Goldman is not shy about taking risks. The bank stood to lose as much as $245 million on any given day during the second quarter, based on a common measure known as value at risk, or VAR. That was up from $184 million in mid-2008. But VAR captures only about a fifth of Goldman’s market risks and excludes investments that are difficult to value. "Our risk appetite continues to grow year on year, quarter on quarter, as our balance sheet and liquidity continue to grow," Mr. Cohn said. He and other executives say Goldman carefully manages its risks, which, for the most part, it has.

Goldman’s latest quarterly disclosures to the Securities and Exchange Commission, filed on Wednesday, provide another glimpse into the bank’s activities. Aided by cheap credit, Goldman generated more than $100 million in daily revenue from trading on 46 separate days during the second quarter — a record. Since late 2007, Goldman has reduced its exposure to illiquid investments, which can pose dangers because they are traded so infrequently, by 8 percent. Its total exposure to these so-called Level 3 assets still stood at $50.4 billion. While VAR is up, other risk measures were down, and the bank’s capital base has grown significantly. Lately, Goldman has been taking more risks in stocks, but fewer in fixed income, currency and commodities.

Some of Goldman’s recent practices are drawing scrutiny from government officials. In its filing Wednesday, Goldman said various government agencies had inquired about its compensation practices, as well as its role in the market for credit derivatives, which fueled the financial crisis. But over all, the events of the past year have not changed the way Goldman views or manages the risks it takes, said David A. Viniar, Goldman’s chief financial officer. "There are a few business units that are taking a little more risk. Most are taking less," Mr. Viniar said.

Mr. Cohn, Goldman’s president, acknowledges his bank is systemically important, meaning that its failure would probably send financial shock waves around the world. But he said that the implications of this status were unclear and that Goldman had no government backing. David A. Moss, a professor at Harvard Business School, disagrees. He says the painful lessons of the financial crisis show the federal government now stands behind all systemically important financial institutions.

"We’re in a situation where we’ve extended important guarantees, both explicit and implicit, to almost all major financial institutions, yet we don’t have the regulations in place to control the excessive risk-taking that could result," said Mr. Moss, the author of "When All Else Fails: Government as the Ultimate Risk Manager." In any case, Goldman has certainly helped itself to government programs that were put in place to stabilize the financial industry. For instance, the bank has issued billions of dollars of bonds guaranteed by the Federal Deposit Insurance Corporation. Since March it has sold $3.4 billion worth without government backing.

And Goldman’s conversion to a bank holding company, executed at the height of the crisis, gives the bank access to money from the Federal Reserve. In exchange, Goldman had to increase its capital, reduce its leverage and accept Fed oversight. Many analysts predicted that switch would force Goldman to rein in riskier businesses like proprietary trading and parts of its commodities operation. But Goldman has largely carried on as usual. It has received standard exemptions that give it two years to comply with federal regulations governing bank holding companies.

"They are very happy to go back to a business model that year-in and year-out has made them untold wealth," said John C. Coffee, a professor of securities law at Columbia University. Mr. Cohn concedes that Goldman, along with other banks, bears some responsibility for the financial crisis. "There’s no performance angel in this," he said. But he bristles at all the fingers being pointed at Goldman. "Every bank has to accept a degree of responsibility, but it sometimes feels like we’re being disproportionately blamed," he said.

BNP Paribas bonuses spark anger in France

French bank BNP Paribas said Wednesday it expected to pay out over one billion euros in bonus payments to traders, executives and some 17,000 staff in its investment banking divisions this year. A spokesman told AFP that an average of 59,000 euros (85,000 dollars) per person was being anticipated, but he said that the bank would "scrupulously respect" guidelines agreed by Group of 20 major economies in April. The scale of the bonuses sparked anger in France when revealed by the left-wing Liberation daily newspaper, with Socialist opposition leader Martine Aubry issuing a statement that termed the amount "a veritable scandal."

Industry Minister Christian Estrosi told French radio that France's central bank will "supervise" the payments in the interests of "transparency and guarantees" that rules drawn up by political leaders in London are adhered to.

But the bank said it had to offer renewed bonuses and was "worried that many of our rivals, notably in the United States, are no longer applying the rules" the spokesman said have been in force internally since last year.

The spokesman said G20 leaders did not suppress bonus payments, but agreed to clamp down on guaranteed bonuses over multiple calendar or financial years, or their calculation on net earnings after write-downs on risk.

The return of the big bonus culture for top banking executives will trigger new "dramas" in the financial sector if tougher regulation is not applied, International Monetary Fund chief Dominique Strauss-Kahn said last month.

"I am appalled at what I see," the Fund's managing director said in reference to multi-billion-dollar bonus provisions set aside at the likes of Wall Street's Goldman Sachs and top London firms. French banking rivals Societe Generale were nearly made insolvent last year by huge exposure on trading positions associated with trader Jerome Kerviel, and it said Wednesday that it would heed the lessons of that experience. "When we come to evaluate remunerations, we will take into account not only results, but also behaviour," said chief executive Frederic Oudea. "We will take into account (acceptable) parameters as much as risk," he added.

Max Keiser on France24 - Criminal Banking Syndicates

US firm closes down factory after French workers beat up boss

US electronics firm Molex Inc announced on Wednesday its factory in Villemur-sur-Tarn in southwestern France was temporarily closed down to reassess security after a labour dispute turned violent. Angry French workers facing lay-offs beat up a senior American executive after he visited the factory, an executive said on Wednesday. Union members said workers had only jostled and thrown eggs at development director Eric Doesburg on Tuesday night when he left the factory in Villemur-sur-Tarn in southwestern France, which Molex plans to close down.

But director-general Markus Kerriou said Doesburg had to be escorted away by bodyguards after he was "really beaten" by about 40 workers. "A medical examination confirmed the injuries, and we’ve decided to file a lawsuit," Kerriou told Reuters. Workers at the factory have been on strike since July 7 over its planned closure but Molex said there would be no further talks over a possible re-start. A union leader at Molex said only "a few small incidents" occurred on Tuesday night. He did not say whether he was present at the events.

"Essentially, egg-throwing and maybe a light scuffle. But no one was injured," Guy Pavan, a member of trade union CGT, told Reuters. "Egg-throwing has never caused serious injuries." Labour disputes in France, which has a strong tradition of protest, have been escalating over the past few months as the economic crisis forces one factory after another to shut down.

After a spate of "bossnappings" in which workers locked up their bosses, protesters in several towns threatened to blow up their factories unless their demands for better lay-off terms were met. Industry Minister Christian Estrosi said a scheduled meeting with Doesburg over the future of the unit had to be cancelled because of the director’s injuries. "(The minister) strongly condemns these acts of violence committed by a minority, which are a disservice to the workers’ cause and make the negotiations even more difficult," the ministry said in a statement.

"Morning Meeting" Panel Uses Masterpiece Theater To Explain Credit Rating Agencies Corruption

A key actor in causing the financial crisis were the credit rating agencies. In a setup doomed to cause major problems, rating agencies were paid by banks to rate the mortgage packages the banks wanted to sell. By design this would give the agencies more incentive to rate loan packages higher than they deserved, otherwise the banks would just take their business, and the fees they paid, to another rating agency. Perhaps due to a feeling that reform of the agencies is not getting enough attention, the panel at "Morning Meeting" decided to try to change that with some Masterpiece Theater, acting out the corruption inherent in the ratings system.Visit msnbc.com for Breaking News, World News, and News about the Economy

SEC chief in call for funding shake-up

The US Securities and Exchange Commission should fund itself directly from industry fees, a system that would allow it to tackle more complex investigations and invest more in technology and skilled people, Mary Schapiro, its chairman, told the Financial Times. The SEC already rakes in more than $1bn annually in registration and transaction fees but, unlike other US financial regulators, cannot spend any of it without going to Congress each year to get its budget approved. That process has made it difficult to plan ahead and invest in multi-year information-technology projects.

"Self-funding has been discussed over the years but I think it may now well be the moment," Ms Schapiro said. "Some stability in funding would be an enormous benefit because it would help with long-term planning in such areas as technology and staffing." Her comments, which come as Congress and the Obama administration are redesigning the US regulatory framework, highlight the SEC's perennial resource problems. The agency oversees everything from mutual funds to credit ratings agencies but has seen its budget decline or stay flat in recent years.

Now, the SEC is under tremendous pressure to be more aggressive after oversight failures that include missing Bernard Madoff's investment fraud. In recent days, the SEC has reached high-profile settlements with Bank of America and General Electric, and it is also likely to gain new responsibilities in the overall regulatory revamp, including oversight of the credit derivatives market. "Self-funding will help us to avoid periods of drought," Ms Schapiro said. "Think about what the markets were doing in terms of growth and innovation at the same time the SEC was in a hiring freeze."

US banking regulators, including the Federal Deposit Insurance Corporation and the Federal Reserve, can use whatever they collect in fees, deposit insurance premiums and interest income. Similarly the UK Financial Services Authority is entirely self-funded. The SEC, by contrast, expects to collect $1.3bn in 2009 but it may only spend the $960m authorised by Congress. For 2010, the administration has asked for an SEC budget of $1.026bn, while the SEC expects to collect $1.5bn in fees. Top Democrats in Congress are divided. Paul Kanjorski, who chairs a subcommittee on capital markets, recently said Congress should consider "moving the agency outside of the appropriations process," but Barney Frank, who chairs the House Financial Services Committee said he did not "entirely agree" with the idea.

America needs a single bank regulator

by Mark Warner

In recent weeks our financial markets have shown signs of recovery thanks to unprecedented action to stabilise markets and stimulate the economy. Yet this crisis has many distressing qualities. Perhaps most dispiriting is the sense that we have seen this movie before, and it wasn’t very good the first time, either. When President Bill Clinton came into office in the early 1990s, the US faced, among other challenges, waves of thrift and bank failures, huge hits to its deposit insurance system, and enormous piles of "toxic assets" in need of taxpayer-financed liquidation. It was a colossal regulatory failure.